Understanding the Health Insurance TPA Sector: From Outsourced Service Provider to Innovation Driver

Previously, VCBeat conducted a systematic analysis of the innovative health insurance sector. (See:In-Depth Analysis of Innovation in the Health Insurance Sector: Unicorns to Emerge from These Key Directions) In this article, we have reviewed innovative health insurance companies, internet insurance channels/platforms, third-party service providers, and medical insurance payment innovation companies, outlining the general landscape of business model innovation in the health insurance sector.

To further “decipher” the innovative landscape of health insurance, we will continue to provide in-depth analyses of specific conditions across various sub-sectors. This article focuses on Third-Party Administrators (TPAs) in health insurance, discussing their traditional business models, the evolution of innovation pathways, and their role in promoting the development of health insurance.

Why We Chose the TPA Sector for the First In-Depth AnalysisThere are several reasons behind this choice. First, the health insurance TPA (Third-Party Administrator) business is relatively mature, with well-established product and service models as well as proven corporate case studies. Second, the health insurance TPA sector is still evolving, offering new insights into both its operational scope and business models. Third, as the scale of health insurance expands, TPAs will be among the first to reap the benefits, providing valuable guidance for venture capital investors in identifying strategic investment directions.

As per our convention, the overview of the full text is as follows:

TPA Business Overview: The “dirty work” and “arduous tasks” outsourced by health insurance companies;

Overview of Leading TPA Companies: How MSH, Shangbaotong, and Others Are Developing;

Synergy between insurance and services: transitioning from expense reimbursement to managed care;

From TPA to Full-Process Innovation: Capturing the Dividends of the Trillion-Yuan Blue Ocean in the Health Insurance Market.

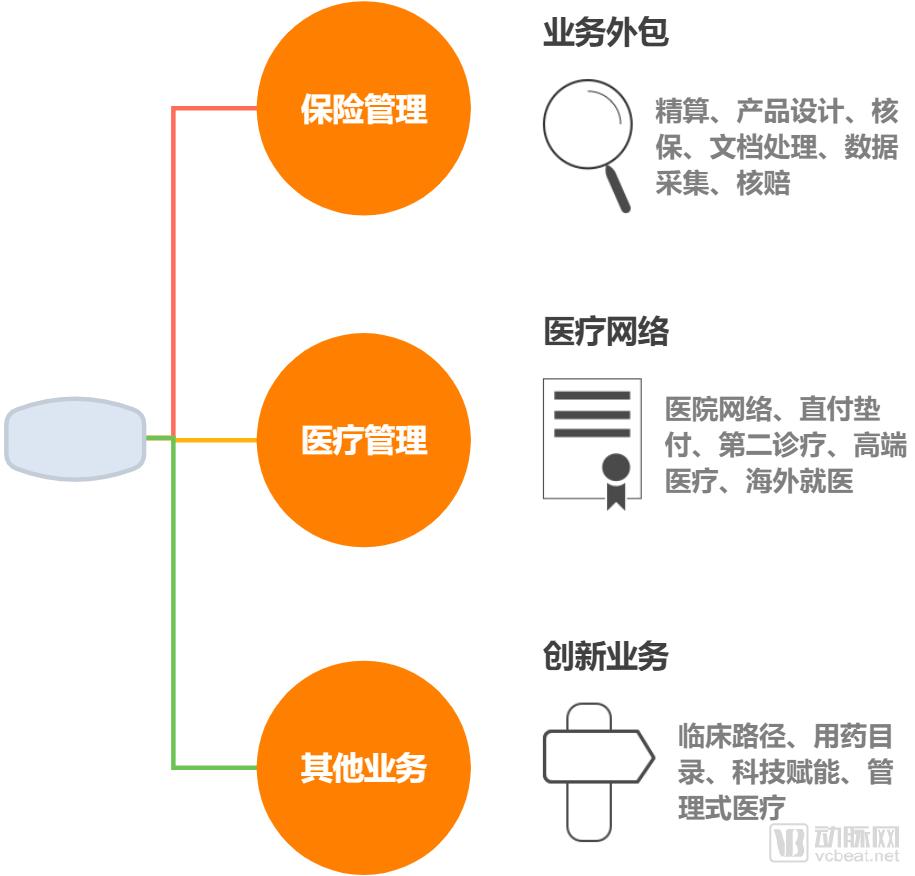

According to the general definition, third-party service providers in the health insurance industry are commonly referred to as TPAs, an acronym for Third Party Administrator for Group Medical Insurance, denoting companies that provide third-party administration services for medical insurance. Within the medical insurance sector, these entities offer third-party management services to health insurers or insurance companies specializing in medical insurance, particularly medical expense coverage. Their services encompass new policy issuance and policy maintenance, claims processing, customer service, establishment of healthcare provider networks, and coordination of medical expense settlement.

Gu Bing, General Manager of Beijing Financial Street Insurance Brokers Co., Ltd., has over thirty years of experience in the insurance industry. He told VCBeat that traditional TPA (Third-Party Administrator) services essentially handle the “dirty” and “tedious” tasks outsourced by health insurers. Their primary functions include processing receipt-based reimbursements, data governance, cost containment management, and providing treatment and claims settlement recommendations to insurers within the limits of coverage amounts.

Figure 1: Core Functions of Health Insurance TPA Companies

Source: Compiled from public information, VCBeat

In the traditional operation of health insurance, issues such as information asymmetry, low specialization, high loss ratios, and weak profitability are prevalent. As an independent third party involved in health insurance operations, Third-Party Administrators (TPAs) can effectively address these challenges. For health insurance companies, TPAs assist in collecting and processing information during underwriting and claims adjudication, thereby enhancing risk management capabilities. For policyholders, TPAs help them better understand insurance terms, rights, and obligations, and ensure that application and claims documentation is completed truthfully and objectively, thus reducing instances of misrepresentation, concealment, and insurance fraud.

