Entering the Harvest Phase: Global New Pharma Investment and Financing Report 2014–2018

Since 2014, VCBeat has been deeply engaged in the healthcare industry for five years. These five years have witnessed the booming development of the new pharmaceutical sector, encompassing biologics, innovative drugs, and novel therapies. Today, this sector has moved beyond its nascent stage, evolving into a complex network characterized by intricate sub-sectors, a vast number of key stakeholders, and deeply entrenched enterprises.

At this juncture, we have decided to take a closer look at this sector, documenting in our own way the people and events that the industry has encountered or will face. The VCBeat New Medicine WeChat official account (biobeat1) marks our new starting point in this field, but it is by no means the end. We will continue to engage in dialogues with more innovators in the new medicine sector, sharing entrepreneurial stories, uncovering cutting-edge cases, and thereby researching the future development of the industry.

Thank you for your continued support and understanding of VCBeat. We will continue to accompany you on the journey ahead.

1. 2014 marked the inaugural year for the new pharmaceutical sector. We define 2014 as the critical starting point for this emerging field;

2. The year 2018, which has just passed, marked another critical turning point in the field of innovative medicine. Genetic testing showed a decline in performance during this period, while immunotherapy and gene therapy secured substantial financing and emerged as new focal points of attention;

3. To date, investment and financing activities in the new pharmaceutical sector remain concentrated at Series A and earlier stages; however, there is a gradual trend toward later-stage rounds.

4. Domestic and international stakeholders have different focal points in the new pharmaceutical sector: China places greater emphasis on biopharmaceutical companies and molecular diagnostics, while overseas markets show stronger interest in precision medicine. However, over the past two years, China has also been shifting toward precision medicine, which may emerge as a new investment trend.

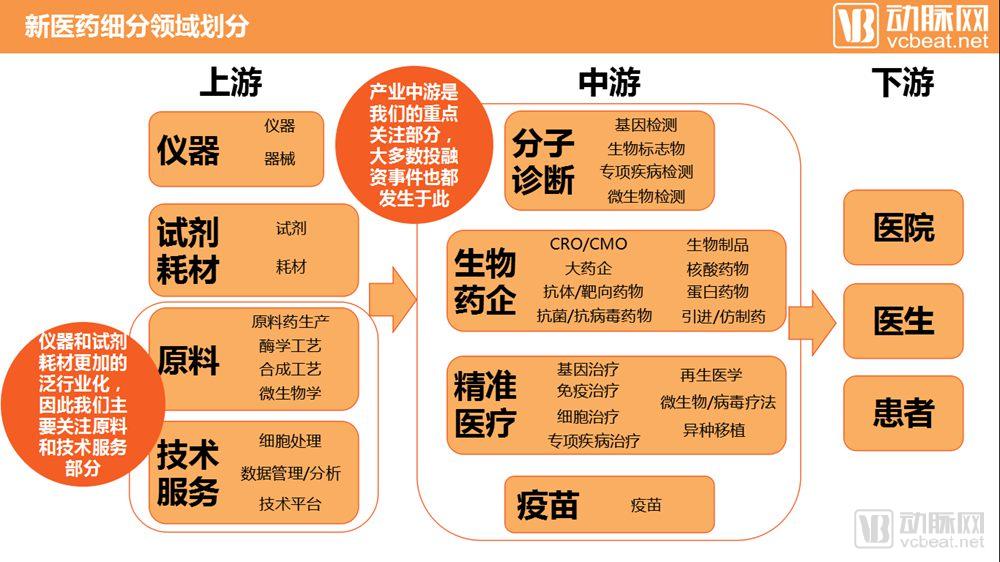

With hospitals, physicians, and patients as downstream clients, we have divided the upstream and midstream segments of the innovative pharmaceutical industry into four subsectors each. The upstream segment includes instruments, reagents/consumables, raw materials, and technical services; the midstream segment encompasses molecular diagnostics, biopharmaceutical companies, precision medicine, and vaccines. Each subsector is further categorized with detailed secondary tags.

Instruments, reagents, and consumables belong to more generalized, industry-specific subsectors; therefore, when discussing industry development in the new pharmaceutical sector, we primarily focus on the other six subsectors.

