Unlocking Pharmaceutical Investment Opportunities Through the Evolution of Human Disease Patterns

Editor’s Note: This article is republished from Zhiyin Medicine, authored by Zhiyin Capital. VCBeat has obtained authorization to republish it.

Meeting patients’ clinical needs is an enduring theme in pharmaceutical R&D innovation and the most direct approach for healthcare investors to identify investment opportunities. The fundamental reason for the pharmaceutical industry’s longevity lies in humanity’s growing aspiration for a higher quality of healthy living. Ultimately, it is this sustained and robust demand that drives innovation and investment in the pharmaceutical sector, underpinning its long-term prosperity.

Corresponding to the robust clinical demand is the spectrum of human diseases and its evolution. In the author’s view, the etiologies of human diseases can be categorized into two major types. The first type comprises exogenous diseases, such as those acquired through bacterial or viral infections, including infectious diseases (e.g., respiratory tract infections), hepatitis C, cervical cancer, and HIV/AIDS. The second type consists of endogenous diseases (which are also influenced by external factors), caused by excessive compensatory mechanisms of the body (such as those involving the immune system) or organ dysfunction. These diseases are mostly multifactorial or have no clear etiology, examples being hypertension, diabetes, cancer, and rheumatoid arthritis. For exogenous diseases, humanity seems always able to adopt strategies to eradicate them completely, thereby achieving a cure. In contrast, for endogenous diseases with unclear etiologies, humanity currently appears “powerless,” able only to delay and control disease progression, thus rendering them chronic conditions.

By the late 1970s, China had basically completed the epidemiological transition, with the leading causes of death shifting from acute infectious diseases to chronic diseases. Deaths attributable to chronic diseases accounted for more than 85% of all deaths in China, making them the primary contributor to the national mortality rate.

A study published in The Lancet compiled statistics on the causes of death among the Chinese population at two time points, 1990 and 2013, covering 240 diseases or injuries. The author has arranged them in descending order based on the causes of death in 2013, with diseases showing an increase in annual deaths marked in red, as shown in the table below:

The author has identified many interesting phenomena from this table, which are shared as follows:

1. This table presents statistics on causes of death in China for the years 1990 and 2013, implicitly involving two variables: first, changes in population size (1.143 billion in 1990 versus 1.361 billion in 2013); and second, shifts in population structure, with China’s population trending toward aging. Therefore, for causes of death with identical numbers of fatalities in 1990 and 2013, one cannot conclude that their incidence and mortality rates were consistent.

2. In terms of the broader trend:

The mortality rates of infectious diseases such as diarrhea, lower respiratory tract infections, intestinal nematode infections, and meningitis have decreased significantly due to the invention and widespread use of antibiotics;

Maternal disorders (postpartum hemorrhage), neonatal diseases (preterm birth), and malnutrition have seen a significant reduction in case fatality rates due to improvements in medical facilities and technology;

Although medications can improve conditions such as cardiovascular diseases, cancer, diabetes, rheumatoid arthritis, and HIV/AIDS, they cannot provide a cure. Furthermore, the rising prevalence of these chronic diseases has led to a year-on-year increase in mortality rates;

Some disease areas remain without effective treatments, such as Alzheimer’s disease, Parkinson’s disease, and chronic kidney disease. With the aging population, the incidence of these conditions continues to rise, leading to a significant increase in annual mortality rates.

3. The top three causes of death are cardiovascular and cerebrovascular diseases, cancer, and chronic obstructive pulmonary disease (COPD). These three categories account for nearly 80% of all deaths in China, making them undeniably major disease burdens.

R&D for cardiovascular diseases was concentrated in the 1980s, yielding numerous antihypertensive, lipid-lowering, and anticoagulant drugs with diverse mechanisms of action. Many of these became blockbuster drugs in the 1990s and 2000s. Currently, pharmaceutical companies are investing relatively less in innovative drug R&D in this field, as existing medications demonstrate favorable efficacy and safety profiles, largely meeting certain clinical needs.