Gu Bing pointed out that, because the clients of Third-Party Administrators (TPAs) are insurance companies and large commercial enterprises rather than individual policyholders, TPAs’ interests are aligned with those of insurers, aiming to enhance operational efficiency and reduce costs. Although optimizing medical services can improve the healthcare experience of insured individuals, it incurs additional costs. In a market characterized by homogeneous insurance products and price wars, the development of medical service networks, high-end medical services, and health management services serves more as an added benefit. This requires insured individuals to cultivate the awareness of paying for premium services.

In terms of TPA company classification, Jiang Guanjun, Partner and Actuarial Consultant at Milliman, told VCBeat that TPA companies can be categorized by their service recipients into three main types: those serving payers (including public health insurance, commercial insurance, and individuals), those serving healthcare providers, and those focused on enhancing individual patient experience.

Currently, most TPA companies serve payers, as they can facilitate direct payments and have established profit models. Their core business areas still include product development, risk control, healthcare service networks, claims enablement, patient services, and chronic disease management. For instance, they develop insurance products for diabetic patients, digitize diagnostic medical records, and implement prescription recognition. In terms of patient needs, services include medical guidance, appointment scheduling, and consultations.

“Segmenting different population groups to offer tailored products, such as insurance for patients with pre-existing diabetes and surgical coverage for complications; chronic disease management and medication adherence are also part of TPA companies’ services. Foreign companies excel in this area—for instance, some U.S.-based TPAs have found that many patients fail to complete their treatment plans on time due to transportation issues and thus arrange transportation services for them, whereas domestic companies in China have not yet achieved such a detailed level of service,” said Jiang Guanjun.

Domestic TPA services remain at a relatively nascent stage, which is closely tied to the modest scale of the health insurance industry itself. According to data from the World Health Organization (WHO), social medical insurance currently accounts for over 60% of China’s total healthcare expenditure, out-of-pocket payments represent approximately 35%, and commercial insurance covers less than 5%. Although the health insurance market has expanded rapidly in recent years, there remains substantial room for growth in both industry scale and influence when compared to the social medical insurance network, which covers more than 95% of the population.

“Overall, the development of the health insurance TPA business in China has not been particularly robust, and there remains a certain gap compared to the mature market in the United States. Large commercial health insurers in the U.S. have dedicated medical management teams, which can be understood as internal TPAs, while external TPAs have also developed well, operating both independently and in an integrated manner. From the perspectives of product innovation and proactive health management, domestic TPAs still have room for improvement,” said Wang Guangying, Executive Partner at Puxin Health Technology Company.

As previously mentioned, the emergence of TPA (Third-Party Administrator) service companies stems from the “pain points” in the health insurance industry. First, life insurance companies currently dominate the domestic health insurance market, with critical illness insurance accounting for a significant share of their product portfolio. Although medical insurance has been growing rapidly, its relative scale remains small; consequently, medical insurance teams hold limited influence within insurance companies.

In such circumstances, life insurance companies prioritize internal resource allocation and do not deploy large-scale medical operations teams, thereby preventing specialized operational capabilities. Furthermore, since health insurance accounts for a relatively small proportion of total social healthcare expenditure, insurers lack sufficient leverage over healthcare providers. This hinders commercial insurance companies from establishing high-quality medical service networks and implementing effective control and intervention measures for healthcare costs.

This has created fertile ground for the emergence and development of third-party service providers. For health insurance companies, the significance of these third-party services lies in business unbundling and outsourcing. Examples include IT system planning and implementation (the most foundational component); market research, data support, product and channel management, and customer relationship maintenance during the insurance product design phase; underwriting and claims adjudication (the “two-core” operations); establishment of medical service networks and fast-track/direct claims payment systems; as well as handling daily health consultation inquiries and providing health management services.

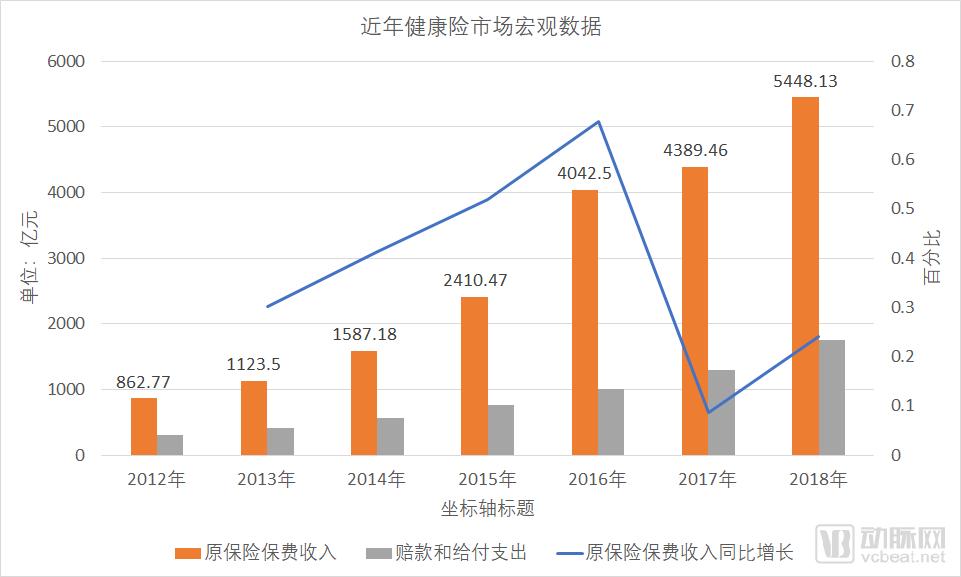

In the field of third-party administration (TPA) for health insurance, domestic companies in China have largely emerged since 2012, a trend closely linked to changes in the overall scale of the health insurance industry. According to data from the China Banking and Insurance Regulatory Commission (CBIRC), the gross written premiums for domestic health insurance business amounted to only RMB 86.277 billion in 2012. From 2013 to 2018, the compound annual growth rate (CAGR) of the health insurance market reached 35.95%. In 2018, gross written premiums for health insurance business totaled RMB 544.813 billion, representing a year-on-year increase of 24.12%, while claims and benefits paid out reached RMB 174.434 billion, up 34.72% year on year. Only in a rapidly expanding market do substantial opportunities for innovation arise.

