The Pharma Sector Knows No Winter: Eight Key Investment Themes for 2019

Editor’s Note: This article is republished from 36Kr, authored by Mengxiangjia Caicai (WeChat: windyhz)

In 2018, the pharmaceutical sector witnessed numerous landmark events: the Nobel Prize in Physiology or Medicine was awarded to immunotherapy; domestically developed PD-1 inhibitors entered the market, with Junshi Biosciences and Innovent Biologics emerging as frontrunners; investment deals in innovative drugs reached a historical high of 23 transactions; and the STAR Market, designed to encourage technological innovation, was on the horizon. Undoubtedly, the scientific community, industry players, and capital markets all hold strong optimism for the future of new drugs and novel therapies.

So, what exactly does the future hold for new drugs and novel therapies? What new technologies will be “Created in China,” and which innovations will cure ailments that have plagued humanity for years, pushing the upper limits of human lifespan? In this article, we attempt to share our perspective on this sector by addressing the following questions:

What were the trends in each sub-sector in 2019? Where lay the opportunities?

Which sectors are worth watching for new drugs and new therapies?

To what extent have leading companies achieved?

Share 36Kr's Industry Landscape Map

From which dimensions should project quality be evaluated?

What happened in the new drug and novel therapy industry in 2018? Where do the opportunities lie in this sector in 2019?

At the outset of this article, we will directly share industry trends in new drugs and novel therapies.

1. In the field of immunodiagnostics, chemiluminescence technology is gradually replacing enzyme-linked immunosorbent assay (ELISA), becoming the major direction for technological advancement in the industry. This market remains dominated by overseas giants. In the future, we will focus on leading companies specializing in cutting-edge chemiluminescence technologies to assess whether import substitution can occur in the high-end immunodiagnostics market.

2. The domestic molecular diagnostics market is characterized by rapid growth (with a compound annual growth rate of approximately 30%), yet it remains in its nascent stage, featuring a small market size, a fragmented competitive landscape, and relatively low penetration by overseas giants. Furthermore, molecular diagnostic technologies are not yet mature; many clinical applications have yet to be developed, preventing them from becoming mainstream techniques. Consequently, there remains substantial room for market expansion. This industry landscape presents a favorable opportunity for the development of domestic startups.

3. The upstream segment of the gene sequencing industry holds significant bargaining power, while midstream and downstream players generally lack cost control. Therefore, it is crucial for companies in this sector to strategically position themselves with regard to upstream resources.

4. The POCT industry still has significant growth potential; however, due to relatively low technical barriers, players face intense homogeneous competition, and the domestic market exhibits a high rate of substitution with domestically produced alternatives.

5. Regarding AI-driven pharmaceutical R&D projects, we believe that the key to assessing project quality lies in evaluating the quality and accuracy of the underlying databases, as well as determining whether major pharmaceutical companies are willing to pay for the technology. We favor companies that focus on niche areas; players should deeply specialize in a specific segment of the pharmaceutical R&D process.

6. Intense homogenized competition and low industry concentration characterize the CRO sector, with top-tier enterprises achieving high profitability. We believe that the current penetration rate of the CRO industry is relatively low; however, the sector is poised for positive growth, with CRO penetration expected to gradually rise to levels seen in developed countries (exceeding 30%).

7. For innovative pharmaceutical companies, Me-too/Me-better drugs should remain the dominant theme over the next 5–10 years.

8. The landscape of tumor immunotherapy is such that CAR-T therapies are at the forefront, cancer vaccines represent an emerging trend, and the industry focus on PD-1 should extend beyond R&D to encompass market strategy.

After sharing the industry trends for 2019, we turn our attention to the key players in the sector, conducting a comprehensive review of the entire business landscape.

