What Are MedTech Giants Like Johnson & Johnson, Medtronic, and Philips Buying? A Look at Their Acquisition Trends in Robotics and Digital Health

If we were to summarize the key themes of the medical device industry in 2018, “mergers and acquisitions” (M&A) would undoubtedly be central, with such activities becoming increasingly frequent. The total value of all M&A deals in the medical device sector reached $98.5 billion in 2017, approximately double the $48.1 billion recorded in 2016. In 2018, data from Silicon Valley Bank showed that the number of M&A transactions far exceeded that of 2017. (Data sources: Silicon Valley Bank, Evaluate)

In fact, divestitures and mergers and acquisitions (M&A) are key strategic moves for medical device giants. Divesting non-core businesses allows companies to focus on their primary operations, maintain industry influence, and ensure stable profit margins. Meanwhile, M&A activities can strengthen competitiveness, acquire complementary technologies or technological reserves, expand product pipelines, or capture opportunities in blue ocean markets.

For industry giants, mergers and acquisitions (M&A) can be seen as a shortcut to maintaining competitiveness in the highly specialized and segmented medical device market. This article focuses on analyzing the trajectory of this “shortcut,” reviewing the investment patterns of major medical device companies from 2017 to 2019, and comparing them with M&A trends in earlier years, aiming to answer which areas have become key focus sectors for these industry leaders.

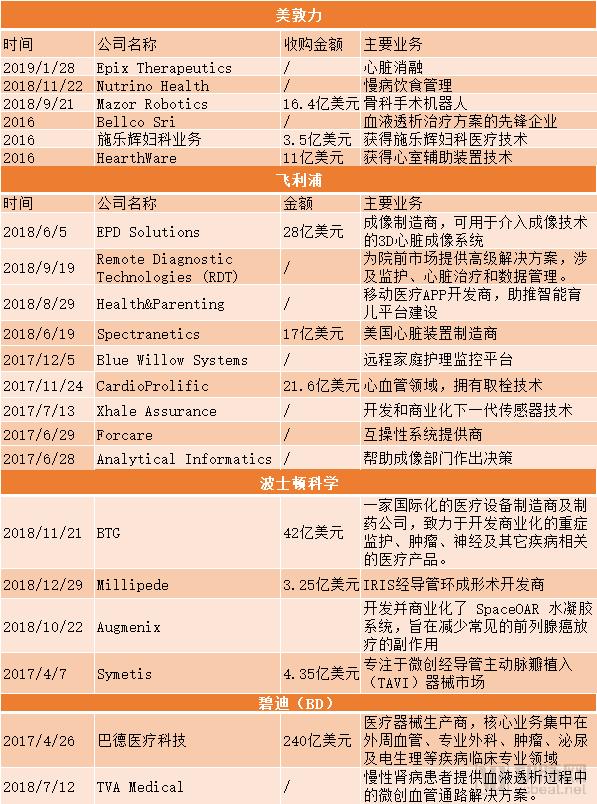

At the start of 2019, several acquisitions took place. Johnson & Johnson acquired surgical robotics company Auris Health for $3.4 billion, while Medtronic entered the cardiac ablation market for the first time by acquiring Epix Therapeutics. Smith & Nephew was reported to be acquiring medical device manufacturer NuVasive for $3 billion.

A flurry of large-scale acquisitions has been dazzling, but these moves are not impulsive; rather, they are strategic decisions based on the companies’ business development trends and market conditions. VCBeat’s analysis reveals that the two sectors most favored by industry giants for acquisition are surgical robots and digital health. Notably, in terms of financing, medical device companies with the highest funding amounts in 2018 were also led by those in the surgical robotics sector.

Undoubtedly, medical device giants continue to prioritize acquisitions in their core business areas, such as cardiovascular and neurosurgical devices. However, surgical robots and digital health have emerged as significant growth areas in recent years. Medtronic acquired Mazor Robotics (a spinal surgery robot), while Johnson & Johnson acquired Auris and Orthotaxy.

