Unicorn Emergence in Health Insurance Innovation: Key Trends and Opportunities

Insurance, particularly commercial health insurance, has experienced rapid development in recent years, with continuous growth in market size, coverage, and insurance penetration. Driven by accelerating population aging, rising income levels, and increasing willingness to purchase insurance, the commercial health insurance market is poised for further expansion. Innovation has been a key driver of this market growth—such as through insurtech enablement, product innovation, diversification of distribution channels, construction of medical service networks, and optimization of underwriting and claims processes. Numerous innovative companies have emerged across these sectors.

VCBeat (WeChat: vcbeat) plans to scan the insurance innovation sector to identify unique innovative companies in this field. The main contents of this article include:

From Scattered Risks to Approximate Certainty: The Essence of Insurance;

Three Stages of Development in China’s Health Insurance Industry: From Inception to Revitalization;

How the Health Insurance Industry Is Innovating Across the Entire Value Chain, from Products to Services;

From Startup to “Unicorn”: Insurance Innovation Companies Show Great Potential.

Insurance is an industry that feels both closest to and most distant from us. It is close because insurance has become the “infrastructure” of our society, akin to water, electricity, and gas; we interact with it constantly through mandatory social security and housing fund contributions, auto insurance, traffic accident liability insurance, and property insurance. Yet it feels distant because many insurance products we encounter in daily life are marketed with aggressive sales tactics, prompting us to keep them at arm’s length.

Insurance possesses both protective and financial attributes. Policyholders pay premiums in advance to secure compensation for potential future losses, thereby eliminating economic uncertainty. Insurance companies aggregate fragmented and sporadic risks, transforming dispersed uncertainties into approximate certainties and realizing commercial value.

In recent years, regulatory authorities have advocated that “insurance should prioritize protection,” urging the industry to return to its roots and focus on risk coverage. This initiative aims to curb various irregularities in the insurance market conducted under different guises, restore the original intent of protection and mutual aid, and truly deliver value in mitigating risks and safeguarding personal and property security.

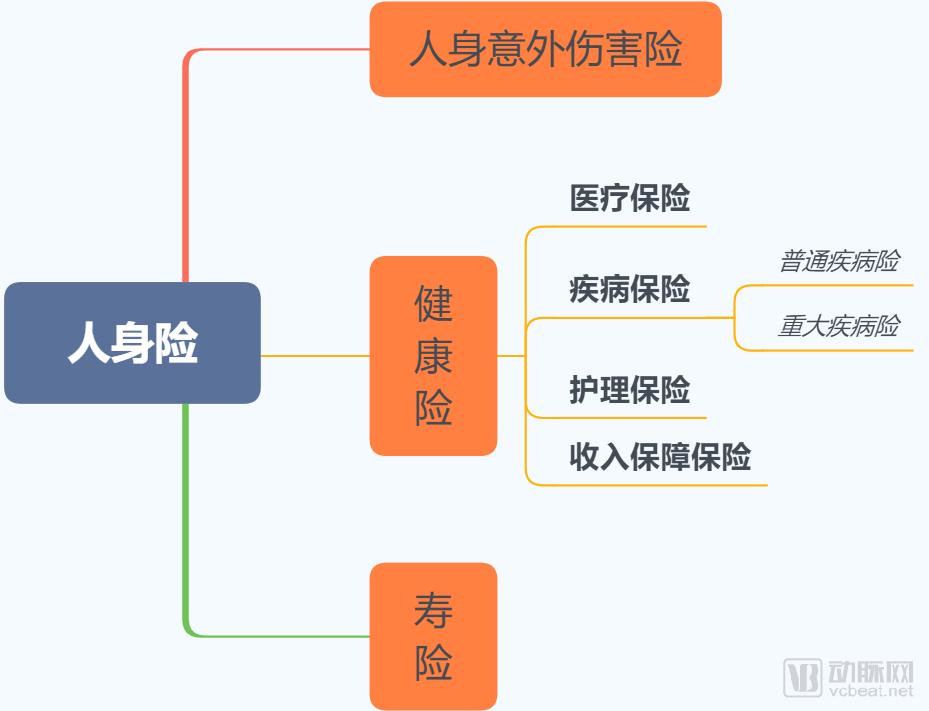

Focusing on health insurance, it generally refers to a branch of life insurance that takes the insured’s body as the subject matter of insurance, providing compensation for expenses or losses incurred when the insured suffers from illness or accidental injury.

Health insurance falls under the broad category of personal insurance, standing parallel to personal accident insurance and life insurance. It is further subdivided into medical insurance, critical illness insurance, long-term care insurance, and income protection insurance. Based on the policyholder entity, it can be classified into group health insurance and individual health insurance.

