Is Allogene, the Youngest Unicorn Founded by Ex-Kite Executives, Worth Its Valuation?

Allogene Therapeutics

Developer of Immunocyte Therapy

Allogene, a clinical-stage biotechnology company focused on CAR-T therapies and less than one year old at the time of its founding, completed its IPO on Nasdaq, raising $324 million.

On the eve of the announcement of its IPO details, Allogene’s rumored share price was $16–$18, a valuation that is exceedingly high for an unprofitable biotechnology company. What factors have kept Allogene’s valuation elevated even as capital markets grow increasingly cautious?

Allogene is headquartered in South San Francisco, California, USA. Founded in late 2017, the company was established by Arie Belldegrun and David Chang, both former executives at Kite Pharma. Kite Pharma was acquired by Gilead Sciences for $14 billion in 2017. Yescarta (axicabtagene ciloleucel), developed by Kite Pharma, was one of the first two CAR-T therapies to receive FDA approval. Allogene is the new company founded by them after their departure from Kite.

On the evening of October 10, 2018, Allogene officially released its prospectus, finalizing the upper end of its pricing range at $18 per share. The company planned to offer 18 million shares of common stock to the public, underwritten by top-tier investment banks including Goldman Sachs, J.P. Morgan, Cowen, and Jefferies, with the offering expected to close on October 15. The total proceeds raised amounted to $324 million.

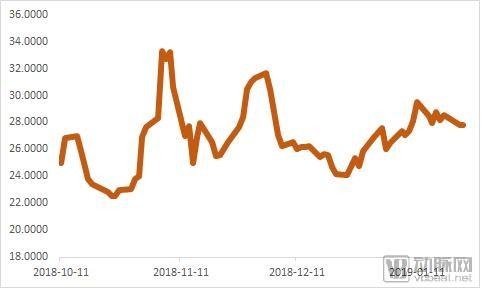

The following day, Allogene’s shares began trading on the Nasdaq Global Select Market under the ticker symbol “ALLO.” After 3:00 p.m. New York time that afternoon, Allogene’s stock price surged as much as 44.38% to $25.99. On its first day of trading, ALLO closed at $25. At the time, the Nasdaq Biotechnology Index was falling to its lowest level since July 2018. As of press time, Allogene’s real-time share price was $31.14.

Allogene’s Price Trend Since Its IPO

Ultimately, Allogene raised $324 million through its IPO, pushing the total value of U.S. biotech IPOs in 2018 above $6 billion and setting a new record for fundraising by U.S. biotechnology companies over the past decade. The period from 2009 to 2018 marked the most active decade for U.S. biotech firms in the capital markets.

After deducting underwriting discounts and offering expenses, Allogene netted $297 million. Following the completion of the offering, Allogene’s market capitalization reached $2.05 billion. Allogene has allocated these funds as follows:

Approximately $25 million, to cover part of the costs for the ongoing UCART19 CALM and PALL clinical trials;

Approximately $40 million, to cover part of the costs for the planned UCART19 CALM II and PALL II clinical trials;

Approximately $40 million, to cover part of the costs for the planned ALLO-501 clinical trials;

Approximately $60 million, for the planned clinical trials of ALLO-715;

Approximately $45 million, allocated for transition services from Pfizer and for expanding our facilities, including establishing our headquarters in South San Francisco, California;

Approximately $35 million will be used to enhance internal R&D capabilities to advance new product candidates, with the remainder allocated to working capital and other general corporate purposes, including additional expenses associated with being a public company.

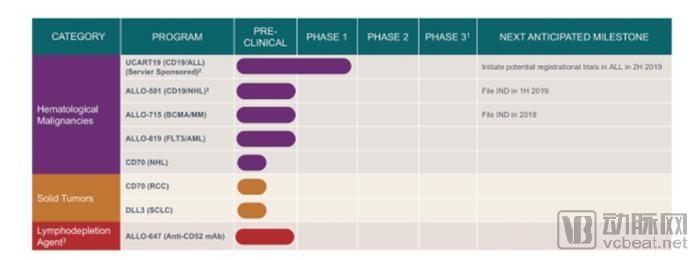

Allogene’s core asset, UCART19, is a gene-engineered allogeneic T-cell therapy designed to treat cancer. As a CAR-T drug targeting refractory/relapsed acute lymphoblastic leukemia (ALL), UCART19 has completed its Phase II clinical trial. Clinical trial results demonstrated a complete response (CR) rate of 81% in patients. Furthermore, compared with traditional autologous CAR-T therapies, UCART19 offers advantages in terms of greater accessibility, higher efficiency, and lower cost.