Table 2: Macroeconomic Data of the Health Insurance Market

Below are some companies in China that offer health insurance TPA services.

Table 1: Overview of Domestic Health Insurance TPA Companies

Data source: VCBeat Knowledge Base

Data source: VCBeat Knowledge Base

TPA Company Case: MSH

MSH China was established in 2001 and is the largest third-party administrator (TPA) in China’s high-end health insurance sector. Headquartered in Shanghai, it operates a Beijing branch, a Guangdong branch, and service representative offices in Suzhou, Dalian, Shenzhen, Wuhan, and Chengdu. Its core business is providing comprehensive TPA services for high-end health insurance to insurance companies. MSH China also serves as the Asia-Pacific headquarters of MSH International, the world’s largest TPA provider.

MSH International is a subsidiary of the French Siaci Saint Honoré (S2H) Group, one of Europe’s leading insurance brokerage and consulting service providers. It appears less frequently in Chinese-language search results. Available news reports indicate that in January 2018, HNA Capital and the French S2H Group planned to strengthen cooperation in multiple areas—including the establishment of a joint-venture international insurance brokerage firm, equity investments, and development of major projects—with the overarching goal of providing comprehensive services to enterprises involved in the Belt and Road Initiative and fully supporting Chinese companies in their global expansion.

Table 2: Wanxinhe’s Main Businesses

Source: Wanxinhe Official Website, VCBeat

Figure 2: Introduction Page of Wanxinhe's Overseas Medical Treatment Insurance for Critical Illnesses

Sources: Public information, VCBeat

Of course, as a provider of high-end medical insurance services, MSH China’s premiums are also substantial, with base product quotes starting at RMB 20,000 per year and reaching up to approximately RMB 200,000 per year.

Figure 3: Wanxinhe Product Quotation

Source: Public information, VCBeat

Wanxinhe also maintains a domestic healthcare service network, including the International Medical Center of Huashan Hospital Affiliated to Fudan University in Shanghai, the Special Diagnosis Department of Shanghai Children’s Hospital, the Special Needs Department of East China Hospital Affiliated to Fudan University, Peking University Health Management Center, and the International Medical Department of China-Japan Friendship Hospital.

Wanxinhe’s business model is a typical example of a medical insurance TPA, focusing on the construction of a healthcare service network. This serves as an attractive value-added service for customers with demands for high-end medical care and can even be marketed as a “selling point” for medical insurance products.

TPA Company Case: Shangbaotong

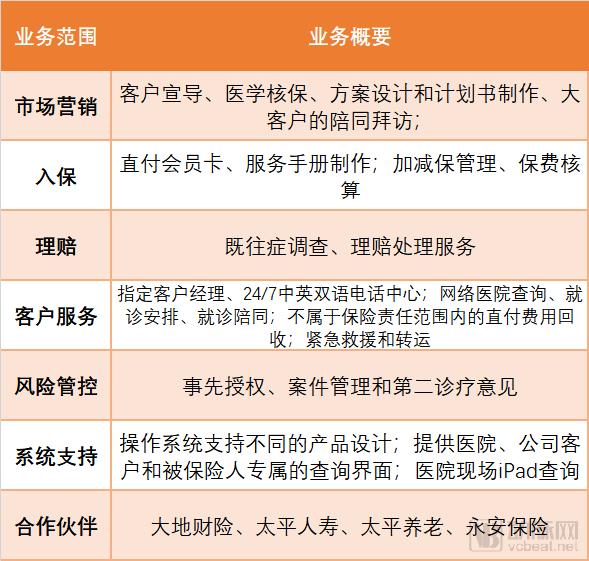

Shangbao Tong is a third-party management service provider under the Shenci Group, specializing in providing direct billing health services to corporate clients and insurance companies. Established in 2005, with its headquarters and operational center in Shanghai, it has dedicated service personnel in Beijing, Guangzhou, Shenzhen, and Jiangsu. Domestically, it boasts a premium direct-billing medical network encompassing over 300 hospitals, while internationally, it partners with more than 10,000 healthcare service providers. Its successfully operated claims service centers and call centers have garnered widespread acclaim within the industry.

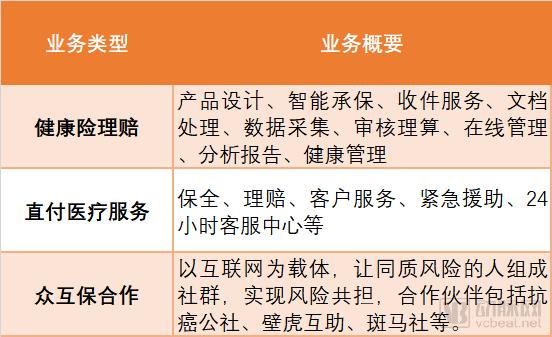

Shangbaotong’s services are primarily divided into three categories: health insurance claims processing, direct-billing medical services, and collaborative mutual insurance partnerships.

Table 3: Main Services of Shangbaotong

Source: Shangbaotong

Ms. Xia Tingying, founder of Shangbaotong, joined AIA Insurance in 1997 and served for eight years. In 2005, she embarked on her entrepreneurial journey, establishing multiple companies specializing in insurance brokerage, insurance loss adjusting, health management, and premium medical healthcare services, which were later integrated into Shangbaotong Health Technology. She completed the EMBA Program (Class 28) at Cheung Kong Graduate School of Business in 2017.

In terms of capital, although Shangbaotong has not publicly disclosed its financing information, records of changes in industrial and commercial registration show that Shanghai Shijian Yeyi Investment Partnership (Limited Partnership) was added as a shareholder in June 2015, currently holding a 20% equity stake. The shareholder background of Shijian Yeyi is Shanghai Industrial Holdings, a large state-owned enterprise group.

