Accenture Report: How AI Empowers Insurance – Three Key Application Scenarios Reshaping the Value Chain

Artificial Intelligence (AI) enables machines to simulate and augment human intelligence, emerging at a time when the insurance industry and other sectors are undergoing digital transformation. Although AI technology is still in its developmental stages, it has already been applied across various industries in the real world. AI is being leveraged to address a wide range of challenges, making interactions between machines and systems smarter and more streamlined.

Insurance companies are also gradually entering this field. Next-generation artificial intelligence technologies are expected to help insurers redefine their operational models, develop innovative products and services, and enhance customer experience. Meanwhile, the adoption of new technologies in this traditional industry continues to face multifaceted challenges.

Whether it is replacing repetitive manual tasks with intelligent automation, empowering employees to enhance their decision-making capabilities and improve customer interactions, or designing smart products, technology will drive the development of insurance companies and help them achieve sustained profitability. VCBeat (WeChat ID: vcbeat) has compiled the “AI + Insurance” industry report released by Accenture, with key highlights including:

• Artificial intelligence will help insurance companies reengineer existing processes, design innovative products, and enhance customer experience;

• Insurance companies must adopt appropriate strategies to better manage human resources;

• Insurance companies should transform their existing operational models, including the adoption of Robotic Process Automation (RPA) and intelligent decision support systems;

• Insurers should allow artificial intelligence to creatively leverage data across the entire value chain, uncovering hidden value within all data sets.

“Artificial Intelligence” encompasses a wide range of technologies and capabilities. We can define artificial intelligence as computer systems capable of perceiving, understanding, acting, and learning. In other words, such a system can perceive its surrounding environment, analyze and comprehend the information it receives, take actions based on this understanding, and improve its performance through learning.

By leveraging machine interactions with the environment, humans, and data, this technology enhances the capabilities of both humans and machines, far surpassing what they can achieve when operating independently.

The practical application of artificial intelligence goes a step further, entailing the integration of intelligent technologies with human wisdom across every business process to help enterprises address their most complex challenges, unlock new markets, or create entirely new revenue streams.

If insurance companies focus their application of artificial intelligence on human resources, workflow management, and data management, they will derive the greatest benefits from it.

As insurance companies face immense pressure, the field of artificial intelligence is advancing at a rapid pace. Competition has become exceptionally fierce, with new entrants disrupting existing business models. Influenced by the rapid technological advancements in other industries, consumer expectations of insurance companies are also rising steadily.

Therefore, insurance companies must find new ways to improve operational efficiency, drive product innovation, and enhance the experience for both customers and employees. For instance, why can’t customers track the progress of their insurance claims just as they track Amazon deliveries or Uber drivers? In terms of engagement with end users, this is merely one area where insurers lag behind other consumer industries.

Furthermore, insurance products themselves are undergoing transformation. Insurers are shifting from a simple claims reimbursement model to one focused on accident prevention and risk management. To make these new products effective, insurers must be able to monitor and proactively respond to vast amounts of data in real time. The speed and scale required to analyze and process this data far exceed human capabilities.

These changes necessitate that insurance companies improve their product design and customer service, with artificial intelligence playing a decisive role. In fact, according to Accenture’s survey on the future workforce, 63% of respondents believe that intelligent technologies will fundamentally transform the industry.

Most insurance companies have stated that their investments in artificial intelligence (AI) technologies have increased compared to two years ago, and they plan to further boost these investments in the future. Insurers have found that their initial investments have yielded tangible results and recognize that the continuous advancement of AI will drive further technological transformation—particularly in product development, risk management, and customer experience.

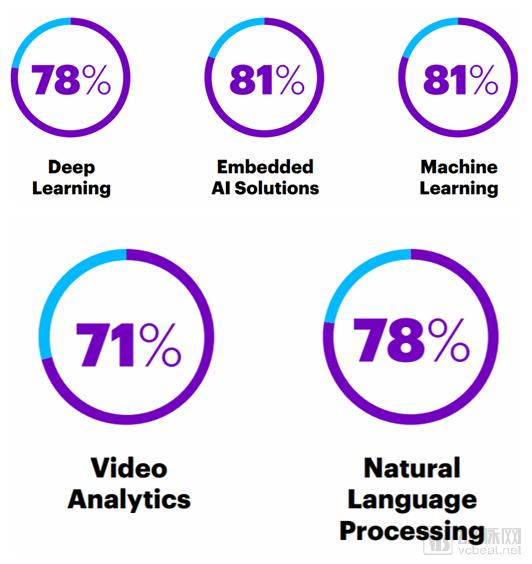

Insurance companies are heavily investing in artificial intelligence technologies, with plans to allocate investments over the next three years to the following areas: deep learning (78%), embedded intelligence solutions (81%), machine learning (81%), video analytics (71%), and natural language processing (78%).