Figure 1: Classification and Categorization of Health Insurance

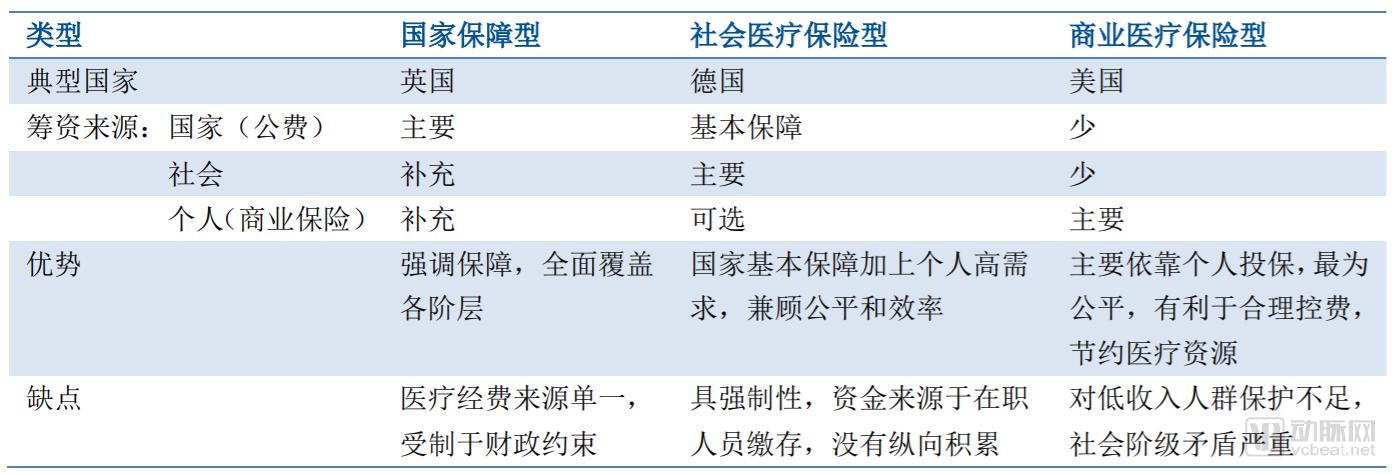

Regardless of the healthcare financing model, health insurance plays a pivotal role. According to a research report by Minsheng Securities, national healthcare systems can be broadly categorized into three types based on their funding mechanisms: state-funded, social health insurance, and commercial health insurance models. Countries such as the United Kingdom and Sweden adopt the state-funded model; Germany, Japan, France, and South Korea implement social health insurance systems; while the United States primarily relies on commercial health insurance.

Under the state-funded and social health insurance systems, funding sources primarily rely on state health security expenditures and social health security expenditures, respectively, with commercial health insurance mainly purchased by high-income groups. In countries with a commercial health insurance-dominated model, national health security relies primarily on individual commercial insurance, with limited contributions from state and social security.

Under different medical insurance systems, variations in the entities bearing insurance liabilities, the degree of government leadership, and funding mechanisms lead to divergent development paths for commercial health insurance. Nevertheless, commercial medical insurance plays a significant role in all contexts, with its importance increasing progressively across national security-oriented, social medical insurance-oriented, and commercial medical insurance-oriented models.

Table 1: The Role of Commercial Health Insurance Varies Across Different Healthcare Financing Systems

Source: Minsheng Securities Research Institute, compiled from public information

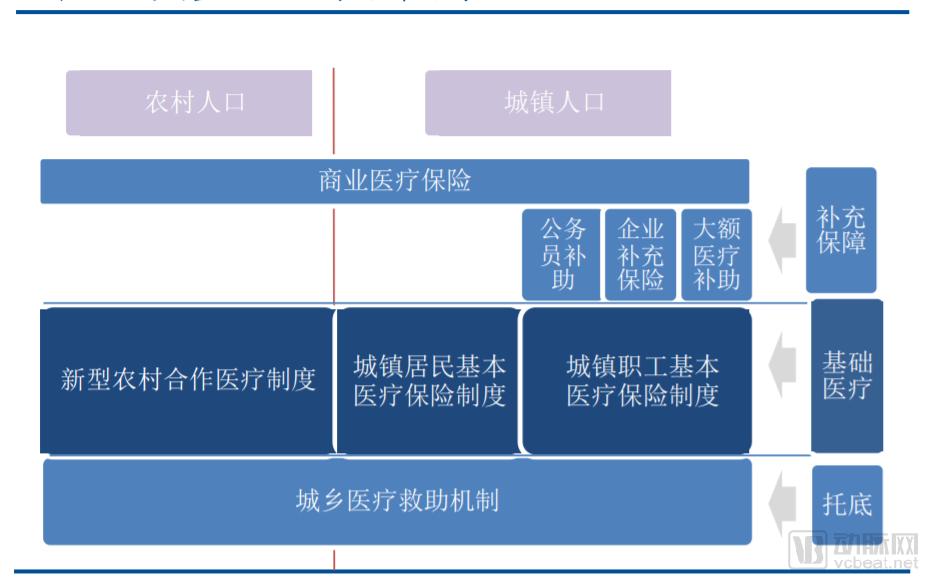

China differs from developed countries in Europe and the United States in terms of the conditions and experiences for implementing healthcare system reforms; therefore, the three typical foreign models are not fully applicable. Currently, China’s healthcare security system is based on the social health insurance model, drawing on the experiences of state-sponsored coverage and commercial medical insurance. It has formed an institutional framework dominated by social medical insurance, supplemented by medical assistance, publicly funded medical care, and commercial health insurance.