Shangbaotong’s health insurance claims management and medical service network business enjoys a strong reputation in the industry, with numerous positive endorsements from industry insiders. Its key advantages include a comprehensive database accumulated over many years, an intelligent underwriting and adjudication system, and risk control experience models.

TPA Company Case: Yi Yong Health

Founded in 2013, Yiyong Health is a company specializing in health insurance services, leveraging its industry-leading automated claims adjudication system and data analytics capabilities. Entering the market as a third-party service provider, Yiyong Health helps insurers achieve precise cost control and product innovation on one hand, while connecting with high-quality hospitals on the other to deepen medical services. This service-driven approach effectively bridges the needs of users, hospitals, and insurance companies.

In August 2018, Yi Yong Health announced the completion of its RMB 50 million Series A1 financing round, led by Aixiang Capital, with existing investors Yuanjing Capital and Haier Capital continuing to participate. Concurrent reports indicated that Yi Yong Health’s next round of financing was also underway.

Concurrently with the announcement of its Series A1 financing, Yi Yong Health launched a provincial-level commercial insurance settlement platform in Henan Province. Patients can be admitted to hospitals connected to this direct billing platform without paying a deposit. Upon discharge, the medical insurance and commercial insurance adjudication systems operate in sync, allowing patients to settle only the out-of-pocket expenses not covered by either insurance scheme before leaving the hospital.

Yi Yong Health will also provide DRG (Diagnosis-Related Groups) and medical record quality control services to hospitals in Henan Province, helping them enhance management capabilities and the quality of electronic medical record data. Meanwhile, it will assist residents in establishing internet-based health records, integrate pharmacy data chains, and incorporate the informatization of primary healthcare institutions into the overall platform.

Summary

Case studies of companies such as Wanxinhe, Shangbaotong, and Yiyong Health help illustrate the specific business operations of domestic health insurance TPA (Third-Party Administrator) companies. It is evident that their core business remains divided into two main segments: health insurance services and medical services. Health insurance services primarily focus on underwriting and claims adjudication (“two-core” functions) as well as risk control. Medical services mainly involve the establishment of healthcare provider networks, including green channels for medical access, expert consultations, and second medical opinions.

In terms of business models, Third-Party Administrator (TPA) companies serve health insurance providers, offering either bundled payment arrangements or fee-for-service pricing. Overall, the third-party services sector for health insurance is relatively mature, yet the market size still holds significant room for growth.

In the traditional service model, health insurers act as “payers” rather than “order-placers,” limited to retrospective reimbursement and unable to establish deep integration with healthcare providers, pharmaceutical suppliers, and health management organizations. This significantly constrains their ability to oversee the healthcare delivery process and implement effective cost containment.

In countries with well-developed private health insurance markets, such as those in Europe and the United States, there are numerous examples of close collaboration between health insurers and healthcare providers. Prominent examples include the renowned Kaiser Permanente and various Preferred Provider Organizations (PPOs). Recent landmark cases of cross-segment integration within the health insurance industry chain include CVS’s acquisition of Aetna and Cigna’s acquisition of Express Scripts.

According to the EY China Health Insurance White Paper, insurance companies, acting as payers, are proactively initiating integration with hospitals, pharmaceutical companies, and health service providers to achieve rational cost control, enhance customer stickiness, accumulate health data, and enable differentiated pricing. These integration models can be categorized into four types: strategic cooperation, capital operations, self-built systems, and service procurement.

It is already an industry consensus that both industrial synergy and capital synergy are required. An industry report released by the Insurance Association of China points out that the greatest challenge facing the development of commercial health insurance in China is the lack of a cooperative mechanism with healthcare service providers featuring risk sharing, balanced interests, and information sharing. To improve this situation, efforts should focus on refining the operational system design for critical illness insurance, promoting the participation of commercial health insurance in the supply-side reform of medical services, and establishing a legal framework for health data.

Health insurance should not be limited to coverage alone; instead, it should provide comprehensive protection grounded in health. Establishing an ecosystem that integrates “insurance + healthcare + health management” not only enhances the insurance experience for policyholders but also maximizes the value of health insurance.

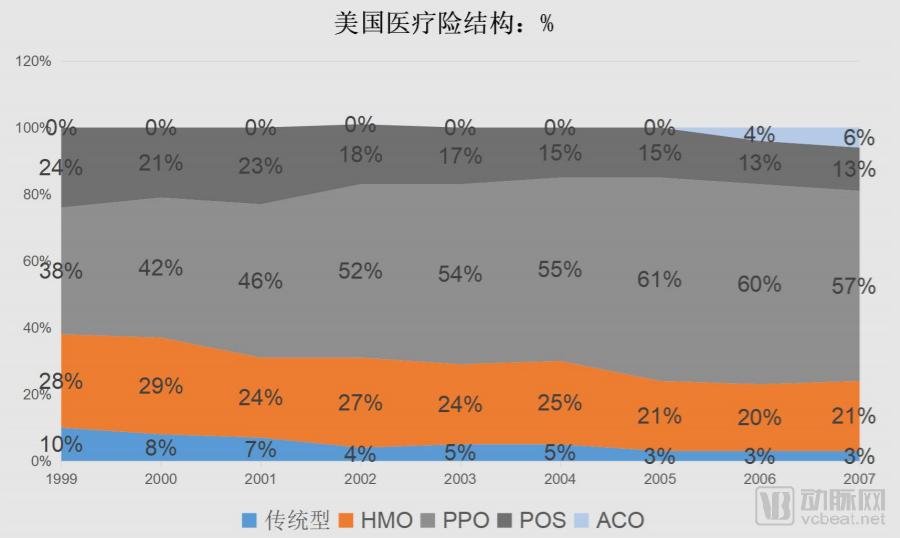

The shift from fee-for-service health insurance to managed care represents one of the most significant trends in the health insurance industry. In the United States, for example, Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs) have rapidly expanded their presence in the commercial health insurance market, now accounting for approximately 80% of the health insurance share.

