2019 Biopharma Trends: Targeted and Antibody Therapies Lead Investment; Rare Diseases and Gene Therapy Emerge as Key Opportunities

For the biotechnology and pharmaceutical industries, 2018 was another extraordinary year. According to the VCBeat database, a total of 1,410 transactions took place globally in the healthcare sector in 2018, involving a total amount of $38.801 billion. Among these, the biotechnology and pharmaceutical industries were the absolute mainstream of the era: with 309 transaction events and financing amounts reaching as high as $13.845 billion, they undoubtedly led other industries by a wide margin, once again securing the top position in healthcare investment and financing.

On the other hand, the global market experienced a capital winter in 2018, with many speculating that startups would face even greater challenges in 2019. For both investors and enterprises, every step became critically important. Those who could accurately assess the situation were poised to go further in this process.

To this end, VCBeat (biobeat1) has re-extracted and compiled data on global biopharmaceutical investment and financing events in 2018, as well as drug approval trends in China and the United States, from the “Report on Investment and Financing Data in the New Pharmaceutical Sector (2014–2018).” This analysis aims to forecast development trends in the biopharmaceutical industry for 2019, providing valuable insights for industry professionals.

Targeted Therapies and Antibody Drugs Lead Investment Rankings

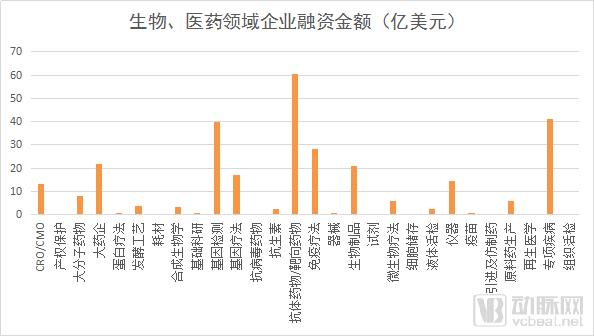

Based on investment and financing data from 2014 to 2018, antibody drugs/targeted therapies, genetic testing, immunotherapy, and specialty disease medications are currently the subsectors attracting the most capital attention. Among these, antibody drugs/targeted therapies firmly hold the top spot on the investment and financing hotspot list, with a total funding amount of $6.064 billion.

A total of 40 financing events occurred in the antibody drug and targeted therapy sectors, with an average deal size reaching hundreds of millions of U.S. dollars, making these fields a hotspot for high-value investments. In recent years, innovative oncology drug development has been regarded as a new investment focus in pharmaceutical R&D, among which antibody drugs and targeted therapies have attracted particular attention.

Targeted drugs act on specific targets involved in tumor growth, enabling intervention against tumors with minimal damage to normal cells. Antibody-based drugs also leverage targeting specificity and disease progression pathways to intervene in disease, offering enhanced target specificity and therapeutic efficacy.

The first targeted therapy was approved in 1997. Today, targeted therapies and antibody-based drugs have become important treatment modalities in clinical oncology, potentially realizing the goal of transforming this malignant disease into a chronic condition.

However, precisely because these two drugs are already widely used in clinical practice, most companies’ development has entered the mid-to-late stages. With intense competition and generally high corporate valuations, most institutions focused on early-stage investment may choose not to enter the market; for those specializing in late-stage investment, it is precisely the season for reaping returns.

A total of 75 financing and investment deals were focused on specific diseases, making this the most active subsector in terms of deal volume. Most of these diseases are related to cancer, cardiovascular diseases, and neurodegenerative disorders. In recent years, R&D for cardiovascular and oncology drugs has consistently been a hotspot for investment. In comparison, research into Alzheimer’s disease is more cutting-edge.

Similar to diabetes and cardiovascular disease, the risk of developing Alzheimer’s disease increases with age. As population aging intensifies, the social burden imposed by age-related diseases has become increasingly prominent. However, while diabetes remains incurable, it can be managed with medication. To date, the pathogenesis of Alzheimer’s disease remains unclear, and no therapeutic drugs are available. It can be said that Alzheimer’s disease, sweeping across every corner of the globe alongside the significant extension of global life expectancy, is one of the few conditions for which humanity currently has no effective countermeasures.

