Who Will Be the First Biopharma Beneficiaries of China’s Sci-Tech Innovation Board?

On February 27, 2019, the State Council Information Office held a press conference on the establishment of the STAR Market and the pilot registration-based IPO system. Yi Huiman, Chairman of the China Securities Regulatory Commission (CSRC), along with Vice Chairmen Li Chao and Fang Xinghai, and Huang Hongyuan from the Shanghai Stock Exchange, introduced the initiative. This marked Yi Huiman’s first public media appearance since assuming office one month prior.

Yi Huiman introduced the purpose and significance of the STAR Market at the meeting, emphasizing that it would adhere to the principle of “strict standards and a steady start.” He highlighted the need to maintain balance across various markets to ensure the smooth launch and implementation of the STAR Market and the pilot registration-based IPO system. He stated, “The establishment of the STAR Market holds significant strategic importance for supporting technological innovation, promoting high-quality economic development, advancing market-oriented reforms in the capital market, and accelerating the construction of Shanghai as an international financial center.”

Image from People's Daily

Since its announcement in November 2018, every news update regarding the establishment of the STAR Market has sparked intense public attention. Primarily targeting strategic emerging industries, the STAR Market’s listing criteria are better aligned with the characteristics of innovative sectors and companies, offering greater inclusivity.

In February 2019, the China Securities Regulatory Commission (CSRC) released the Implementation Opinions on Establishing the Science and Technology Innovation Board (STAR Market) at the Shanghai Stock Exchange and Piloting the Registration-Based IPO System, with related work progressing in an orderly manner. Meanwhile, supporting rules, including the Shanghai Stock Exchange’s Rules for Reviewing the Issuance and Listing of Stocks on the STAR Market, were open for public comment in accordance with established procedures. Three months after the announcement of its establishment, the long-anticipated “blueprint” for the implementation of the STAR Market was finally unveiled.

Pilot registration-based IPO system, expanded daily price fluctuation limits for stocks, and no price fluctuation caps during the first five trading days after listing... The STAR Market features numerous highlights in areas such as mandatory co-investment by sponsoring securities firms, price fluctuation limits, issuance pricing, delisting mechanisms, and information disclosure requirements. For investors and entrepreneurs alike, the establishment of this new listing channel undoubtedly provides an additional avenue for exit and financing.

As early as the evening of January 30, 2019, the China Securities Regulatory Commission (CSRC) and the Shanghai Stock Exchange (SSE) intensively issued multiple policy rules targeting the STAR Market, including three departmental regulations—such as the “Measures for the Administration of Registration of Initial Public Offerings on the STAR Market (Draft for Comments)” —and six exchange rules. The previously market-focused T+0 trading mechanism and the RMB 500,000 investor eligibility threshold remained unchanged, reflecting the principle of “prioritizing quality and ensuring stability.”

Of greater note, the Shanghai Stock Exchange has unveiled five market capitalization criteria for initial public offerings, which may serve as a reference for startups eyeing the STAR Market.

The detailed rules stipulate:

(1) The projected market capitalization is no less than RMB 1 billion, with positive net profits in each of the last two years and cumulative net profits of no less than RMB 50 million; or the projected market capitalization is no less than RMB 1 billion, with a positive net profit in the most recent year and operating revenue of no less than RMB 100 million;

(II) The estimated market value is no less than RMB 1.5 billion, the operating revenue for the most recent year is no less than RMB 200 million, and the aggregate R&D investment over the most recent three years accounts for no less than 15% of the aggregate operating revenue over the same period;

(3) The projected market capitalization is no less than RMB 2 billion, the operating revenue for the most recent year is no less than RMB 300 million, and the cumulative net cash flow from operating activities over the past three years is no less than RMB 100 million;

(4) The projected market capitalization is not less than RMB 3 billion, and the operating revenue for the most recent year is not less than RMB 300 million;

(5) The estimated market capitalization shall be no less than RMB 4 billion. The main business or products must be approved by relevant national authorities, possess significant market potential, have achieved phased results, and have secured investment of a certain amount from well-known investment institutions. Pharmaceutical companies must have obtained approval for at least one Class I new drug to enter Phase II clinical trials. Other enterprises aligned with the positioning of the STAR Market must demonstrate clear technological advantages and meet the corresponding conditions.