According to the prospectus, in addition to UCART19, Allogene’s product portfolio includes 16 preclinical assets of T-cell therapies. The following is an excerpt from the description of Allogene’s promising pipeline in the prospectus.

“ALLO-501. We plan to submit an Investigational New Drug (IND) application in the first half of 2019 for our second allogeneic anti-CD19 CAR T-cell product candidate, ALLO-501, for the treatment of patients with relapsed or refractory non-Hodgkin lymphoma (R/R NHL). Although the manufacturing process for ALLO-501 differs from that of UCART19, the two candidates are identical in molecular design.”

ALLO-715. We plan to submit an Investigational New Drug (IND) application in 2019 for ALLO-715, an allogeneic CAR T-cell product candidate targeting BCMA for the treatment of patients with relapsed/refractory (R/R) multiple myeloma. Several clinical studies of third-party autologous CAR T-cell therapies targeting BCMA have already yielded promising results in this indication.

ALLO-647. We are developing ALLO-647, an anti-CD52 monoclonal antibody, designed to be administered prior to the infusion of our other candidate products as part of a lymphodepletion regimen. We believe that ALLO-647 can reduce the likelihood of patient immune system rejection of engineered allogeneic T cells and may create a persistence window during which our engineered allogeneic T cells can actively target and destroy cancer cells.

Allogene’s Product Pipeline as Disclosed in the Prospectus

Prior to its IPO, Allogene had already demonstrated strong performance in the capital markets. Founded in late 2017, the company saw robust momentum in the capital markets throughout 2018.

In April, Allogene completed its Series A and Series A-1 financing rounds, raising $300 million through the issuance of convertible preferred shares. In September, Allogene raised $120 million by issuing convertible notes. Each round set a new record.

Allogene’s prospectus reveals that prior to its IPO, the company held approximately $410 million in cash and cash equivalents. Based on the cash burn rate during the first half of 2018, Allogene’s available funds were sufficient to sustain operations for only 1.5 years. Financial reports indicate that in the first half of 2018, the company incurred total operating expenses of $137 million, including $122 million in research and development (R&D) expenses, with R&D accounting for a substantial 89% of the total. Given that Allogene’s product pipeline is still in relatively early stages, such expenditure levels are expected to persist for a considerable period.

Therefore, Allogene’s massive fundraising has drawn considerable skepticism.

On October 12, Bloomberg published an article stating that Allogene’s blockbuster IPO defied market risks. The piece was written by Max Nisen, a Bloomberg columnist covering biotechnology, pharmaceuticals, and healthcare. Nisen argued that Allogene’s market valuation was based on the monetization of its management team’s strength, and that the single drug candidate used in human trials alone could not justify how Allogene rose from an idea to a valuation of over $2 billion in less than a year. “This is an example of a biotech management premium, where investors focus excessively on the company’s leadership while overlooking the business itself, which is misguided.”

Max cited similar examples of management premiums in his article. Axloant Sciences was the only biotechnology company with an IPO size larger than that of Allogene Therapeutics. Its lead drug candidate, a novel investigational therapy previously abandoned by major pharmaceutical companies, had suffered a disastrous failure in clinical trials for Alzheimer’s disease. After David Hung joined Axloant Sciences as CEO, the company’s stock price soared. However, in September 2017, its investigational new drug failed again, causing the stock price to plummet and leading to David Hung’s discreet departure. External analysts suggest that the surge in Axloant Sciences’ stock price was closely linked to David Hung’s prior sale of his company, Medivation Inc., to Pfizer for $14 billion.

Coincidentally, the CEO of Clovis Oncology Inc. also has experience selling his company to Celgene. In 2016, Clovis Oncology’s lung cancer drug failed to meet expectations, triggering a sell-off that halved the company’s value.