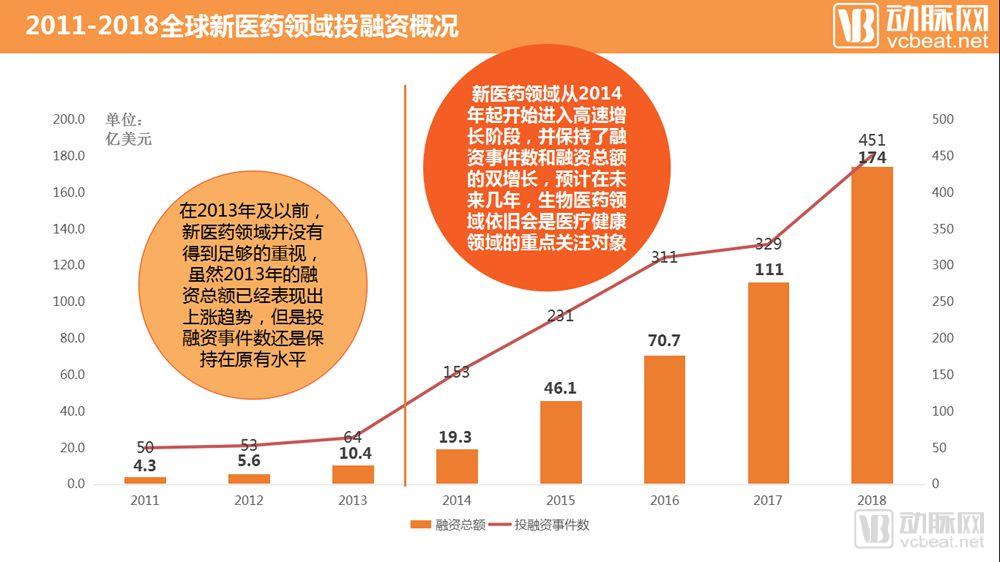

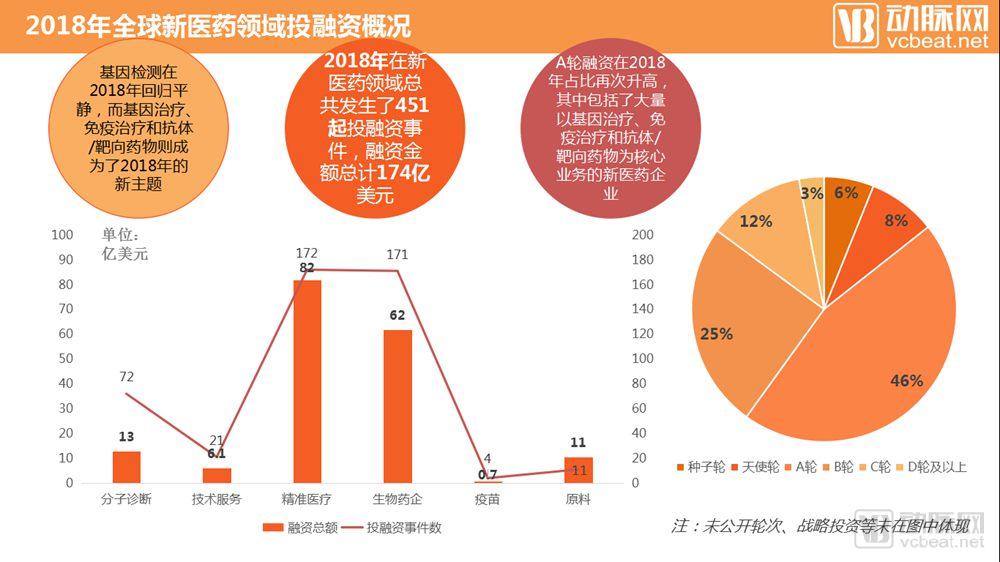

In 2018, a total of 451 financing and investment transactions occurred in the new pharmaceutical sector, representing a year-on-year increase of 37.08%; the total financing amount reached $17.4 billion, a year-on-year increase of 56.8%.

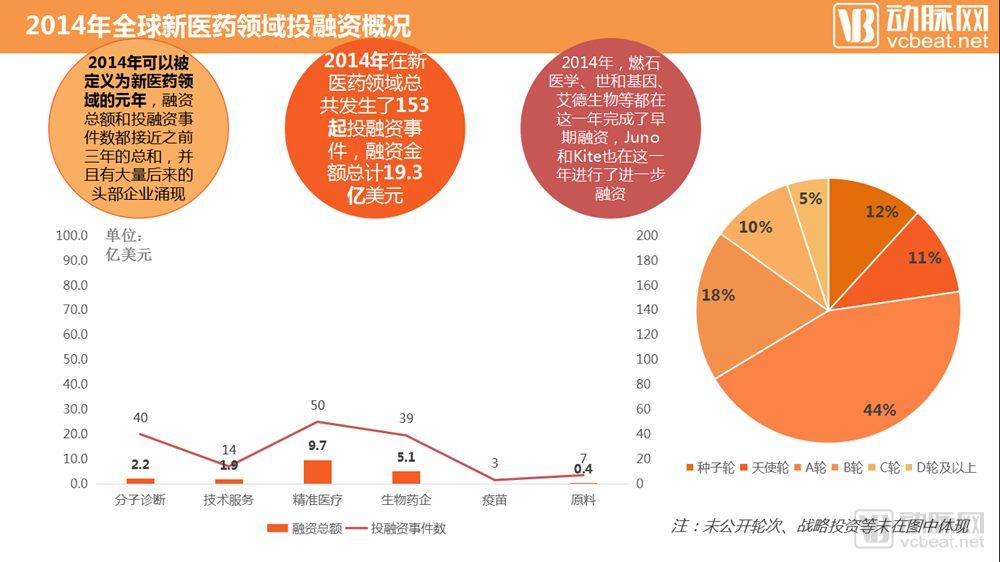

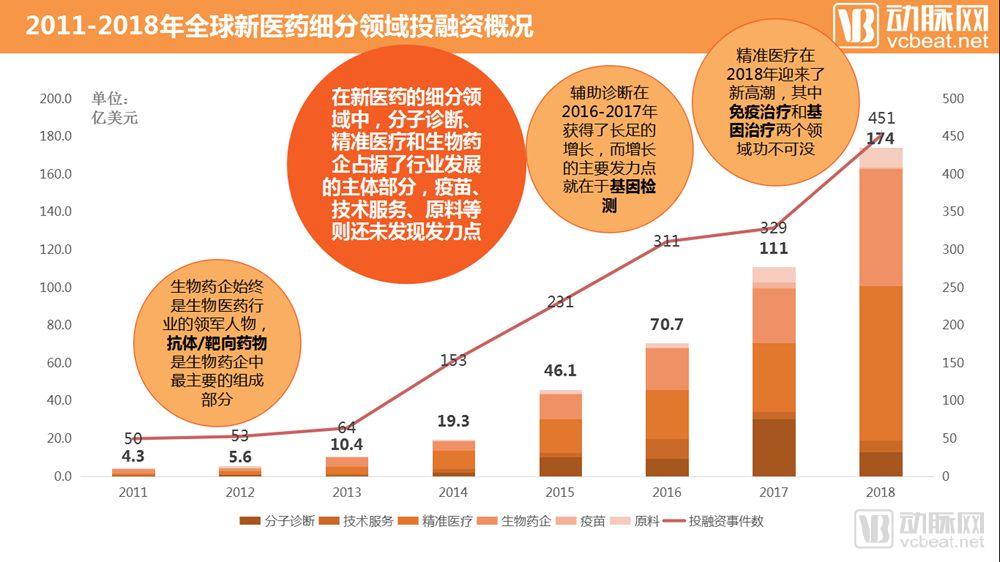

Looking back at the history of investment and financing in the innovative pharmaceutical sector, we find that 2014 was a pivotal milestone in its development. In that year, the number of investment and financing deals in the sector rose from 64 in 2013 to 153, representing a year-on-year increase of 139.1%; the total financing amount increased from USD 1.04 billion in 2013 to USD 1.93 billion, a year-on-year growth of 85.6%. From 2015 to 2018, the innovative pharmaceutical sector sustained this growth momentum, reaching a peak in 2018 with 451 investment and financing deals totaling USD 17.4 billion. Given the current trajectory of the sector, this momentum is unlikely to wane in the coming years; rather, it is poised to intensify further.