Among these developments, the most exciting aspect is the STAR Market’s support for high-tech enterprises that are not yet profitable. With the release of the detailed implementation rules, we cannot help but wonder which companies will be among the first to list. Significant innovation and corporate valuation may serve as key criteria for listing on the STAR Market. Drawing on VCBeat’s “2018 Future Healthcare 100” and New Drug Rankings, and combining them with the detailed rules issued by the Shanghai Stock Exchange, we have made predictions based primarily on the following criteria:

1) Biopharmaceutical companies valued at over RMB 4 billion, with at least one Class I new drug in their pipeline having obtained approval for Phase II clinical trials;

Note: Due to the difficulty in accurately obtaining revenue data for startups, other detailed rules will not be discussed at this time.Discussion.

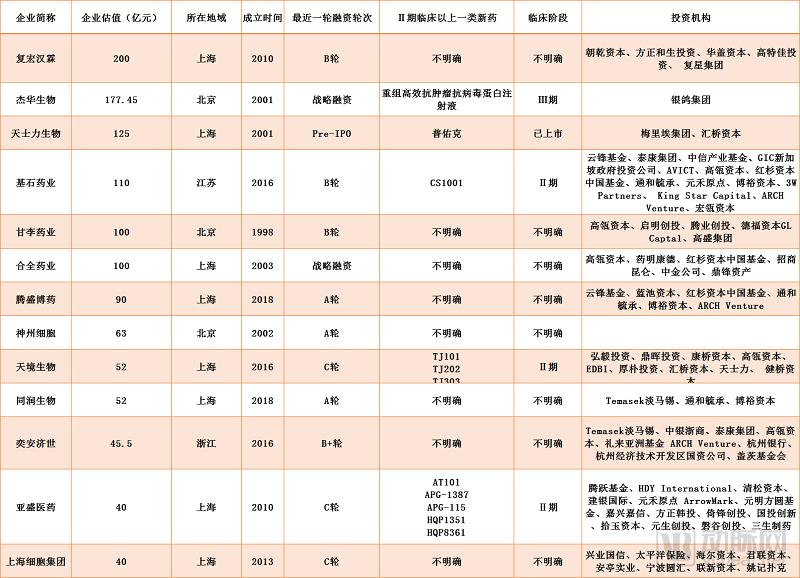

These detailed rules apply to enterprises with significant product pipelines and substantial strategic importance. In the healthcare sector, biopharmaceutical companies are at the forefront. According to VCBeat’s 2018 New Drug List, 13 of these companies had valuations exceeding RMB 4 billion.

Among these companies, the highest valuation reached RMB 20 billion, while the lowest was RMB 4 billion. All of them have products in various stages of clinical development. Given that the STAR Market imposes requirements on the drug pipelines of pre-profit biopharmaceutical companies, we further screened these companies’ pipelines and identified those with at least one innovative drug candidate that has entered Phase II clinical trials.

Ultimately, a total of five companies met this criterion: Genor Biopharma, Tasly Biologics, CStone Pharmaceuticals, I-Mab, and Ascentage Pharma.

In terms of product development progress, Jiehua Biopharmaceutical and Tasly are leading the pack: Jiehua Biopharmaceutical’s recombinant high-efficiency anti-tumor and antiviral protein injection has entered Phase III clinical trials, while Tasly’s original innovative drug, Puyouke, has already been launched to the market with impressive performance.

Among the other three companies, Ascentage Pharma has five Class 1 new drugs in Phase II clinical trials, with interim results from two clinical studies presented at the ASCO 2018 annual meeting; I-Mab’s TJ101, TJ202, and TJ301 are also in global Phase II clinical development, primarily indicated for pediatric growth hormone deficiency, cancer, and autoimmune diseases; CStone Pharmaceuticals focuses on combination immuno-oncology therapies, with its product CS1001 having entered Phase II clinical trials, positioning it as one of the leading domestic companies targeting PD-L1.

CStone Pharmaceuticals was listed on the Hong Kong Stock Exchange on February 26, 2019, while Tasly Biopharmaceuticals has already submitted a listing application to the Hong Kong Stock Exchange. Ascentage Pharma first filed its listing application in August 2018; however, that application has since lapsed, leaving open the possibility of a U.S. listing (Ascentage Pharma had begun preparing for a U.S. IPO even before the opening of the Hong Kong stock market).