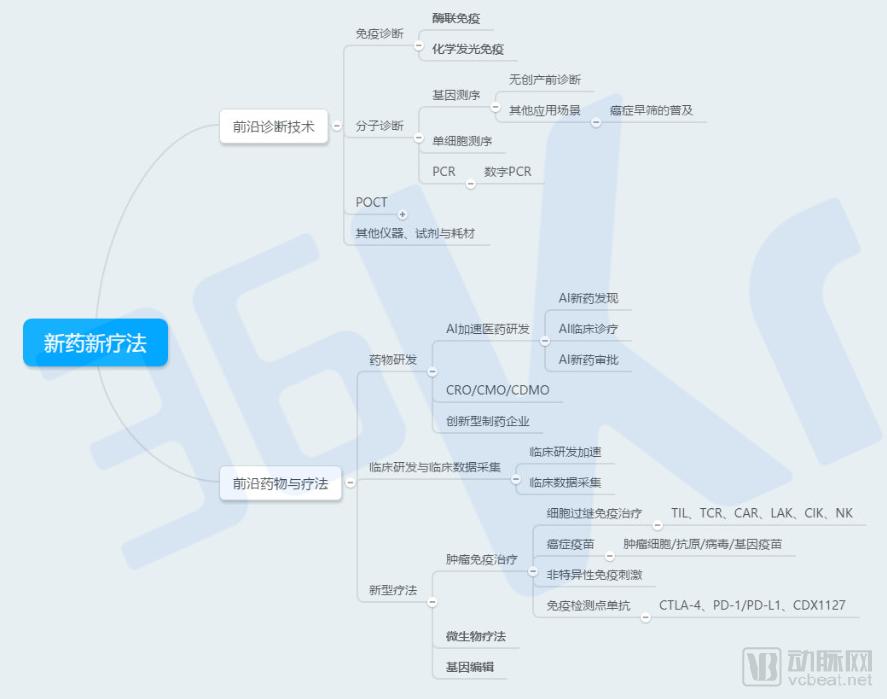

The upstream and downstream segments of the industrial chain for new drugs and novel therapies are highly interconnected and mutually influential. A clear approach to categorization is to distinguish between diagnosis and treatment.

The diagnostics sector encompasses diagnostic technologies, instruments, reagents, consumables, and more, with investment opportunities primarily concentrated in in vitro diagnostics (IVD). Although IVD is classified as medical devices in many jurisdictions, we wish to discuss it here given its significant integration of diagnostic services and technologies. The IVD field comprises several subsectors, among which the following three stand out:

Immunodiagnostics: Chemiluminescence technology is a new growth driver; watch for import substitution in the high-end immunodiagnostics market.

Molecular Diagnostics: The sector is in its early stages, with rapid market growth and a fragmented competitive landscape, presenting a favorable window for the development of domestic startups;

POCT: The domestic market is relatively underserved, with fragmented competition, presenting new opportunities.

Regarding the treatment segment, the primary focus is on pharmaceuticals and therapies. The pharmaceutical value chain is extensive, encompassing R&D, manufacturing, commercialization, and more. Currently, the mainstream market opportunities lie in three major areas:

Drug Discovery: AI Technology Brings New Possibilities to Drug Discovery;

CRO: As the entire pharmaceutical industry flourishes, market demand for CROs is becoming increasingly strong;

Innovative Pharmaceutical Companies: Poised for Explosive Growth.

Similar to new drugs, novel therapies have also witnessed numerous technological breakthroughs in recent years, attracting significant attention from the capital market. We categorize novel therapies into three types: cancer immunotherapy, gene editing therapy, and microbiome therapy.

First, let us share our investment philosophy for evaluating projects:

3.1 Immunodiagnostics

Immunodiagnostics applies immunological principles to diagnose diseases, specifically by detecting the specific binding between antigens and antibodies. It is commonly used in hospitals and health examination centers for hepatitis screening, sexually transmitted disease testing, tumor marker detection, and prenatal testing.

Immunodiagnostics has undergone a process of technological evolution, beginning with radioimmunoassay (RIA), followed by the emergence of enzyme-linked immunosorbent assay (ELISA) and chemiluminescent immunoassay (CLIA). The latter two have since become the mainstream technologies in the market, particularly ELISA and CLIA. With its superior precision and high level of automation, chemiluminescence offers distinct advantages. The latest technological trend indicates that chemiluminescent technology is gradually replacing ELISA, representing the primary direction of technological advancement in the industry.

The global market for immunodiagnostics is monopolized by overseas giants, with Roche, Abbott, Beckman Coulter, and Siemens holding the majority of the market share. This monopoly exists because these four companies have mastered the most advanced direct chemiluminescence technology and offer a comprehensive range of testing assays. Furthermore, Roche holds a significant advantage in tumor marker detection, while Abbott excels in infectious disease testing.