Figure 2: China's Multi-tiered Medical Security System

Source: Minsheng Securities Research Institute

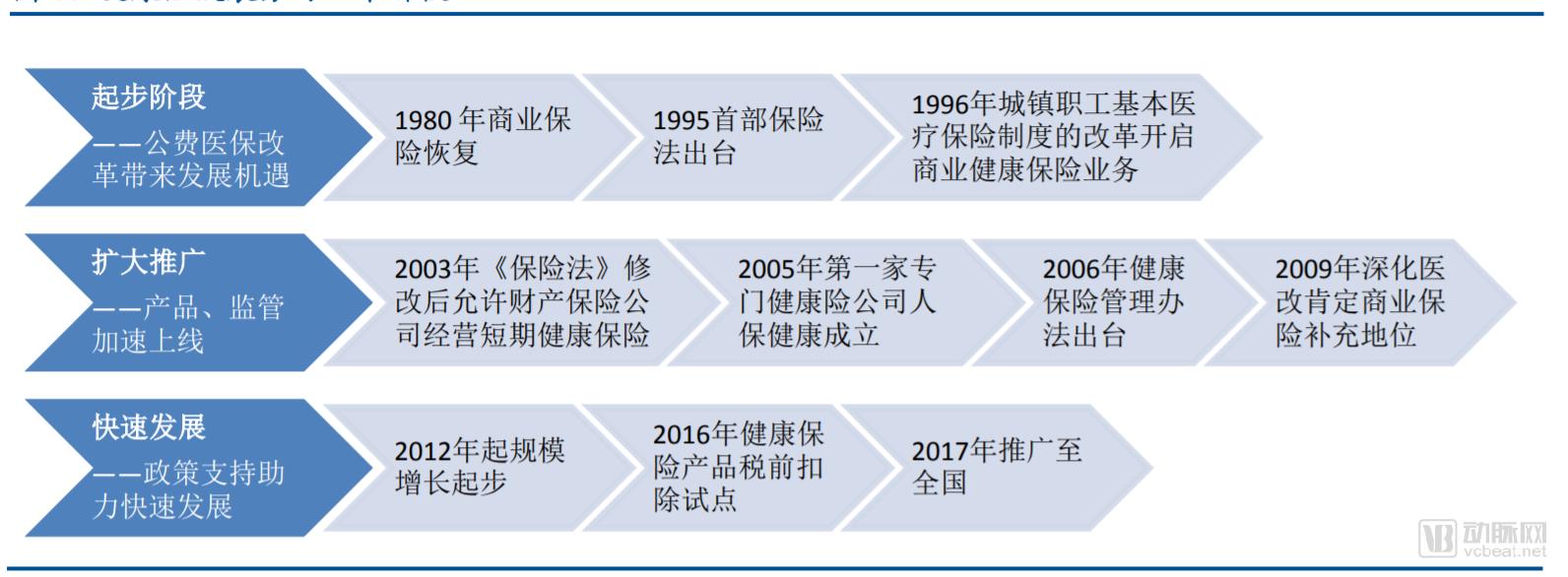

As a supplementary safeguard to basic medical insurance, commercial health insurance in China has been continuously advanced alongside the reform and development of social medical insurance, entering a period of rapid growth. The development of China’s health insurance industry can be broadly divided into three major stages: the initial stage, the expansion and promotion stage, and the rapid development stage.

Figure 3: Development Stages of Commercial Health Insurance in China

Source: Minsheng Securities Research Institute

With the introduction of several favorable policies, heightened insurance awareness among residents, and improved consumption capacity, commercial health insurance has become the fastest-growing segment within the insurance industry in recent years. However, it is also important to note that health insurance currently faces challenges such as low penetration rates, a small market scale, and an imbalanced product structure. Service capabilities remain insufficient, as evidenced by weak control over medical expenses and inadequate provision of health management services.

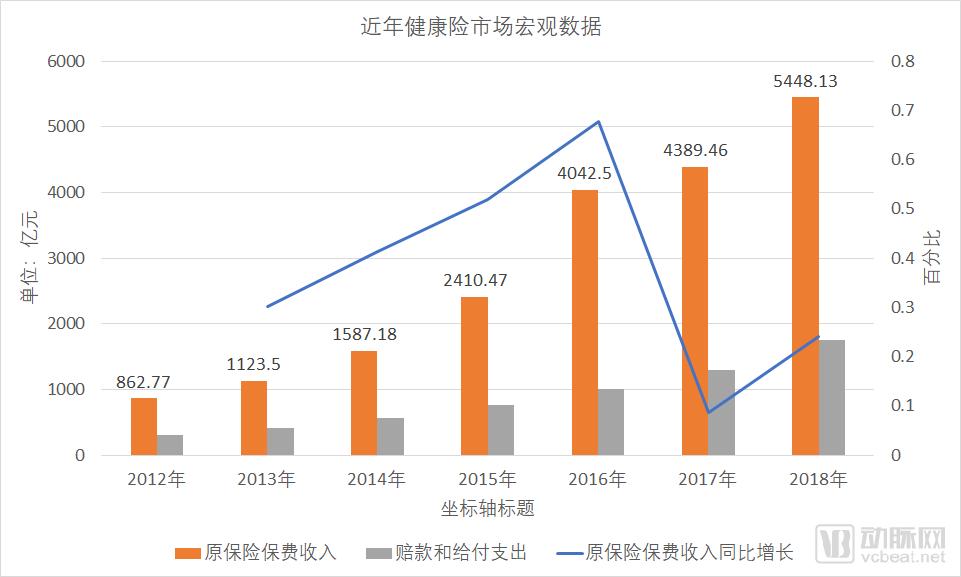

Table 2: Macroeconomic Data of the Health Insurance Market

Source: China Banking and Insurance Regulatory Commission

According to data from the China Banking and Insurance Regulatory Commission (CBIRC), the original premium income of health insurance business reached RMB 544.813 billion in 2018, a year-on-year increase of 24.12%. Claims and benefits paid for health insurance business amounted to RMB 174.434 billion, representing a year-on-year growth of 34.72%. In 2012, the original premium income of domestic health insurance business was only RMB 86.277 billion. From 2013 to 2018, the compound annual growth rate (CAGR) of the health insurance market reached 35.95%.