Strictly speaking, they are not merely surgical robots, but a complete surgical solution. Preoperative surgical planning is required to execute precise, personalized surgical plans.

In fact, to date, most medical device giants have already entered the surgical robotics field. As early as 2016, Smith & Nephew acquired the orthopedic robotics company BlueBelt (including its Navio robot) for $275 million. Stryker had earlier acquired Mako Surgical Corp. for $1.4 billion in 2014.

In 2015, Johnson & Johnson partnered with Verily, a subsidiary of Google’s parent company, to establish Verb Surgical, an independent company focused on developing surgical solutions. Although four years have passed since its inception, the company has yet to launch any products.

Meanwhile, several other medical device giants have already launched products for various applications. Less than a year after acquiring Mazor Robotics, Medtronic announced on January 30 that the Mazor X Stealth Edition had completed its first batch of spinal surgeries.

Johnson & Johnson, having entered the race later, is also gradually ramping up its efforts. In 2018, it acquired Orthotaxy, a next-generation robotic-assisted orthopedic surgery platform, and this year, it acquired Auris for $3.4 billion.

There are two reasons for their decision to acquire surgical robots: first, to consolidate their existing business, create growth highlights, and stimulate sluggish operations; second, the surgical robotics sector itself boasts significant growth momentum that cannot be underestimated.

Based on the financial annual report, Johnson & Johnson's total revenue in 2018 amounted to $81.582 billion. Of this, medical device sales reached $27 billion for the year, representing a 1.5% increase year-over-year; meanwhile, the pharmaceutical segment generated $40.7 billion in revenue, a 12.4% year-over-year increase.

The medical device business experienced slower growth, primarily due to the divestiture of the diabetes care business, LifeScan, and the impact of acquisitions. Growth was mainly driven by electrophysiology products within Interventional Solutions, contact lenses, and wound closure products used in general surgery; as well as endocutters and biosurgical products within the Advanced Surgery business.

Over the past three years, orthopedics business has begun to decline. Once the largest segment within Johnson & Johnson’s MedTech portfolio, it has now contracted for two consecutive years.

Among the “Big Five” in orthopedics (Johnson & Johnson DePuy Synthes, Medtronic, Smith & Nephew, Zimmer Biomet, and Stryker), 2018 revenue data showed that only Johnson & Johnson’s orthopedic business experienced negative growth.

Although Auris, acquired at a significant premium, currently has commercialized products focused on lung cancer, Johnson & Johnson’s primary motive for the acquisition was to complement its previously acquired Orthotaxy orthopedic surgical assistance robot. In the future, we may see orthopedic surgical robots drive new revenue streams for Johnson & Johnson’s medical device division.

Medtronic had already performed surgical cases within a year of acquiring Mazor Robotics. Medtronic’s acquisition of the spinal robotics company was also aimed at safeguarding its leading position in the spine sector. In the highly specialized and segmented medical device market, acquisitions enable companies to acquire new technologies and open up new markets.

From a positive perspective, those who strategically positioned themselves for early acquisitions have already reaped the benefits. In 2016, Smith & Nephew acquired BlueBelt Technologies, an orthopedic robotics company (including its Navio robotic system).

Since 2014, Navio has gradually achieved commercialization. In 2017, Smith & Nephew announced the launch of its NAVIO handheld robotic-assisted total knee arthroplasty (TKA) application. This expanded the NAVIO platform to total knee procedures, which account for 80% of knee replacement surgeries worldwide.

Currently, the NAVIO robotic-assisted system does not require preoperative imaging, such as CT scans. This allows patients to avoid additional steps, costs, and radiation exposure associated with extra preoperative imaging.

In 2017, the Navio robotic system already contributed to the growth of Smith & Nephew’s surgical business. In 2018, the “Other Surgical Businesses” segment, which includes the Navio robotic system, was also the fastest-growing division.

From a macro perspective, surgical robotics is also a highly promising sector. Intuitive Surgical, the company behind the da Vinci Surgical System, saw its stock price increase 63-fold over 17 years. As of 2017, there were 4,409 da Vinci systems installed worldwide.