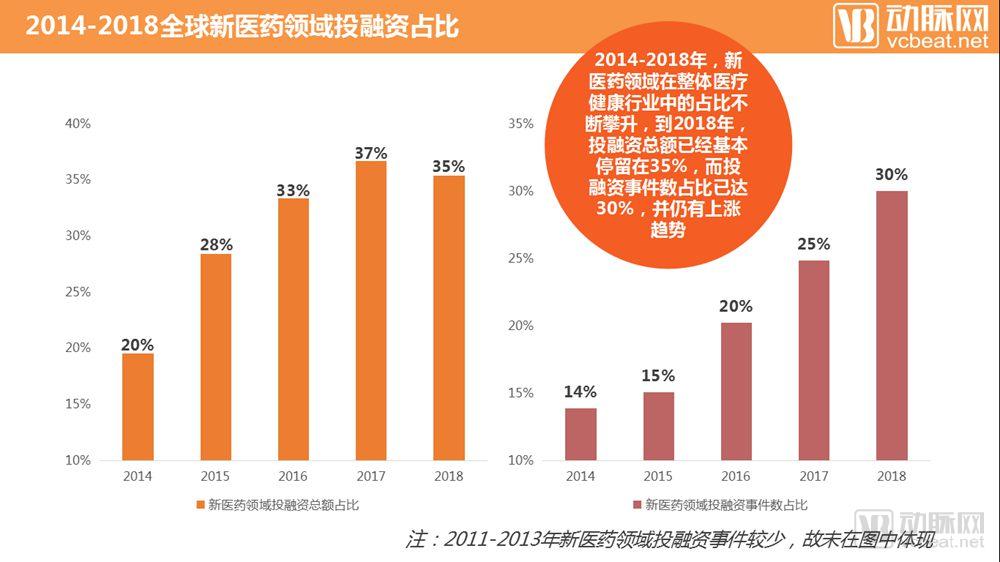

From 2014 to 2018, both the proportion of total investment and financing amount and the proportion of the number of investment and financing events in the new pharmaceutical sector maintained an upward trend. Currently, the total investment and financing amount accounts for a stable share of approximately 35% of the entire healthcare industry, while investment and financing events account for 30%. It is expected that the new pharmaceutical sector will be able to maintain this share in the future, becoming the largest component of the healthcare industry.

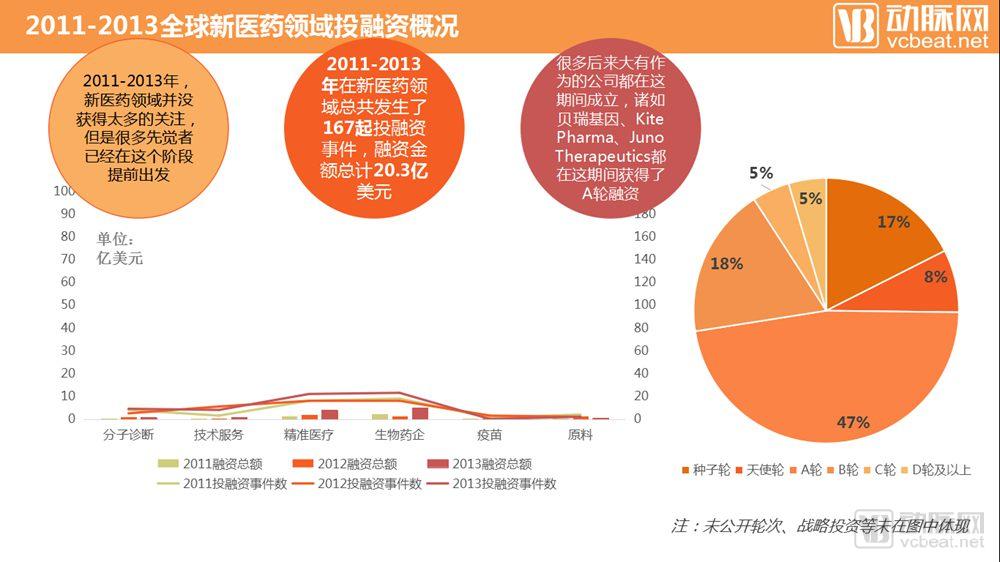

2011–2013 were the wild, nascent years before the emergence of the new pharmaceutical sector. Although financing and investment activities in this field attracted limited attention during that period, many companies that would later achieve remarkable success were either founded or secured early-stage funding at that time, including Berry Genomics, Annoroad Gene Technology, Kite Pharma, and Juno Therapeutics.

In 2014, following the industry’s nascent stage, the new medicine sector witnessed a surge in financing and investment activities. As the industry was just taking off, the majority of these deals were concentrated at Series A and earlier stages. Nevertheless, many of the companies that secured funding in 2014 have since emerged as leading players in the new medicine field. BGI Genomics completed three consecutive rounds of financing that year; Berry Genomics closed its Series C round; and Burnstone Medicine, Geneseeq, AmoyDx, and Haloplex all secured early-stage funding. Additionally, leading international CAR-T therapy companies Kite Pharma and Juno Therapeutics also chose to raise further capital in 2014.

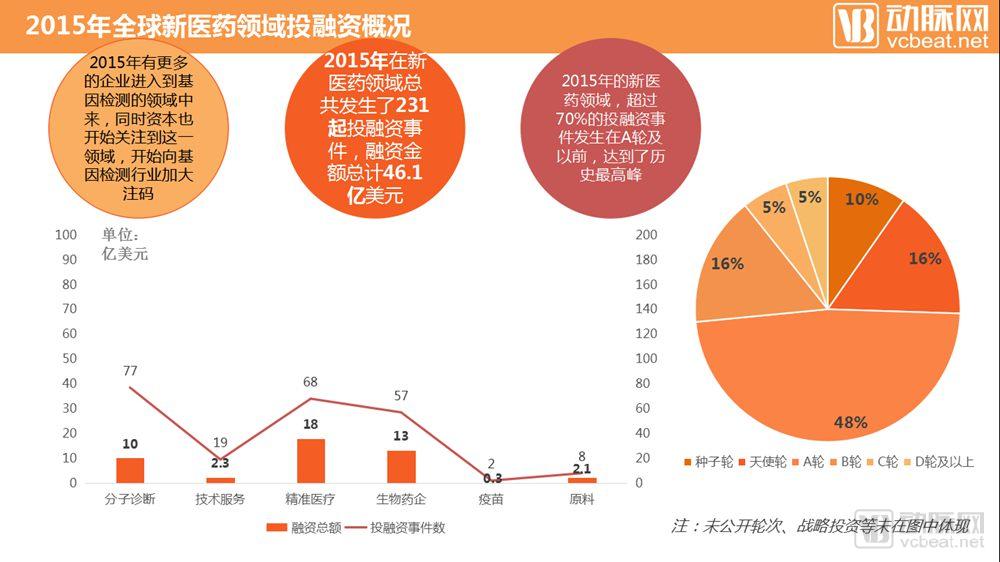

2015 was a continuation of the trend set in 2014. An increasing number of new entrants, following the prevailing market momentum, led to pre-Series A financing and investment activities accounting for nearly 75% of all such transactions that year. Meanwhile, capital began to favor the growth prospects of the innovative pharmaceutical sector. In 2015, total investment and financing in this sector reached USD 4.61 billion, representing a year-on-year increase of 138.9%. Molecular diagnostics, dominated by genetic testing, emerged as the fastest-growing subsector in 2015, a trend that had already shown early signs in 2014.