However, our review of business registration information reveals that the controlling entities of Ascentage Pharma, CStone Pharmaceuticals, and I-Mab are all overseas legal persons, indicating the possible existence of VIE structures.

If a company lacks any Class 1 new drugs that have entered Phase II clinical trials or later stages, does this mean it has no possibility of going public? Certainly not. Even without any marketed products, if there is a market gap and the company holds a clear competitive advantage over its peers, it may still exhibit a strong trend toward profitability despite current losses. Such companies are also taken into consideration for listing on the STAR Market.

We have once again expanded the scope of our pharmaceutical ranking to include companies with valuations between RMB 3 billion and RMB 4 billion, totaling nine enterprises. These companies must offer products that either fill gaps in the domestic market or pioneer new markets, based on the following criteria:

1) Whether it fills a domestic gap or creates a new market;

2) Are there other competitors in the current market, and do they possess competitiveness?

We have taken into account valuation, pipeline, and market factors to compile a list of potential IPO candidates: Henlius, Junshi Biosciences, CanSino Biologics, Genor Biopharma, and Caying Technology.

Among these companies, Henlius is undoubtedly highly competitive. On February 25, 2019, Henlius’s rituximab injection (HLX01) was officially approved by the National Medical Products Administration for the treatment of non-Hodgkin lymphoma, becoming the first domestically produced rituximab injection to receive formal approval in China. Its product, adalimumab, has also had its marketing application accepted. From December 2015 to April 2017, Henlius obtained approvals for two indications of this drug, for the treatment of rheumatoid arthritis and plaque psoriasis, respectively.

Rituximab (MabThera), originally developed by Genentech, a subsidiary of Roche Pharmaceuticals, was the first monoclonal antibody approved by the FDA in 1997 for the treatment of cancer. According to Roche’s financial reports from the past two years, global sales of this product reached CHF 7.388 billion in 2017.

Patent protection for rituximab has expired in Europe and the United States in 2014 and 2018, respectively. In China, companies such as Hisun Pharmaceutical, Chia Tai Tianqing, Innovent Biologics, Hualan Biological Engineering, and Livzon Mabpharm are actively developing and filing regulatory applications for biosimilars of MabThera. Among them, the rituximab biosimilars from Innovent Biologics and Hisun Pharmaceutical are both in Phase III clinical trials.

Adalimumab (Humira) is a fully human monoclonal antibody against TNF-α developed by AbbVie, primarily indicated for rheumatoid arthritis, psoriasis, ankylosing spondylitis, and Crohn's disease. It received FDA approval on December 31, 2002, and was introduced to the Chinese market on February 26, 2010, under the brand name Humira.

Public data show that Humira’s sales reached $18.9 billion in 2017, an 18% year-on-year increase, ranking first globally in pharmaceutical sales. However, due to pricing factors and differences in market awareness, the penetration rate of adalimumab in China remained extremely low, with domestic sales in 2017 totaling only about $140 million, accounting for approximately 0.1% of global sales.

HLX03 is the third monoclonal antibody project developed by Henlius. The company stated that it has demonstrated pharmacokinetic bioequivalence to the originator drug, Humira, with similar safety and immunogenicity profiles. Furthermore, patients in China with rheumatoid arthritis, psoriasis, and ankylosing spondylitis collectively account for approximately 9.0% of global cases, representing a substantial market size.

Zhongtai Securities stated: “Adalimumab Injection HLX03 will become an affordable alternative for patients with relevant diseases in China, and is expected to enter the market and capture a share of the large potential market for rheumatoid arthritis.”

Currently, there are no domestically produced biosimilars targeting this agent available on the Chinese market. The high cost of the originator drug remains unaffordable for most patient families. However, in addition to Henlius, biosimilar adalimumab candidates from Bio-Thera Solutions, Innovent Biologics, and Hisun Pharmaceuticals are all in the stage of filing for marketing approval. Consequently, the drug will face significant competitive pressure upon its market launch.

In addition to Humira and adalimumab biosimilars, Henlius’s HLX02 (Herceptin) and HLX04 (Avastin) have both reached Phase III clinical trials. First-in-class innovative drugs such as HLX22, HLX10, and HLX20 have also entered clinical development. As its biosimilar projects advance rapidly, Henlius’s innovative achievements are increasingly evident. A mature and comprehensive integrated platform for monoclonal antibody biologic development has been quietly established, positioning the company as a leader in the monoclonal antibody field.

