Prospect 2019: Panoramic Atlas of China's Elderly Care Industry

Editor’s Note: This article is republished from Qianzhan.com, authored by Li Mingjun. Republished with permission by VCBeat.

On September 24, 2018, the State Council issued the “Implementation Plan for Improving Systems and Mechanisms to Promote Consumption (2018–2020),” which abolished the licensing requirement for establishing elderly care institutions, encouraged public elderly care facilities to transition to a model of public ownership with private operation, and further relaxed market access.

The elderly care industry in the broad sense refers to industries providing services centered on human life, forming a diverse industrial cluster aimed at achieving long-term health and well-being. According to the concept proposed by the Global Aging Research Center (OLDAGE), the elderly care industry primarily encompasses industries related to life security for individuals. This industry cannot be simply categorized under a single sector; rather, it spans the primary, secondary, and tertiary industries, constituting an integrated industrial agglomeration system that combines production, operation, and services. In the narrow sense, the elderly care industry mainly serves individuals aged 60 and above, with “elderly care services” as its core, focusing on mainstay and supporting industries that address their needs in clothing, food, housing, transportation, and medical care.

“Clothing” refers not only to garments for the elderly, but broadly to daily necessities for seniors, including reading glasses, hearing aids, dentures, and wigs.

“Food” primarily refers to food products for the elderly, including low-salt, low-sugar, and low-fat foods, as well as health supplements and nutritional products.

“Living” primarily refers to elderly care facilities, such as senior housing developments, retirement apartments, and community-based elder care facilities;

“Mobility” primarily involves transportation means required for elderly travel, recreational facilities and equipment for the elderly, and tourism services for the elderly;

“Medical care” primarily includes elderly convalescence, medical nursing, and related services.

According to the Industrial Classification for National Economic Activities published by the National Bureau of Statistics, the main entities and pillar industries of senior housing real estate involve six sectors: manufacturing; health and social work; accommodation and catering; real estate; culture, sports, and entertainment; and education.

In recent years, with the rapid development of new-generation information technologies characterized by Internet of Things (IoT) integration, network connectivity, and intelligence, as well as the continuous improvement of digital literacy among the elderly population, the elderly care industry has been expanding outward, giving rise to more supporting industries in areas such as finance, information transmission, software and information technology services, public administration, social security, and social organizations. Consequently, “smart elderly care” and “integrated medical and elderly care” have become hot topics of discussion.

In addition to the aforementioned pillar and supporting industries of elderly care, the sector exerts a strong pull on upstream and downstream industries. Examples include the construction industry, the production and supply of heating, gas, and water associated with senior housing; transportation services related to elderly mobility; scientific research and technical services dedicated to the R&D of products for seniors; and business services providing legal assistance to the elderly. As the elderly care industry matures and becomes more comprehensive, its influence will extend across various sectors, making the “silver economy” a significant driver of economic growth.

Prior to the reform and opening-up, retired employees of urban enterprises, public institutions, and government agencies relied on state and employer support, which facilitated robust development of the elderly care industry. In rural areas, collective economies and government relief provided elderly care services for “Five-Guarantee” seniors.

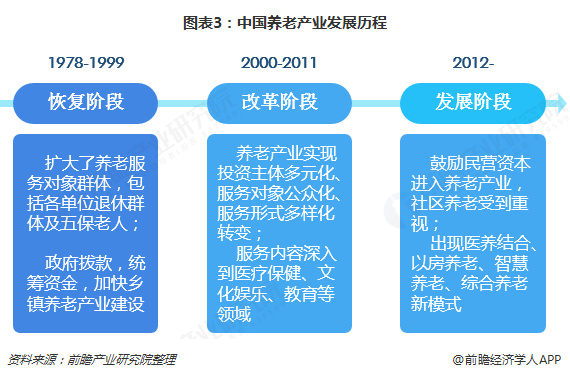

Since the reform and opening-up, with the rapid development of the national economy and relative social stability, the elderly care industry has undergone three phases—recovery, reform, and development—and has gradually exhibited new changes.