Figure 4: Changes in the Structure of U.S. Health Insurance

Data Source: Sullivan & Cormwell, Gaotejia Insurance Industry Research Report

Health Maintenance Organizations (HMOs) are health insurance entities that tightly integrate insurers with healthcare providers, merging third-party payers and service suppliers into a unified system. With aligned interests, healthcare providers are incentivized to proactively control medical costs. According to a research report by Ping An Securities, HMOs offer six major advantages: innovative payment models, comprehensive review of the entire healthcare service process, careful selection of high-quality healthcare providers, emphasis on disease prevention, robust information management systems, and strict referral protocols.

Figure 5: Advantages of the HMO Model

Source: Ping An Securities

Preferred Provider Organization (PPO) insurance is a voluntary insurance plan that falls between Fee-for-Service insurance and Health Maintenance Organizations (HMOs). PPO insurers negotiate discounted rates for medical services with doctors and hospitals, thereby enabling them to offer more affordable health insurance coverage to their members.

Whether HMO or PPO, both emphasize the synergy between insurance and healthcare services. Their core logic is to transform insurers and healthcare providers into a community of shared interests, featuring cost-sharing and benefit-sharing. By intervening in the behavior of the insured, they promote healthy lifestyles and treatment adherence, thereby reducing disease risk and controlling medical costs.

This model has been validated in European and American markets, proving its effectiveness, and is currently being piloted in the Chinese market. For instance, WeDoctor and Ping An Good Doctor are adopting this approach: WeDoctor, as an internet healthcare service provider, collaborates with insurance companies, while Ping An Good Doctor primarily serves the health insurance customers of the Ping An Group. The synergy between insurance and healthcare will be the key focus for third-party administrators (TPAs) in the next phase of health insurance development.

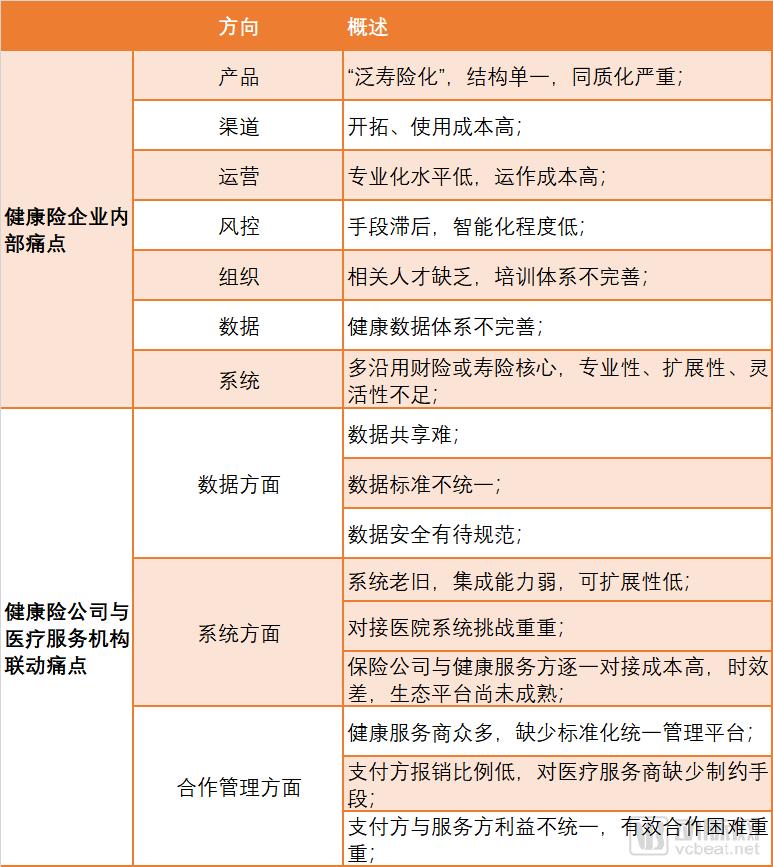

In the health insurance market, beyond medical services, there are numerous operational pain points. These pain points also represent key opportunities for innovation. In addition to Third-Party Administrators (TPAs), it is worth focusing on innovations that cover the entire process and full life cycle of the health insurance service chain.

Table 4: Operational Pain Points in the Health Insurance Industry

Source: EY China Commercial Health Insurance White Paper

Based on research into societal and customer needs, analysis of the current ecosystem landscape, and a summary of operational pain points, EY China believes that the future development trends of health insurance can be summarized in four key phrases: customer-centricity, professional operations, ecosystem collaboration, and regulatory compliance.

Specifically, health insurance will gradually shift toward a family-based service closed loop centered on meeting the medical needs of individual customers. Operations will move away from traditional property and life insurance business models, transitioning toward ecosystem-driven, specialized, and intelligent management. Efficient collaboration between payers and providers is key to facilitating the formation of this health insurance service closed loop.

Integrating commercial health insurance with government medical insurance programs in a manner tailored to local conditions is key to achieving mutual benefits and win-win outcomes. Actively cooperating with various government departments to participate in healthcare system reform serves as a critical entry point for deepening engagement as a service provider. Furthermore, technology is a focal point for innovating operations within the health insurance industry; representative technologies include cloud computing, big data, the Internet of Things (IoT), mobile internet, artificial intelligence (AI), social networks, and blockchain.

Below are innovative cases in other service models and technologies within the health insurance innovation sector.

Industry Case: Medbanks Health

Magi Health is a healthcare payment innovation company founded in 2017. As a leader in the healthcare payment innovation sector, Magi focuses on the patient side and is committed to addressing issues of healthcare affordability and accessibility through innovative insurance and financial models, ensuring that patients can both “afford” and “access” high-quality medicines and medical services.

