Domestic Ultrasound Diagnostic Industry: The Rise and Development Path of Chinese Brands

Editor’s Note: This article is republished from the WeChat official account “Siyu Medical Device Observation,” authored by Alex. VCBeat has obtained authorization to repost it.

With technological advancements, the demand for non-invasive diagnostic equipment is growing. Due to its advantages of accuracy, intuitiveness, non-invasiveness, and ease of operation, ultrasound has become the preferred diagnostic method for many diseases in clinical practice. With the rise of domestically produced ultrasound systems, Chinese brands led by Mindray and SonoScape are continuously challenging foreign brands dominated by the “GPS” trio (GE, Philips, and Siemens). Given the continuous expansion, upgrading, and replacement within China’s ultrasound diagnostics market, along with increasing policy support for domestic ultrasound manufacturers, we have reason to believe that import substitution by domestically produced ultrasound systems will become more pronounced, offering new development opportunities for Chinese brands. Therefore, this article aims to systematically analyze the competitive landscape of China’s ultrasound diagnostics market and explore future investment opportunities in the industry.

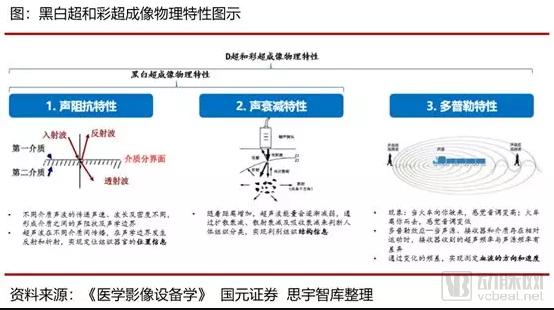

(I) Principles of Ultrasound Imaging

Ultrasound imaging is primarily achieved based on the physical properties of ultrasound wave propagation in continuous media. B-mode ultrasound mainly relies on two principles: acoustic impedance characteristics and acoustic attenuation characteristics. Color Doppler ultrasound, building upon B-mode ultrasound, additionally utilizes the imaging characteristics of the Doppler effect.

(II) Definition and Classification of Color Doppler Ultrasound

Color Doppler Ultrasound, short for Real-time Two-dimensional Color Doppler Flow Imaging System, is a high-end medical device that integrates advanced multidisciplinary technologies, including acoustic materials, information detection, electronic technology, microcomputer technology, image processing, and precision engineering. It can instantly calculate the direction, velocity, and distribution of blood cells in human blood flow, accurately displaying tissue perfusion status. Color Doppler ultrasound is an advanced ultrasonic diagnostic technique that combines conventional two-dimensional grayscale ultrasound with color Doppler flow imaging, representing the developmental trend of medical ultrasonic diagnostics.

Depending on the classification criteria, color Doppler ultrasound can be categorized into the following types:

1) Based on differences in imaging principles, color Doppler ultrasound systems are categorized into analog and fully digital types: owing to the more advanced imaging technology of fully digital systems, traditional analog color Doppler ultrasound is gradually being replaced by fully digital counterparts.

2) Based on the installation method, they are classified into console-based and portable systems: Portable color Doppler ultrasound systems offer advantages such as portability, a user-friendly interface, and rapid operation; in contrast, console-based color Doppler ultrasound systems are relatively bulky and less portable, but they provide more powerful features and superior performance.

3) Based on different application fields, they can be divided into general-purpose machines and specialized machines. General-purpose machines are generally used for whole-body examinations, while specialized machines are mainly used for specialized examinations such as cardiac and gynecological examinations.