——Recovery Phase of the Elderly Care Industry (1978–1999)

After 1978, the state began to uniformly adjust and restore various social welfare security measures, including the revitalization of the elderly care industry. In June 1978, the State Council promulgated the Interim Measures for the Placement of Elderly, Weak, Sick, and Disabled Cadres and the Interim Measures for the Retirement and Resignation of Workers, which standardized the retirement systems for employees of state-owned enterprises, government agencies, and public institutions. These measures integrated the retirement system into the old-age insurance system framework, thereby expanding the scope of beneficiaries. In 1994, the State Council issued the Regulations on Rural Five-Guarantee Support Work, clarifying the nature, support mechanisms, and standards of the Five-Guarantee system. In 1997, the Ministry of Civil Affairs promulgated the Interim Measures for the Administration of Rural Welfare Institutions, proposing the standardization and development of rural welfare institutions through local government funding and centralized financial pooling to increase the rate of institutionalized care. In 1998, a total of 2.226 million people nationwide received “Five-Guarantee” benefits, among whom 620,000 were provided with centralized care by township welfare institutions.

During this period, China’s social welfare sector experienced rapid recovery and shifted toward a more socially oriented model.

——Reform Phase of the Elderly Care Industry

Entering the 21st century, China began to experience population aging. According to data from the 2000 Chinese Census, the population aged 65 and above accounted for 6.96% of the total population, making elderly care a critical issue affecting the nation’s economic, political, and social development. Various sectors of society have gradually become involved in building the elderly care industry, thereby promoting its transformation.

In 2000, various ministries and commissions jointly issued the "Opinions on Accelerating the Socialization of Social Welfare," which explicitly proposed policies for the socialization of social welfare, advocating an elderly care model based on home care, supported by communities, and supplemented by social welfare institutions. In 2003, the Ministry of Civil Affairs released the "Guiding Opinions on Private Operation with Public Support and Public Ownership with Private Management of Social Welfare Institutions," affirming support for socially run welfare institutions.

Since the beginning of the new century, guided by policies promoting the socialization of welfare, China’s elderly care industry has further developed, achieving a transition toward diversified investment entities, public-oriented service recipients, and varied service models. The scope of services in the elderly care sector has gradually expanded into areas such as medical and healthcare services, domestic housekeeping, entertainment and fitness, and education for the elderly. By the end of 2009, the number of various elderly care institutions in China reached 40,000, including nursing homes, senior apartments, welfare institutes, and custodial care facilities. The number of elderly care beds increased to 2.89 million, representing an approximately two-fold increase compared with 1999.

——Development Stages of the Elderly Care Industry (2012–)

In 2012, the 18th National Congress of the Communist Party of China proposed “actively responding to population aging and vigorously promoting the development of the elderly care service industry,” bringing new opportunities to the growth of the senior care sector. During this period, community-based elderly care gradually gained government attention. As population aging intensified, the number of elderly care institutions showed a trend of rapid expansion. In September 2013, the State Council issued the Several Opinions on Accelerating the Development of the Elderly Care Service Industry, calling for accelerated development of the sector and encouraging social forces and private capital to enter it. This prompted various sectors to actively explore approaches to address the challenges posed by an aging population. Models such as integrated medical and elderly care, reverse mortgages for elderly care, smart elderly care, and comprehensive elderly care gradually came into public view.

Currently, the prevalent model of integrated medical and elderly care in China involves establishing medical institutions, such as geriatric hospitals and rehabilitation hospitals, within nursing homes. In November 2017, the National Health Commission issued the Notice on Canceling Administrative Approval and Implementing Filing Management for Medical Institutions Established Within Elderly Care Facilities, thereby facilitating the establishment of in-house medical institutions in nursing homes.

As of 2017, elderly care services in China had expanded from over 8,000 service institutions in 1978 to 155,000 various types of elderly care service providers, including elderly care institutions, community-based elderly care facilities, and mutual-aid elderly care facilities. Furthermore, with the rapid development of new-generation information technologies characterized by Internet of Things (IoT) connectivity, networking, and intelligence, internet technology companies have accelerated their penetration into the smart elderly care industry. In November 2017, the National Health Commission released a list of pilot demonstration projects for smart health and elderly care applications, comprising 53 enterprises and 19 demonstration bases.