Figure 1: AI Investment Directions for Insurance Companies

Source: Accenture

Insurtech startups have also recognized the importance of these technologies, with many companies positioning artificial intelligence (AI) as their strategic core and ensuring their employees are proficient in using AI tools. Accenture analyzed more than 450 global financing and investment deals involving insurtech companies, revealing that between 2014 and 2016, the number of investments related to AI or intelligent automation approximately tripled.

Only by enhancing employee productivity through intelligent frameworks and driving product innovation via intelligent automation and data analytics can insurance companies maximize their benefits with the help of artificial intelligence.

Human Resources—Leverage artificial intelligence to enable employees to allocate their time rationally and enhance work efficiency. Generate 80% of the value through 20% of non-routine tasks.

Process Management – Revisiting Business Models and Workflows. Continuously review end-to-end processes through intelligent machines, and apply “intelligent automation” to improve and optimize existing workflows.

Data Analytics—Insurance companies will leverage artificial intelligence to enhance their big data analytics capabilities, refine algorithms through transactional data, and combine data in novel ways to identify trends.

Many insurance companies have already invested heavily in technologies such as deep learning, video analytics, and natural language processing. Although intelligent technologies are advancing rapidly, insurers will be unable to fully unlock the potential of artificial intelligence unless they adapt their existing workforce to the changes it brings, which includes cultivating the right corporate culture and skill base.

Insurance companies need to develop strategies to adapt to the advancement of new technologies and enhance employees’ professional skills. The emergence of virtual customer service agents and chatbots has automated routine task workflows, allowing staff to focus on higher-value activities; therefore, targeted training remains essential. Functions such as underwriting and pricing will also increasingly rely on machine learning algorithms rather than human experience and judgment.

Corporate employees must understand that technology is a powerful enabler, not a replacement for their jobs. Artificial intelligence will create new jobs for the human workforce—even entirely new job categories. For example, insurance companies will need more staff to perform control and management tasks, as virtual workers and algorithms require human supervision. In fact, according to research by Accenture, 68% of insurance company executives anticipate that intelligent technologies will drive net job growth within their organizations over the next three years.

If insurance companies wish to adopt artificial intelligence (AI) technologies, their relevant personnel—such as data scientists and AI developers—must possess the skills to build, utilize, and maintain these technologies. This entails recruiting top-tier technical talent into a traditional industry characterized by relatively slow development. According to Accenture’s research on insurtech, one-third of insurance companies believe that a “shortage of professionals skilled in intelligent technologies” is hindering the advancement of AI.

To address evolving business needs, insurance companies must also leverage external resources to augment their human workforce and virtual employees. New technologies are fostering novel partnerships between insurers and tech firms, thereby necessitating a fundamental transformation in their outsourcing models.

Insurance companies must strictly regulate the application of artificial intelligence to ensure trust and transparency, particularly given the sensitivity of data. This entails establishing rigorous guidelines for AI use and implementing processes that are fully compliant with regulatory requirements.

Survey data also show that 52% of insurance company executives believe human-machine collaboration is crucial to achieving their core strategies; 61% anticipate that the proportion of employees required to work with artificial intelligence will rise over the next three years; and 68% consider that AI will have a positive impact on their work.

Intelligent automation should not merely automate existing manual processes to compensate for the shortcomings of current systems. Instead, it should fundamentally redefine these processes, and even business models, to achieve optimal results.

Insurance companies have begun to adopt Robotic Process Automation (RPA), laying a solid foundation for future technological advancements by creating a virtual workforce with rule-based capabilities and adaptability. Given current development trends, they need to build upon intelligent automation, enabling the virtual workforce to learn and adapt to business needs. This entails enhancing RPA with advanced artificial intelligence technologies, shifting from pre-programmed processes to intelligent decision-making.

For the insurance industry, the most significant benefit of the aforementioned transformation will be reflected in customer service. Intelligent end-to-end solutions can integrate front-end and back-office operations. For instance, they enable customer service representatives to access relevant customer data or provide recommendations to claims adjusters. This solution will create a frictionless experience for customers, delivering consistently high-quality customer service across any device and at any time.

Insurance companies anticipate that artificial intelligence will fundamentally transform their business models over the next three years. Seventy-five percent of insurance executives believe it is highly likely that tasks and processes within insurance firms will be automated in the coming three years, while 63% contend that intelligent technologies will bring about radical change to the industry.