In November 2017, Bill Gates personally committed $100 million to research on the treatment of Alzheimer’s disease. He allocated $50 million of this amount to the Dementia Discovery Fund, a venture capital fund, and the remaining $50 million will be invested in startups focused on Alzheimer’s disease research.

Among the companies that secured financing in 2018, 27 were engaged in Alzheimer’s disease-related businesses. Prominent pharmaceutical companies and venture capital firms—including Johnson & Johnson, Eli Lilly, WuXi AppTec, Pfizer, ARCH Venture Partners, Sequoia Capital, and OrbiMed—invested nearly $500 million.

The prolonged market void has brought about a duality: on one hand, patients face anxious waits; on the other, there are unprecedented opportunities. In recent years, major breakthroughs in Alzheimer’s disease research have emerged frequently. Leading venture capital firms specializing in early-stage life sciences investments have already begun to act, while institutions focused on cutting-edge technologies have entered a phase of strategic planning.

In October 2017, the market launch of Spark Therapeutics’ Luxturna sparked a frenzy among companies and investors across the gene therapy sector. With the first true gene therapy finally reaching the market, an influx of capital and startups entered the field.

On the corporate front, according to the “2018 Global Gene Therapy Research Report” by the leading international think tank Jain PharmaBiotech, more than 183 companies worldwide are engaged in gene therapy research—over four times the number in 1995—with more than 2,000 clinical projects underway.

Clinical research on gene therapy dates back to the 1990s. Due to early technological limitations and an incomplete understanding of diseases, the development of gene therapy was less than satisfactory. However, with the refinement of foundational technologies such as gene editing and viral vectors, along with improved understanding of diseases and tissues, the safety and efficacy of gene therapy are increasingly maturing.

First, the emerging company Spark achieved a breakthrough. Subsequently, three leading scientists in the field of gene editing—Feng Zhang, David Liu, and J. Keith Joung—jointly founded Beam Therapeutics, a gene therapy research company. Later, Editas Medicine, another gene editing company in which Feng Zhang is involved, announced approval to commence clinical trials for Leber Congenital Amaurosis 10 (LCA10). After three decades of setbacks, gene therapy technology is rapidly advancing, becoming a powerful tool for humanity to overcome various genetic and acquired diseases. Genetic immune disorders, blood diseases, and neurodegenerative conditions represent areas where current biological and chemical drug research has struggled to make significant breakthroughs.

