Investment Institutions Eye Opportunities in the Greater Bay Area's Biopharmaceutical Sector Amid IPO Surge

SCGC

Investment Institutions in Innovative Fields

The plane landed at Guangzhou Baiyun International Airport under the cover of night. Not long after the Rain Water solar term had passed, the humid air carried a gentle warmth. As one of China’s earliest treaty ports, the city remains bustling with traffic and activity, even as its demographic dividend gradually fades.

In recent years, Guangzhou, long renowned for its traditional manufacturing sector, has been committed to industrial innovation, with technological advancement emerging as the city’s new hallmark. Major companies such as NetEase’s headquarters, Tencent’s WeChat division, Vipshop, Cisco’s China Innovation Headquarters, and AsiaInfo’s global headquarters have all established a presence in Guangzhou, while all four of the world’s leading robotics groups are set to build production centers in the city. In its competitive dynamic with neighboring Shenzhen and Hong Kong, Guangzhou has already surpassed Shenzhen in automobile production volume and exceeded Hong Kong in port container throughput.

Today, this tug-of-war is increasingly being replaced by integration. On February 18, 2019, the long-anticipated Outline Development Plan for the Guangdong-Hong Kong-Macao Greater Bay Area (hereinafter referred to as the “Outline”) was released. It centers on the cluster development of the “9+2” cities around the Pearl River Delta’s Lingdingyang area, aiming to form the world’s third-largest urban agglomeration after New York and Tokyo. The “9” refers to nine adjacent cities in Guangdong Province: Guangzhou, Shenzhen, Zhuhai, Foshan, Dongguan, Zhongshan, Jiangmen, Huizhou, and Zhaoqing; the “2” denotes the two Special Administrative Regions of Hong Kong and Macao.

From the inclusion of the Guangdong-Hong Kong-Macao Greater Bay Area (GBA) in the Government Work Report for the first time in 2017, to the signing of the “Framework Agreement on Deepening Guangdong-Hong Kong-Macao Cooperation and Promoting the Development of the Greater Bay Area” by the governments of Guangdong, Hong Kong, and Macao, and further to the release of the “Outline Development Plan for the Guangdong-Hong Kong-Macao Greater Bay Area,” the GBA boasts promising prospects. With the publication of the Outline, a world-class bay area and city cluster are gradually taking shape. In no time, headlines featuring phrases like “Striking Gold in the Greater Bay Area” have frequently appeared in the media.

The Outline, totaling 27,000 words, elaborates on the development of the Guangdong-Hong Kong-Macao Greater Bay Area over the next decade or more from the perspectives of spatial layout, scientific and technological innovation, economy and finance, educational cooperation, cultural soft power, ecological construction, infrastructure connectivity, the Belt and Road Initiative, and regional integration.

A VCBeat reporter found that, although the Outline devotes limited space to the biopharmaceutical sector, it sets a clear direction. The Outline calls for cultivating a batch of major industrial projects in key areas such as protein-based biopharmaceuticals, high-end medical diagnostic and therapeutic equipment, genetic testing, and modern traditional Chinese medicine, while explicitly increasing financial support for innovative pharmaceutical companies and improving capital-raising channels.

This reporter was invited to attend the Second Symposium on “Chinese Pharmaceutical Companies Going Global” held in Guangzhou (hereinafter referred to as the “Symposium”), during which an interview was conducted with Mr. Yuan Quanhong, President and Founding Partner of Jianxin Capital. The Outline mentions “improving capital fundraising channels,” signaling that the Greater Bay Area is opening its doors to various forms of social capital. Given the inherent long development cycles and high-risk nature of biopharmaceutical enterprises, they naturally require substantial funding. At this juncture, investors’ assessments of investment opportunities in the Greater Bay Area’s biopharmaceutical industry are undoubtedly crucial.

