Hospital M&A Activity in China Declined in Both Volume and Value in 2018, with Multiple Listed Companies Planning to Divest Healthcare Assets

According to the data from the "2018 China Hospital M&A Report," there were 30 hospital merger and acquisition projects in China last year, involving 48 target hospitals and a total transaction value of RMB 7.76 billion.

VCBeat (WeChat: vcbeat) previously compiled statistics on hospital mergers and acquisitions involving listed companies in 2017: 27 listed companies participated in nearly 50 hospital projects, with the largest single investment amounting to nearly RMB 1 billion.

Compared with 2017, both the number and scale of hospital mergers and acquisitions by domestic capital in China declined last year. The drop was even more striking compared to previous years: investment in private and public hospitals saw explosive growth in 2016, with 106 hospitals changing ownership throughout the year, involving amounts exceeding RMB 16 billion.

After several years of rapid expansion, hospital investment and M&A appear to have entered a “halftime break.” On one hand, the capital winter has prompted investors to make more prudent decisions; on the other, the hospital assets acquired rapidly require time to digest. Hospital investment and M&A are transitioning from quantitative growth to qualitative improvement.

In this article, you will see:

Overview of Hospital Investment in 2018: Private Specialty Hospitals Favored;

Multidimensional Comparison of Historical Data: A "Halftime Break" for Hospital Investment;

Fleeting Players: Multiple Companies Plan to Divest Hospital Assets;

From “Quantitative Change” to “Qualitative Change”: An Analysis of Hospital Investment Pathways.

Data from the "2018 China Hospital M&A Report" reveals that the number of domestic hospital mergers and acquisitions declined significantly last year. Meanwhile, the proportion of public hospitals involved in M&A transactions dropped from one-third in 2016 to less than 19%. Specialty hospitals have once again become a focal point for M&A activity since 2015, with ophthalmology hospitals surpassing plastic surgery and aesthetic medicine hospitals as the new hotspot for investment and mergers and acquisitions.