To what extent have domestic brands developed? Currently, in the fields of mid- and low-end reagents and instruments—particularly ELISA-compatible plate washers and enzyme immunoassay analyzers—monopolies have been broken, and localization has been basically achieved. However, cutting-edge chemiluminescence technology remains monopolized by overseas giants, with high-end reagents and instruments still dominated by foreign products.

Therefore, future focus will be placed on leading chemiluminescence technology companies to assess whether import substitution can occur in the high-end immunoassay diagnostics market.

3.2 Molecular Diagnostics

Molecular diagnostics is a technology for detecting nucleic acids (DNA or RNA). Its primary application scenario is clinical testing, with additional uses in veterinary medicine, criminal investigations, and other fields, demonstrating a broad range of applications.

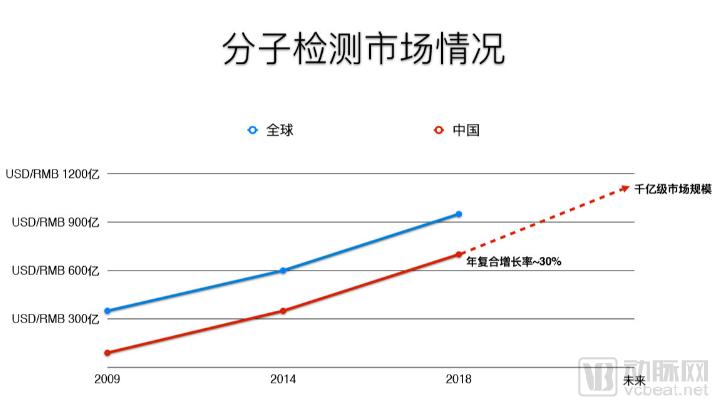

The molecular diagnostics market holds significant potential and represents the fastest-growing segment among cutting-edge testing technologies. Data show that in 2018, the global molecular diagnostics market size approached USD 100 billion, while China’s molecular testing market exceeded RMB 60 billion, with a compound annual growth rate of approximately 30%.

The characteristics of China’s molecular diagnostics market are as follows: rapid growth (with a compound annual growth rate of approximately 30%), yet it is still in its nascent stage, featuring a small market size, a fragmented competitive landscape, and relatively low penetration by overseas giants. Moreover, molecular diagnostics technologies have not yet matured, many clinical applications remain undeveloped, and the field has not become mainstream, leaving substantial room for market expansion. This industry landscape presents a favorable opportunity for the development of domestic startups.

Furthermore, China’s favorable clinical resource conditions—characterized by a comprehensive range of disease types and a large volume of case samples—are particularly advantageous to the genetic testing industry, enabling domestic players to compete with foreign giants. In China’s molecular diagnostics market, domestic companies Da An Gene and Kehua Bio-engineering hold 13% and 10% market shares, respectively, ranking third and fourth. The top two positions are occupied by foreign players Roche (16%) and Qiagen from Germany (14%).

We have observed that this sector is ushering in a new trend—the primary growth driver is shifting from pure sequencing services to the extraction of data value. The next winner will be the one who first identifies a viable model for data monetization.

Based on the mainstream branches of molecular diagnostics, we will next divide the molecular diagnostics market into three segments for discussion: gene sequencing, single-cell sequencing, and PCR.

Gene Sequencing

The mainstream application in the market is next-generation sequencing (NGS), a technology that reduces sequencing costs, improves detection sensitivity, and enables high-throughput analysis. Key players in this sector include Illumina, Life Technologies, Roche, BGI Genomics, Novogene, Berry Genomics, Burning Rock Biotech, Genetron Health, and Annoroad Gene Technology, among others. The NGS instrument market has long been dominated by the U.S. companies Illumina and Life Technologies.

In the field of next-generation sequencing (NGS), non-invasive prenatal testing (NIPT) is the most mature application. The China Food and Drug Administration (CFDA) has approved several sequencers and reagents for prenatal diagnosis. Currently, the domestic prenatal diagnosis market has largely stabilized, with the majority of the market share held by two giants: BGI Genomics and Berry Genomics.