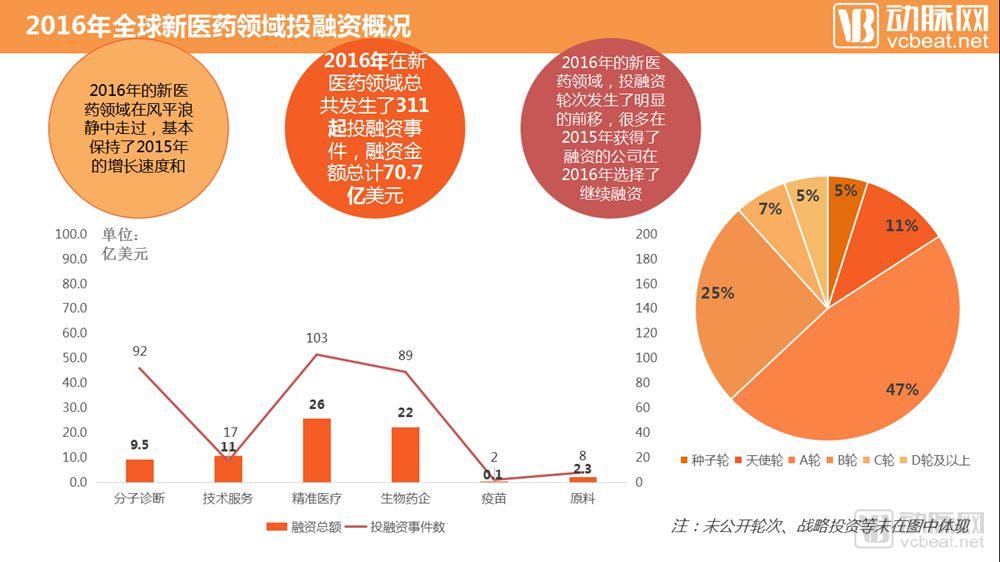

The biopharmaceutical sector continued to show strong performance across the board in 2016. Following the influx of numerous companies into the field during 2014–2015, some gradually validated their business models and proceeded with further financing rounds. Concurrently, a significant number of new entrants continued to join the sector, either by identifying novel entry points or leveraging strong founding teams. As a result, although the overall timing of investment and financing rounds shifted later in 2016, early-stage deals (Series A and earlier) still accounted for a substantial proportion of total transactions.

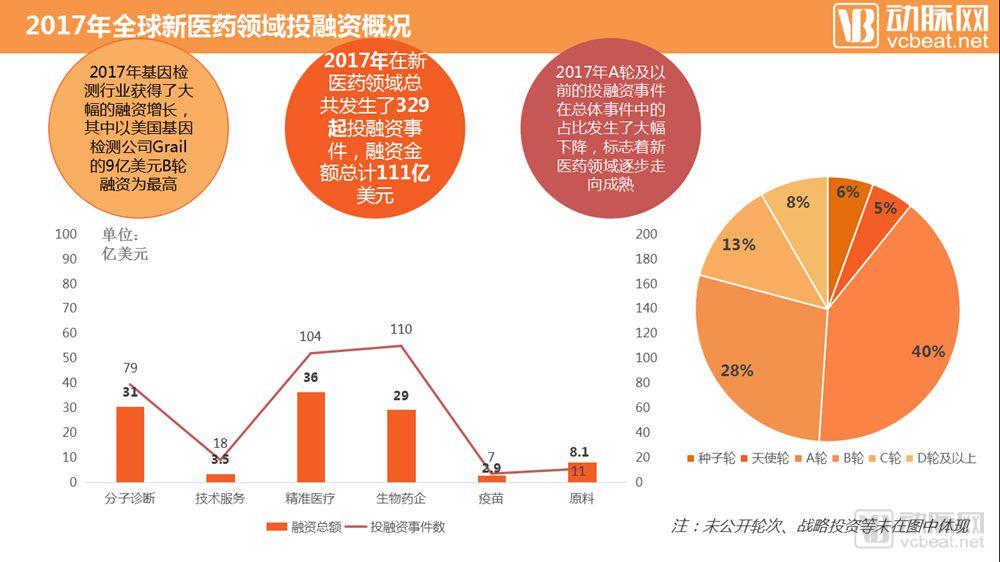

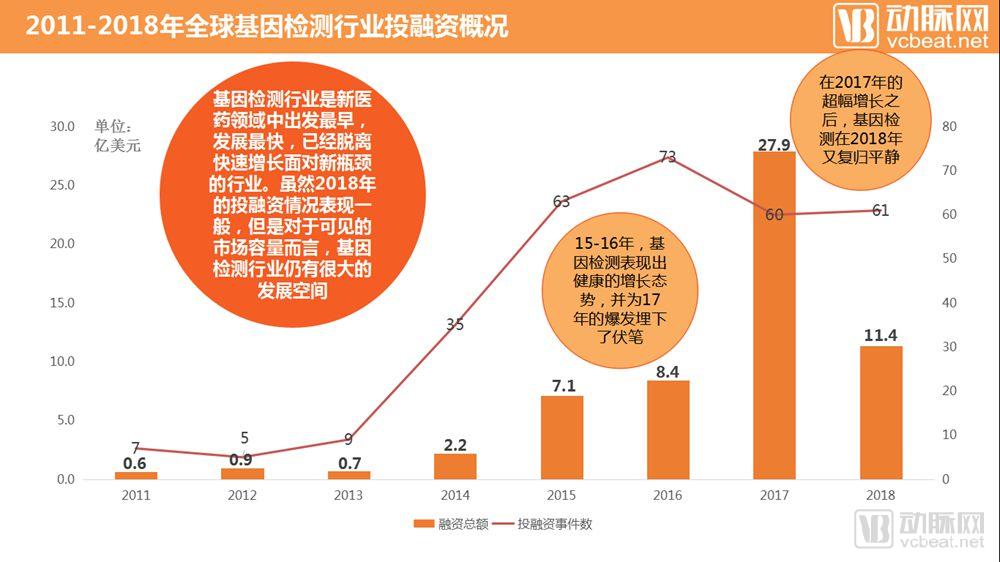

In 2017, the new pharmaceutical sector reached a new peak. While the number of financing and investment events saw only modest growth, the total amount continued to surge at a high rate, surpassing $10 billion. During this year, the proportion of financing and investment events at Series A and earlier stages shrank significantly, replaced by a large number of Series B and C deals. Led by genetic testing, the molecular diagnostics industry hit a peak of $3.1 billion, simultaneously laying the groundwork for the rapid cooling that would follow in the future.

The year 2018, which has just passed, may mark another new starting point for the innovative pharmaceutical sector. While total financing amounts and the number of investment and financing deals continued to grow rapidly, subtle shifts occurred in the development of specific subsectors. The proportion of Series A and earlier-stage investment and financing deals rose again, encompassing a large number of emerging companies primarily focused on biologics and precision medicine. After a major surge in 2017, the molecular diagnostics industry cooled down sharply, securing only $1.3 billion in total financing in 2018.