Mr. Yuan Quanhong, President and Founding Partner of Jianxin Capital

Jianxin Capital, established in 2010, has successively invested in more than forty biopharmaceutical projects. In retrospect, Jianxin Capital’s investment strategy clearly reflects a consideration of geographic factors. The Yangtze River Delta urban agglomeration was the preferred destination for Jianxin Capital’s early-stage investments in biopharmaceuticals, with half of its deals located in Jiangsu, Zhejiang, and Shanghai, while the remaining projects were based in Beijing and along the southeastern coast. As an early-stage institutional investor, Jianxin Capital typically enters projects around the Series A round, a phase during which company growth is heavily dependent on the external environment. Focusing on regions with mature industrial chain ecosystems and identifying high-quality projects within them is a logical decision-making approach for institutional investors.

However, for Jianxin Capital, the Greater Bay Area stands as an exception to this investment logic. Jianxin Capital has deployed four projects across the Guangdong-Hong Kong-Macao Greater Bay Area, including Shenzhen Chipscreen Biosciences, Zhongshan Akeso Biopharma, Guangzhou Hengnuokang, and Guangzhou Genetron Health, operating in the sectors of small-molecule novel drug R&D, antibody drug R&D, antiviral drug R&D, and molecular diagnostics, respectively. Notably, both Akeso Biopharma and Chipscreen Biosciences rank among the top 10 non-listed companies in the Greater Bay Area in terms of capital attraction. Mr. Yuan Quanhong described Jianxin Capital’s presence in the region as “both inevitable and coincidental,” noting that they were initially drawn by high-quality projects before turning their attention to the region itself.

So when a reporter from VCBeat asked if he had also been busy recently formulating plans to capitalize on opportunities in the Greater Bay Area, Mr. Yuan Quanhong remained calm: “I’ve been very busy lately and haven’t yet discussed investment opportunities in the Greater Bay Area with my team.”

This composure is not without merit, as biomedicine has not historically been a stronghold of the Greater Bay Area (GBA). The region has long been centered on manufacturing, with rapidly growing ancillary sectors such as finance and transportation emerging from it. In recent years, as manufacturing and services have shifted toward high-end segments, the GBA’s industrial mainstream has gradually transitioned to a booming computer technology and services sector driven by Tencent. Against this backdrop, despite the endorsement of IPO star BGI Genomics, the biomedicine sector remains inconspicuous in the GBA’s industrial landscape.

Having reaped the benefits of the Greater Bay Area’s business environment—characterized by an abundance of talent, a high degree of marketization, and favorable policies—Mr. Yuan Quanhong stated that Jianxin Capital will subsequently focus on projects in the Greater Bay Area. “The Greater Bay Area represents the direction of China’s economic development and is the most dynamic region,” he said.

In the investment community, defining the stages of industrial development remains a perennial topic of discussion. Currently, valuations for high-quality biopharmaceutical projects are being driven ever higher, yet Mr. Yuan Quanhong believes that investment levels remain insufficient. “We are still in a pioneering phase characterized by widespread emergence; corporate spheres of influence have not yet been delineated, and no regional dominants have emerged.”

Therefore, in Mr. Yuan Quanhong’s view, product and technological innovation in the biopharmaceutical industry will remain on an upward trajectory in 2019 and even over the next decade. The industry will enter its second half only when enterprises comparable to Tencent and Alibaba in the internet sector emerge, at which point entrepreneurship and investment will cool down. Specifically for 2019, on the one hand, macro-level policies encouraging pharmaceutical innovation will continue to improve; on the other hand, the market share released through structural adjustments of existing generic drugs will be gradually captured by innovative drugs.

For corporate development, technology, talent, land, and capital are indispensable elements. Many biotechnology startups are founded by professionals who possess advanced technologies, thereby naturally meeting the requirements for technology and talent, whereas land and capital often necessitate external support. This creates a demand for an industrial ecosystem, which Mr. Yuan Quanhong describes as an environment with “big fish in big waters” that is favored by venture capitalists. For investors, investment institutions, market entities, industry associations, and industrial parks are important components of the industrial ecosystem.

“Investment is, in fact, an ecosystem where different institutions need to pass the baton at various stages of a project’s development.” The Greater Bay Area boasts a large number of venture capitalists who are active and astute, providing substantial support for regional innovation and entrepreneurship. From a business perspective, the core strengths of small enterprises often lie in technology, while they frequently lack the necessary resources for clinical trials, product manufacturing, and even sales, thus requiring collaboration with partners across the industry chain.