The future development trend in this sector involves expanding the application of next-generation sequencing (NGS) technology to more areas, such as tumor detection and the widespread adoption of early cancer screening. Currently, the U.S. FDA has approved several tumor detection products.

Third-generation gene sequencing is characterized by single-molecule sequencing, which eliminates the need for sample amplification and enables the sequencing of long DNA fragments. Although third-generation sequencers have been developed, they have not yet become mainstream in the market due to the novelty of the technology. Few companies possess the capability to independently develop third-generation sequencers, including China’s Hanhai Gene, the US-based Pacific Biosciences, and the UK-based Oxford Nanopore Technologies.

Single-Cell Sequencing

Single-Cell Sequencing Is a Technology in the Sample Preparation Phase. Over the past few decades, DNA sequencing has been performed by analyzing average responses from cell populations rather than detecting individual cells. This approach yields only an averaged result, failing to reveal the unique characteristics of individual cells.

The distribution of the single-cell sequencing industry mirrors that of the overall gene sequencing sector. The upstream segment, comprising instruments, reagents, and consumables, is monopolized by foreign giants, while domestic companies such as BGI Genomics, Berry Oncology, Daan Gene, and CapitalBio are striving to achieve breakthroughs. Since upstream instruments and reagents determine costs for the mid- and downstream segments, upstream players hold significant bargaining power within the industry, leaving mid- and downstream entities with limited cost control. Consequently, it is crucial for industry participants to strategically position themselves in the upstream sector.

As for midstream sequencing services, the low barrier to entry has led to a highly fragmented market with varying quality among players. Many companies lack sufficient data interpretation capabilities and will face industry consolidation.

Downstream enterprises are third-party intermediaries situated between consumers and laboratories, engaging in laboratory information management, analysis, and sharing, or recommending genetic testing services to consumers, without involvement in testing technologies. Key players in this sector include international companies such as Grail and Bio-Rad, as well as Cirina from Hong Kong, China.

Current market growth opportunities lie in its niche segment—digital PCR. In the future, it is highly likely to be widely adopted for standardized clinical molecular diagnostics. Building upon conventional PCR, digital PCR leverages microchip and fluorescence detection technologies to achieve absolute quantification of nucleic acids. Its technical advantages include absolute quantification, high precision, high sensitivity, and low throughput. Its primary application scenarios are companion diagnostics and non-invasive prenatal testing.

Image source: Shanghai Chuangfeng Capital

From the perspective of business models, the star players in this sector are foreign companies ABI and Bio-Rad. This technology is at a very early stage, with very few companies possessing it, all of which are foreign enterprises. Currently, the market is basically monopolized by the aforementioned foreign star enterprises, and product prices are relatively high. According to public information, no digital PCR products have yet been launched in China.

3.3 POCT

POCT is a point-of-care testing technology, commonly referred to as bedside testing. Its analyzers and reagents are portable; some POCT devices are as small as a water cup, making them easy to carry. They do not require a fixed testing location and can complete tests within a short period of time.

In terms of market size, POCT is primarily applied in cardiovascular testing, with a domestic market size of approximately RMB 1 billion and maintaining a growth rate of around 30%. Additionally, POCT can be used for infectious disease testing, where the market size is RMB 600 million, growing at a rate of about 10%.

Due to relatively low technical barriers, intense homogenized competition among players, and a high rate of domestic substitution in the Chinese market. Currently, the POCT market in developed countries is relatively mature, accounting for the majority of the market share, with Cepheid, Roche, and Johnson & Johnson being the major players. There is still significant room for growth in the Chinese market, leading to rapid development. Major players in the Chinese market, such as Wondfo Biotech, Getein Biotech, and Mingde Biotech, have achieved annual performance growth rates exceeding 30% in recent years.

It is worth noting that many instrument companies operate simultaneously across POCT, digital PCR, and gene sequencing businesses; therefore, we should not analyze these sectors in isolation.