Oncology R&D is currently the hottest area for research, development, and investment, attracting substantial capital inflows. The emergence of PD-1 inhibitors has brought hope for curing cancer to humanity; however, this clinical need remains far from being fully met. Consequently, capital is increasingly concentrated in the fight against cancer, making it a focal point of ongoing R&D efforts.

COPD is a progressive and irreversible disease. Current medications can slow its progression but cannot reverse it. Furthermore, the penetration rate of these drugs remains low. Since they are typically administered via inhalation devices, which are difficult to replicate, the rate of domestic substitution is low. Therefore, significant opportunities still exist for generic versions.

4. It is truly staggering that, excluding traffic accidents and accidental injuries, Alzheimer’s disease and other forms of dementia have become the fourth leading cause of death in China. Moreover, with a severe lack of available therapeutics and a continuously rising incidence rate, neurological disorders such as Alzheimer’s disease, Parkinson’s disease, amyotrophic lateral sclerosis (ALS), and multiple sclerosis will represent the next major diseases that humanity must conquer.

5. The incidence and mortality rates of complications such as liver cirrhosis, hepatitis, chronic kidney disease, nephritis, and pulmonary fibrosis—caused by other factors (e.g., alcohol consumption, air pollution) or chronic conditions (e.g., diabetes)—are continuously rising. Currently, there are no effective medications available to control or reverse these conditions. Just as non-alcoholic steatohepatitis (NASH) has become a hot spot for investment, these areas will represent blue-ocean markets in the future management of chronic diseases.

6. Alcohol use disorder, primarily alcohol abuse; and substance use disorders, such as addiction to opioids, cocaine, and amphetamines. These conditions impose a particularly heavy healthcare burden in the United States, yet there are currently no highly effective alternative or withdrawal medications available.

7. The incidence of musculoskeletal disorders, such as rheumatoid arthritis, is on the rise, a trend that has given birth to today’s blockbuster drug, Humira. Although pharmacological treatments have improved significantly compared to the past, autoimmune diseases such as rheumatoid arthritis, ankylosing spondylitis, systemic lupus erythematosus, and ulcerative colitis still lack satisfactory clinical solutions.

The above statistics cover the more common causes of disease-related mortality, excluding numerous rare diseases such as idiopathic pulmonary arterial hypertension, idiopathic pulmonary fibrosis, and generalized myasthenia gravis. Additionally, many prevalent conditions are not fatal but significantly impair quality of life, including obesity, hair loss, benign prostatic hyperplasia, overactive bladder, non-alcoholic steatohepatitis (NASH), pain, chemotherapy-induced nausea and vomiting, sleep disorders, and dry age-related macular degeneration. Therefore, a substantial number of disease areas remain inadequately treated.

The evolution of incidence rates in the human disease spectrum can effectively predict future market potential, while changes in current disease mortality rates reveal which conditions remain underserved by existing treatments. Before exploring opportunities in the next chronic disease sector, it is instructive to review the evolution of blockbuster drugs over the past three decades.

The author compiled the top 10 best-selling drugs globally for the years 1990, 2000, and 2015, as follows:

These three figures effectively illustrate the pharmaceutical industry’s shifting focus on specific disease areas across different periods, and how the discovery of related targets has driven advances in disease treatment:

~1990s: Focus on hypertension (selective β-blockers, calcium channel blockers, angiotensin-converting enzyme inhibitors); COX-2 nonsteroidal small-molecule anti-inflammatory drugs; antibiotics and H2 receptor antagonists for the treatment of peptic ulcers and other conditions

~2000: Statins (HMGCR inhibitors) for lipid-lowering; proton pump inhibitors for digestive system diseases; and psychotropic drugs for depression (5-HT) and epilepsy, as well as certain antibiotics.

2015~: Primarily focused on drugs for autoimmune diseases and oncology, insulin glargine, and gliptin-based diabetes medications;

Across these three years, the top five drugs all originated in the field of mass-market chronic diseases, with shifts in the rankings driven by therapies featuring novel targets and mechanisms.

