The Three Engines Driving the Pharmaceutical M&A Surge: Innovation, Synergies, and Portfolio Strategy

The United States passed tax reform at the end of 2017, slashing the corporate tax rate from 35% to 15%, which sparked speculation that the wave of mergers and acquisitions (M&A) in the pharmaceutical industry would soon heat up. In fact, this has become a reality: in the first half of 2018, there were 212 M&A deals in the pharmaceutical industry, with a transaction value exceeding $200 billion—61 more deals than the 151 recorded during the same period in 2017.

This is a surprising growth, but from a broader strategic perspective, such transactions are not unexpected. The mergers and acquisitions in the pharmaceutical industry are no different from those in industries with similar acquisition appetites, such as telecommunications, media, and energy. In these sectors, new technologies are reshaping operating costs and driving companies to continuously seek innovation externally. Against this backdrop, large-scale deals by major pharmaceutical companies have become the norm rather than the exception. Tax reform is merely the latest in a series of market forces—such as blockbuster drugs and biotechnology—that have transformed how pharmaceutical companies think about and pursue deals over the past decade or more.

McKinsey Knowledge Center research experts Roerich Bansal, along with colleagues Ruth De Backer and Vikram Ranade, examined trends in the pharmaceutical industry and produced an industry analysis report titled “What Are the Drivers Behind M&A in the Pharmaceutical Industry?” incorporating M&A cases from the U.S. pharmaceutical sector in 2018. VCBeat (WeChat Official Account: vcbeat) has translated the main content of this report for our readers.

This report analyzes the long-term drivers of mergers and acquisitions (M&A) in the pharmaceutical industry, concluding that pharmaceutical companies pursue M&A transactions with three core motivations: innovation, synergies, and portfolio optimization.

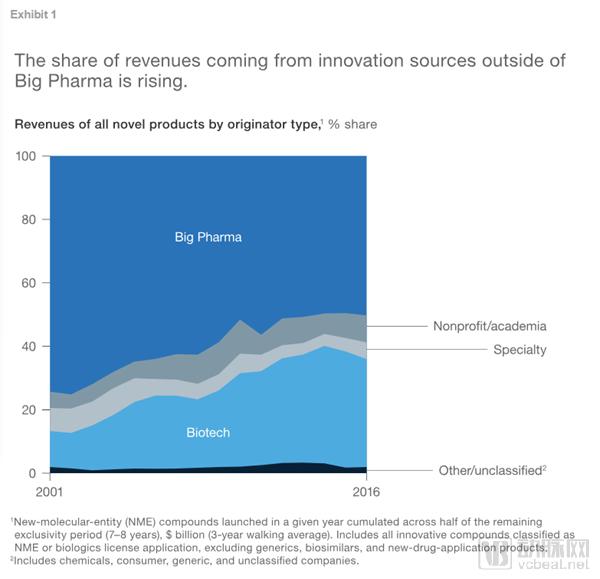

For a long time, large pharmaceutical companies have relied on mergers and acquisitions (M&A) to drive innovation, a trend unlikely to change in the near term. Previous research by McKinsey indicates that the share of innovation-derived revenue originating from outside large pharmaceutical companies increased from 25% in 2001 to 50% in 2016 (see Table 1). The development of new drugs requires substantial upfront investment, while the probability of success remains typically low. Meanwhile, late-stage clinical trials demand significant capital and the ability to navigate complex regulatory pathways—capabilities that large pharmaceutical companies generally possess.

These dynamics have fostered an industry trend in which smaller, creative companies drive innovation. Once their research advances further, large pharmaceutical companies enter the field to seek out the next “new” breakthrough and marshal the necessary resources to fund costly late-stage clinical trials and large-scale commercial marketing campaigns. Regardless of this trend, innovation within the industry will remain fragmented both now and in the future.

Figure 1: The Revenue Share from Innovation Sources Outside Large Pharmaceutical Companies Is Rising

Over the past year, industry interest in several emerging drugs has prompted pharmaceutical companies to seek acquisition targets. The median premium for the 16 listed pharmaceutical companies acquired in the first half of 2018 was approximately 60%. Among the six M&A transactions completed in the first quarter, the median premium paid was around 90%, primarily involving companies focused on immuno-oncology therapies and rare disease treatments—two areas that have recently attracted significant industry attention. For example, on January 16, 2018, Celgene acquired Juno at a 91% premium.