IV. Frontier Drugs and Therapies: Which Sectors Are Worth Watching? How Far Have Leading Companies Advanced?

First, let me share our investment thesis for evaluating projects:

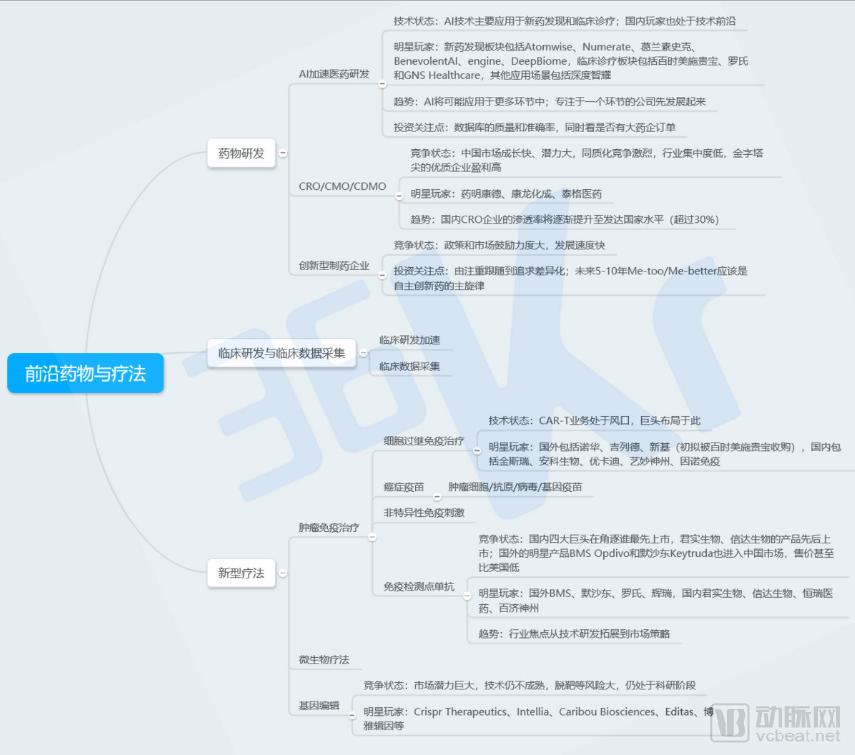

4.1 Drug Development

In the drug development arena, developed countries led by the United States are at the technological forefront, while in recent years, China’s R&D capabilities have begun to catch up rapidly.

In recent years, the domestic market environment in China has been highly favorable. Policy incentives are driving pharmaceutical innovation, and the sheer scale of the Chinese market is substantial. These factors are attracting an increasing number of highly experienced overseas talents to return home. This powerful “returnee wave” is further advancing China’s R&D capabilities.

We have compiled data on investment and financing events in pharmaceutical R&D from 2014 to 2018. The number of financing events was merely 171 and 254 in 2014 and 2015, respectively. Starting in 2016, the sector heated up dramatically, with the number of financing events peaking at 401 that year. Despite the onset of a capital winter, the figures for 2017 and 2018 saw only slight declines, standing at 302 and 279, respectively, thereby remaining largely stable.

The high level of prosperity in the drug development sector is evident.

In the drug development sector, key areas worth watching include AI-driven pharmaceutical R&D, CRO/CMO/CDMO services, and innovative pharmaceutical companies. Next, we will analyze each segment individually.

In the drug development sector, key areas worth watching include AI-driven pharmaceutical R&D, CRO/CMO/CDMO services, and innovative pharmaceutical companies. Next, we will analyze each segment individually.

AI + Pharmaceutical R&D

AI technology primarily focuses on two key areas: “new drug discovery” and “clinical diagnosis and treatment.”

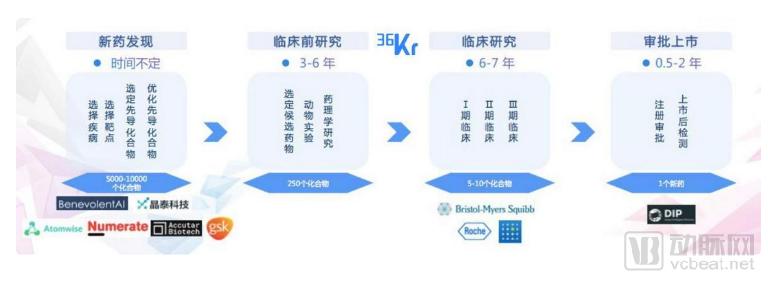

New drug discovery involves stages such as target selection, lead compound identification, and lead optimization. During this process, researchers must conduct high-throughput screening of up to 5,000–10,000 compounds, ultimately identifying candidate drugs that are both effective and safe through iterative cycles of trial-and-error, elimination, and optimization. This screening process entails numerous repetitive experiments and is highly time-consuming.