Two trends can be observed from the 2015 drug list:

(1) The current landscape of pharmaceutical therapy is no longer dominated solely by small molecules. In the 2015 sales rankings, the top ten drugs included monoclonal antibodies, peptides, small molecules, and vaccines. Moreover, if small-molecule drugs for hepatitis C are excluded, biologics demonstrate an overwhelming advantage in sales revenue.

(2) Although lenalidomide, used for treating multiple myeloma, is not a medication for common chronic diseases, it has still become a blockbuster drug. Moreover, an increasing number of orphan drugs are expected to achieve significant economic returns.

The achievements we have made across numerous disease areas stem from a deeper understanding of diseases and the discovery of breakthrough new targets or mechanisms, which inevitably involve a significant element of luck. The lack of effective clinical treatments in many other fields today is not due to an absence of clinical need, but rather because these diseases are more challenging to tackle, our understanding remains insufficient, or we have simply not been fortunate enough.

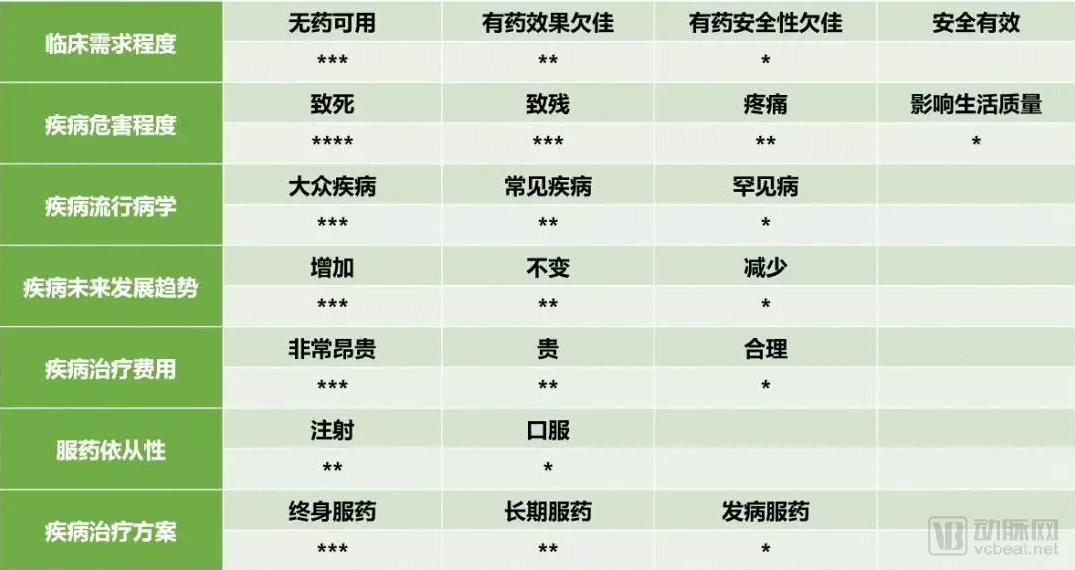

In fact, we can design multiple dimensions to qualitatively or quantitatively evaluate the clinical need for different diseases. The author personally uses the following dimensions to assess disease needs (*the more asterisks, the higher the level of clinical need):

It is evident that diseases characterized by a lack of available treatments, high prevalence, the need for lifelong medication, high mortality rates, and rising incidence represent the most ideal therapeutic areas for R&D or investment. Researchers and investors can identify opportunities for the next blockbuster drug by analyzing the disease spectrum.

Certainly, beyond the heavily pursued areas of diabetes and oncology, the investment-hot NASH space, and the notoriously challenging Alzheimer’s disease, there are several major chronic disease areas that I believe urgently need to be addressed:

1. Obesity

The Lancet published the largest obesity study to date, revealing that the global obese population has reached 640 million. Obesity is associated with numerous complications, including type 2 diabetes, hypertension, metabolic syndrome, dyslipidemia, myocardial infarction, stroke, certain cancers, sleep apnea, and osteoarthritis. Obesity has severely impacted the health of many individuals and imposed a substantial economic burden on society. Currently, there are few weight-loss medications available on the market, and those that exist often suffer from limited safety profiles, modest efficacy, and frequent adverse reactions. Furthermore, both physicians and patients lack sufficient awareness regarding pharmacological interventions for obesity. Consequently, this therapeutic area represents a significant untapped market with considerable long-term potential.