Mr. Yuan Quanhong told VCBeat New Medicine that he has observed a surge in industry collaborations since the start of the new year. These collaborations include partnerships between innovative enterprises, such as Chipscreen Biosciences and Innovent Biologics jointly conducting clinical trials; alliances between innovative companies and industry giants, exemplified by the partnership between Hangzhou Shangjian Biopharmaceutical and China National Biotec Group (CNBG); as well as mergers among innovative firms. Mr. Yuan believes that the shifting attitudes and perceptions of industry giants toward innovative enterprises, coupled with the latter’s recognition of their own shortcomings and subsequent pursuit of external partnerships, represent noteworthy micro-trends within the biopharmaceutical industry. “Collaboration and merger will be the mainstream forms of future development,” he stated.

Despite nearly diametrically opposed views on the 2019 biopharmaceutical outlook, the panelists at the seminar’s roundtable discussion were highly consistent in their perspective on the Greater Bay Area: they all coveted this once-in-a-lifetime historical opportunity.

Roundtable Panelists at the Seminar

Jianxin Capital

Completed Investments: Hennocom, Chipscreen Biosciences, Akeso, Basecare Medical

Mr. Yuan Quanhong pointed out that even without the development plan for the Guangdong-Hong Kong-Macao Greater Bay Area city cluster, Jianxin Capital would still prioritize this region for biomedical and pharmaceutical investments. “Experience has proven that we can always find outstanding entrepreneurs and scientists here, and there are always promising startups. This demonstrates the strength of this region.”

However, it is also important to recognize the shortcomings in the development of the Greater Bay Area. In terms of talent pool, number of enterprises, and financing environment, the Yangtze River Delta region remains unparalleled nationwide. On one hand, the Yangtze River Delta boasts a more robust industrial foundation and a more complete industrial chain; most R&D outsourcing firms, China’s largest clinical trial companies, and the Chinese R&D centers of multinational corporations tend to establish their presence there. On the other hand, while the Greater Bay Area prioritized manufacturing 5–10 years ago, it is now shifting its focus toward innovative enterprises.

“Both in terms of scale and influence, the contribution of the biopharmaceutical industry to the Greater Bay Area lags behind its economic size and strength, with a potentially significant gap.” However, the other side of the coin is that, starting from this baseline, the dividends from policy support and talent availability are far from peaking, presenting a prime opportunity for investors to make their mark in the region’s biopharmaceutical sector. VCBeat New Medicine will use data to elucidate the investment environment for the biopharmaceutical industry in the Greater Bay Area in the final section of this article.

CMB International

Completed Investments: Burning Rock Biotech, Chipscreen Biosciences

Burning Rock Biotech has demonstrated strong capabilities in tumor gene sequencing, while MicroCore Bio is preparing to become one of the first companies listed on the STAR Market. Mr. Zhou Kexiang, Head of Healthcare Investment at China Merchants Bank International (CMBI), stated that as an investment firm headquartered in Shenzhen, CMBI is particularly eager to enhance collaboration with biopharmaceutical enterprises in Guangzhou.

IDG Capital

Over the past two decades, IDG Capital has invested approximately RMB 20 billion in Guangdong Province, covering all sectors including biopharmaceuticals and TMT, with around RMB 5 billion allocated to Guangzhou. Currently, IDG Capital is seeking to strengthen its presence in the Greater Bay Area, deepen cooperation with the Guangzhou Municipal Government, and gradually shift its investment hub to South China or the Greater Bay Area.

Mr. Zhang Jianbin, Partner at IDG Capital, stated that he personally views the Greater Bay Area as a historic opportunity, offering excellent prospects for investment and entrepreneurship in China, particularly in South China, and that IDG Capital places significant emphasis on this opportunity.

Yunfeng Capital

Over the past three years, the pharmaceutical industry has become a key investment focus for Yunfeng Capital. In the last 12 months, Yunfeng Capital’s funds have begun shifting from the IT, finance, and TMT sectors to the pharmaceutical sector.

GTJA Group

Completed Investments: Mindray, Akeso (Zhongshan), Huayin Medical (Guangzhou), etc.