Junshi Biosciences also holds a competitive advantage. As an innovation-driven biopharmaceutical company, it is dedicated to the global research, development, and commercialization of innovative drugs.

Junshi Biosciences is a leader in China in the fields of tumor immunotherapy, autoimmune diseases, and metabolic disease treatment. It was the first Chinese company to submit an Investigational New Drug (IND) application and a New Drug Application (NDA) for an anti-PD-1 monoclonal antibody to the National Medical Products Administration (NMPA). Additionally, it was the first Chinese company to receive NMPA approval for IND applications targeting anti-PCSK9 and anti-BLyS monoclonal antibodies.

Currently, Junshi Biosciences’ core product, JS001 (PD-1), is the first domestically approved drug targeting this checkpoint. The product is named toripalimab injection (brand name: Tuoyi), an anti-PD-1 monoclonal antibody. On the evening of January 7, 2019, Junshi Biosciences announced the price of toripalimab injection (Tuoyi), consistent with prior rumors: RMB 7,200 per 240 mg vial, equivalent to RMB 30 per mg, resulting in an annual treatment cost of RMB 187,200. Compared with Merck’s Keytruda, which is indicated for the same conditions, the price of toripalimab is less than one-third that of Keytruda.

On February 26, 2019, Junshi Biosciences began nationwide distribution of its anti-PD-1 monoclonal antibody, toripalimab injection. In collaboration with charitable organizations, the company launched a patient assistance program: eligible patients with melanoma can receive four cycles of medication free of charge for every four cycles they pay for out-of-pocket. Upon successful application, the annual cost of treatment can be reduced to as low as RMB 93,600.

Tuoyi has two indications under Phase III clinical trials (first-line melanoma and nasopharyngeal carcinoma) and four indications under Phase II clinical trials (gastric cancer, esophageal cancer, urothelial carcinoma, and non-small cell lung cancer). For this product, Junshi Biosciences also initiated a Phase I clinical trial in the United States in March 2018. In addition, Junshi Biosciences’ biosimilar UBP1211 (TNF-α) has entered Phase III clinical trials, with Humira as the reference drug.

In December 2018, Junshi Biosciences listed on the Hong Kong Stock Exchange following its listing on the New Third Board, becoming the first company to achieve a “New Third Board + H-share” dual-listing structure.

CanSino Biologics is a vaccine R&D company, which we previously introduced in our Hong Kong stock market series. The company’s flagship product, an Ebola vaccine, has already been launched on the market. Its other products are at various stages of clinical development, with most nearing commercial launch.

Ad5-EBOV, jointly developed by CanSino Biologics and the Academy of Military Medical Sciences of the Academy of Military Sciences, is the world’s first approved Ebola vaccine. The vaccine market is substantial. CanSino’s product portfolio is primarily categorized into three segments: globally innovative vaccines addressing unmet medical needs in China; vaccines under development with the potential to become first-in-class in China; and world-class vaccines of superior quality designed to replace current mainstream vaccines, as well as potential best-in-class vaccines developed to compete with imported products in the Chinese market.

Currently, in addition to the Ebola vaccine, CanSino has two other products in the clinical trial application and Phase III clinical trial stages, respectively, while its remaining products are all in the early clinical and clinical research stages.

Genor Biopharma is a biopharmaceutical company dedicated to the research, development, and commercialization of antibody-based therapeutics and other novel biologics. Its pipeline primarily consists of monoclonal antibody biosimilars and innovative monoclonal antibody drugs, with the latter focusing mainly on fast-followers and biobetters.

Currently, Jiayue Bio has 10 key monoclonal antibody products under development, all of which have obtained clinical trial approvals in China. Additionally, several of these products are concurrently undergoing clinical trials in overseas markets such as Australia and South Korea.

Public information indicates that Genor Biopharma’s anti-HER2 humanized monoclonal antibody (brand name of the reference product: Herceptin), infliximab biosimilar (brand name of the originator product: Remicade), and bevacizumab biosimilar (brand name of the originator product: Avastin) are all in Phase III clinical trials. Genor’s anti-PD-1 monoclonal antibody is also poised to initiate Phase II and Phase III clinical trials for multiple indications.

