Li Yang of Puhua Capital: Decoding the Insurability Model for Pre-existing Conditions and Seizing New Opportunities in Health Insurance

Editor’s Note: This article is republished from Puhua Capital, with authorization granted to VCBeat for republication.

According to the “2018 Commercial Health Insurance Industry Analysis Report” issued by the Insurance Association of China, there remains a significant gap in the development of health insurance in China compared with the structure dominated by short-term medical insurance in developed countries.

At the same time, companies have encountered unprecedented favorable conditions, ushering in an explosion of big data. The pharmaceutical and medical device industries have undergone unprecedented transformations. Those who can address the pain points of multiple stakeholders and design products that align with patient needs will be able to rapidly develop commercial health insurance solutions for individuals living with chronic conditions.

Li Yang of Puhua Capital has conducted research on the ongoing transformation of the insurance industry. She believes that the health insurance sector holds significant future growth opportunities. How can insurers reach healthy individuals? The most viable approach at present is to enter the market by serving patient populations first, and then gradually expand into broader markets.

Li Yang, Director of Puhua Capital

Since 2014, my colleagues and I have closely observed numerous internet upstarts as well as established insurance companies. We sensed that despite the immense potential for growth, it remained difficult to secure a share of the market. At that time, I asked myself two questions: Who is closest to the health insurance sector? And how can we reach these individuals?

According to the "2018 Commercial Health Insurance Industry Analysis Report" issued by the Insurance Association of China, total U.S. commercial medical insurance expenditures amounted to $1.12 trillion in 2016, accounting for 34% of national health spending and covering 67.5% of the U.S. population, reflecting an extremely high penetration rate. Moreover, policyholder education is highly developed; the prevailing model involves obtaining insurance coverage first and then accessing designated services. After years of development, health insurers, as payers, have taken a leading role in guiding healthcare delivery.

For example, the well-established UnitedHealth Group integrates Optum Health (a health insurance company), Optum Insight (a health information technology services company), and Optum Rx (a pharmacy benefit management company). The insurance arm delivers products to customers as the payer, while the other entities serve as managers that streamline backend services to achieve cost containment and enhance the patient care experience.

Although the average annual growth rate of domestic health insurance in China has remained at around 37% over the past five years, its net value reached only RMB 400 billion in 2017. Structurally, it is dominated by long-term insurance products (such as critical illness coverage), which still lags significantly behind the structure in developed countries, where short-term medical insurance predominates.

The underlying reasons are as follows. First, the domestic health insurance sector has a relatively short development history. Setting aside life insurance products packaged as health insurance, some enterprise employee supplemental insurance plans, which were previously dominated by group insurance, featured no leverage and no claims underwriting. Although ostensibly targeted at China’s 100 million white-collar workers, these plans suffered from inadequate premium coverage and insufficient medical service provision, yielding minimal effectiveness.

Secondly, constrained by limited experience and data, product homogenization is also severe. For instance, the emergence of the “million-yuan medical insurance” concept not only attracted a large number of consumers with its low entry threshold, high coverage limits, and broad reimbursement scope, but also drew in numerous market players, such as Fosun’s Lexiang Yisheng, ZhongAn’s Zunxiang E-Sheng, Ping An’s E-Sheng Bao, Allianz’s Zhen’ai, and Taiping’s Yibao Wuyou, resulting in substantial user education costs.

In addition, many objective issues remain:

1. Premium payments account for less than 10% of public hospital revenue and are insufficient in private medical institutions, leaving limited room for collaboration;

2. Government Focus on “High Cost of Medical Care” vs. Commercial Insurance’s Focus on Profitability, Limiting the Government’s Role;

3. Mismatch between education and sales channels and SKUs;

4. Numerous participants and complex processes;

5. Poor reach and insufficient data feedback;

6. Health insurance, like chronic diseases, is difficult for users to experience;

7. Small sales volume, resulting in low bargaining power in collaborations with pharmaceutical companies.

As is well known, a patient typically goes through several stages, including diagnosis, prescription, treatment (such as purchasing medications or undergoing surgery), follow-up visits, and recovery. Prior to recovery, some patients may struggle with complications, the risk of recurrence, and difficulties in accessing medications.

These are not only related to hospitals and doctors, but also deeply connected to the pharmaceuticals and medical devices required by patients, as well as involving auxiliary diagnostics.

At which stage should medical insurance be integrated? This is closely tied to the challenges and opportunities faced by pharmaceutical and medical device manufacturers, as well as testing service providers.

In recent years, the pharmaceutical and medical device industries have first encountered unprecedented changes—comprehensive price reductions and compliant sales practices.

In 2018, the prices of 17 drugs, including anticancer agents and patented medicines, were affected. Additionally, the national government launched centralized drug procurement pilot programs in selected sub-provincial cities, further reducing drug prices and significantly compressing profit margins.