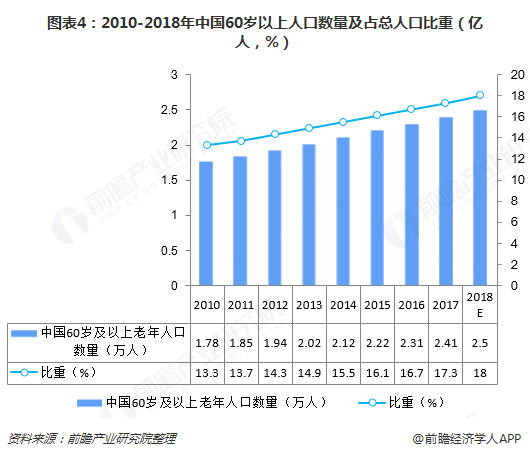

According to data from the National Bureau of Statistics, China had 241 million people aged 60 and above in 2017, accounting for 17.3% of the total population, indicating an intensifying aging problem. Furthermore, the World Health Organization predicts that by 2050, 35% of China’s population will be over 60 years old, making it one of the most severely aged societies in the world.

In China, the main providers of elderly care institutions are public ones. Other forms of elderly care institution providers have not developed sufficiently, with a small supply of beds, which cannot fill the supply gap left by public elderly care institutions.

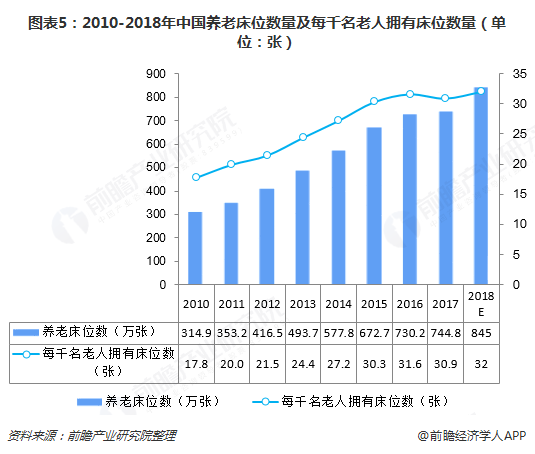

According to data released by the Ministry of Civil Affairs, there were a total of 155,000 elderly care service institutions and facilities across China in 2017, representing a year-on-year increase of 10.7%. Among these, there were 29,000 registered elderly care service institutions, 43,000 community-based elderly care institutions and facilities, and 83,000 community mutual-aid elderly care facilities. The total number of elderly care beds reached 7.448 million, a year-on-year increase of 2.0%; the number of elderly care beds per 1,000 elderly people was 30.9, a decrease of 2.2% compared with the previous year.

On September 24, 2018, the State Council issued the Implementation Plan for Improving Systems and Mechanisms to Promote Consumption (2018–2020), further relaxing market access in the consumer sector. In the elderly care segment, the licensing requirement for establishing elderly care institutions was abolished, public elderly care facilities were encouraged to transition to a model of public ownership with private operation, and various market entities were supported in increasing the supply of elderly care services. The integration of medical and elderly care services was also promoted.

With the deregulation of licensing for elderly care institutions, the entry barriers for private enterprises into the elderly care industry have been significantly lowered, and the market for privately run elderly care institutions is expected to enter a period of rapid growth. Considering the potential service market of the elderly care industry and the development status of its upstream and downstream sectors, the potential market size of the elderly care industry was approximately RMB 5.6 trillion in 2017. It is projected to reach around RMB 14 trillion by 2024.

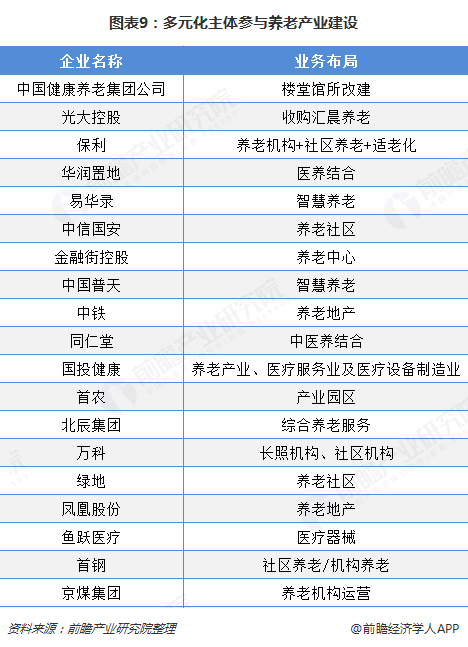

In recent years, investment in the elderly health services sector has accelerated, with real estate and insurance companies beginning to engage in the development of senior care facilities. Key participating enterprises include Vanke, Poly Real Estate, World Union, Phoenix Shares, Yuwell Medical, E-Hualu, Greentown Group, and Taikang Life Insurance.