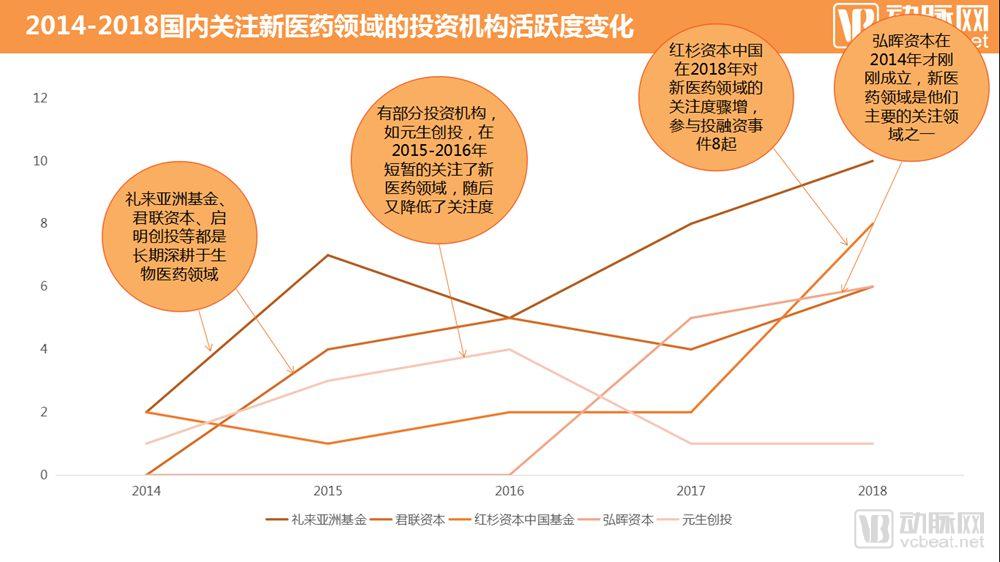

Over the past five years, among the top ten institutions most active in investment and financing transactions, only Lilly Asia Ventures is rooted in China, while the others are primarily foreign-based investors.

Mergers and acquisitions (M&A) also reflect shifting trends in the healthcare sector. In early 2019, the largest M&A deal in the history of the healthcare industry took place, with Bristol-Myers Squibb acquiring Celgene for $74 billion. Celgene, known for its aggressive acquisition strategy, was ultimately acquired by another player. Meanwhile, since 2014, many traditional pharmaceutical giants have been actively involved in M&A activities within the innovative medicine space. World-class pharmaceutical companies such as Johnson & Johnson, Pfizer, Eli Lilly, and Gilead Sciences have all entered the field of innovative medicines through mergers and acquisitions.

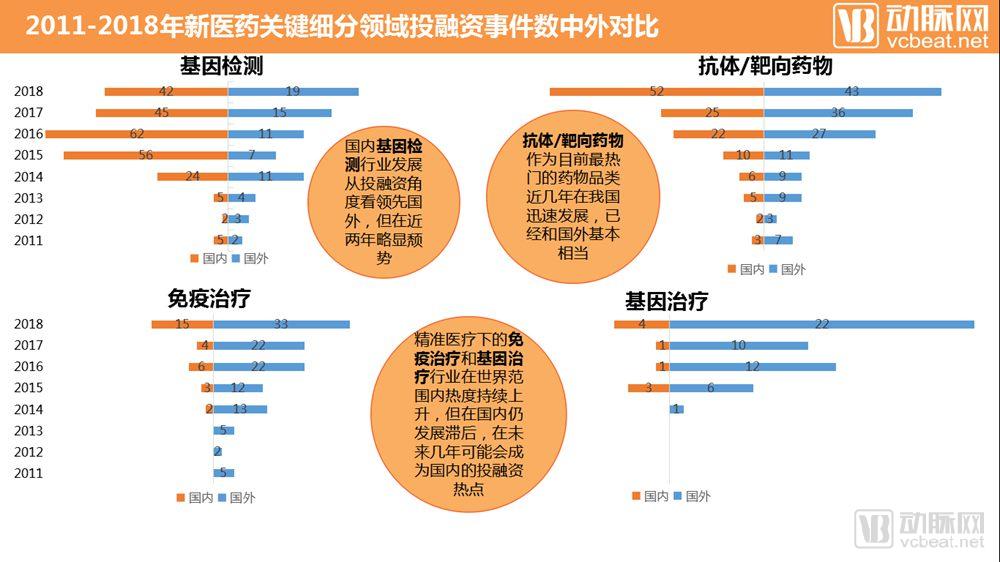

Among the six key subsectors we focus on, technical services, vaccines, and raw materials account for a relatively small share of the overall landscape and have not exhibited clear development trends over the past five years. Therefore, our discussion of subsector dynamics primarily centers on the remaining three areas. From 2014 to 2017, the three primary sectors—molecular diagnostics, biopharmaceutical companies, and precision medicine—largely advanced in tandem. However, in 2018, there was a significant shift in financing allocation. These changes were most pronounced in four secondary sectors: genetic testing, targeted/antibody drugs, immunotherapy, and gene therapy.

The genetic testing industry has carved out its own unique trajectory during its development. When it emerged in 2014, the sector took a significant leap forward, rapidly reaching a historical peak of $2.79 billion in 2017. In contrast, the genetic testing field appeared somewhat subdued in 2018, with total financing amounting to less than half of that in 2017. This decline may be attributed to funding difficulties amid a market winter, or possibly because the capital raised in 2017 was sufficient to support the industry’s future growth. However, setting aside the exceptional performance of 2017, the financing landscape in 2018 actually remained consistent with the growth curve observed from 2014 to 2016. The genetic testing industry has not stagnated; rather, it has entered a bottleneck phase. It is believed that once the industry breaks through this current bottleneck, it will once again become a favorite among investors.

Immunotherapy and antibody/targeted therapy have followed similar development trajectories in recent years. Both sectors have exhibited standard exponential growth curves over the past few years. Notably, in 2018, total financing in the immunotherapy sector increased by 84.8%, while that for antibody/targeted drugs rose by 121.1%. Both areas have been focal points in the emerging pharmaceutical industry in recent years. Targeted therapies against PD-1, PD-L1, EGFR, and other targets have emerged in rapid succession, while the increasing maturity and widespread adoption of CAR-T therapy has propelled immunotherapy into the spotlight. Although these two subsectors have already attracted significant attention within the industry, they still possess substantial room for growth. Therefore, immunotherapy and antibody/targeted therapy will remain central topics of discussion in the emerging pharmaceutical field in the coming years.