Within hospitals, departmental consumption of pharmaceuticals and medical devices has been linked to administrative penalties. The blanket approach to compliance governance is forcing manufacturers to innovate more in their promotional strategies, particularly for new drugs. For product managers, the ratio of marketing and sales expenses allocated to their teams relative to sales revenue was already required to decrease annually; now they face further constraints on operational flexibility.

These changes have placed immense pressure on pharmaceutical and medical device manufacturers, affecting both their costs and product sales volumes.

In the past, it was standard practice for products to reach patients through physicians, who held absolute control over the treatment process.

What pharmaceutical manufacturers now need to consider is how to continuously build patient brand awareness and loyalty, while ensuring reasonable conversion and repurchase rates, amid shrinking profit margins and operational flexibility. Should they introduce new patient education concepts or launch new products?

Despite the numerous challenges mentioned above, manufacturers have also encountered unprecedented favorable conditions—the explosion of big data.

Health authorities have increased their emphasis on epidemiological investigations, providing vendors with access to more low-cost public data. Meanwhile, these vendors possess substantial clinical data of their own, particularly Phase IV clinical trial data.

The government has been substantially increasing funding year by year, enabling manufacturers to engage in more scientific research collaborations and thereby obtain research data. Single-disease specialty alliances and specialized departmental medical consortia continue to emerge, such as the Respiratory Alliance and Chest Pain Centers. Through cross-regional collaborations, manufacturers are continuously deriving broader cohort study findings and statistical reports.

Amid the predicaments facing pharmaceutical companies and medical device manufacturers, there is another role that cannot be overlooked—testing companies.

The growing emphasis on testing service providers is evident. First, with the refinement of technical platforms, these testing services have become more precise, gradually transitioning from qualitative and semi-quantitative methods to cost-effective quantitative approaches, thereby steadily increasing user acceptance.

Secondly, investors see the potential for rapid scale-up and capital operations in these enterprises, intending to continuously increase their investments. This is evident from how molecular diagnostic companies have become a strong stimulant for the secondary market.

The pain points of pharmaceutical and medical device manufacturers have precisely become opportunities for testing companies. By offering testing services for conditions such as myocardial infarction and heart failure, these companies can offset the sales restrictions on drugs and stents imposed by the new healthcare reforms. Moreover, this approach aligns with the concept of personalized/precision medicine, which garners greater interest from experts.

Testing companies themselves also face sales pressure, with the most severe issue being homogenization. For instance, certain tumor-targeted tests and mutation sites are based on publicly available information, and the testing methods, instruments, and reagents are relatively standardized (mostly PCR). Consequently, companies must continuously accelerate and increase their investments in new product development and market promotion.

If the service itself does not require CFDA certification as a barrier to entry, such as consumer genomics and certain microbial tests sold to health checkup institutions, the market becomes even more chaotic and crowded, necessitating substantial investment in consumer education.

Rather, these changes have built a bridge between enterprises and insurance services.

Therapeutic companies leverage diagnostic services to identify more precise patient cohorts while reallocating a portion of their sales revenue; meanwhile, diagnostic services utilize relevant channels to reduce the additional out-of-pocket costs associated with products, thereby creating a more comprehensive treatment solution.

This approach also introduces a certain degree of financial betting nature, such as the effectiveness of the plan or whether missed detections affect treatment. Insurance companies then design products that meet actual needs based on these factors, ensuring adaptation to the medical process from front-end, middle-end to back-end.

The integration of three systems has evolved from past outreach to physicians toward direct, long-term patient education. Insurance companies can fully leverage this shift to provide scenario-based, precision insurance services to the 400 million insured individuals with pre-existing conditions.

Taking non-invasive prenatal testing (NIPT) products as an example, as a form of auxiliary screening, they offer reference value in the assessment of Down syndrome but lack the status of a gold standard. Therefore, risk control and user education for these tests can be addressed using models similar to those employed by financial products. Recently, BGI Genomics and Taikang Insurance collaborated to launch an NIPT screening insurance product, providing mutual endorsement and facilitating customer base exchange.

The tumor-targeted therapy services mentioned earlier have also gained recognition from the insurance industry. Some cancer patients who undergo targeted testing and still see no results after treatment with specific branded drugs can receive compensation under “inefficacy insurance,” a model similar to the outcome-based payment approach for CAR-T therapy in the United States.

The core issue has emerged: pharmaceutical and medical device manufacturers, testing companies, and insurance enterprises operate with vastly different discourses. Moreover, larger organizations within these sectors often have complex internal management systems. Is there a platform capable of connecting these stakeholders to significantly enhance collaboration efficiency?

In 2017, we conducted due diligence on numerous health insurance companies with diverse market entry strategies and ultimately selected Jianyibao.