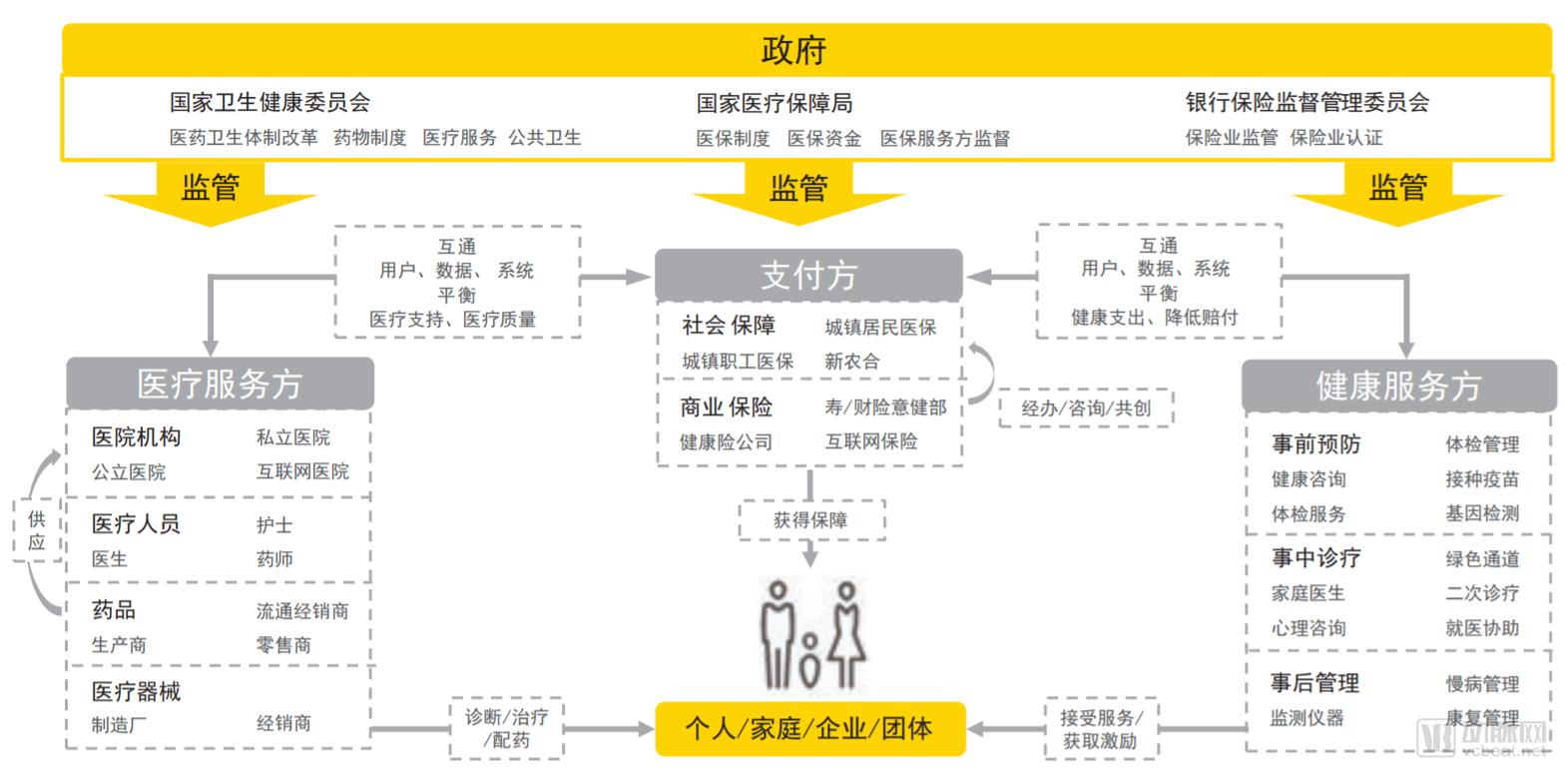

The operation of health insurance involves multiple segments, including “medical care, pharmaceuticals, insurance, and health management,” requiring coordinated efforts among medical services, pharmaceutical supply assurance, insurance, and health management systems. Since the subject matter is human “health,” health insurance cannot be viewed solely from a financial or insurance perspective.

From the perspective of service delivery, health insurance customers first obtain health insurance coverage. Subsequently, when medical needs arise, they seek care at healthcare institutions to receive treatment plans, followed by rehabilitation and health management services. As the payer, the insurance provider offers financial support either in advance or retrospectively. Insurance, medical, pharmaceutical, and other related products or services operate under the supervision of regulatory authorities, including the China Banking and Insurance Regulatory Commission (CBIRC), the National Healthcare Security Administration (NHSA), the National Health Commission (NHC), and the National Medical Products Administration (NMPA).

Figure 4: Health Insurance Ecosystem

Source: EY China Commercial Health Insurance White Paper

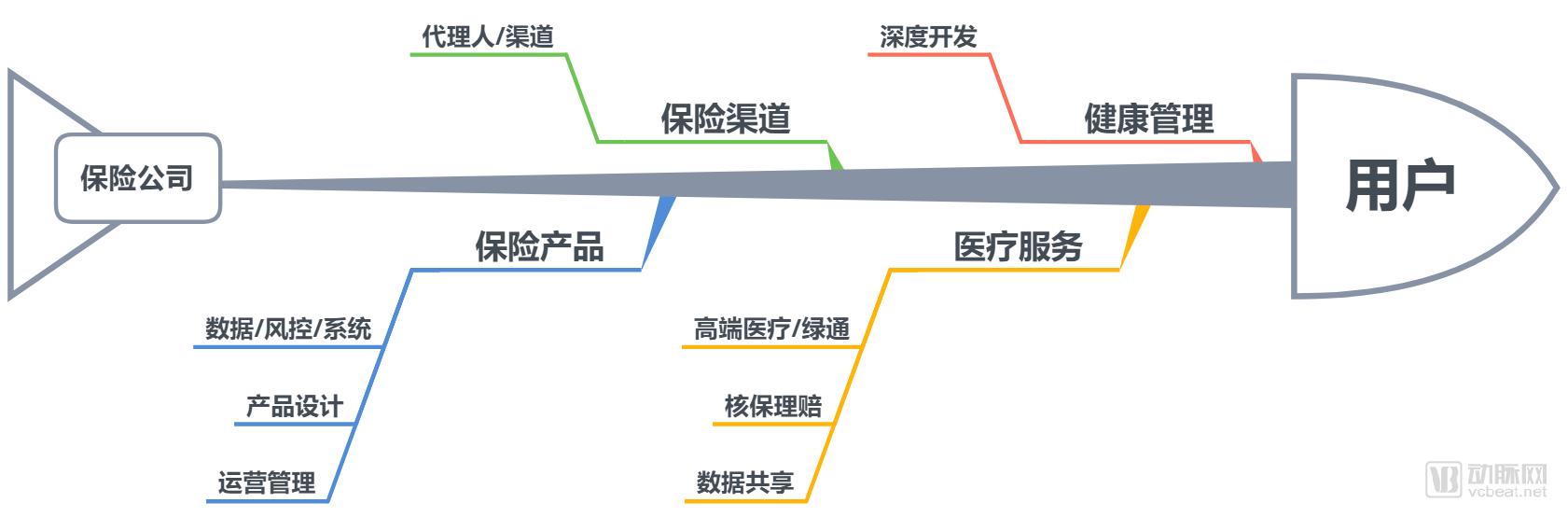

Figure 5: Health Insurance Service Process

In the service workflow of health insurance, key stages include insurance product design, channel development, medical services, and health management. The varying degrees of coordination across these stages reflect the distinct operational characteristics of health insurance companies. For instance, linking insurance fund management with the control of medical service costs aligns the interests of both parties, creating a community of shared interests. This business model is known as managed care.

Key aspects of the health insurance service process also represent areas of innovation. For instance, in terms of product innovation, traditional health insurance products were primarily targeted at healthy individuals, excluding those with pre-existing conditions. However, by requiring truthful disclosure of health status, leveraging comprehensive clinical data, and employing more refined pricing models, it is possible to unlock the market for health insurance covering chronic diseases and specific medical conditions.