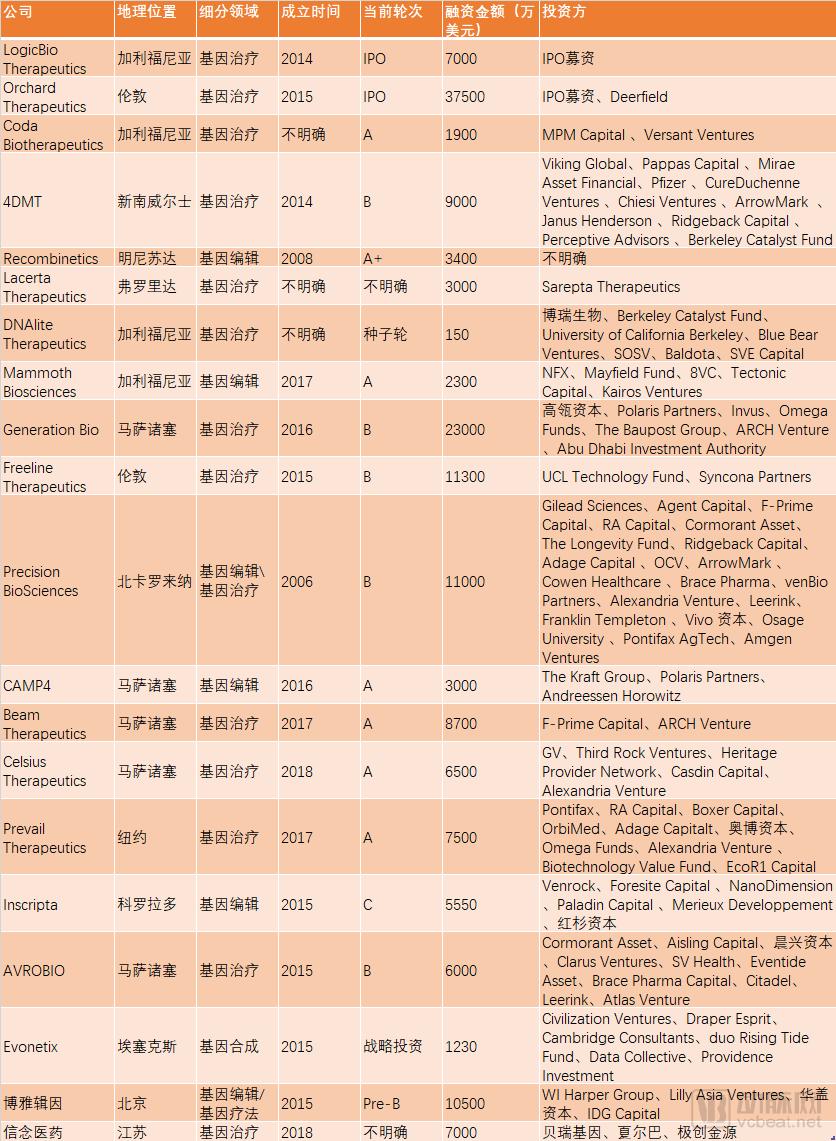

VCBeat’s database shows that in 2018, a total of 17 gene therapy companies worldwide secured financing, with capital investments in the field reaching $1.7 billion.

Although the majority of financing and investment activities have taken place overseas, leading investment firms such as Lilly Asia Ventures and IDG Capital are also quietly making strategic moves within China through several rounds of investments. Gene therapy has long set off a trend abroad, and this wave is poised to rapidly sweep across the Chinese market as well.

While capital support provides the fuel for industry advancement, the role of policy and regulatory approval cannot be overlooked. When an emerging technology gains regulatory endorsement, the sector is bound to attract greater investments of human and material resources. As policy approvals serve a guiding function for the industry, analyzing annual drug approval trends by regulatory authorities is essential for forecasting future development.

The China NMPA approved a total of eight new drugs throughout the year, namely Albuvirtide, Anlotinib, PEGylated Recombinant Human Granulocyte Colony-Stimulating Factor (Sulfated), Danoprevir, Pyrotinib, Fruquintinib, Toripalimab, and Sintilimab.

Since the release of the “Announcement on Conducting Self-Inspection and Verification of Clinical Trial Data for Drugs” in July 2015, regulatory authorities have raised requirements for drug clinical trials and marketing applications to what is regarded as the “strictest standards in history.” In the aftermath, companies with “core proprietary technologies” managed to break through the competitive landscape and attract capital market attention. The approval of these drugs in 2018 was viewed as the emergence of the first batch of outcomes after years of preparation.

In addition to the improvement in drug quality, we have also observed an acceleration in drug approval speeds by regulatory authorities.

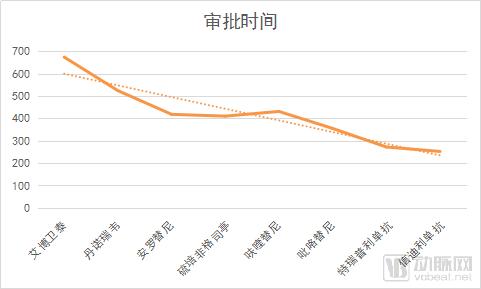

From the 674 days for Albuvirtide (handled in July 2016) to the 252 days for Sintilimab (handled in April 2018), we can observe the regulatory authorities’ proactive stance toward major innovations and drugs addressing urgent social needs. These measures have bolstered the confidence of capital markets and enterprises, encouraging continued research and development of innovative, high-quality domestically produced drugs.