Headquartered in Shenzhen, GTJA Investment Group has long maintained a strong focus on the healthcare sector. Specializing in healthcare has become a defining hallmark of GTJA. Beyond providing capital, GTJA is committed to supporting industry growth with greater concentration and focus by leveraging its comprehensive resource capabilities.

Ms. Teng Yuhang, Executive Partner at GTJA Investment Group, believes that the pharmaceutical industry in the Greater Bay Area has historically been dominated by more mature enterprises, primarily concentrated in relatively traditional sectors such as traditional Chinese medicine (TCM), proprietary Chinese medicines, and active pharmaceutical ingredients (APIs). Although the innovative drug sector has seen significant momentum and rapid growth, its scale and volume remain in the early stages. “The bubble that previously existed in the biopharmaceutical field still persists, and we are currently in a process of returning to rationality. The past model of blind investment and cash burn will continue to change in the future.” Ms. Teng’s assessment of the investment stage aligns with that of Mr. Yuan Quanhong.

SCGC

Completed Investments: Chipscreen Biosciences, Mindray, Akeso

SCGC is a comprehensive investment institution, with biopharmaceuticals being one of the seven key sectors it focuses on. Last year, SCGC established a dedicated biopharmaceutical fund. As the most active investment firm in the Greater Bay Area, Mr. Cao Xuguang, Executive General Manager of SCGC, stated that the rollout of the Greater Bay Area development plan presents a significant historical opportunity. Truly high-quality enterprises will have no difficulty raising capital in the Greater Bay Area.

Leveraging data structures to analyze industries is VCBeat’s standard approach. In this section, we will provide a brief quantitative characterization of this attractive market segment based on biomedical investment and financing data from the Greater Bay Area over the past decade (2009–2018). Meanwhile, we will compare the biomedical industry in the Greater Bay Area with that in the Yangtze River Delta urban agglomeration to identify differences and opportunities.

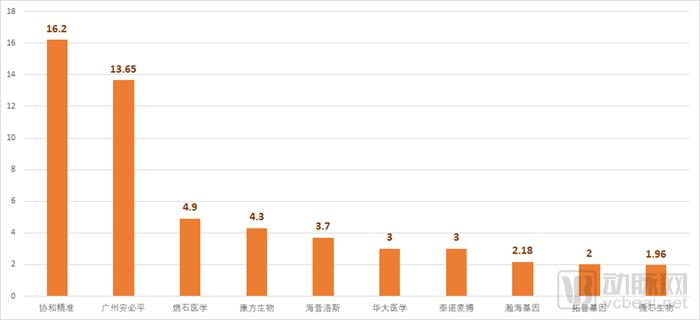

An Introduction to the Biopharmaceutical Industry in the Greater Bay Area: Starting with the Financing Performance of Private Companies, We Identified the Top 10 Most Fund-Attractive Enterprises Over the Past Decade—Union Precision Medicine, Guangzhou LBP Medicine Science, Burning Rock Biotech, Akeso, Halomics, BGI Genomics (BGI), Tnuomab, Hanhai Gene, TopGene, and Chipscreen Biosciences. Companies specializing in genetic testing and molecular diagnostics account for half of this list.

Figure 1. Top 10 Companies in the Greater Bay Area by Private Financing Volume, 2009–2018

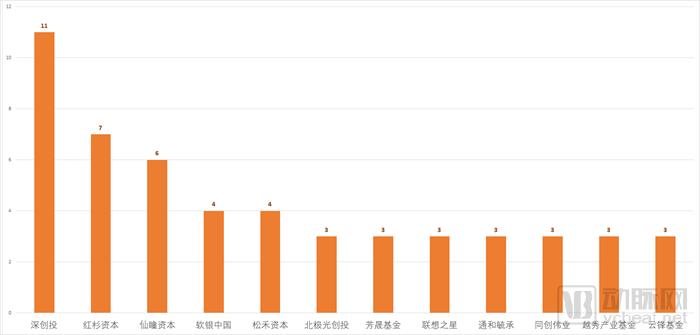

In the ranking based on the number of investment deals, SCGC ranked first with a total of 11 investments completed. Notably, although leading firms have been eyeing biomedical investment opportunities in the Greater Bay Area, as discussed in the previous section, few institutions have actually made moves over the past six years. Among the top investment firms previously featured in VCBeat New Medicine’s “Report on Global New Medicine Investment and Financing Data from 2014 to 2018: Approaching the Harvest Period,” only SCGC, Sequoia Capital, Legend Star, and Northern Light Venture Capital appeared in Figure 2.