Cayin Technology’s R&D team comprises over 50 overseas-returnee and domestically trained PhDs and master’s degree holders, with expertise spanning biomolecular science, pharmacology, process development, quality control, and formulation. The company focuses on the field of liver diseases, boasting a portfolio of products for hepatitis C treatment and establishing a comprehensive product lineup covering antiviral, immunomodulatory, hepatoprotective, anti-hepatic fibrosis, and liver cancer therapies. In 2010, the company completed its joint-stock restructuring. In 2011, it successively introduced strategic partners such as Legend Capital, Haitong Kaiyuan, Cybernaut, and Lilly Asia Ventures.

According to inquiries made with the Center for Drug Evaluation (CDE), Kaiyin Technology currently has 45 applications under review, including 10 generic drug applications, 11 new drug applications (four of which are Class 1 new drugs and three are Class 1.1 new drugs), one import drug application, with the remainder being supplemental applications.

In June 2016, Cayan Technology submitted an IPO prospectus to the Shenzhen ChiNext. The prospectus revealed that the company’s operating revenues for 2013, 2014, and 2015 were RMB 200.4297 million, RMB 225.1478 million, and RMB 267.7473 million, respectively, while the net profits attributable to shareholders of the parent company were RMB 17.0572 million, RMB 12.0936 million, and RMB 23.9305 million, respectively. However, this IPO attempt was unsuccessful, as the issuer planned to undertake financing and adjust its equity structure.

In addition to pharmaceutical companies, other innovative biotechnology firms with hard-tech capabilities that can fill gaps in the domestic market may also have opportunities. We refer to VCBeat’s 2018 Future Healthcare Top 100 list and select from itBiotechnology companies with a valuation of over RMB 3 billion and a certain scale of revenue.

Both companies are oncology gene sequencing enterprises. Novogene originated in scientific research services and has gradually established a leading genomics service portfolio covering scientific research, oncology, and genetic diseases. Burning Rock Biotech focuses on providing personalized treatment guidance for cancer patients and has now become the industry leader in this field.

Novogene was established in 2011, focusing on pioneering the application of cutting-edge molecular biology technologies and high-performance computing in life science research and human health. The company is committed to becoming a global leader in genomics products and services. Novogene has built leading-scale gene sequencing and high-performance computing platforms, effectively supporting the big data analysis and storage needs in the fields of life science research and healthcare. The company’s business spans more than 50 countries and regions across six continents, serving over 2,000 clients.

Novogene has established extensive collaborative relationships with numerous academic institutions worldwide. As of June 2018, Novogene and its project partners had co-published more than 350 SCI-indexed articles, with a cumulative impact factor exceeding 2,290. The company has obtained 149 software copyrights and 22 patents. Its partners span the globe, including over 1,920 research institutes and universities, more than 720 hospitals, and over 1,430 pharmaceutical and agricultural enterprises.

As a leading player in China’s gene sequencing sector, Novogene offers services spanning basic life science research, medical research and technical services, and library preparation and sequencing platform solutions. It provides gene sequencing, mass spectrometry analysis, and bioinformatics support to research universities, scientific institutes, hospitals, pharmaceutical R&D enterprises, and agricultural companies worldwide.

Furthermore, Novogene’s Class III medical device innovative product, the “Human EGFR, KRAS, BRAF, PIK3CA, ALK, and ROS1 Gene Mutation Detection Kit (Semiconductor Sequencing Method),” received approval from the National Medical Products Administration in August 2018 and was officially authorized for market sale. This product had previously qualified for the Special Approval Pathway for Innovative Medical Devices. It is approved for detecting mutation statuses of six genes closely associated with targeted therapy in FFPE tumor tissue samples from patients with non-small cell lung cancer (NSCLC), thereby identifying patients suitable for targeted drug treatment.

Founded in 2014, Burning Rock Biotech leverages next-generation sequencing (NGS) and medical bioinformatics as its core technologies, with routine molecular pathological testing for tumors as its foundation. The company is dedicated to providing clinical diagnostic services for personalized cancer therapy and comprehensive one-stop research solutions.

Burning Rock Biotech is the only third-party clinical laboratory with a dedicated Department of Clinical Medicine. Furthermore, the company was the first in China to enter the CFDA’s green channel for NGS-based tumor applications, with its corresponding product being the “Human EGFR/ALK/BRAF/KRAS Gene Mutation Combined Detection Kit (Reversible Terminator Sequencing Method).” This kit received market approval from the National Medical Products Administration (NMPA) in August 2018, marking the first NGS-based regulatory approval in the oncology sector issued by the NMPA.