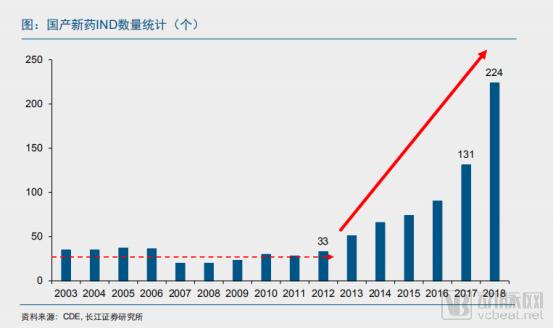

Not only has the number of new drug approvals increased, but the number of Investigational New Drug (IND) applications accepted by the National Medical Products Administration (NMPA) this year has also reached a record high in nearly 15 years. According to data from Changjiang Securities Research Institute, the number of domestically produced INDs reached 224 in 2018, representing a 71% year-on-year increase from 131 in 2017.

Image from Changjiang Securities Research Institute

The dual improvement in both the volume and efficiency of regulatory submissions, coupled with stringent data quality control throughout the entire process, will inevitably lead to a breakthrough in the number of new drugs within a certain timeframe. The year 2018 is regarded as Year One of the rise of innovative drugs in China; the approvals granted that year were merely the beginning, and it is believed that more medications with significant clinical value will enter the market in the coming years.

Products Expected to Launch in 2019

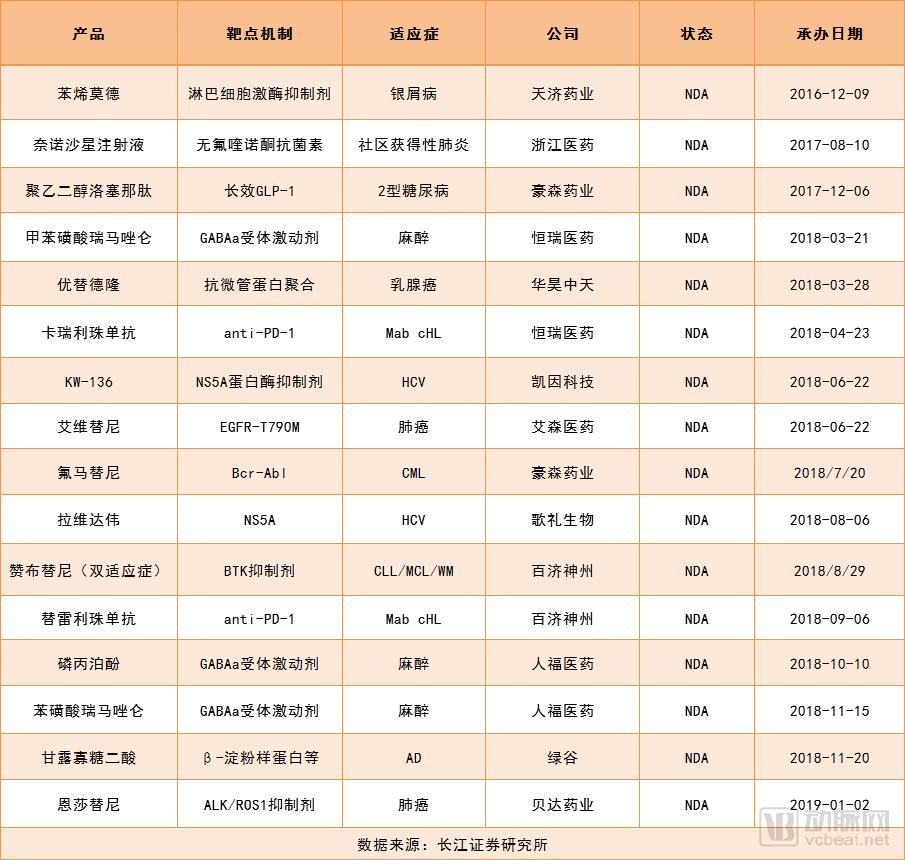

In 2018, 15 domestically produced new drugs were submitted for marketing approval in China. The number of approved domestically produced new drugs is expected to increase further in 2019, with the fruits of new drug innovation beginning to materialize from 2018 onward. Citing data from Changjiang Securities Research Institute, it is highly likely that more than 10 domestically produced new drugs will be approved in 2019, among which anti-tumor drugs will account for the largest share, potentially reaching seven.