Next is channel innovation. Under the traditional model, insurance agents play a crucial role, with health insurance policies sold through them accounting for more than 60%. However, with the development of internet platforms and content operation platforms, distribution channels are becoming increasingly diversified. For end users, greater information transparency has enhanced their willingness to purchase insurance.

Medical services are the core component of health insurance. In particular, mid-to-high-end medical insurance products typically provide users with value-added medical services, such as health check-ups, green-channel access to medical care, expert consultations, overseas medical treatment, and health counseling. These value-added services not only serve as the foundation for understanding customers’ health status and delivering differentiated services but also enhance customer stickiness and create opportunities for in-depth client development. Therefore, building a high-end medical service network and strengthening operational capabilities in medical resource management are particularly critical.

Finally, in the health management phase, the development of smart wearable devices, Internet of Things (IoT) devices, and smart hardware enables better tracking of users' health status and timely, rational health interventions, which is beneficial for enhancing insurance engagement and reducing healthcare costs.

Finally, we summarize the innovations across the entire health insurance value chain into two key concepts: “growth” and “efficiency.” “Growth” refers to identifying and tapping into underserved or untapped market demands through product, channel, and service innovation, thereby driving incremental growth in policyholders and insurance needs. “Efficiency” denotes enhancing the operational efficiency of the health insurance system, providing users with more convenient services, and potentially reducing certain costs by optimizing service processes.

Based on the above analysis of the health insurance process, we categorize innovative companies in the health insurance sector into several major groups: insurance carriers, channels/platforms, third-party service providers, and integrated players. Within these categories, VCBeat will comprehensively review relevant domestic and international companies and provide detailed case studies.

Innovative Health Insurance Company

Table 3: Innovative Health Insurance Companies

Oscar Health and Clover Health are representative examples of new-generation health insurance companies; both have secured substantial financing rounds and remain privately held.

Oscar Health

Oscar Health was founded in 2012. Its founder and CEO, Mario Schlosser, holds an MBA from Harvard Business School and previously worked at Goldman Sachs. Co-founder Josh Kushner, the brother-in-law of former U.S. President Donald Trump’s son-in-law, is a former investor who participated in investments in companies such as Reddit, Hightower, and Instagram. His investment firm was an early investor in Oscar Health.

Oscar Health integrates technology concepts with health insurance, primarily targeting younger demographics. It attracts the uninsured by simplifying products and repricing them. In terms of distribution channels, it extensively leverages mobile apps, websites, and social media platforms to promote its offerings, while deploying specialized teams to address questions related to insurance purchases and medical services. Regarding healthcare delivery, Oscar Health departs from the broad provider networks typical of traditional insurers; instead, it establishes narrow networks through strategic partnerships with high-quality healthcare providers, sharing costs and profits to forge tighter alliances.

In addition, Oscar Health offers systematic health management and user health incentives. Members can communicate with healthcare professionals through various channels, such as phone calls and its mobile app, while maintaining a healthy lifestyle in their daily lives (primarily earning rewards for step counts). This approach helps reduce disease risk, thereby lowering medical expenditures.

According to data from Oscar Health’s official website, the company currently operates in six U.S. states, including Ohio, Texas, New Jersey, New York, and California, serving a total of 250,000 individual and group members (primarily individuals). In terms of revenue, Oscar Health had been reporting losses in previous years. In 2017, its annual premium income amounted to $229 million, with a net loss of $127 million. In the first half of 2018, the company generated $363 million in revenue and achieved profitability for the first time, with a net profit of $5 million.

Clover Health

Clover Health is equally noteworthy, as it targets the elderly population by offering insurance products specifically designed for individuals aged 65 and older. Of course, Clover Health provides more than just insurance; it offers chronic disease management services that include insurance coverage. Clover Health has chosen chronic disease management as its entry point into the health insurance sector, believing that managing chronic conditions represents significant potential for cost control by reducing medical expenses and improving overall health outcomes through proactive health management.

Insurance observers note that Clover Health’s decision to focus on chronic disease management stems from the fact that medical research on chronic conditions is relatively mature compared to diseases such as cancer. Taking cancer prevention and treatment as an example, the medical community has yet to reach a consensus on the causes of cancer, making it difficult to predict its occurrence. In contrast, research into the risk factors for chronic diseases, including cardiovascular diseases, is now well-established, indicating that it is meaningful to use data analytics to predict complications associated with these conditions.

Clover Health employs a complex data processing workflow, collecting data such as public health records, electronic medical records (EMRs), laboratory and diagnostic test results, medication data, and claims data. The data is then cleaned and processed to predict complications and propose intervention strategies, with the aim of reducing healthcare expenditures.

Clover Health’s business model is characterized by reducing medical costs through improving members’ health outcomes, a approach that aligns closely with the payment structure of the Medicare Advantage program. Under Medicare Advantage, the government employs a risk-adjusted payment model, whereby it makes monthly payments to insurance plans based on each member’s risk score. This means that the sicker the enrollee, the higher the reimbursement received by the insurance plan.

For example, if the government pays $500 per month for a healthy enrollee, it would pay $1,400 per month for a patient with diabetes. These benchmark payments are equivalent to the costs incurred under the Medicare program for caring for patients with the same conditions. Under this capitated payment model, if an insurance plan receives $1,400 per member per month for diabetic patients but incurs actual costs of only $1,000 per month, it generates a monthly surplus of $400. This represents the market opportunity through which Clover Health achieves profitability by reducing medical expenses.

Clover Health currently has approximately 40,000 members, with 41% being African American or Hispanic. In late January 2019, Clover Health announced the completion of a new $500 million funding round led by Greenoaks Capital. To date, Clover Health’s total fundraising amount reaches $925 million, with its previous funding round valuing the company at $1.2 billion.

Summary

In addition to Clover Health, two other companies targeting the U.S. Medicare program are also worth noting: Devoted Health and Bright Health. U.S. Medicare is divided into four parts: Part A primarily covers inpatient hospital care; Part B mainly covers physician outpatient services and preventive screenings; Part C, known as Medicare Advantage, offers additional healthcare benefits such as vision, hearing, and dental care, requiring beneficiaries to pay extra premiums; and Part D primarily covers prescription drugs.