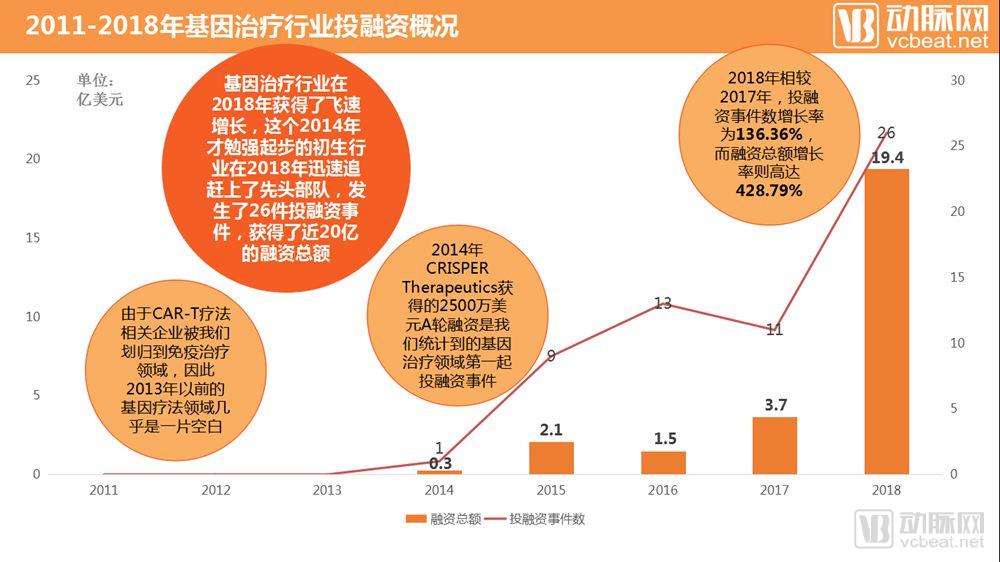

The concept of gene therapy garnered significant hype in 2018, with total financing surging by 428.8%. The crux of gene therapy lies in its potential to address many diseases that are intractable to conventional treatments, such as autoimmune disorders and genetic diseases. While traditional therapeutic approaches can only intervene in and control these conditions without eradicating them, gene therapy has the capacity to target the root causes of pathogenesis, thereby offering a cure for these stubborn and difficult-to-treat ailments. Whether 2018 represented merely a concentrated speculative bet by capital or the inaugural year for the industry’s takeoff remains to be seen; nevertheless, the sector’s remarkable ability to attract investment and its future growth potential continue to make it one of the most noteworthy subsectors within the innovative pharmaceutical landscape.

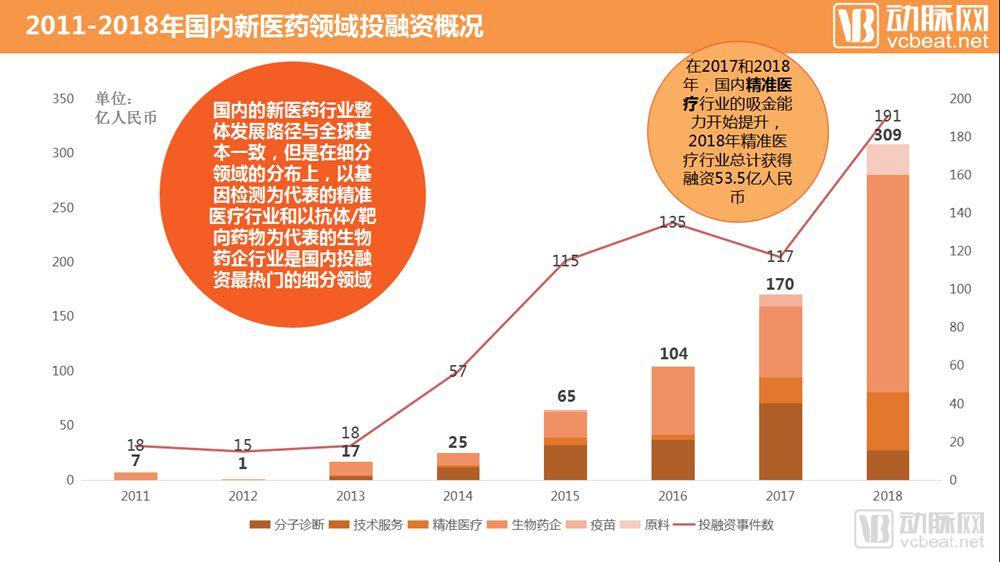

The overall development trajectory of China’s innovative pharmaceutical sector mirrors global trends. 2014 marked a significant milestone in China, with the number of investment and financing deals surging to 57, exceeding the total of the previous three years combined. In 2018, the country’s innovative pharmaceutical sector experienced another upswing, with nearly 200 investment and financing deals and total funding surpassing RMB 30 billion.

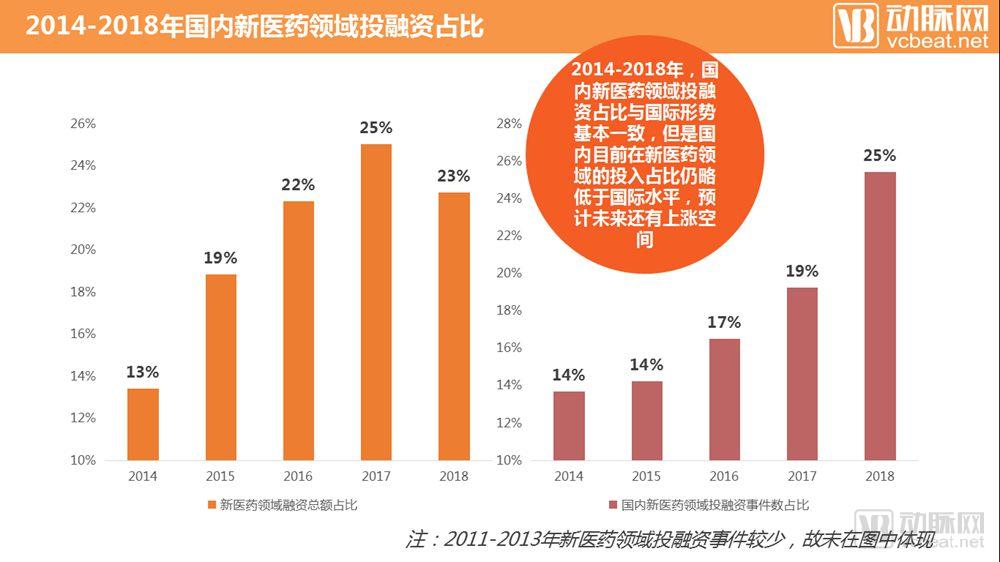

The shift in the proportion of China’s innovative pharmaceutical sector within the broader healthcare industry mirrors global trends. However, since its inception, investment in this sector in China has consistently lagged behind global levels, with both the share of financing deals and the share of total funding amounting to 5–10 percentage points lower than global figures. Currently, financing deals in China’s innovative pharmaceutical sector account for approximately 25% of those in the overall healthcare industry, while its share of total funding remains stable at around 25%.