To help patients access medications at lower costs and with greater convenience, Magnesium Trust delivers services along three core pillars: New Payment, New Retail, and New Services. “New Payment” focuses on promoting value-based medication adherence by providing corresponding pharmaceutical solutions, such as medical financing, efficacy insurance, pharmaceutical benefits, and continuous incentive programs. “New Retail” encompasses both in-store pickup at offline Direct-to-Patient (DTP) pharmacies and home delivery via cloud pharmacies. “New Services” revolves around the patient’s medication journey, offering a range of value-added services to enhance the patient experience.

In terms of insurance innovation, Medbanks has collaborated closely with dozens of leading domestic commercial health insurance direct insurers and reinsurers to develop the “Meixin Anxin Drug Coverage Plan,” a specialty oncology drug insurance product designed for healthy individuals. This plan marks the first time that newly launched specialty drugs purchased outside hospitals have been included in coverage responsibilities, providing more comprehensive protection and enhanced pharmaceutical services to millions of people.

In the realm of out-of-pocket payments for patients, Magnesium Health has partnered with the top 20 foreign pharmaceutical companies operating in China as well as domestic innovative drug manufacturers to customize innovative payment solutions for many of their blockbuster products. Its Yaokangfu platform has provided innovative drug payment services to over 100,000 patients, cumulatively saving them more than RMB 100 million in medication costs, and has offered diverse drug benefit programs—including interest-free installment plans and efficacy insurance—to tens of thousands of patients.

The hallmark of Magent’s business model lies in its entry into the existing ecosystem as a “value creator,” establishing a multi-win framework with key stakeholders. On the patient side, it aggregates substantial demand to achieve the effects of “centralized procurement,” thereby securing greater payment benefits for patients. For pharmaceutical companies, it offers a new model that returns to “value” and enhances accessibility at scale, driving incremental business growth and further laying the groundwork for “value-oriented” national reimbursement drug list (NRDL) negotiations, thus shortening the time between new drug launch and NRDL inclusion. For pharmacies, Magent empowers them through its IT infrastructure and patient management capabilities, comprehensively enhancing service quality and providing diversified patient solutions. For partner insurance or financial institutions, it provides reliable and credible patient data, forming the foundation for product development, pricing, operations, and iteration, thereby optimizing the industry’s value chain as a whole.

Industry Case: Haorensheng Technology

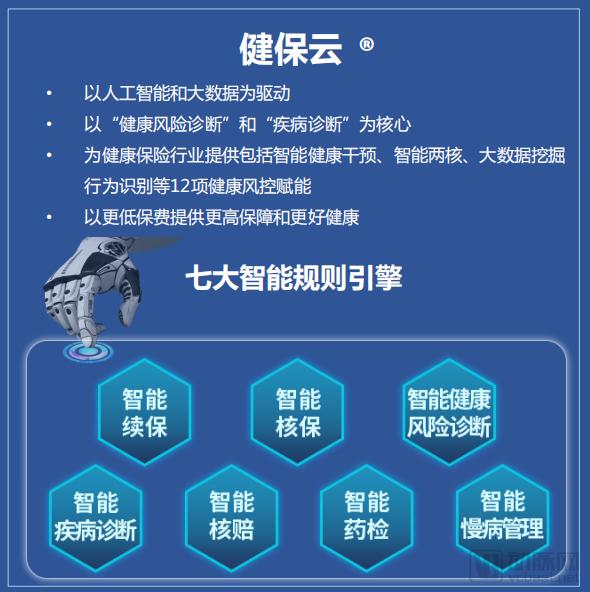

Haorensheng Technology, a subsidiary of the Haorensheng Group, leverages over a decade of R&D and service expertise in the health insurance and health management sectors. As a third-party enterprise specializing in health insurance risk control, Haorensheng Technology has integrated its experiential and technological advantages to launch “Jianbaoyun,” an AI-driven health insurance risk control platform that has become a more efficient verification tool for insurance companies.

Currently, driven by artificial intelligence and big data, and centered on “health risk assessment” and “disease diagnosis,” “Jianbao Cloud” provides the health insurance industry with modular deployment featuring four core technologies—including intelligent health intervention, intelligent underwriting and claims processing (the “two cores”), and big data-driven behavioral recognition—six intelligent rule engines, and twelve health risk control empowerment modules. Meanwhile, it continuously and efficiently iterates and optimizes the system while progressively integrating substantial industry big data from healthcare, insurance rules, and health risk management practices.

Figure 6: Haorensheng “Jianbao Cloud” System

Source: Hao Ren Sheng

Ms. Zhang Zhiyun, Founder and CEO of Hao Ren Sheng Technology, told VCBeat that Hao Ren Sheng provides risk management services to health insurance companies and policyholders throughout the pre-underwriting, underwriting, and post-underwriting stages. By empowering the health insurance industry with technology, the company aims to drive its digital and intelligent transformation.

For instance, in intelligent underwriting, the traditional process relies on questionnaires and disclosure forms, which are then processed by an underwriting engine. However, this conventional model presents a dilemma: overly cumbersome questionnaires can discourage applicants, leading to customer churn; conversely, incomplete collection of applicant information results in insufficient risk awareness and makes risk control difficult.

The solution proposed by Haorensheng is the “three-tier questionnaire” model, in which questionnaires are differentiated and more detailed inquiries are triggered only based on specific answers. This approach not only enhances the accuracy of pre-underwriting information collection and effectively identifies risks, but also improves the customer experience.

Secondly, during the claims adjudication phase, medical documents are processed using OCR and NLP technologies, leveraging artificial intelligence for data organization to enhance the accuracy and efficiency of data entry. The Haorensheng system enables data integration with hospitals and medical insurance systems, employing technical means to identify fraudulent invoices and insurance fraud while ensuring data privacy, thereby assessing the reasonableness of claims.

Another commendable asset is Hao Rensheng’s knowledge graph. In 2013, the Mayo Clinic made a strategic direct investment in Hao Rensheng Group, contributing its knowledge graphs for disease diagnosis and healthy lifestyles. This knowledge graph consolidates over 150 years of diagnostic experience and data from the Mayo Clinic, laying the foundation for Hao Rensheng’s Health Insurance Cloud artificial intelligence system.