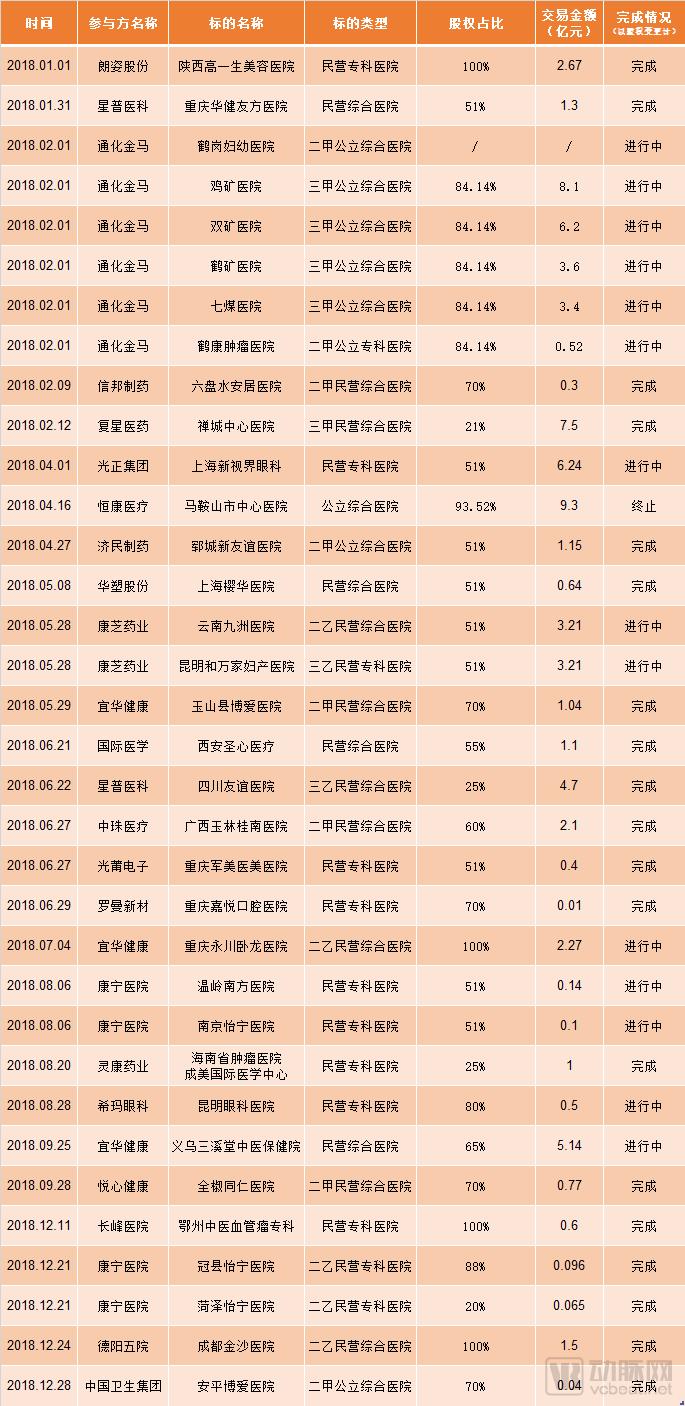

2018 Data on Hospital Mergers and Acquisitions in China

Data source: 2018 China Hospital M&A Report, VCBeat

Based on detailed data analysis, hospital investments in 2018 exhibited the following characteristics:

Investors remain diversified.Social capital is pouring into the healthcare services sector, with pharmaceutical companies extending their industrial chains, hospital groups acquiring specialized hospitals with similar business models, and cross-industry investors seeking new profit growth points.

Private Hospitals Have the "Quantity," Public Hospitals Have the "Quality."The number of transactions involving private hospitals is approximately three times that of public hospitals; however, the overall transaction amounts are nearly identical, indicating that public hospital targets command higher valuations, particularly for Grade A tertiary hospitals, which involve substantially higher transaction values.

The number of general hospitals and specialized hospitals is balanced.Overall, the number of transactions for general hospitals and specialized hospitals is roughly similar. However, public hospitals are predominantly high-tier general hospitals, which implies that private hospitals have a higher proportion of specialized hospitals and consequently a greater transaction volume. Additionally, the transaction volumes between tiered hospitals and non-tiered hospitals are relatively balanced.

Among private specialty hospitals, ophthalmology, psychiatry, and oncology institutions see more transactions.Among the private specialized hospitals involved in M&A integration, ophthalmic hospitals account for approximately 50%, psychiatric hospitals 15%, and oncology hospitals 10%, followed by medical aesthetics, traditional Chinese medicine (TCM), and orthopedics.

The Three “Mosts” of Hospital M&A in 2018: Tonghua Jinma Was the Most “Lavish”

On February 1, 2018, Tonghua Jinma issued an announcement stating that it had signed a framework cooperation agreement and planned to acquire equity interests in six hospitals—Qitaihe Coal General Hospital, Shuangyashan Mining Group General Hospital, Jixi Mining Group General Hospital, Hegang Mining Group General Hospital, Hegang Kangning Tumor Hospital, and Hegang Maternal and Child Health Hospital—through a combination of share issuance to multiple companies and individuals and cash payments.

On June 20, 2018, the detailed transaction plan was announced. Except for Hegang Maternal and Child Health Hospital, whose operating losses would lead to its entrustment rather than inclusion in the listed company’s performance consolidation, the other five hospitals were valued at a total of RMB 2.19 billion. Among them, Qitaihe Coal General Hospital, Shuangyashan Mining Group General Hospital, Jixi Mining Group General Hospital, and Hegang Mining Group General Hospital are Grade A tertiary hospitals, while Hekang Oncology Hospital is a Grade B secondary general hospital.