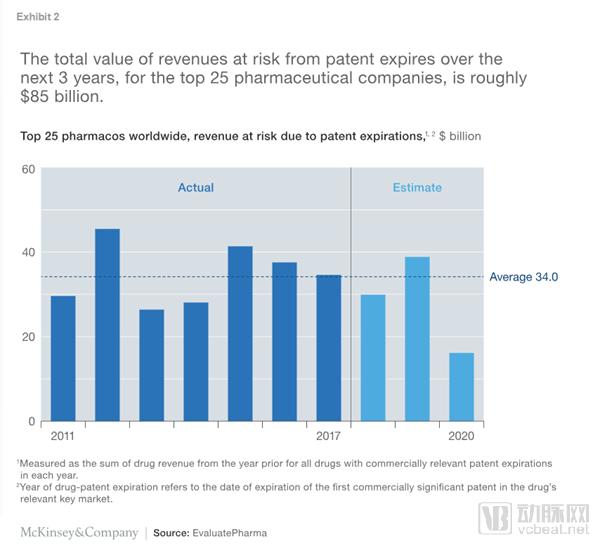

More commonly, pharmaceutical companies must continuously update their portfolios and product pipelines to counteract the inevitable decline in revenue that occurs when brand-name drug patents expire and companies lose their exclusive rights to manufacture and market these products. While accurately predicting the exact expiration dates of brand-name drug patents may not be realistic, general forecasts indicate that the total revenue at risk due to patent expirations over the next three years for the top 25 pharmaceutical companies in the United States amounts to approximately $85 billion (see Table 2).

Figure 2. For the top 25 pharmaceutical companies, the total revenue at risk from patent expiration over the next three years is approximately $85 billion.

This is a considerable amount, but in any consecutive three-year period this century, the revenue lost by companies due to patent expirations has been higher than this figure. Furthermore, pharmaceutical companies rarely wait until they face a “patent cliff” to expand their product pipelines. Therefore, viewed in isolation, this factor should not lead to a significant increase in M&A activity compared with previous years.

Another motive for mergers and acquisitions is to achieve synergies through scale expansion. Taking Takeda as an example, the company acquired Shire in May 2018. Due to the complementary nature of the two companies’ product portfolios and organizational structures, annual run-rate cost synergies of $1.4 billion were projected within three years after the closing of the transaction.

Given the substantial financial and operational benefits that mergers can bring, pharmaceutical companies’ motivation to pursue such transactions is unlikely to change. In fact, to assess future opportunities, Roerich Bansal and his colleagues conducted an analysis of mid-sized and large pharmaceutical and biotechnology companies, categorized by profit margins. The results revealed significant disparities in profit margins: pharmaceutical companies with annual revenues exceeding $1 billion reported EBITDA margins (operating profit as a percentage of total revenue) ranging from 20% to 50%, while biotechnology companies with annual revenues over $1 billion posted EBITDA margins between 30% and 50%. These findings suggest that companies with greater profit margin differentials have more significant opportunities to achieve synergies through acquisitions.

Roerich Bansal’s study did not delve into the specific details of value creation, but he observed that in the early 21st century, when the industry was generally plagued by overcapacity, the companies involved in the largest deals created the most value, with synergies justifying the premium paid for these transactions. In recent years, however, pharmaceutical companies that have been more selective in their transactions, and those that have supplemented smaller deals with partnerships and licensing agreements, have generated the greatest value. This demonstrates that synergies enhance the competitiveness of merging entities, producing a “1+1>2” effect.

Large pharmaceutical and biotechnology companies often adjust their portfolios through transactions, either because their strategies have shifted and they are seeking opportunities to strengthen their commercial pipelines, or because they are divesting assets acquired in previous deals as they are no longer the optimal owners of these assets. In this regard, U.S. tax reform may make it more attractive for American pharmaceutical companies to divest non-core assets compared with prior years. Colleagues of Roerich Bansal estimate that, for a typical company, the after-tax proceeds from divestitures could increase by approximately 23%, driven by lower taxation on sellers’ gains and higher valuations resulting from reduced after-tax cash flows. We have already observed several large healthcare companies divesting non-strategic assets from their portfolios.

As in other industries, competition for the most attractive and innovative assets in the pharmaceutical sector is likely to remain intense, thereby stimulating M&A activity. Strategic acquirers are expected to continue actively sourcing new innovations, such as through early-stage licensing and collaboration agreements, to drive sustained corporate growth.

About the Author

Roerich Bansal is a research expert at the McKinsey Knowledge Center; Ruth De Backer is a partner in McKinsey’s New York office, and Vikram Ranade is an associate partner in the same office.

(Compiled by: Tan Xin)