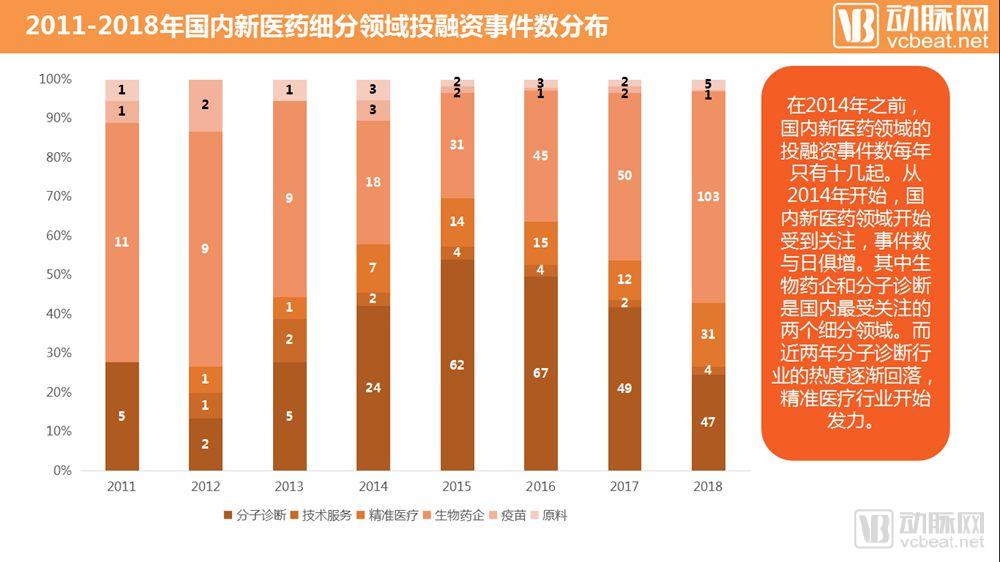

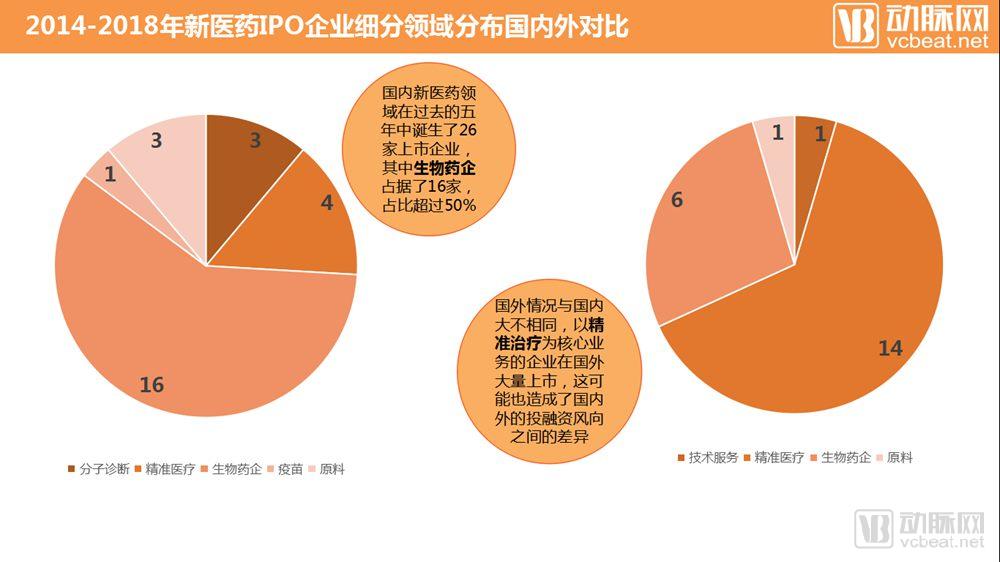

In terms of distribution across sub-sectors, domestic investment in the new pharmaceutical field is primarily concentrated in molecular diagnostics and biopharmaceutical companies. While precision medicine has garnered significant global attention, its profile in China remains relatively modest, although interest has been accelerating over the past two years. The molecular diagnostics industry, after experiencing a surge in popularity during 2015–2016, has gradually cooled in recent years. In contrast, biopharmaceutical companies have maintained a trajectory of rapid growth, with the number of financing and investment transactions exceeding 100 in 2018 alone.

Domestic investment and financing activities remain dominated by Series A and earlier rounds; however, Series B and later rounds now account for a significant share of the total. Aligning with global trends, China’s innovative pharmaceutical sector is gradually transitioning from its nascent stage toward maturity. Nevertheless, in the coming years, Series A and earlier deals are likely to continue constituting the majority of domestic investment and financing activities. This is because many subsectors within the innovative pharmaceutical industry remain underdeveloped in China, leaving ample room for new entrants.

Among investment institutions focusing on the Chinese market, attitudes toward the new pharmaceutical sector vary significantly. Firms such as Lilly Asia Ventures, Legend Capital, and Qiming Venture Partners have maintained a long-term focus on this sector, initiating investments when it was still in its infancy and steadily increasing their deal activity year over year. Some investors, notably Sequoia Capital China, did not initially prioritize the new pharmaceutical space but have significantly ramped up their commitments and expanded into this field over the past two years. Conversely, certain institutions that were highly active in financing and investment deals within the new pharmaceutical sector between 2014 and 2016 have since faded from the scene. Hui Capital stands out as a special case: established in 2014, it identified the new pharmaceutical sector as one of its core focus areas from inception.

Between 2014 and 2018, biopharmaceutical companies accounted for the majority of large-scale financing and investment transactions in China’s emerging pharmaceutical sector. There were 12 deals exceeding USD 150 million; two occurred in the molecular diagnostics industry, two in the precision medicine industry, and the remaining eight all involved biopharmaceutical companies. The landscape of China’s emerging pharmaceutical sector reflects this trend: biopharmaceutical companies remain the dominant component. Although other segments are developing concurrently, they have not yet reached the scale achieved by biopharmaceutical companies in China.