Detailed Transaction Plan Announced by Tonghua Jinma in June 2018

Source: Announcements by Listed Companies

However, this most “lavish” deal did not proceed smoothly. On December 19, 2018, after the listed company announced the transaction plan, the Mergers and Acquisitions and Restructuring Review Committee of the China Securities Regulatory Commission (CSRC) rejected the transaction, citing uncertainties regarding the achievability of the performance compensation commitments and the future profitability of the target assets, which failed to comply with relevant regulations.

The latest development is that Tonghua Jinma resumed trading on January 15, stating: Given the strong profitability of the target assets in this restructuring, the company considers this restructuring a significant measure to perfect its industrial chain, leverage synergies, achieve leapfrog growth, diversify its core business lines, and enhance its overall risk resistance. Meanwhile, the completion of this transaction will strengthen the listed company’s profitability and improve shareholder returns.

Industry insiders point out that Tonghua Jinma’s original core business was the R&D, production, and sales of pharmaceuticals. After Beijing Jinshang-affiliated capital took a stake in 2013, the company became keen on M&A and integration of healthcare assets, acquiring multiple hospitals successively and boosting its operational performance. This transaction faces challenges such as unreasonable valuation of the target assets, heavy reliance on major customers, consecutive losses, misappropriation of funds by related parties, and the risk of forced liquidation due to pledged equity stakes held by the listed company’s actual controller. The road ahead may still be fraught with twists and turns.

The Three “Mosts” of Hospital M&A in 2018: Kangning Hospital Was the Most “Stable”

Wenzhou Kangning Hospital Co., Ltd. is a chain hospital group specializing in psychiatric care. The company was established in February 1996 and is headquartered in Wenzhou, Zhejiang Province. On November 20, 2015, it was listed on the Main Board of the Hong Kong Stock Exchange under the stock short name “Kangning Hospital” and stock code 2120.HK. Currently, the group’s business has expanded from Wenzhou to cover the entire country.

In 2018, Kangning Hospital announced the acquisition of four hospitals: Heze Yining Hospital, Guanxian Yining Hospital, Nanjing Yining Hospital, and Wenling Nanfang Hospital, with a total valuation of approximately RMB 40 million. The acquisitions have now been fully completed, underscoring Kangning Hospital’s position as the most “stable.”

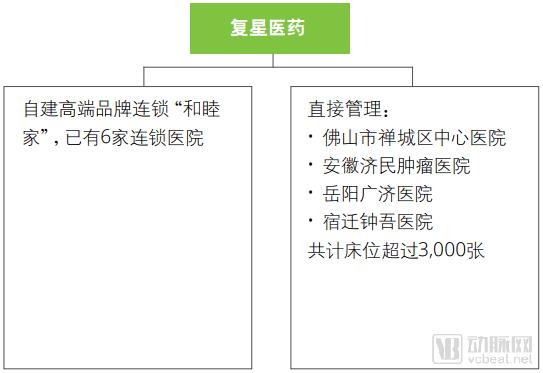

The Three “Mosts” of Hospital M&A in 2018: Fosun Pharma Is the Most “Devoted”

On February 13, 2018, Fosun Pharma announced that it had approved its controlled subsidiary, Shanghai Fosun Hospital Investment (Group) Co., Ltd., to acquire approximately 21.43% equity interest in Foshan Chancheng District Central Hospital Co., Ltd. for approximately RMB 750 million.

In fact, as early as 2013, Fosun Pharma spent nearly RMB 700 million to acquire a 60% equity stake in Chancheng Central Hospital. With two investments totaling over RMB 1.4 billion, Fosun’s hospital investment arm currently holds an 87.41% shareholding in Chancheng Central Hospital.

From 2013 to 2018, Fosun Pharma supported the continuous growth of Chancheng Central Hospital, establishing it as the flagship platform of its healthcare services. The company’s majority-controlled healthcare services business generated a total revenue of RMB 1.2 billion in the first half of 2018, representing an 18.62% year-on-year increase compared to the same period in 2017.