Built upon the core knowledge and logic graphs for evidence-based diagnosis and intelligent underwriting from internationally authoritative institutions, and integrated with big health and medical data, Jianbao Cloud has achieved rapid iteration of its knowledge graph under supervised learning with Class A evidence. This approach avoids the “demon” phenomenon associated with zero-basis unsupervised learning that starts from “garbage data,” positioning it as an industry leader.

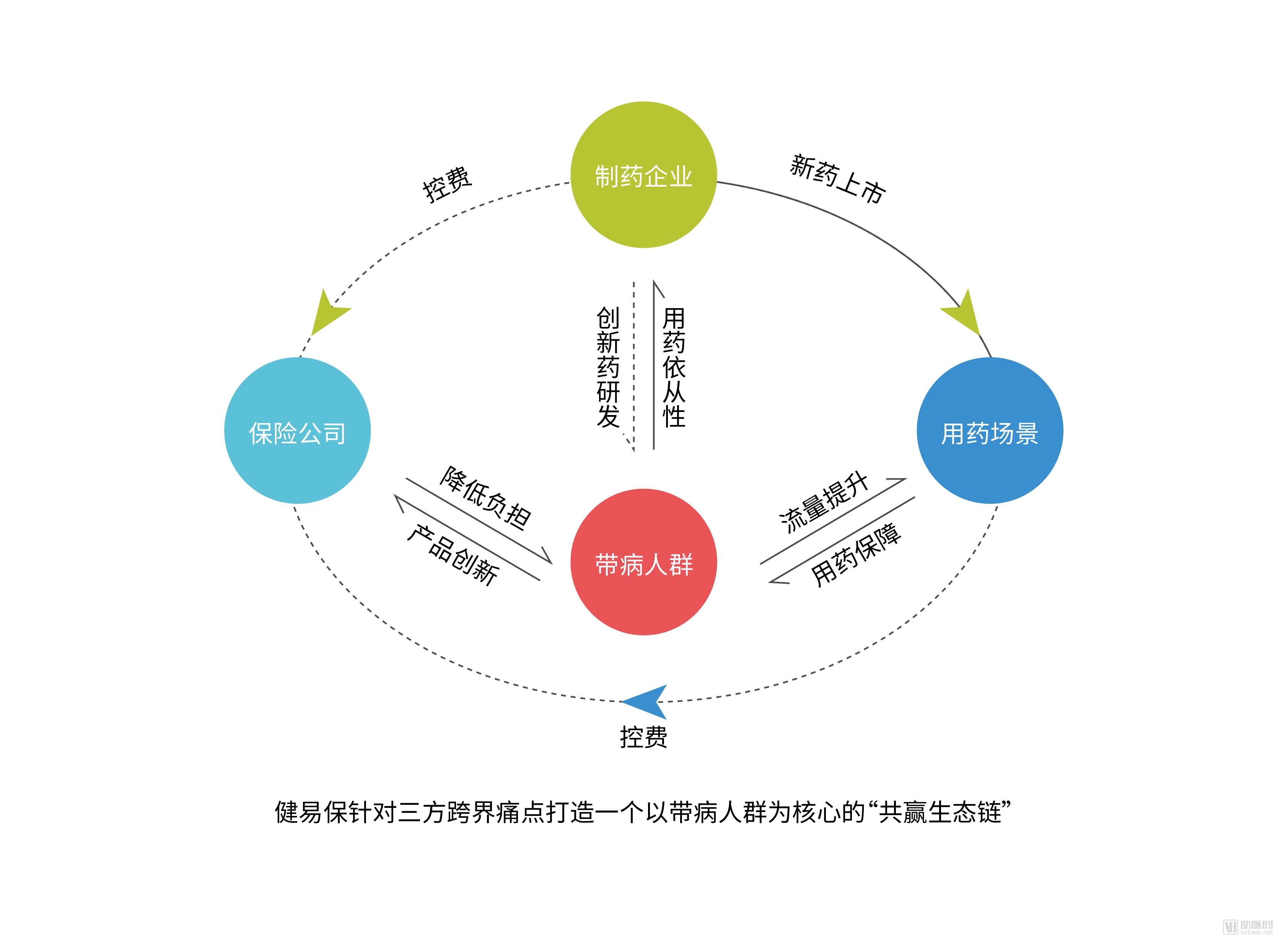

Industry Case: Jianyibao

Beijing Jianyibao, established in 2017, is a next-generation medical insurance solution platform for individuals with pre-existing conditions. By connecting pharmaceutical companies, medication usage scenarios, and financial insurance institutions, Jianyibao develops innovative insurance products to address cross-industry pain points among these three parties, thereby resolving health coverage challenges for individuals with pre-existing conditions and building a comprehensive insurance service platform catering to 450 million such individuals.

As a company whose core founding team hails from the pharmaceutical and insurance industries, Jianyibao deeply understands the “pain points of cross-industry integration.” Since its inception, founder Mr. Zhang Shengming has been committed to building a “win-win ecosystem” centered on individuals with pre-existing conditions, achieving multilateral win-win outcomes for partners while fully safeguarding the tangible interests of this population.

Jian Yi Bao Business Introduction

Source: Jianyibao

Under China’s unique healthcare security system and the current state of commercial insurance, individuals with pre-existing conditions often face significant financial burdens. By collaborating closely with financial and insurance companies to jointly develop insurance products tailored for those with pre-existing conditions, Jianyibao covers medication reimbursement as well as compensation for complications and adverse reactions, thereby alleviating patients’ out-of-pocket medical expenses. As of February 2019, Jianyibao’s “Medication Coverage” program had provided policy coverage for 254,618 individuals, with a cumulative insured amount reaching RMB 344,429,600.