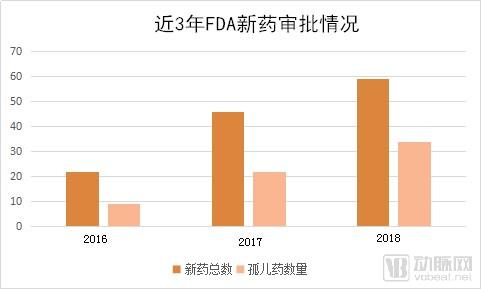

Looking at the global market, the FDA approved a total of 59 new drugs in 2018, breaking the highest record in 20 years. Among these 59 new drugs, 34 were approved as orphan drugs.

In 2018, the FDA approved for the first time therapeutic drugs for a rare genetic cartilage disorder, Fabry disease (a rare and severe condition that can lead to multiple adverse symptoms), and phenylketonuria (a rare disorder in which patients are unable to break down foods containing protein and sweeteners, leading to brain and nerve damage).

Due to market considerations, pharmaceutical companies have historically placed little emphasis on the development of orphan drugs. In 1983, the United States enacted legislation and passed the world’s first Orphan Drug Act (ODA). This act provides protections for companies developing orphan drugs through market exclusivity and clinical trial prioritization, while also facilitating their research and development by waiving application fees, providing research grants, and offering expedited regulatory review pathways.

In addition to the United States, regions such as the European Union, Japan, Australia, and Singapore have successively enacted orphan drug laws, which have significantly promoted the research, development, and market approval of orphan drugs.

The development of new drugs is influenced by multiple factors, including R&D complexity, drug patent terms, and generic competition. In contrast, orphan drug development faces less competition due to policy protections, often resulting in strong commercial performance. For instance, Celgene’s primary sales revenue stemmed from its orphan drug Revlimid, which achieved annual sales of $8.187 billion in 2017. In the same year, Merck’s blockbuster PD-1 inhibitor generated $3.809 billion in sales, less than half of Revlimid’s figure.

Against the backdrop of rising R&D costs and increasingly stringent regulatory approval requirements, rare disease drug development has emerged as a strategic priority for pharmaceutical companies. Industry giants such as Roche, Celgene, Bristol Myers Squibb (BMS), Novartis, AbbVie, and Johnson & Johnson allocate a significant portion of their annual R&D budgets to the development of rare disease therapies. In 2018, Japan’s Takeda Pharmaceutical acquired Shire, a leader in rare diseases, for $64 billion; notably, Takeda submitted five successive bids before finalizing the deal. Similarly, in 2019, BMS acquired Celgene in a transaction valued at $74 billion.

As the number of indications for orphan drugs continues to grow, an increasing number of blockbuster medications—such as eculizumab, imatinib mesylate (Gleevec), and Revlimid—have emerged. EvaluatePharma previously projected that global orphan drug sales would reach $209 billion in 2022, accounting for 21.4% of the prescription drug market (excluding generics). The compound annual growth rate (CAGR) from 2017 to 2022 was expected to be 11.1%, twice that of the overall prescription drug market.

Looking back at the approval process, the U.S. Orphan Drug Act stipulates that orphan drugs enjoy seven years of market exclusivity after launch, during which the FDA will not approve other new drug applications (NDAs) for the same indication; the FDA also provides an expedited review pathway for NDAs of orphan drugs; furthermore, the FDA may assist companies in conducting clinical trials for orphan drugs and waive the application fees for their NDAs.

Beyond policy-based protection and support, the determination is also evident from the number of orphan drugs approved by the FDA over the years.