Fosun Pharma's Healthcare Services Layout

Source: Deloitte, VCBeat

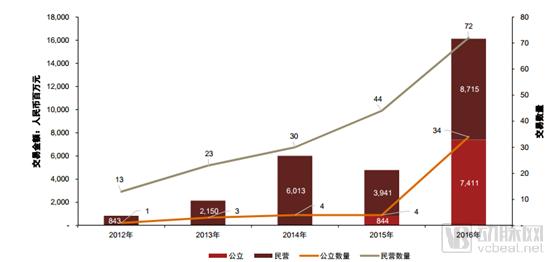

A comparison of historical data reveals that investment in both private and public hospitals experienced explosive growth in 2016, with the number of transactions and total amounts reaching new records. Driven by an increase in transactions involving specialized hospitals, the value of investments and M&A activities in private hospitals more than doubled, reaching RMB 8.7 billion. Investment activities in public hospitals also surged significantly in 2016, with disclosed transaction amounts rising to RMB 7.4 billion. The combined total for both sectors amounted to RMB 16.1 billion.

2012-2016 Domestic Hospital M&A Data

Data Source: PwC

As shown in the table above, the number of investments in private hospitals has increased year by year, with only 13 deals in 2012 and 72 in 2016. Mergers and acquisitions involving public hospitals remained relatively stable between 2012 and 2015, with fewer than five transactions annually and negligible investment amounts. However, the number surged to 34 deals in 2016.

PwC’s report further highlights that M&A transactions involving public hospitals were exceptionally active in 2016, with strategic investors increasing their investment intensity. The disclosed investors in public hospital transactions were primarily large healthcare management groups and conglomerates with long-standing presence in the healthcare sector. All acquired entities were general hospitals, predominantly Class II Grade A hospitals. Attracted by national policies, a significant number of Class III Grade A hospitals also became acquisition targets for listed companies seeking to optimize their industrial chain layouts.

In 2017, the fervor for investment and M&A in China’s hospital sector eased slightly, signaling a period of adjustment, yet it remained at a relatively high level. According to incomplete statistics from VCBeat, by the end of October 2017, 27 listed companies had participated in nearly 50 hospital projects, covering general hospitals, specialized hospitals, rehabilitation centers, and the renovation of public hospitals, with major participation methods including acquisitions, investments, and new constructions.

In 2018, the capital market cooled down, financing channels narrowed further, and with a decrease in high-quality targets, hospital investment entered a "halftime break."

A hallmark of a vibrant sector is its “ease of entry and exit,” meaning that barriers to entry do not constitute insurmountable industry obstacles, while clear and efficient exit channels are also available. This is precisely the case with investment and financing in the hospital sector: we observe a continuous influx of new entrants, alongside investors actively exiting this field.

Changbao Shares is one of several companies that once sought to aggressively expand into medical services but are now looking to exit. Primarily engaged in the R&D, production, and sales of specialized steel pipes—including pipes for natural gas, boilers, and machinery—Changbao Shares is a quintessential manufacturing company. In recent years, its performance has declined due to industry downturns, falling international oil prices, and fluctuations in raw material costs. It is against this backdrop that Changbao Shares has pursued diversification by venturing into the broader health industry.

On January 26, 2017, it issued an announcement proposing to acquire 100% equity interest in Shifang Second Hospital, 90% equity interest in Yanghe People’s Hospital, and 100% equity interest in Ruigao Investment (which holds a 71.23% equity stake in Shanxian Dongda Hospital). The three transactions were valued at RMB 228 million, RMB 351 million, and RMB 413 million, respectively, for a combined total of nearly RMB 1 billion. With a one-time investment of nearly RMB 1 billion to secure control of three hospitals, Changbao Shares’ enthusiasm for healthcare investment was evident. These transactions were completed successively in 2017.

However, just over a year later, on November 28, 2018, Changbao Shares issued another announcement stating that, in light of the company’s current actual operating conditions, the Board of Directors had approved the company’s exit from the healthcare services industry to further focus on its core business of energy tubing. This announcement prompted the Shenzhen Stock Exchange to issue a letter of inquiry, requiring the company to explain the compliance of asset disposals related to its exit from the healthcare business and to clarify whether such actions constituted a change of prior commitments.