Almost simultaneously, another noteworthy article raising doubts appeared on the Medium platform. Nisarg Patel, founder of Memora Health, used a series of quantitative financial analyses to point out that even granting Allogene’s core product UCART19 a greater than 20% probability of successful commercialization, the company’s net present value (NPV) was insufficient to support its $2.05 billion valuation. Below is VCBeat’s summary and synthesis of Patel’s analytical framework:

Market Size.Allogene’s flagship product, UCART19, is indicated for the treatment of refractory or relapsed acute lymphoblastic leukemia (ALL). Approximately 5,960 new ALL cases are diagnosed annually in the United States. Among adult patients, about one-third have standard-risk ALL, while two-thirds have high-risk ALL, the latter being the target population for UCART19. Each year, around 3,000 patients under the age of 20 are diagnosed with ALL, and 15%–20% of pediatric patients experience relapse after treatment. Accordingly, Patel estimates that the total annual market demand for UCART19 and its competitors comprises 1,500 adult patients and 600 pediatric patients.

Penetration rate.Patel projects a market penetration rate of 35% for UCART19, corresponding to treatment for 735 patients. On one hand, the market size is in an upward trajectory, with Kymriah currently being the only competitor. If Allogene can bring UCART19 to market first, it will gain a first-mover advantage. Meanwhile, UCART19 holds certain advantages over Kymriah in terms of manufacturing cost and efficiency.

On the other hand, CAR-T therapy remains confined to large hospitals, and its widespread adoption in community settings requires further reduction in toxicity. Under MS-DRG 016, the Centers for Medicare & Medicaid Services (CMS) provides only a base reimbursement of $36,000 and a New Technology Add-On Payment (NTAP) of $186,500 for CAR-T therapy, resulting in patient out-of-pocket costs exceeding 50%.

Net Cash Flow.Kymriah is priced at $475,000, with the maximum price for UCART expected to be $400,000.

Based on an estimated 35% market share, the annual sales revenue of UCART19 is projected to be $294 million. Sales are expected to reach saturation five years after launch. Calculated over a 13-year period of patent exclusivity, the risk-adjusted net present value (rNPV) of the UCART19 pipeline is approximately $440 million. UCART19 was the primary and sole product pipeline of Allogene Therapeutics at the time of its public listing.

The final point to note is that even with its UCART19 pipeline, Allogene faces a highly competitive external environment. In addition to strong competitors such as Atara Biotherapeutics and Fate Therapeutics, major pharmaceutical companies including Gilead, Celgene, and Novartis are also investing in next-generation cell therapies. Moreover, first-generation CAR-T drugs have seen slow market adoption; for Allogene’s products to succeed, they must demonstrate exceptionally high levels of safety and efficacy.

According to Max, Allogene is expensive due to the halo effect surrounding its management team’s professional experience. VCBeat’s review reveals that the founding team of Allogene indeed has an impressive track record.

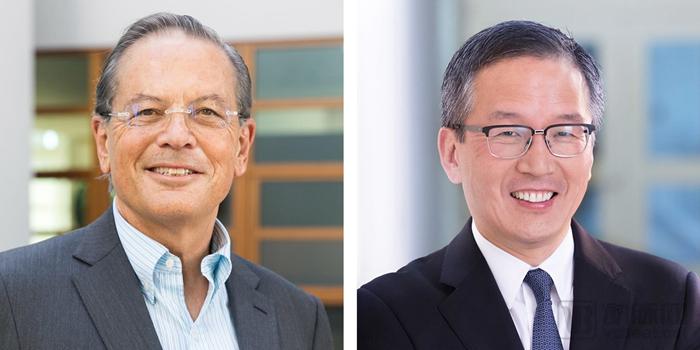

Arie and David

Arie Belldegrun, Co-founder; M.D. from the Hebrew University of Jerusalem Hadassah Medical School; Director of the Institute of Urologic Oncology at the David Geffen School of Medicine at UCLA; Fellow of the American College of Surgeons and the Society of Urologic Oncology.

David Chang, Co-Founder, holds a Bachelor of Science in Biology from the Massachusetts Institute of Technology and an M.D. He served as an executive and director at Amgen from July 2006 to May 2014.

Arie and David’s paths crossed through their co-founding of Kite Pharma, where David served as Chief Medical Officer and Executive Vice President of Research and Development. Together, they drove the FDA approval of Yescarta, an oncology gene therapy. In 2017, Arie and David sold Kite Pharma to Gilead Sciences for $12 billion. In just three years, Kite Pharma executed a remarkable triple play: launching its IPO, securing FDA approval, and achieving a high-value acquisition.

Given the industry influence of Arie and David, it is only natural that every move by Allogene Therapeutics draws attention from the sector.