Why is it viewed favorably? First, Jianyibao’s innovative model, through multi-party collaboration, adeptly aligns with the current landscape in which participants are mutually dependent yet maintain a system of checks and balances.

Pharmaceutical companies possess the research data and patient populations that insurers need, yet they also covet insurers’ vast existing member bases and their lower-cost cash reserves. Although testing service providers offer low-cost products that can trigger users’ initial payments, they cannot exist independently of treatment protocols. While insurance enterprises appear formidable, the healthcare service system is inherently complex and represents a channel they have not previously engaged. Patients may seem to need insurance, but what they truly require is service.

JianYiBao proposes a new value proposition: It is unfeasible to simply copy and paste foreign insurance systems. While it is difficult to persuade a large number of asymptomatic individuals to purchase insurance merely for future peace of mind, an alternative approach can be adopted. By leveraging the support of pharmaceutical, medical device, insurance, and diagnostic companies, individuals with pre-existing conditions who benefit significantly from medical insurance can serve as early adopters. Their experiences can then influence their friends and family, thereby fostering insurance awareness through a reverse-engagement strategy.

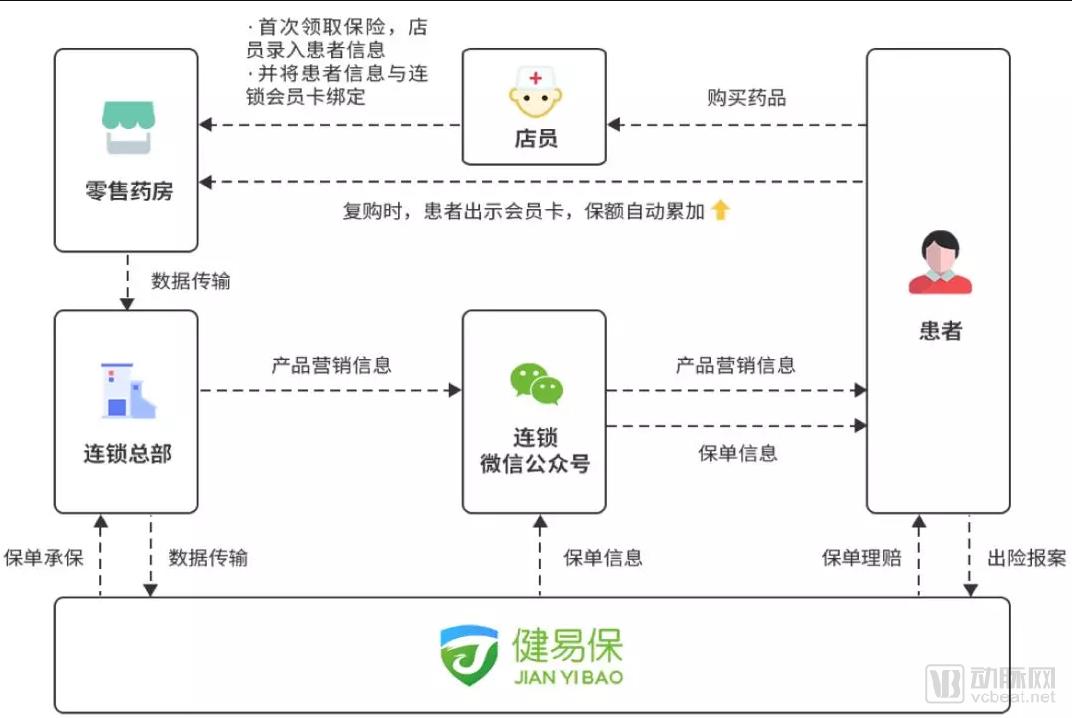

Taking a patient’s journey as an example, a coronary heart disease patient with an established habit of purchasing Plavix learned about Jianyibao through the introduction at an offline pharmacy. Upon his first purchase, he directly enrolled in the insurance plan. The store clerk entered the patient’s information and linked it to the pharmacy membership card. For subsequent purchases, the patient simply presented the membership card, and the insurance coverage accumulated automatically. Policy details, product marketing information, and subsequent claims applications can all be completed directly via the Jianyibao app or official WeChat account.

From a practical standpoint, the team has aligned the payers for its initial product offerings with the marketing budgets of pharmaceutical companies and insurers. For pharmaceutical companies, whether launching new drugs or driving volume growth for existing ones, covering insurance premiums can enhance medication adherence. Conversely, this approach also serves as a strong incentive for patients.

Meanwhile, pharmaceutical companies leverage their real-world data to offer complication insurance and recurrence insurance, providing patients with multi-layered protection.

For patients, Jianyibao helps supplement drug reimbursements by precisely integrating commercial insurance into pharmaceutical sales, thereby preventing situations where high medical costs force patients to abandon their medications.