On the other hand, due to the highly complex pathogenic mechanisms of the human body, new drug development demands a substantial knowledge base from researchers, who typically require interdisciplinary expertise.

The introduction of AI technology can provide pharmaceutical R&D with a powerful “knowledge base,” facilitating the integration of multidisciplinary knowledge. Meanwhile, AI can leverage big data to conduct “virtual” screening of compounds—that is, performing analyses using databases instead of conducting physical experiments—thereby significantly accelerating the R&D process.

Due to the high technical barriers, there are still relatively few players in this sector. One group consists of startups that have focused on AI-driven drug discovery and development since their inception, while the other comprises traditional pharmaceutical companies undergoing a strategic pivot.

In this arena, prominent international players include Atomwise, Numerate, GlaxoSmithKline, BenevolentAI, Engine, and DeepBiome. We are delighted to see the presence of Chinese companies—XtalPi and Calcite BioTech—which are also at the global forefront of market competition.

In the realm of clinical diagnosis and treatment, current technologies primarily leverage databases to explore disease etiologies, predict patient responses to medications, and match patients with appropriate therapies, thereby enabling precise personalized medicine. The application of such technologies in the clinical trial phase helps enhance trial efficiency. Leading players in this field include Bristol-Myers Squibb, Roche, and GNS Healthcare.

In addition to the two major sectors mentioned above, some companies have adopted more innovative approaches; for example, Deep Intelligence has developed an AI-powered automated translation and writing system for regulatory submissions, as well as an AI pharmacovigilance system.

As for the methods to evaluate project quality, we will focus on the quality and accuracy of the database, while also considering whether major pharmaceutical companies are willing to "pay for" the technology.

Furthermore, two predictions are worth making. First, AI remains relatively underutilized in the three stages of pharmaceutical R&D: preclinical research, clinical trials, and regulatory approval for market launch. These stages are plagued by pain points such as repetitive experiments, prolonged timelines, and high costs, creating significant opportunities for AI integration in the future. Second, companies focusing on niche segments are promising; players should concentrate on deeply optimizing a specific, narrow segment within the pharmaceutical R&D process.

CRO/CMO/CDMO

Pharmaceutical contract manufacturing includes Contract Research Organization (CRO) services, Contract Manufacturing Organization (CMO) operations, and Contract Development and Manufacturing Organization (CDMO) services, providing customers with innovative process development and large-scale production solutions.

In China, this is a fast-growing sector with significant potential. Data shows that from 2013 to 2017, the domestic market size achieved a compound annual growth rate (CAGR) of 24.4%, reaching $4.2 billion in 2017. The market size is projected to exceed $15 billion by 2022.

In terms of business landscape, there are numerous domestic players, with over 500 CRO companies. The industry is characterized by intense homogeneous competition and low concentration, while high-quality enterprises at the top of the pyramid enjoy high profitability. The leading CRO companies in terms of market share include WuXi AppTec, Pharmaron, and Tigermed; the combined market share of these three industry leaders is only approximately 30%.

The author believes that the CRO sector will trend positively in the future, with the penetration rate of CRO companies gradually rising to the level of developed countries (exceeding 30%).

This is attributable to two main factors. On the one hand, the Chinese government has introduced a substantial number of policies encouraging innovative drug development, leading to an increased proportion of R&D efforts in this area and thereby boosting demand for Contract Research Organizations (CROs). On the other hand, China’s accession to the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH) has aligned the Chinese pharmaceutical industry with international standards, enabling foreign enterprises to collaborate with domestic CROs and further expanding the target market.

Innovative Pharmaceutical Company

We consider 2018 to be a year of “explosive growth in independent R&D and innovation” for China’s pharmaceutical industry, with innovative pharmaceutical companies securing frequent financing and the development of novel drugs entering a “harvest period.” This likely marks a turning point for the domestic pharmaceutical industry, shifting from a focus on follow-on strategies to the pursuit of differentiation.

According to statistics, in terms of the number of investment and financing events, domestic innovative drug R&D was merely “scattered sparks” before 2014, with only 1–6 investment transactions occurring annually. After 2016, it began to “ignite into a flame,” with the number surging to 16. The growth momentum has remained strong in the past two years, reaching a peak of 23 investment deals in 2018.