It is reported that the product has been officially launched in major Grade A tertiary hospitals and specialized oncology hospitals across China, primarily for the precise selection of targeted drug therapies for patients with non-small cell lung cancer.

Currently, Burning Rock Biotech has developed more than 30 testing products tailored to different cancer types and clinical stages, covering early cancer screening, differentiation between benign and malignant tumors, companion diagnostics for targeted therapy, monitoring of tumor recurrence, and hereditary cancer testing.

Meanwhile, Burning Rock Biotech has actively pursued in-depth collaborations with leading domestic medical institutions, internationally renowned equipment manufacturers, and pharmaceutical companies. This effort has earned the favor of numerous medical experts and industry-leading corporations, resulting in strategic partnerships with Illumina, AstraZeneca, Agilent, and CTONG.

Whether it is Burning Rock Biotech or Novogene, both companies are fiercely competing in the oncology testing sector. The application of next-generation sequencing (NGS) in personalized cancer treatment is mainly reflected in two aspects: first, identifying the specific gene mutations responsible for tumorigenesis through sequencing; and second, detecting targets for targeted cancer therapies. Currently, the approvals issued by the National Medical Products Administration (NMPA) are all directed toward the detection of targets for targeted cancer drugs. By using gene sequencing to determine whether patients carry specific drug targets before administration, treatment efficiency can be improved, optimal therapeutic efficacy achieved, and healthcare costs reduced for patients. In the current oncology pharmaceutical market dominated by targeted therapies, the detection of targets for targeted cancer drugs holds significant market potential.

Although the NMPA has taken the first step in approving NGS applications for oncology, a closer examination reveals that the currently approved products are all small-panel assays, i.e., those targeting specific loci. This trend is consistent globally; apart from FDA-approved FoundationOne, no other large-panel NGS products for oncology have been approved worldwide. Therefore, we can conclude that while there is substantial and rigid market demand for oncology NGS testing, significant opportunities remain untapped in both regulatory frameworks and product development.

Summary

Fang Xinghai, Vice Chairman of the China Securities Regulatory Commission (CSRC), stated in a media interview that the establishment of the STAR Market would have a significant impact on technological innovation by providing equity financing for early-stage technology enterprises, while also accelerating the growth of China’s high-tech companies.

JPMorgan Asset Management believes that since the concept was proposed in November 2018, market expectations for the launch of the STAR Market have remained high, with various regions previously expressing strong support for actively facilitating companies’ listings on the board. However, the period from the initial proposal to the official release spanned only three months, which further underscores the decision-makers’ substantial support for innovative enterprises and their firm resolve to deepen structural reforms.

Following the launch of the STAR Market, innovative enterprises with substantial growth potential and rapid development, yet constrained by profitability metrics, will receive enhanced financing support. Together with existing trading venues—including the Main Board, ChiNext, SME Board, and NEEQ—it will form a more diverse, multi-tiered financing system, thereby strengthening the capital market’s support for the real economy, particularly the innovation-driven sector.

On January 30, 2019, with the official release of the “Implementation Opinions on Establishing the Science and Technology Innovation Board (STAR Market) at the Shanghai Stock Exchange and Piloting the Registration-Based IPO System” by the China Securities Regulatory Commission (CSRC), it was announced that the highly anticipated STAR Market had finally been launched. China’s capital market is poised for significant transformation.

For the first batch of companies to list on the STAR Market, stringent requirements will certainly apply; these firms will have been carefully selected by securities firms, local governments, regulatory authorities, or the stock exchange before going public. Changes in the rules of the game may also prompt investors to adopt a different approach, potentially allowing them to exercise greater patience with China’s biopharmaceutical enterprises and creating more opportunities for industrial and value investors.

“Earlier, we released the implementation guidelines. The Shanghai Stock Exchange is refining its relevant business rules based on feedback received, and the public consultation period for the CSRC’s two measures will conclude on the 28th,” Yi Huiman stated at the meeting. “Moving forward, we will continue to carry out thorough and meticulous preparatory work to ensure the effective implementation of this major reform.”

Note: The above results were obtained by screening based on reference criteria such as valuation and pipeline. They merely indicate that the company meets our hypothetical listing requirements, but do not imply whether the company currently has an IPO plan, nor do they represent the final outcome.