Following the unsuccessful external transfer of medical assets, Changbao Shares stated that it would continue to hold the other medical assets acquired through its previous share issuance. After the termination of this transaction, all parties involved in the share issuance for asset acquisition and related-party transaction will continue to strictly fulfill their respective commitments.

If Changbao Shares represents capital from outside the industry, some “industry insiders” are also seeking to divest: On December 19 last year, Yibai Pharmaceutical announced its plan to transfer its 53% equity stake in Huainan Chaoyang Hospital to an external party for RMB 660 million. By January 10, the transaction had been completed. Yibai Pharmaceutical is a well-known player in the hospital investment sector, having acquired stakes in multiple hospitals over the past few years. This divestment was primarily aimed at optimizing the company’s asset structure and freeing up capital.

Another player undergoing “adjustment” is Jingfeng Pharmaceutical, which announced on December 25 last year its plan to sell 100% equity interest in Chengdu Jinsha Hospital to Deyang Fifth Hospital Co., Ltd. for RMB 150 million. The transaction is currently underway.

Jingfeng Pharmaceutical originally focused on medications for cardiovascular and cerebrovascular diseases, with core products including Shenxiong Glucose Injection, Xinnaoning Capsules (exclusive nationwide), and Lemai Pills (exclusive nationwide). Its medical services segment comprises projects such as Jinsha Hospital, Liandun Orthopedics, and Liandun Obstetrics and Gynecology.

Jingfeng Pharmaceutical acquired a 90% equity interest in Chengdu Jinsha Hospital Co., Ltd. in 2014 for a merger consideration of RMB 51.3 million, and achieved full ownership in 2015. Meanwhile, it established Guizhou Renjing Hospital Management Company and Shanghai Huayu Medical Investment Management Company to expand its presence in the healthcare services sector. In 2016, Jingfeng Pharmaceutical also obtained a 55% equity stake in Yunnan Ye’an Hospital through Shanghai Huayu.

The proceeds from the transfer of 100% equity interest in Jinsha Hospital will be utilized for the daily operational activities of Jingfeng Pharmaceutical. Upon completion of the transaction, this move is expected to optimize the company’s asset structure, increase working capital, further improve its financial position, and better support the strategic layout focused on the development pathway of internationalized, high-end, specialized generic-innovative drugs. According to preliminary calculations by the company’s finance department, the impact of this equity transfer on the company’s profit and loss is estimated to increase the total profit in the consolidated financial statements by more than RMB 60 million.

In addition, on January 24, China Resources Sanjiu announced that it had transferred its 82.89% equity stake in Shenzhen Sanjiu Hospital through a listed transfer method, with the corresponding transaction amounting to RMB 926 million. The transaction is conducive to revitalizing the company’s assets, optimizing its asset allocation, and enhancing its sustainable development capabilities, while also generating approximately RMB 680 million (after tax) in gains from asset disposal.

Of course, the aforementioned divestitures should not be overinterpreted. They merely indicate that there is robust asset liquidity within the hospital investment landscape. If hospitals were not worthy of investment, no one would be willing to “take them off their hands.” However, it is worth noting that Changbao Shares, Jingfeng Pharmaceutical, and Yibai Pharmaceutical held the hospitals slated for transfer for only a short period. Their quick exits may reflect certain challenges in asset integration, offering valuable lessons for pharmaceutical companies investing in hospitals.

A market overview reveals that the current hospital investment landscape comprises roughly three types of targets and four categories of participants. The three types of targets are: public general hospitals/private general hospitals, private specialized hospitals, and chain clinics; the four categories of participants are: large medical groups, specialized medical groups, international players, and industrial capital.