Recently, Jianyibao and Geneseeq Technology jointly announced the launch of China’s first innovative payment insurance plan designed for tumor testing and targeted therapy medications. The inaugural product primarily covers lung cancer and breast cancer, the two most prevalent cancers among men and women, respectively. Looking ahead, the coverage scope of such products is expected to expand further, ultimately encompassing 80% of high-incidence cancers.

For pharmaceutical companies, the lack of suitable and quantifiable methods to effectively reach and influence patients has resulted in medication adherence rates below 40%. By developing insurance products for individuals with pre-existing conditions and conducting online education and outreach, Jianyibao has helped patients cultivate scientific health management concepts, significantly improving their medication adherence.

Meanwhile, Jianyibao leverages its extensive offline medication dispensing network to help pharmaceutical companies secure commercial insurance reimbursement access for new drugs. As of February 2019, Jianyibao had completed data integration with over 20,000 pharmacies across China and registered nearly 50,000 pharmacy staff members. In the future, Jianyibao plans to incorporate community hospitals and internet hospitals into its network.

For chain pharmacies, deep collaboration with Jianyibao helps staff receive training in basic insurance knowledge, providing value-added services to patients and thereby driving traffic growth.

In the future, Jianyibao will continue to exert efforts across multiple fronts. By addressing the pain points of pharmaceutical companies, medical scenarios, and individuals with pre-existing conditions, it aims to establish an insurance product system that covers the vast majority of pharmaceutical enterprises and chronic disease types. This initiative seeks to effectively resolve the critical livelihood issue of “poverty caused or exacerbated by illness” among the broad population living with pre-existing conditions.

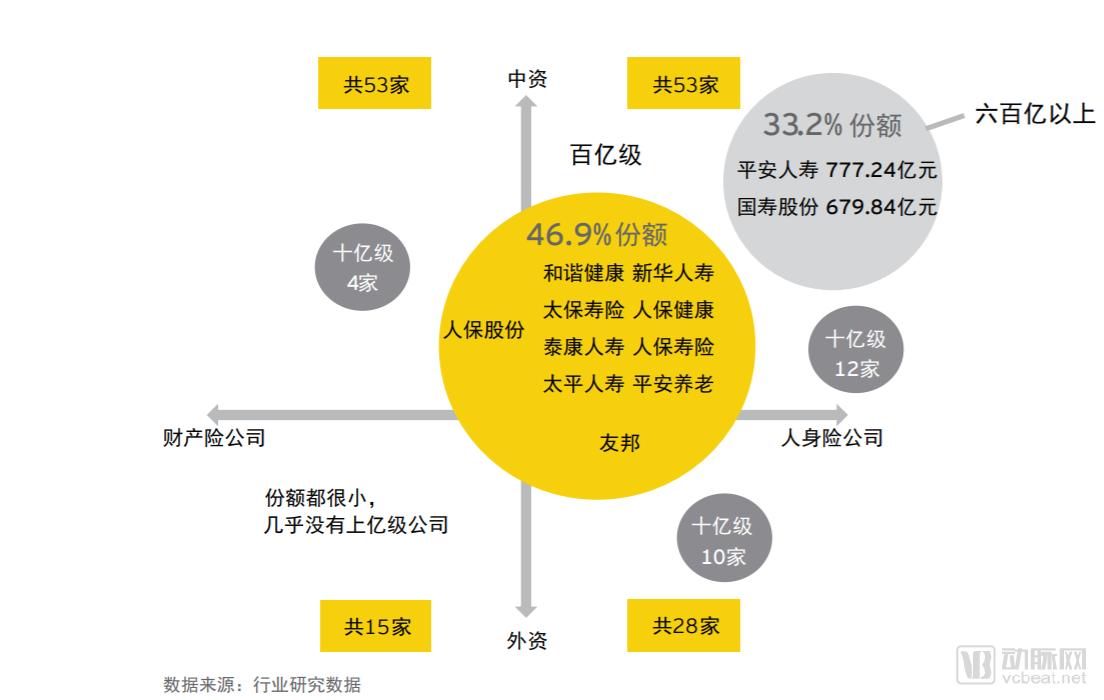

Product homogenization and intense competition are the consensus among industry insiders regarding the health insurance market. The former is reflected in the lack of product differentiation; for insured individuals in different regions and with different lifestyles, the risks of both general diseases and critical illnesses vary, necessitating the provision of differentiated products. The latter is characterized by high market concentration, reliance on agent channels, and insufficient drive for innovation.

Figure 7: Market Concentration in the Health Insurance Sector

Image source: China Health Insurance White Paper

Market data shows that the top two insurance companies have captured approximately one-third of the market share, while the second-tier insurers have secured nearly half. Small enterprises hold insufficient market share to accumulate the resources necessary for product and service model innovation.

Innovation is the key to breaking through. How to innovate? Jiang Guanjun, partner and actuarial consultant at Mingde Actuarial Consulting, told VCBeat that the focus should mainly be on “areas where there is already international validation and similar market demand.”

First, at the technical and data levels, the development and operation of health insurance products rely on data. In the past, medical data was scarce; however, with the support of big data and artificial intelligence technologies, data can now be better acquired and utilized. Furthermore, AI capabilities in image recognition, assisted diagnosis, and risk screening can be integrated with health insurance services.

The second aspect is innovation in business models, such as exploring new insurance scenarios, developing new products, and integrating insurance with medical services. In particular, the latter has seen initial attempts by Ping An Health Insurance and CPIC, demonstrating a certain exemplary effect. While “not economically viable in the short term, it holds long-term value,” this is inevitably the direction for the future. Additionally, practices already implemented overseas could be considered for introduction into the Chinese market.

Certainly, as the operational pressure on medical insurance funds continues to grow and the National Healthcare Security Administration actively promotes reforms in healthcare payment methods—such as Diagnosis-Related Groups (DRGs) or bundled payment models—hospitals themselves face cost-containment imperatives. In this context, hospital services become a cost center, necessitating strategic financial planning. This represents a potential area for innovation that may have been overlooked.