SCGC is a state-backed investment institution native to the Greater Bay Area (GBA), and supporting local economic development is its inherent responsibility. From this perspective, it can be interpreted that despite the GBA’s high degree of marketization, it has not yet formed a biomedical industry ecosystem capable of strongly attracting social capital. Social capital, particularly in vertical sectors, has been hesitant in previous investment decisions. However, SCGC has not yet established an absolute advantage in the GBA, where the investment landscape remains highly fragmented.

Furthermore, we examined mergers and acquisitions (M&A) in the Greater Bay Area’s biopharmaceutical industry over the past six years. The VCBeat database recorded only four M&A transactions between biopharmaceutical companies within the Greater Bay Area. While this data may be incomplete, it nonetheless supports the view that commercial interactions among biopharmaceutical enterprises in the region are not active.

Figure 2 Active Investment Institutions in the Greater Bay Area, 2009–2018

We further examine the number and volume of financing and investment activities among biopharmaceutical enterprises in the Greater Bay Area. Despite two downturns in 2011 and 2016, the overall trend has been upward, with the absolute number of deals remaining at around 20 per year over the past five years—equating to more than 1.5 biopharmaceutical financing events per month. Notably, since the concept of the Guangdong-Hong Kong-Macao Greater Bay Area was first included in the State Council’s Government Work Report in 2017, both the volume and value of biopharmaceutical investments and financing in the region have shown significant simultaneous growth. This concurrent rise in deal count and amount strongly validates investors’ assertions regarding the historical opportunities presented by the Greater Bay Area.

However, when comparing the Greater Bay Area’s financing performance over the past decade with that of the Yangtze River Delta urban agglomeration, the gap becomes clearly evident. The latter has been on a steady upward trajectory since 2011 and has maintained an approximately five-fold lead over the Greater Bay Area in both deal volume and value over the past five years.

Figure 3. Number and Amount of Biopharmaceutical Financing Deals in the Greater Bay Area and the Yangtze River Delta, 2009–2018

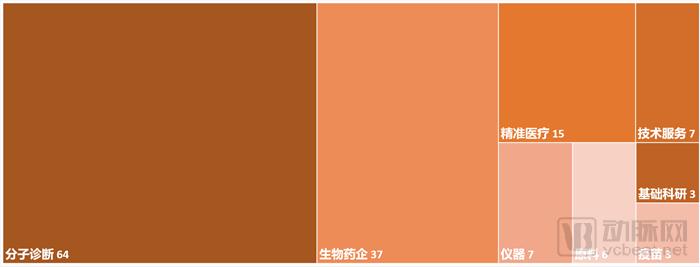

We conclude our analysis by examining the high-growth sectors within the Greater Bay Area’s (GBA) biopharmaceutical industry. Genetic testing has long been a traditional strength of the GBA’s biopharmaceutical sector, giving rise to molecular diagnostics, which has emerged as the most dynamic segment over the past decade. With the advancement of precision medicine and personalized treatment, market demand for companion diagnostics is gradually being unleashed. As the predominant technology in companion diagnostics, molecular diagnostics boasts a substantial market size.

Figure 4 Distribution of Sub-sectors in the Greater Bay Area, 2009–2018

Through data analysis, we believe that the biomedical industry ecosystem in the Greater Bay Area is beginning to exhibit mature trends characterized by diverse sectors and a rich variety of market participants, while urban cluster development planning will accelerate this trend. Leveraging the technological and talent advantages accumulated from its early lead in genetic testing, the Greater Bay Area is gradually forming a differentiated industrial structure centered on molecular diagnostics. As the market remains highly fragmented, capital investors are presented with favorable opportunities for market entry.