More importantly, for certain innovative, high-value drugs, patients can also achieve outcome-based payment through Jianyibao.

Patients can gradually transition from initially receiving complimentary supplemental insurance to purchasing self-paid insurance with broader and deeper coverage, shifting from market-driven cost-shifting payments to autonomous consumer spending.

Testing services, whether for front-end diagnostics or recurrence monitoring, can be integrated with treatment regimens to identify suitable patient subgroups. This facilitates objective evaluation of therapeutic outcomes and precision medication, while further providing patients with an additional layer of protection through financial value-at-risk mechanisms.

In terms of channels, such as chain pharmacies, online platforms, and future prescription outflow channels, which previously relied primarily on procurement volume to control upstream pricing, profit margins were closely tied to fluctuations in market SKUs, resulting in significant volatility. Now, these channels can achieve new profit growth by leveraging value-added financial products and their own membership systems.

Pharmacy staff naturally possess the advantage of initially acquiring user traffic, receiving unified training from platform-based enterprises such as Jianyibao.

Initially, we were also concerned that, given the vast disparity in scale between startups and pharmaceutical companies or insurers during negotiations, what leverage would we have to secure their partnership?

We have indeed observed that a growing number of large insurance groups are incorporating insured coverage for pre-existing conditions into their online business offerings, while some companies that previously entered the market through multidisciplinary team (MDT) collaborations or in-hospital services have suddenly launched such products.

Encouragingly, as of November 2018, Jianyibao had partnered with 56 pharmaceutical retail chains across China, bringing its insurance products for individuals with pre-existing conditions to more than 20,000 retail pharmacies nationwide.

These pharmacies have become the “offline outlets” for insurance products developed by Jianyibao and insurance companies, while their staff have become “part-time insurance agents.”

In its early stages, Jianyibao received strong support from partner pharmaceutical companies, with over 200 medical representatives across more than 100 cities providing drug knowledge training to pharmacy staff.

Secondly, I highly recognize the team at Jianyibao. Most of them have experience in pharmaceutical sales, chronic disease management, and even insurance product design. They possess deep industry insights and are extremely sensitive to evolving customer needs. I believe that startups in the insurance sector must possess six core capabilities:

1. Possess a clear and profound understanding of the current state of medical insurance;

2. Understand the internal management structure of healthcare-related enterprises, particularly the collaboration models for innovative businesses;

3. Familiar with the medical consultation process;

4. Sensitive to new products;

5. Exceptional capability in acquiring consumer-facing (C-end) traffic;

6. Data Acquisition and Actuarial Capabilities.

Most critically, in an industry that is so heavily reliant on connectivity and operations, teams need to possess exceptional adaptability.

It can be said that the robust growth of Jianyibao has initially validated our team’s market analysis, though there is still a long road ahead.

With 400 million users and a trillion-yuan market, the future opportunities are immense. It is highly likely that the market will initially target patients with pre-existing conditions, then gradually expand to a broader audience. The business model will evolve from B-side acquisition of patients—where premiums are facilitated by businesses—to a stage where patients proactively purchase insurance on their own initiative.

I am often asked where the new opportunities in this industry lie. I believe that in the coming period, as advancements are made in informatization, regulation, and data support, a large number of medical insurance service enterprises will be able to provide support in areas such as innovative sales outreach, supplemental services, and premium actuarial analysis.

From an informatization perspective, the state has laid the technological and data foundation for health insurance by establishing medical big data centers, implementing rational oversight of internet-based healthcare, liberalizing prescription circulation, and issuing approval policies for AI products. Coupled with the aforementioned departmental alliances and medical consortia, this enables a broader range of population sample data to inform health insurance product design.

From the perspective of commercial health insurance regulation, the state continues to encourage commercial health insurance to serve as a supplementary coverage to public healthcare, thereby diversifying residents' medical security options.

The Tianjin Insurance Regulatory Bureau has stepped up supervision of short-term medical insurance products such as “Million Medical” plans, aiming to establish industry standards while maintaining an overall open stance.

For instance, Henan Province has launched a provincial-level commercial insurance settlement platform. Patients can be admitted to hospitals connected to this direct-billing platform without paying a deposit. Upon discharge, the medical insurance and commercial insurance adjudication systems operate in sync, allowing patients to leave after paying only the out-of-pocket expenses not covered by either insurance scheme.

Hospital information technology departments or medical insurance management divisions should also appropriately disclose medical insurance and treatment data, or provide them to authorized partners. Meanwhile, health insurance distribution channels have become more precise than before; insuring individuals with pre-existing conditions enables a tighter integration of insurance product SKUs with distribution channels, facilitating earlier intervention and faster customer education.

For entrepreneurs, overtaking on a bend by breaking into the health insurance industry holds promising prospects.