Three Types of Investment Targets and Four Categories of Participants in Healthcare Services

Source: Boston Consulting Group, VCBeat

The policy environment is favorable. The "Opinions on Further Encouraging and Guiding Social Capital to Establish Medical Institutions" points out that the access scope for social capital to establish medical institutions should be relaxed: encourage and support social capital to establish various types of medical institutions, prioritize social capital when adjusting and adding new healthcare resources, reasonably determine the practice scope of non-public medical institutions, encourage social capital to participate in the reform of public hospitals, allow foreign capital to establish medical institutions, simplify and standardize the approval procedures for foreign-funded medical institutions, improve the operational environment for medical institutions established by social capital, and promote the sustainable and healthy development of non-public medical institutions.

Mature M&A integration models have led large domestic healthcare groups to attempt building “closed-loop” supply chains by acquiring hospitals. China Resources Healthcare currently manages over 100 hospitals, with nearly 11,000 beds, and its affiliate, China Resources Pharmaceutical, supplies medications to these facilities. Insurance companies are also leveraging similar business models to promote the development of commercial health insurance, as exemplified by Taikang Xianlin Gulou Hospital.

In recent years, privately run healthcare has made significant progress. Ten types of third-party medical service institutions, along with various general and specialized hospitals, have emerged in large numbers, offering multi-level and diversified options. In the future, social capital entering the medical services sector, or hospital investment, should focus on "qualitative transformation" rather than quantitative accumulation.

Changes in the Number of Hospitals, 2008–2017

Source: Zhongtai Securities, National Health Commission

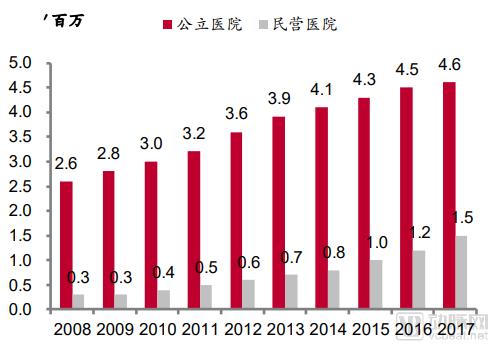

Comparison of Bed Counts Between Public and Private Hospitals

Source: Zhongtai Securities, National Health Commission

Guosen Securities’ research report posits that the healthcare services industry offers substantial growth potential and features a favorable competitive landscape. According to statistical data from the National Health and Family Planning Commission, specialized medical care and health examination services both represent vast market segments. Specialized fields such as ophthalmology and dentistry have maintained growth rates exceeding 15%, while the number of health examinations has risen rapidly alongside heightened public health awareness. These sectors have nurtured industry leaders such as Aier Eye Hospital and Meinian Onehealth, both of which hold the largest market shares in their respective non-public healthcare domains. Given the abundance of public healthcare resources in China’s first- and second-tier cities, these companies have expanded into the relatively underserved markets of third- and fourth-tier cities, providing differentiated supplementation to the public healthcare system. Driven by consumption upgrades and channel penetration into lower-tier markets, they have sustained robust growth.

Specialized chain clinics boast strong replicability and potential for large-scale expansion. The success of Meinian and Aier lies in replicating the success of individual stores across multiple locations. After establishing a mature presence in first- and second-tier cities, they have extended their reach into lower-tier markets, tapping into vast blue-ocean opportunities to meet the growing demand for upgraded medical services in third- and fourth-tier cities. Through centralized group management, resource sharing, and improved operational efficiency, these chains achieve economies of scale, develop standardized models with high replicability, and enable cross-regional expansion.

However, it should be noted that the healthcare services industry actually has high barriers to entry, with capital, talent, and management requirements all serving as moats for companies. It is characterized by high initial investment capital requirements, a strong demand for technical professionals, and high demands on corporate management and operational capabilities for achieving economies of scale and replication/expansion.

Looking ahead, social capital holds promising prospects in the grassroots medical services market, the high-end medical services market, the specialized and niche medical services market, and the public health services market. Development pathways include establishing talent growth platforms with a focus on human resources; enhancing mutual trust and recognition between doctors and patients by prioritizing patient-centered care; and leveraging specialized services to build competitive advantages for non-public hospitals.