2. Chronic Kidney Disease

According to the report released at the 2017 World Congress of Nephrology, one in ten people worldwide suffers from kidney disease, yet most individuals are unaware of their condition. Epidemiological studies indicate that the prevalence of chronic kidney disease (CKD) among Chinese adults is 10.8%, while acute kidney injury (AKI) occurs in approximately 4% of hospitalized patients. Diabetic kidney disease (DKD), one of the most significant complications of diabetes, currently lacks specific pharmacotherapies capable of altering its clinical course. Consequently, there remains a substantial unmet medical need in the field of chronic kidney disease.

3. Gout

Hyperuricemia, known as the “fourth high” following hypertension, hyperlipidemia, and hyperglycemia, poses significant threats to human health. The global annual incidence rate ranges from 0.20% to 0.35%. In the United States, the prevalence of gout is approximately 3.9%. Currently, therapeutic options in this field are limited, with most drugs causing either hepatotoxicity or nephrotoxicity; furthermore, the classic drug allopurinol is associated with severe hypersensitivity reactions. URAT1 inhibitors remain the most active area in the global R&D pipeline. Two drugs targeting this mechanism have been approved: benzbromarone and lesinurad (Zurampic). However, both are limited by side effects such as hepatorenal toxicity, precluding their long-term clinical use. Therefore, there is an urgent need for novel agents with well-defined mechanisms and favorable safety profiles.

4. Pain (Chronic Pain, Cancer Pain, Neuropathic Pain)

According to a report on non-opioid drug development released by BIO in February 2018, up to 100 million people in the United States suffer from chronic pain, resulting in annual healthcare expenditures exceeding $600 billion. The number of deaths caused by opioid overdoses each year surpasses those from motor vehicle accidents. The entire pharmaceutical industry has made slow progress in developing non-opioid, non-addictive alternative analgesics, due to factors including a lack of fundamental scientific understanding of pain and market hesitancy toward adopting new drugs. Nevertheless, there is an urgent human need for non-opioid medications that offer efficacy comparable to opioids without the risk of addiction.

The disease areas selected above represent merely the author’s personal perspective, intended to spark discussion and encourage peers to reflect on investment opportunities from the standpoint of the disease spectrum.

The persistent mismatch between evolving clinical needs and available treatment capabilities constitutes the primary contradiction in the advancement of human health. The innovative drug research and development (R&D) industry has emerged in response to this demand and discrepancy. The invention of innovative therapies has extended human life expectancy, which in turn has given rise to new disease spectra and replaced old disease-related challenges, thereby generating new therapeutic demands. Where there is demand, there is naturally a market; and where there is a market, there is inherent momentum for R&D and investment. Consequently, changes in the disease spectrum and the R&D of innovative drugs are mutually causal. This intertwined co-evolution has driven the robust growth of the pharmaceutical industry.

To date, human life expectancy has approached 80 years. Reflecting on the history of humanity’s fight against disease, the author offers the following thoughts:

1. Antibiotics Sector: Bacteria and humans are locked in a struggle for survival, with the upper hand shifting back and forth. In an effort to combat multiple bacterial species simultaneously, there has been a strong drive to develop broad-spectrum antibiotics. However, driven by natural selection, drug-resistant bacteria continue to emerge, evolving into “superbugs” that are nearly impossible to eradicate.The current landscape of antibiotic development remains grim; we are still at a loss against numerous drug-resistant bacteria, and these infections continue to claim many lives.

2. Cardiovascular and cerebrovascular diseases, diabetes, and other therapeutic areas: Although numerous drugs are already available, these conditions remainFields That Produce Super Blockbusters, of course, it is also a game played by large pharmaceutical companies. Such fieldsInnovative Drugs with Novel Mechanisms Also Present Opportunities, but most require head-to-head comparisons with established drugs to demonstrate superior survival benefits. Examples include Repatha (PCSK9 inhibitor), apixaban (anticoagulant), Entresto (for chronic heart failure), and semaglutide (for diabetes). These are novel-mechanism drugs that have emerged in recent years within this therapeutic area, each with a projected peak annual sales exceeding $5 billion.