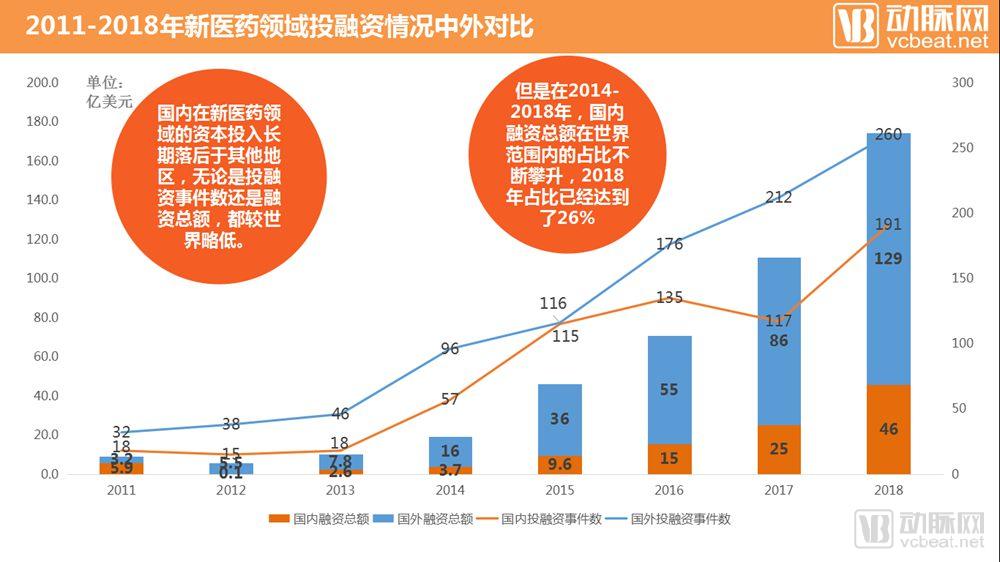

To date, domestic investment in the field of innovative pharmaceuticals still cannot compare with that of foreign countries. Foreign investment in this sector surpassed $10 billion in 2018, whereas China’s stood at only $4.6 billion. However, China’s share of the global total is gradually increasing, reaching 26% in 2018.

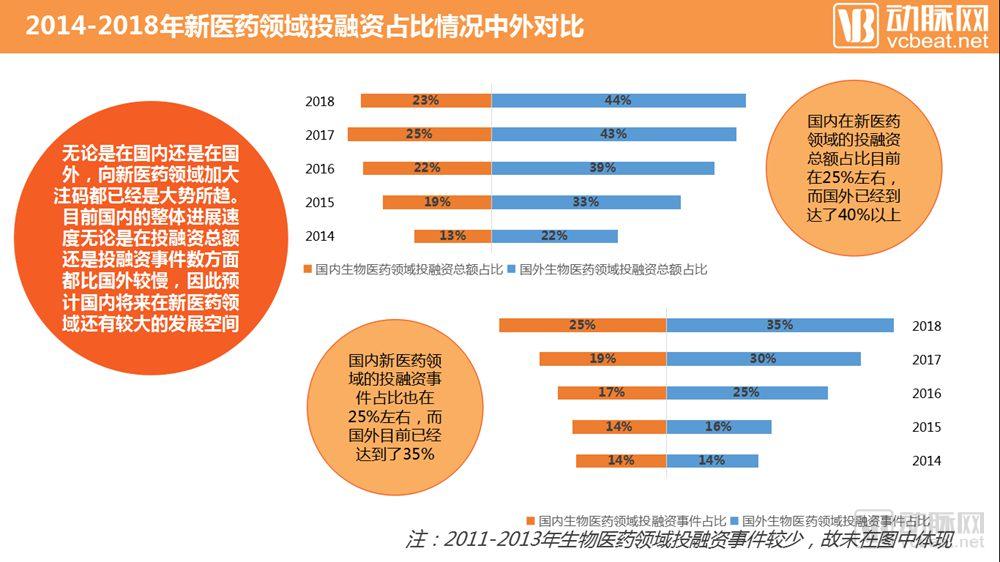

In 2018, the share of the emerging pharmaceutical sector within the overall healthcare industry abroad reached 44% in terms of total financing amount and 35% in terms of the number of investment and financing deals. In contrast, China’s figures stood at only 23% and 25%, respectively. There remains a significant gap between domestic and international attention paid to the emerging pharmaceutical sector, which is unlikely to be reversed in the short term. However, given the numerous untapped niche segments within this field, China still has ample opportunities to catch up.

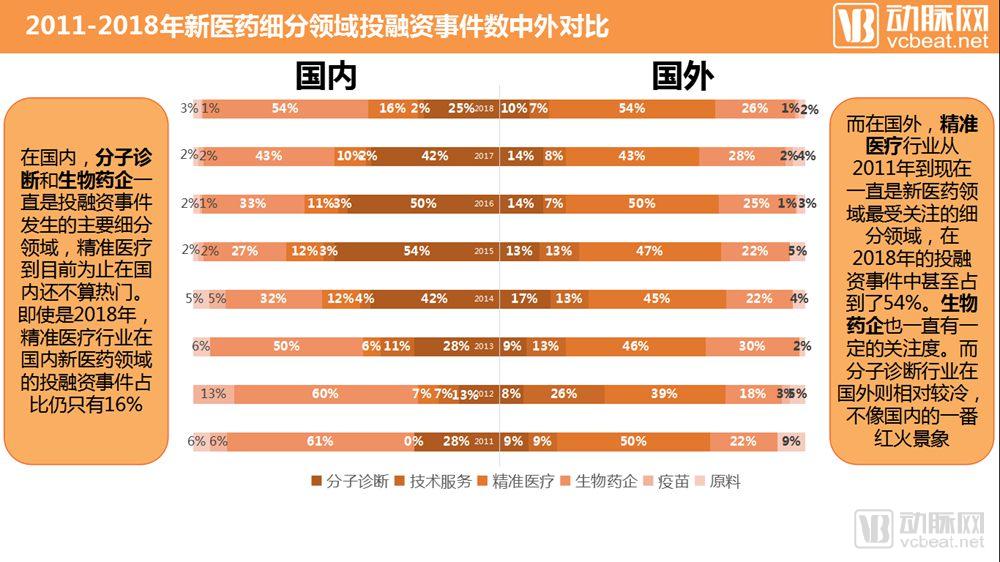

There are significant differences in investment patterns within niche sectors between China and other countries. In China, biopharmaceutical companies and molecular diagnostics are developing rapidly; whereas abroad, precision medicine has already captured a substantial market share. This represents the primary gap between domestic and international markets in the new pharmaceutical sector. While investment levels in biopharmaceuticals and molecular diagnostics are broadly comparable between China and other countries, foreign markets have pulled far ahead in the field of precision medicine.

A similar disparity was observed in IPO activities within the new pharmaceutical sector from 2014 to 2018. In China, these listings were still dominated by biopharmaceutical companies and molecular diagnostics firms, whereas abroad, they occurred almost exclusively in the precision medicine industry.

When we examine more specialized subfields, the gap between China and other countries becomes even more pronounced. Domestic investment in genetic testing and antibody/targeted therapies is roughly on par with international levels, with China even taking a lead in genetic testing. However, there remains a substantial disparity in precision medicine areas such as immunotherapy and gene therapy. The good news is that China’s precision medicine sector experienced rapid growth in 2018, with both the number of financing events and the total amount of capital raised increasing significantly compared to the previous year.

Driven by the accelerated development of China’s precision medicine industry in 2018 and the current lag in its progress, the sector is likely to experience a surge over the next two years, with capital inflows attracting a wave of top-tier new talent. To download the full report in PDF format, please scan the QR code to follow the “VCBeat New Medicine” WeChat official account and reply with “report” to initiate the download.

Scan the QR code to follow the VCBeat New Medicine official account (biobeat1)