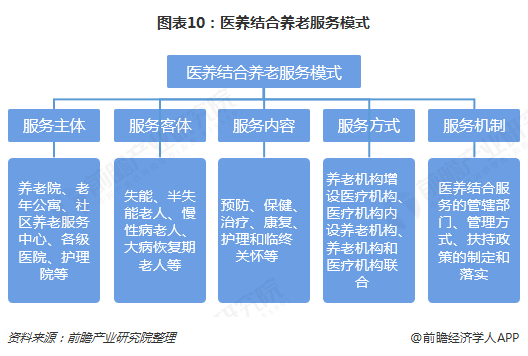

Integrated Medical and Elderly Care Services represent an upgrade and extension of traditional elderly care models. In this framework, “medical care” encompasses services such as healthcare and health screenings, while “elderly care” includes daily living assistance and cultural activities. By adopting an integrated development model that combines medical treatment, rehabilitation, wellness, and elderly care, this approach resolves the issue whereby elderly individuals’ health concerns could previously only be addressed in hospitals. It meets the needs of disabled and partially disabled seniors while maximizing the utilization of social resources.

In the report to the 19th National Congress of the Communist Party of China in 2017, the “Healthy China Strategy” explicitly emphasized the establishment of a policy framework and social environment for elderly care, respect for the elderly, and filial piety toward the elderly; it also called for advancing the integration of medical and elderly care services and accelerating the development of both public initiatives and industries related to aging. In September 2018, the State Council issued the Implementation Plan for Improving Systems and Mechanisms to Promote Consumption (2018–2020), which once again highlighted the promotion of integrated medical and elderly care services.

Currently, elderly care institutions in China generally suffer from a lack of high-quality medical services. Many adopt a model that separates medical care from elderly care, forcing seniors to shuttle inconveniently between care facilities and medical institutions. Although policy support for the integration of medical and elderly care has intensified in recent years, progress remains relatively slow. On one hand, "medical care" and "elderly care" are two distinct industries with different regulatory bodies, making it difficult to coordinate and unify relevant standards. On the other hand, achieving profitability in integrated medical and elderly care services is challenging. As this integration is largely a public welfare undertaking with thin profit margins, private enterprises are hesitant to commit substantial time and capital.

China’s business models for integrated medical and elderly care remain in an exploratory phase. With the opening of market access for elderly care institutions and the promotion of privatization of public elderly care facilities, a more diverse range of investors will participate in the elderly care market to explore models of integrated medical and elderly care suited to the Chinese context.

——Diversification of Elderly Care Service Models

China’s elderly care models remain relatively homogeneous, primarily consisting of welfare institutes, nursing homes, homes for the aged, and senior apartments. Community-based elderly care services are largely limited to senior service centers, universities for the elderly, and senior clubs. Emerging models, such as smart elderly care and integrated medical and elderly care, are still in the exploratory phase. Drawing on the experience of developed Western countries, the elderly care industry will inevitably become more refined, specialized, regulated, standardized, and systematic in terms of service functions and types. This evolution will foster a multi-tiered, diverse, and broadly accessible elderly care service network, offering seniors a wide range of services that extend from basic daily living assistance to medical rehabilitation, emotional support, legal services, compassionate caregiving, and emergency aid.

——Public-Private Operation of Elderly Care Institutions

To address the growing pressure of elderly care, developing a "publicly owned, privately operated" model in the elderly care sector—by introducing social forces and private capital into the market to expand supply—is a viable approach. In 2018, the State Council issued policies that abolished the licensing requirement for establishing elderly care institutions and simultaneously encouraged the adoption of the publicly owned, privately operated model. As elderly care service models gradually evolve toward greater specialization and division of labor, the publicly owned, privately operated model, wherein the government funds and contracts professional elderly care institutions for operation and management, will become the mainstream trend of the era.

——The Advantages of Smart Elderly Care Service Models Are Gradually Becoming Prominent

Smart elderly care emphasizes the use of the Internet of Things (IoT), big data, and intelligent technologies. Smart elderly care services leverage perceptual and intelligent methods to create a living environment with real-time monitoring, intelligent early warning, and rapid response capabilities, thereby safeguarding the health and safety of older adults. The components of smart elderly care include smart homes, wearable intelligent devices, smart communities, and smart healthcare. In an era where information technology continues to bring profound changes to various sectors of society, leveraging IT to optimize the allocation of elderly care resources and innovate service models is an inevitable path to addressing the challenges of aging.