Medicare Advantage is widely regarded as the most stable and valuable segment of the U.S. healthcare system. With over 20 million enrollees and $20 billion in annual revenue, it already constitutes a substantial market. By 2025, Medicare Advantage is projected to grow to an annual revenue exceeding $500 billion. Furthermore, because Medicare is a government-sponsored benefit program, the Medicare Advantage sector remains resilient year after year, regardless of fluctuations in the broader economy. This market, which functions similarly to supplemental health insurance, is operated by commercial health insurers, offering them considerable profit margins.

Health Insurance Platform/Channel Innovation

First, we define insurance channel/platform companies as those that leverage information technology to provide online services including insurance education, product comparison, product screening, purchase facilitation, and customer support. On the backend, such companies may also collaborate with insurers to optimize products or service workflows. However, proprietary online service platforms operated by insurance companies themselves are excluded from this definition; most large- and medium-sized insurers typically operate their own online “product supermarkets.”

Table 4: Channel/Platform-Based Innovative Companies

Such channel- or platform-based companies address the challenges of market education and customer acquisition in the insurance sector. Leveraging their third-party status, they are more likely to gain user trust. Furthermore, dedicated content production and operations teams ensure the consistent delivery of high-quality content and campaigns, thereby driving new user acquisition and boosting user engagement.

First, we will introduce the strategic layouts of Alibaba and Tencent in this sector. As tech giants with extensive traffic, data resources, and financial service capabilities, both companies have already made significant moves in the internet insurance services market.

Ant Financial has established an “Ant Insurance” section within Alipay, offering insurance products across multiple major categories—listed in order of priority—including health, accident, travel, property, and life insurance. Health insurance products are provided by companies such as PICC Health, ZhongAn Insurance, Ping An Insurance, and Guohua Life & Taikang Online. In addition, Trust Mutual Life Insurance Society partnered with Alipay to launch the mutual aid insurance product “Xianghu Bao” (later renamed “Xianghubao”) in October 2018, which has since attracted 34.87 million participants.

Tencent WeSure is Tencent’s first majority-controlled insurance platform. WeSure partners with leading domestic insurance companies to provide high-quality insurance services, enabling users to purchase policies, check policy details, and file claims through WeChat and QQ, two of China’s most widely used lifestyle service platforms. The company operates as an insurance agency, offering products such as medical insurance, critical illness insurance, and long-term critical illness insurance for children.

ZhongAn Online has driven the popularity of “million-yuan medical insurance” products through a model combining product innovation with platform innovation. Its flagship “Zunxiang Yisheng” medical insurance series is among the most renowned and best-selling products in its category. Its subsidiary, ZhongAn Technology, is committed to exporting its proprietary technologies, promoting the digital transformation of the insurance industry, and serving as an incubator for both internal and external innovation, having established five technology product lines that “empower” the industry.

Other companies, such as Da Te Bao and Xiao Yu San, have also achieved considerable success. Supported by insurtech, Da Te Bao provides comprehensive insurance operational services to insurers and cross-industry partners. With a focus on health insurance, it offers users integrated health management, medical, and pharmaceutical services, serving as a one-stop portal for addressing users’ health needs throughout their entire life cycle. The company has sequentially launched multiple innovative insurance products, including Da Te Bao Medical Insurance, Children’s Vaccine Insurance, and Diabetes Insurance.

Online channels have their pros and cons. The advantages include low cost, broad coverage, and high reusability of information. The disadvantages lie in the fact that insurance policy terms are generally complex; certain items require guidance from professionals to be properly interpreted and completed. Online operations are prone to misunderstandings or misinterpretations, which can hinder subsequent policy administration. Therefore, online channels are more suitable for products with simple terms and well-defined target audiences.

Health Insurance Third-Party Administration (TPA)

Third-party service providers in the health insurance sector are commonly referred to as TPAs, an abbreviation for Third Party Administrator for Group Medical Insurance, denoting third-party medical insurance management companies. Within the healthcare industry, these entities provide third-party administrative services to health insurers or insurance companies specializing in medical insurance, particularly medical expense coverage. Their services encompass new policy issuance and policy maintenance, claims processing, customer service, provider network management, and coordination of medical expense settlements.

Table 5: Third-Party Service Providers for Health Insurance

The emergence of TPA service companies stems from the “pain points” in the health insurance industry. First, life insurance companies currently dominate the domestic health insurance market, with critical illness insurance accounting for the largest share of their product portfolio. Although medical insurance has been growing rapidly, its scale remains relatively small. As a result, medical insurance teams have limited influence within insurance companies. Under such circumstances, life insurers tend to allocate resources unevenly and lack professional healthcare talent, making it difficult to achieve specialized operations.

Secondly, since health insurance accounts for a relatively small proportion of total social healthcare expenditure, it lacks strong bargaining power over medical institutions. This prevents commercial insurance companies from establishing high-quality medical service networks and effectively controlling and intervening in medical costs.

This has created fertile ground for the emergence and development of third-party service providers. For health insurance companies, the significance of these third-party services lies in business unbundling and outsourcing. This includes foundational IT system planning and implementation, market research and data support during the product design phase, product and channel management, customer relationship maintenance, establishment of medical service networks, rapid and direct claims settlement systems, as well as handling daily health consultation inquiries and providing health management services.

U+ Health

Youjia Health was established in June 2017. Its founder, Wang Yanping, has over a decade of experience in the health insurance industry and was an early founding team member and preparatory committee member at iKang Guobin, Ping An Health, and Taikang Health. She previously served as General Manager of the Medical Network Department and Key Accounts Department at Ping An Health, as well as General Manager of the Medical Management Department at Taikang Health. In early 2018, Ding Haochuan, former President of Wish China, joined Youjia Health as a co-founder. Other members of the founding team come from the insurance, healthcare, and internet sectors, bringing extensive management and operational expertise.

UJia Health provides insurance-side solutions and healthcare-side solutions. The former helps insurance companies integrate medical resources, curate Preferred Provider Organization (PPO) networks, and build an S2B-based integrated empowerment platform leveraging internet technologies. The latter involves establishing a value-based healthcare service evaluation system and partnering with hospitals to create a preferred direct-billing medical network. When UJia Health customers require hospitalization due to illness, UJia Health provides payment guarantees to the preferred hospitals, enabling customers to enjoy the convenience of direct settlement for inpatient medical expenses.