3. Currently, humanity has only achieved chronic disease management for common conditions such as cardiovascular diseases, diabetes, COPD, rheumatoid arthritis, and HIV/AIDS; however, there remains an urgent lack of treatments for many other common chronic diseases in various fields, as mentioned above:Tumors, obesity, NASH, chronic rhinosinusitis, sleep disorders, chronic kidney disease, liver cirrhosis, analgesia, Alzheimer's disease, Parkinson's disease, alopecia areata, dry age-related macular degeneration, gout, pulmonary fibrosis, pulmonary arterial hypertension, osteoporosis, type 1 diabetesThese areas remain a blue ocean, urgently awaiting breakthroughs.

4. In addition to the segment focused on common chronic diseases,Development of Rare Disease (Orphan) DrugsThey are also increasingly favored by large pharmaceutical companies due to factors such as the lack of existing treatments, high R&D success rates, and rapid clinical development. There remains a significant number of rare diseases for which humanity has no effective solutions, such as amyotrophic lateral sclerosis, idiopathic pulmonary arterial hypertension, and phenylketonuria; these conditions also present considerable investment opportunities.

5. For common chronic diseases (with multiple or unknown etiologies), current interventions can only slow disease progression but cannot reverse it; therefore, weCan We Progress from Delaying to Reversing and Ultimately Curing in the Future?

6. Currently, human understanding of most diseases remains incomplete, and perspectives on diagnosis and medical care are outdated. Consequently, therapeutic interventions are often administered only in the late stages of disease progression, akin to Bian Que’s treatment of Duke Huan of Cai. A truly superior physician would resemble Bian Que’s elder brother,Will the future development trend shift from disease treatment to disease prevention?, such as shifting more R&D efforts from treating patients with advanced-stage cancer to preventing cancer? Indeed, many current anti-cancer studies are focusing on inhibiting cancer metastasis and recurrence.

7. The ultimate challenge facing the cause of human health remains longevity (including organ failure), and we currently lack reliable technical means to verify that it is possible toAnti-aging.However, there is a substantial body of related research, including studies on mitochondria, gut microbiota, blood transfusion, and targeted senescent cells. Due to the immense complexity of the aging process, our current understanding remains insufficient. Nevertheless, I remain convinced that aging is reversible; while the path may be tortuous, the future is bright.

This article systematically reviews the evolution of the human disease spectrum and blockbuster drugs, aiming to provide readers with a perspective for thinking about the R&D and investment of innovative drugs through the lens of disease patterns. The author has included personal insights on chronic diseases, intended to spark discussion and encourage collective reflection among pharmaceutical professionals. Venture capital firms or industrial M&A funds in the healthcare sector may consider early, track-based positioning according to disease areas, though this is merely one strategic approach.

From the perspective of combating disease progression, we have only made modest gains, with many diseases still requiring better prevention and treatment. As the human desire for health becomes increasingly prominent, innovation in the pharmaceutical sector will advance more rapidly, bolstering our confidence in this trajectory.

There is still much to be done in the pharmaceutical industry; even after another century of development, we believe there will remain many unmet clinical needs.

References:

【1】Zhou, Maigeng, et al. "Cause-specific mortality for 240 causes in China during 1990–2013: a systematic subnational analysis for the Global Burden of Disease Study 2013." The Lancet 387.10015 (2016): 251-272.

【2】Roth, Gregory A., et al. "Global, regional, and national age-sex-specific mortality for 282 causes of death in 195 countries and territories, 1980–2017: a systematic analysis for the Global Burden of Disease Study 2017." The Lancet 392.10159 (2018): 1736-1788.

【3】Zhu, Bifan, et al. "Disease burden of COPD in China: a systematic review." International journal of chronic obstructive pulmonary disease 13 (2018): 1353.