From an investment strategy perspective, Me-too/Me-better drugs should remain the main theme of independent innovative drug development over the next 5–10 years. For the Chinese market, the most urgent needs are to accelerate access to new medicines and reduce healthcare costs. Moreover, First-in-class drug development demands exceptionally high R&D capabilities and substantial funding, making short-term opportunities limited. Although the “4+7” policy introduced in 2018 did impose a brief shock on Me-too innovative pharmaceutical companies, it broadly encourages the pharmaceutical ecosystem to move toward innovation.

From an investment strategy perspective, Me-too/Me-better drugs should remain the main theme of independent innovative drug development over the next 5–10 years. For the Chinese market, the most urgent needs are to accelerate access to new medicines and reduce healthcare costs. Moreover, First-in-class drug development demands exceptionally high R&D capabilities and substantial funding, making short-term opportunities limited. Although the “4+7” policy introduced in 2018 did impose a brief shock on Me-too innovative pharmaceutical companies, it broadly encourages the pharmaceutical ecosystem to move toward innovation.

4.2 Novel Therapies

Tumor Immunotherapy

There are four branches of tumor immunotherapy, including adoptive cell therapy (TIL, TCR, CAR, LAK, CIK, NK), cancer vaccines (tumor cell/antigen/viral/gene vaccines), non-specific immune stimulation, and immune checkpoint monoclonal antibodies (CTLA-4, PD-1/PD-L1, CDX1127).

In the realm of adoptive cellular immunotherapy, CAR-T therapies are at the forefront of industry attention, with international giants such as Novartis, Gilead Sciences, and Celgene—which was proposed to be acquired by Bristol-Myers Squibb earlier this year—actively establishing their presence. Leading domestic enterprises include GenScript, Anke Biotechnology, Ucart Therapeutics, ImmuneOnco, and Inno Immune.

As for cancer vaccines, this technology was propelled into the spotlight in July 2017. At that time, two research teams from the United States and Germany simultaneously announced in *Nature* magazine that their clinical trials of personalized cancer vaccines had achieved significant breakthroughs. This signifies a groundbreaking advance in cancer vaccine technology, with the potential for application across a wide variety of cancers and a vast market outlook. Of course, this represents progress only at the scientific research level; there is still a long road ahead from laboratory research to commercialization.

At the level of immune checkpoint monoclonal antibodies, PD-1/PD-L1 technology is at the forefront. The leading international companies are BMS, Merck & Co., Roche, and Pfizer. The first-tier domestic companies are Junshi Biosciences, Innovent Biologics, Hengrui Medicine, and BeiGene. Among these four, Junshi Biosciences’ and Innovent Biologics’ PD-1 products were approved for market launch at the end of last year.

Last year witnessed intensifying competition in the PD-1 inhibitor sector. In addition to the market launches of products from Junshi Biosciences and Innovent Biologics, as previously mentioned, blockbuster international agents—BMS’s Opdivo and Merck & Co.’s Keytruda—also targeted the Chinese market, entering for commercial sale in China last year at prices even lower than those in the United States. With successive product approvals among leading companies, the industry’s focus on PD-1 inhibitors should shift beyond R&D to encompass market strategies.

Gene Editing

Gene editing is often vividly referred to as “genetic scissors.” This technology can cut, knock out, or even insert specific gene segments like a pair of scissors, thereby editing genes to ultimately cure diseases or enhance certain capabilities.

This technology holds significant market potential. Analysts estimate that the global market size for monogenic disease diagnostics is approximately $75 billion, while the market for gene therapy could reach $2 trillion. Leading companies in this space include CRISPR Therapeutics, Intellia Therapeutics, Caribou Biosciences, and Editas Medicine, with prominent Chinese players such as Edigene. Many of these leading firms were founded by pioneers who invented the underlying frontier technologies.

Despite the enormous market potential of gene editing, the technology remains immature, with significant risks such as off-target effects. It is still in the stage of scientific research, and there is a long way to go before commercial application. What broke this research status quo was He Jiankui and his gene-edited twins; this controversial project was named “Science Breakdown of the Year” by Science magazine.