Yuguo Doctor

YuGuo Doctor is China’s leading premium private healthcare discount platform, founded in 2012. Currently, YuGuo Doctor has partnered with nearly 1,000 high-end private medical institutions, including international healthcare brands such as United Family Healthcare,明德 (Mingde), Amcare, ParkwayHealth, and Ward. Its services cover more than 10 regions and cities, including Beijing, Shanghai, Guangzhou, Shenzhen, Hong Kong (China), and Japan. The platform achieves over 80% coverage in the premium private healthcare sector, 100% coverage of top-tier medical brands, and offers exclusive discounted rates for more than 60% of its partners.

Yuguo Doctor connects with over 12,000 senior physicians, 70% of whom are experts at the associate chief physician level or above from Tier-3 Grade-A hospitals. It covers hundreds of high-end medical insurance plans for individuals and families offered by 90% of premium health insurers, including Bupa, MSH, Cigna & CMG, and Ping An, reaching more than 1 million users per month across all channels.

As a utility-driven patient navigation product, it enables users to conveniently access essential information on the Yuguo Doctor platform—such as physicians’ practice details and hospital discount offers—once their needs arise. Hospitals benefit from platform-generated traffic and transparent word-of-mouth promotion, while insurance institutions gain access to high-value medical data and precisely targeted users, creating a win-win scenario for all stakeholders.

Collaboration Between Health Insurance Companies and Healthcare Providers

In the traditional service model, health insurance companies act merely as “payers” rather than “decision-makers,” limited to retrospective reimbursement and unable to establish deep integration with medical institutions, pharmaceutical suppliers, and health management organizations. This significantly restricts their ability to oversee the healthcare delivery process and implement effective cost containment measures.

In countries with well-developed private health insurance markets, such as those in Europe and the United States, there are numerous examples of close collaboration between health insurers and healthcare providers. Notable examples include the renowned Kaiser Permanente and various Preferred Provider Organizations (PPOs). Recent landmark cases of cross-segment integration within the health insurance industry value chain include CVS’s acquisition of Aetna and Cigna’s purchase of Express Scripts.

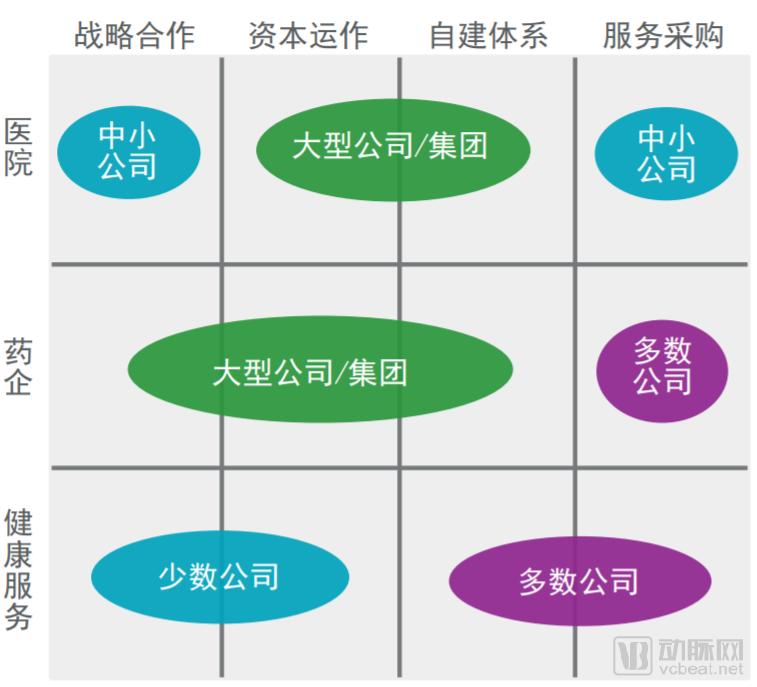

According to EY China’s Health Insurance White Paper, insurance companies, acting as payers, are proactively initiating integration with hospitals, pharmaceutical companies, and health service providers to achieve rational cost control, enhance customer stickiness, accumulate health data, and enable differentiated pricing. These integration models can be categorized into four types: strategic cooperation, capital operations, self-built systems, and service procurement.

Figure 6: Collaboration Models Between Insurance Companies and Healthcare Service Providers

Source: EY China Commercial Health Insurance White Paper

From the perspective of current integration models between insurance companies and service providers, large insurance groups tend to make substantial investments in building their own systems or leveraging capital operations to secure control over high-end medical resources when partnering with hospitals. In contrast, small and medium-sized insurers collaborate with hospitals in differentiated niche segments (such as international departments) by leveraging their respective strengths. Regarding pharmaceutical companies, most adopt partnerships with third-party drug distributors or strive to gain control over resources in specialized, scarce, and high-end medication sectors (such as diabetes treatments). For health services, the predominant approaches involve either building proprietary platforms or integrating with third-party providers.

It has become an industry consensus that both industrial and capital synergy are essential. An industry report released by the Insurance Association of China points out that the greatest challenge facing the development of commercial health insurance in China is the lack of cooperative mechanisms with healthcare service providers for risk sharing, balanced interests, and information sharing. To improve this situation, efforts should focus on refining the operational design of critical illness insurance, promoting the participation of commercial health insurance in supply-side reforms of healthcare services, and establishing a legal framework for health data.

Health insurance should not be limited to mere coverage; instead, it should provide comprehensive protection grounded in health. Establishing an integrated ecosystem of “insurance + healthcare + wellness” will not only deliver a superior insurance experience for policyholders but also maximize the value of health insurance.

Other Companies in the Insurance Innovation Track

In addition to the companies mentioned above, certain niche segments have not been covered, such as technology-enabled healthcare, insurance big data, Pharmacy Benefit Management (PBM), and medical insurance administration. Similar to PBM, these areas would typically fall under third-party services; however, as they are still in their infancy in China with few market players, they are not listed separately. Furthermore, given the ongoing reform of medical insurance payment methods and the exploration of diversified payment models, DRGs (Diagnosis-Related Groups) and medical insurance administration companies also warrant attention.