Yescarta and Novartis’s Kymriah are the two CAR-T therapies approved by the FDA in the United States to date, priced at $373,000 and $475,000, respectively.

Among them, Yescarta received FDA approval for marketing on October 18, 2017, for the treatment of adult patients with certain types of large B-cell lymphoma, including diffuse large B-cell lymphoma (DLBCL), primary mediastinal B-cell lymphoma, high-grade B-cell lymphoma, and DLBCL arising from follicular lymphoma, in patients who have been refractory to or relapsed after at least two prior lines of therapy.

DLBCL is the most common type of NHL in adults. In the United States, 72,000 new cases of NHL are diagnosed each year, with DLBCL accounting for approximately one-third of newly diagnosed cases. Yescarta is also the first gene therapy approved for certain types of non-Hodgkin lymphoma (NHL).

Kymriah, another CAR-T therapy drug, is a competitor to Allogene’s UCART19. It received FDA approval for marketing on August 30, 2017, becoming the first CAR-T therapy approved by the FDA. Kymriah is indicated for children and young adults (under 25 years of age) with certain cases of acute lymphoblastic leukemia (ALL) that are refractory or have relapsed for the second time or later. ALL is the most common childhood cancer in the United States. The FDA granted Kymriah Priority Review and Breakthrough Therapy designation.

The safety and efficacy of Kymriah were confirmed in a multicenter clinical trial involving 63 pediatric and young adult patients with relapsed or refractory B-cell precursor acute lymphoblastic leukemia (ALL). The overall response rate within three months of treatment was 83%; however, clinical trial data for UCART19 indicate that it has a superior safety profile compared to Kymriah.

The prospectus reveals that Allogene’s lead drug, UCART19, along with a series of preclinical assets, were acquired from Pfizer. Interestingly, Pfizer itself acted as an intermediary for these investigational assets, whose original developer is the French biotechnology company Cellectis. Under prior agreements, if these drugs successfully complete development, Allogene is required to pay Cellectis hundreds of millions of dollars in milestone payments, despite Cellectis’s current valuation being less than half that of Allogene.

In fact, Cellectis was on the verge of bankruptcy when it pushed UCART19 into Phase I clinical trials. In February 2014, Servier, the second-largest pharmaceutical company in France, came to Cellectis’s rescue, paying a $10 million upfront fee and $140 million in milestone payments to secure global exclusive options for Cellectis’s lead candidate, UCART19, and five other candidates targeting solid tumors. This was a win-win deal: it saved Cellectis while allowing Servier to acquire a substantial portfolio of high-quality assets at a low valuation. Four months later, when Pfizer took over another 15 early-stage assets from Cellectis, the upfront payment had risen to $80 million.

Thereafter, the clinical development of UCART19 entered the fast track. In November 2015, upon completion of the Phase I clinical trial of UCART19, Servier’s global exclusive option for UCART19 was converted into a global exclusive commercialization right. Pfizer paid to secure a share, obtaining the U.S. commercialization rights for UCART19.

In April 2018, Pfizer became an A-1 shareholder of Allogene Therapeutics and sold to the company its portfolio of 15 cell therapy assets acquired from Cellectis, along with the rights to share in the sales revenues of UCART19 with Servier. This transaction, valued at over $800 million, was the most significant deal for Arie and David’s new company, as the product pipeline acquired from Pfizer constituted nearly all of Allogene’s assets.

Regarding this asset transfer, Dr. David Chang, President and Chief Executive Officer of Allogene Therapeutics, believes that Allogene is well-positioned to advance Pfizer’s CAR-T asset portfolio into potential innovative therapies and reach patients more rapidly. He characterized this move as a bold and innovative initiative by a leader in the field of tumor immunotherapy.

Allogene and Servier plan to initiate the Phase II study of UCART19 in 2019.

It is worth noting that, in addition to channeling substantial R&D funding into its product pipeline, Allogene must also make timely milestone payments for its in-licensed assets. When further considering the restricted sales rights during the commercialization phase, the risks faced by Allogene’s investors are not to be underestimated. Allogene boasts a diverse pipeline of investigational products, and coupled with the management team’s extensive professional expertise, the enthusiasm from the capital market is by no means unfounded.

However, as David noted, Allogene’s mission is to expedite patient access to effective therapies. Heavy is the head that wears the crown; whether Allogene delivers value for money will ultimately be determined by the market.

Scan the QR code to follow the VCBeat New Medicine official account (biobeat1)