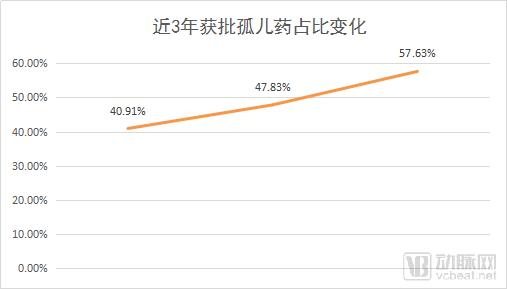

As previously mentioned, the FDA approved a total of 34 rare disease drugs in 2018, accounting for approximately 57.63% of all newly approved drugs; among the 46 new drugs approved in 2017, 18 were orphan drugs; even in 2016, when the number of approvals was below the annual average of the preceding decade, the FDA still approved nine orphan drugs (with only 22 new drugs approved by the FDA in 2016).

However, even as policies and industry efforts accelerate, the drugs currently approved or under review remain a drop in the bucket for rare disease treatment. Globally, more than 7,000 rare diseases have been identified, yet only 5% have effective treatments; in China, this figure stands at merely 1%. The field of rare disease therapy is still in its nascent stages, with many more solutions to be discovered and a vast market awaiting exploration.

In addition to the designation of orphan drugs, several first-wave medications approved by the FDA in 2018 also warrant attention. Drugs such as Aimovig, Ajovy, and Emgality were all approved in 2018 for the preventive treatment of migraine in adult patients. Furthermore, the FDA granted its first approvals for two therapies indicated for Dravet syndrome: Doptelet and Mulpleta. Dravet syndrome is a rare and severe form of epilepsy. Both agents are thrombopoietin receptor agonists, primarily approved for managing thrombocytopenia in patients with Dravet syndrome, and currently represent the only two therapeutic options available for this indication.

Among the first wave of drugs approved in 2018, one stood out distinctly from the others: Onpattro, developed by Alnylam Pharmaceuticals, which remains the only approved small interfering RNA (siRNA)-based targeted therapy. In the same year, Ionis Pharmaceuticals’ RNA-targeted product, Tegsedi, also received regulatory approval. The approval of these innovative therapies signifies that RNA-based therapeutic platforms are reaching maturity. Since the launch of fomivirsen, the first antisense oligonucleotide drug, in 1998, a total of eight oligonucleotide drugs have been approved to date.

In addition to the RNA therapy products from emerging players such as Alnylam, Ionis, and Quark, which have already entered mid-to-late stages of development, major pharmaceutical companies including Janssen, Amgen, Novartis, and Pfizer are also strategically positioning themselves through partnerships and other means. Statistics show that there are currently more than 30 mid-to-late stage clinical trials for RNA therapies underway, with more products expected to gain approval in the coming years.

If the biopharmaceutical industry is likened to a sailboat, technology serves as the engine of this vessel; capital is the essential fuel that powers the engine’s forward motion; and policy acts as the wind and sails, charting the course for its advancement.

Even in the depths of winter, capital remains generous toward promising technologies. In both China and the United States, regulatory authorities achieved significant breakthroughs in 2018; technologies and enterprises capable of genuinely addressing market challenges are poised to benefit from favorable conditions in the coming years.

Unlike the U.S. market, China’s biopharmaceutical industry lacks a capital market akin to NASDAQ that allows pre-profit companies to go public, leaving investment institutions with limited exit channels. Given that drug development cycles can span a decade, innovative enterprises have little possibility of generating profits during this period. However, the situation is beginning to turn around.

In 2018, the Hong Kong Stock Exchange announced that it would open its doors to pre-revenue biotechnology companies; in early 2019, the STAR Market announced that preparations were underway. Following improvements in policy, talent, and capital environments, the capital market has seen renewed turbulence. What impact will these changes in the capital market have on enterprises and investment institutions? After Genscript, InnoCare, and Hua Medicine, which biopharmaceutical companies will list domestically? Stay tuned for the next installment.

Follow the VCBeat New Medicine official account (biobeat1) and reply with “Report” to receive the “2014-2018 Investment and Financing Data Report for the New Medicine Sector.”

Scan the QR code to follow the VCBeat New Medicine official account (biobeat1)