Table 6: Other Noteworthy Companies in the Insurance Innovation Sector

Ping An Health Insurance Technology

Ping An Health Insurance Technology was established in 2016 as a member of the “Big Healthcare” segment under Ping An Group. It primarily serves domestic basic medical insurance and health administration systems, commercial insurance enterprises, healthcare institutions, and the pharmaceutical distribution sector. Against the backdrop of national policies encouraging “public-private partnership” and the development of commercial health insurance, Ping An has actively responded to state directives by engaging in various collaborative medical insurance initiatives. These efforts aim to assist medical insurance administrative authorities in better managing medical insurance funds, thereby achieving the goal of “one reduction and two improvements”: reducing healthcare costs, enhancing coverage levels, and improving the patient experience in medical services.

In just two years, Ping An HealthCare Technology has cumulatively provided medical insurance and commercial insurance management services to over 200 cities and a population of 800 million. Its automated commercial insurance operations network has connected more than 5,000 hospitals, and the “City One-Account Pass” app has been launched in 68 cities. The company raised $1.15 billion in its first round of financing, reaching a post-money valuation of $8.8 billion, making it a bona fide unicorn.

Household Remedies

In 2012, Professor Fang Zhiwu resigned from Express Scripts’ ESI division to found Wanhu Liangfang, aligning the Pharmacy Benefit Management (PBM) model with China’s healthcare reform initiative of tiered diagnosis and treatment, thereby establishing a Chinese PBM model. Centered on the core mission of “lowering drug prices, safeguarding medical insurance funds, and benefiting public welfare,” Wanhu Liangfang provides solutions consistent with the direction of healthcare reform. By situating its service delivery within community health service centers, the company delivers high-quality services to its enrolled members.

Wanhu Liangfang’s products and services encompass several key areas: First, a family physician empowerment system. In collaboration with Professor Gu Yuan, a leading authority in the field of family medicine, we have established a family physician training system to empower healthcare professionals at community health service centers and launched an elite general practitioner development program. Second, an information technology system, including the establishment of a Pharmacy Benefit Management (PBM) database and comprehensive IT solutions. Third, a centralized drug procurement system that negotiates with pharmaceutical manufacturers to implement “group purchasing,” thereby reducing drug prices.

The Wanhu PBM model has been rolled out in cities such as Wuhu (Anhui), Taiyuan (Shanxi), and Nanjing (Jiangsu). The pilot program in Wuhu was the earliest, expanding from a single community health service center to the district and municipal levels. It currently manages medication for over 100,000 patients with chronic diseases, providing prescribed drugs at designated locations, on fixed schedules, and in specified quantities.

Jianyibao, Quanyi Health, Medbanks, Yaoshiquan, Meideyi, Jindou Data, and Neusoft Wanghai are all innovative companies that have emerged within the framework of healthcare payment. Why is healthcare payment a issue worth attention, or why is innovation in healthcare payment a promising direction?

Let us first examine the case of the United States. As previously reported by VCBeat, healthcare is one of the most critical industries in the U.S., with healthcare expenditure accounting for approximately 18% of its GDP—significantly higher than that of other developed countries. Research indicates that patient out-of-pocket payments constitute 35% of healthcare providers’ revenue, second only to Medicare and Medicaid. However, complex medical billing and the rising proportion of out-of-pocket costs have become barriers to healthcare payment, creating opportunities for innovation.

Amidst complex and bloated medical processes and difficult-to-understand bills, healthcare payment has become a significant area of innovation in the United States. VCBeat has identified approximately 10 companies in this sector, including Patientco, Simplee, Cedar, and CareCloud. All these companies have received capital support, with Cedar raising a total of $49 million, Simplee $37.8 million, and Patientco $31.8 million.

A similar entrepreneurial environment exists in China: In 2017, China’s total health expenditure reached RMB 5.16 trillion, accounting for 6.2% of GDP, a proportion that has been steadily rising in recent years. In 2017, out-of-pocket health payments amounted to RMB 1.49 trillion, representing 28.8% of total health expenditure. Although the share of out-of-pocket spending has been continuously declining, it remains significantly higher than that in other developed countries. Meanwhile, basic medical insurance funds are also under operational pressure: official reports previously projected that by 2024, the Urban Employee Basic Medical Insurance Fund would face a cumulative deficit of RMB 735.3 billion.

Therefore, there are two key tasks in healthcare financing: first, to ensure the efficient and prudent management of basic medical insurance funds while curbing the risk of fund deficits; and second, to accelerate the development of commercial health insurance, thereby establishing a multi-tiered and diversified social healthcare security system that minimizes the out-of-pocket financial burden on individuals.

Following the establishment of the National Healthcare Security Administration, medical insurance administration has been placed under a unified management body, with cost-containment measures further strengthened through initiatives such as the “4+7” volume-based procurement and reforms in healthcare payment methods. As public medical insurance undergoes structural optimization—shifting resources from low-value to high-value services—the responsibility for meeting remaining healthcare service demands has fallen to commercial health insurers. Can these insurers effectively assume this role? They require “empowerment” not only in product design but also in operational management.

Here, we may as well make some predictions about the future trends in the health insurance industry:

1. Stricter management of medical insurance funds, with continuous advancement of payment method reforms;

2. Increased involvement of commercial health insurance companies in administering various medical insurance services;

3. Insurance needs of individuals with pre-existing conditions are being tapped, making chronic disease insurance the norm;

4. The market size of commercial health insurance continues to expand, with an increasing number of innovative health insurance companies;

5. The increasing number of TPA companies provides more diversified third-party services;

6. Health insurance companies and healthcare service providers are forging closer ties, achieving interoperability in information, data, and systems;

7. The application of new technologies—cloud computing, big data, the Internet of Things (IoT), mobile internet, and artificial intelligence (AI)—has become more widespread, comprehensively enhancing the product development, operational, and service capabilities of health insurance.

8. Health management and incentives for user health behaviors have become important components of health insurance, promoting healthy lifestyles.

[References]

1. Minsheng Securities - Health Insurance Market Analysis and Outlook: A Blue Ocean with Trillion-Yuan Potential

2. Clover Health: How Technology Is Reshaping the Health Insurance Industry | Insurance Insights

3. EY China Commercial Health Insurance White Paper