Intuitive Surgical’s revenue is primarily derived from two sources: equipment and services. Each system costs approximately RMB 20 million to manufacture. The da Vinci surgical robot typically features four robotic arms, each with a manufacturing cost of RMB 100,000 and a usable lifespan limited to 10 procedures.

In 2017, Intuitive Surgical’s revenue from service fees alone reached as high as $581.8 million. (Source: Forbes)

According to estimates by Boston Consulting Group (BCG), the global medical robotics market was projected to reach a valuation of $11.4 billion by 2020. The incidence rates of chronic diseases, such as cardiovascular, neurovascular, and oncological conditions, continue to rise. The growing prevalence of chronic diseases will expand the market for surgical robots. Favorable healthcare and reimbursement policies, coupled with the adoption of advanced technologies in microsurgical robots, further support this growth.

The growth prospects in the EU region are particularly promising, with the German microsurgical robotics market projected to achieve a growth rate of 15.3%. This high growth rate is attributed to initiatives undertaken by the EU to promote the adoption of advanced technologies, including robot-assisted microsurgery for healthcare applications. For instance, the European Association of Urology has introduced robotic urology programs. This will lead to high adoption rates of microsurgical robots in urology, thereby driving business growth.

In China, regulatory authorities are also vigorously promoting the application of medical robots. Under "Made in China 2025," biopharmaceuticals and high-performance medical devices are listed among the ten key sectors for breakthrough development. On January 30, 2019, the General Office of the National Health Commission issued the "Notice on Establishing the Expert Committee for Clinical Application Management of Surgical Robots." The notice stated that, to standardize the clinical application of surgical robots, improve healthcare quality, and ensure medical safety, the National Health Commission would establish the Expert Committee for Clinical Application Management of Surgical Robots. The development of the domestic market is likewise expected to be promising.

The promising prospects of surgical robots can be seen as favorable information for medical device companies to enter new fields. Large companies also have to enter new areas, especially in the context of fierce competition in the homogeneous market of medical devices abroad and sluggish market growth.

According to the annual reports of Johnson & Johnson, Philips, and Boston Scientific over the past two years, the growth trend in emerging markets has far exceeded that in the United States and Europe.

Moreover, with the advent of healthcare cost containment measures and the digital era, the role of value-based healthcare is becoming increasingly prominent. For medical device companies, their business models are beginning to undergo transformation.

To maintain competitiveness in niche markets,Medical device manufacturers need to not only carry out vertical mergers and acquisitions as before, but also seamlessly acquire real-world data.. A support platform that integrates individual medical technology products and services into holistic care solutions, particularly against the backdrop of continuous technological advancements across the industry, growing uncertainty in regulation and legislation, and tightening healthcare insurance reimbursement policies.

Moreover, beyond competition from traditional medical device giants, advancements in sensor technology and artificial intelligence (AI) have expanded the use of medical devices beyond hospitals to include digital products and data-related services. The FDA registration of the Apple Watch serves as one example. Companies entering the medical device industry are becoming increasingly diverse.

Medical device giants cannot afford to fall behind; although it may not be a core business focus, they must establish more flexible business models to address this.

Prior to 2017, medical device giants were still in the process of gradually embracing digital health. Between 2015 and 2016, notable collaborations included Philips partnering with the pathology company PathAI; Stryker collaborating with Microsoft on augmented reality to build the operating room of the future; Johnson & Johnson establishing a joint venture with Verily to research surgical robots; and Medtronic working with IBM Watson to develop a predictive app for blood glucose management.

But now, we can see that Medtronic has moved to directly acquire an AI nutrition technology company, and Philips is also vigorously transforming into a health technology company.

Looking back after two years, some specific initiatives have yet to yield returns, but none of these strategic directions have been scaled back; instead, investment has largely been increased. In the realm of digital health, the strategy has shifted from partnerships to acquisitions, with previously peripheral products moving to the center stage.