67% of insurance company executives believe that intelligent technologies will help enterprises stand out in fierce market competition. 52% of insurance company executives believe that smarter decision-making can only be achieved through intelligent technologies capable of generating information in real time.

Figure 2: Insurance Company Executives' Predictions on AI-Driven Business Transformation

Source: Accenture Report

Intelligent automation not only enhances customer service but also improves work efficiency. Skilled and experienced employees are freed from repetitive tasks that can be automated, allowing them to dedicate time to higher-quality work and focus on tasks requiring human intervention or manual operation. This shift also makes their jobs more engaging.

Multiple enterprises have already applied intelligent decision-making to insurance processes. For instance, South Africa’s Santam Insurance utilizes predictive analytics and machine learning to reduce fraud and improve operational efficiency. This initiative helped them save $2.4 million in the first four months and accelerated the claims processing workflow.

Fukoku Mutual Life Insurance, a Japanese life insurer, is leveraging artificial intelligence to interpret medical certificates and factor in variables such as length of hospital stay, medical history, and surgical procedures to determine policyholders’ insurance premiums. This system is expected to boost productivity by 30% within two years and deliver a substantial return on investment.

However, the above examples do not imply that Robotic Process Automation (RPA) has become obsolete. Traditional forms of automation still play a role in enhancing AI-centric processes. For instance, once intelligent decisions are made, RPA can be leveraged to execute the corresponding actions. Furthermore, it helps reduce costs, thereby providing funding for the further development of intelligent automation.

Case Study—Intelligent “First Notice of Loss” (i-FNOL): Imagine that during your morning commute, you collide with another vehicle while adjusting the radio. You can call your insurer’s claims hotline to seek assistance and complete the basic FNOL report. The claims adjuster will confirm liability for the accident and request that you upload photos of the incident via the mobile app on your phone.

The system leverages computer vision and machine learning to analyze images, verify accident details, and automatically arrange post-accident vehicle handling. While awaiting processing, you can monitor real-time progress through the application.

Meanwhile, another algorithm automatically analyzes claims. When the predicted risk score for personal injury reaches as high as 63%, the claim is displayed in the relevant application for review by professional claims adjusters. They will immediately contact the other driver to arrange vehicle repairs.

To leverage data for pricing and risk management, insurance companies have made substantial investments in technology and personnel. However, their continued reliance on traditional actuaries indicates that data is not being fully utilized as it should be. Therefore, insurers should harness artificial intelligence to uncover the hidden value within their data, such as by querying and visualizing corporate and customer data in unprecedented ways.

This approach can break through the limitations of existing value chains and data silos, leveraging impact across the entire business. Customer claims data can be used not only to identify fraud but also to design better insurance products, or to leverage real-time analytics to predict customer needs and recommend products or services accordingly.

For example, Zurich Insurance Group is collaborating with EagleEye Analytics to leverage its Talon predictive analytics system. Machine learning algorithms generate real-time scores to better inform decision-making in claims management, pricing, underwriting, and other areas.

Insurance companies should not only focus on their own datasets but also leverage external or public datasets to achieve sustained growth, unlock new revenue streams, and drive business model innovation.

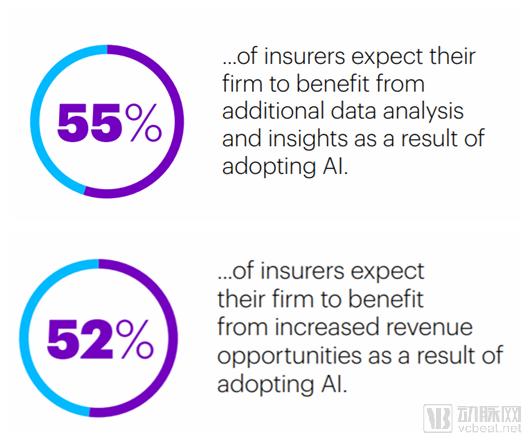

Artificial intelligence will help insurers gain richer insights from big data and may even open up new revenue streams. Fifty-five percent of insurers expect that leveraging AI for data analytics will deliver additional benefits, while 52% anticipate that AI will help them increase revenue.

Figure 3: Insurance Company Executives' Expectations of AI Value

Source: Accenture

In the future, artificial intelligence will transform how insurance companies organize, operate, and develop their businesses. They will leverage this technology to reduce costs, drive innovation, and create better experiences for customers. By adjusting human resources and operational models while implementing strict guidelines, insurance companies can better apply artificial intelligence technologies.

The most crucial point is that artificial intelligence does not stand in opposition to humanity; rather, it serves as a tool to help people improve work efficiency. As AI technology continues to evolve, its application in the insurance industry will inevitably drive a wave of reform in this traditional sector.

[Original Article Link]