(3) Core Components of Ultrasound Systems

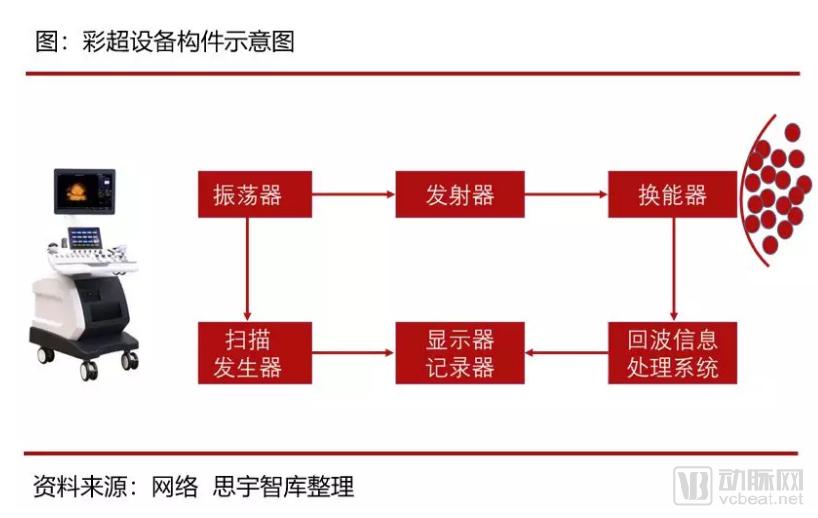

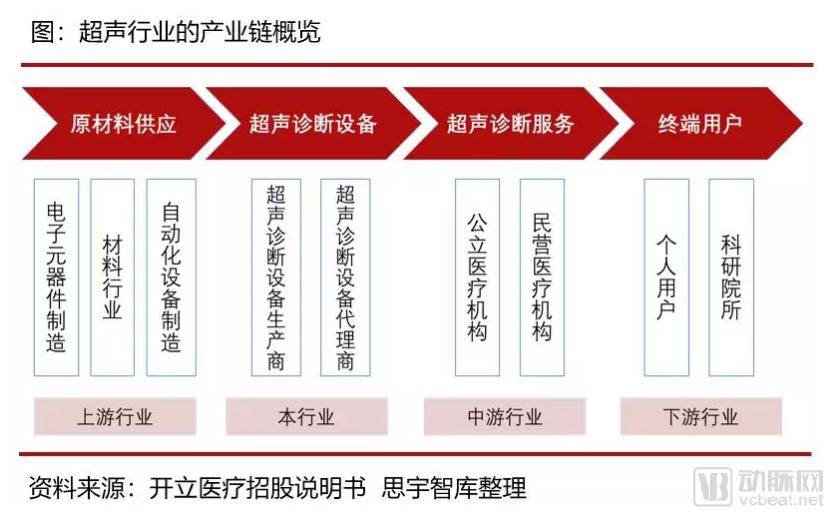

The upstream sector of the ultrasound industry involves the supply of raw materials such as electronic components, materials, and automation equipment, while ultrasound manufacturers engage in research and development, design, and production. The ultrasound transducer is the core factor determining imaging quality. Ultrasound diagnostic systems generate incident ultrasound waves and receive reflected waves through the transducer. Capable of both transmitting and receiving ultrasound, the transducer performs electro-acoustic signal conversion: it converts electrical signals from the main unit into high-frequency oscillating ultrasound signals, and transforms ultrasound signals reflected back from tissues and organs into electrical signals, which are then displayed on the monitor of the main unit.

The number of physical channels is the most critical parameter of an ultrasound probe. Generally, a higher channel count corresponds to a higher grade of color Doppler ultrasound systems. Based on the number of physical channels, color Doppler ultrasound systems can be categorized into five tiers: low-end, mid-low-end, mid-range, high-end, and ultra-high-end. The “Indicator Requirements for Industrialization Projects of Key Technologies in High-End Medical Devices and Pharmaceuticals,” issued by the National Development and Reform Commission in 2017, sets forth explicit requirements for high-end color Doppler ultrasound systems:

1) Key technologies: novel imaging technologies such as digital beamforming, high-frame-rate color flow imaging, contrast harmonic imaging, real-time 3D imaging, and shear wave elastography; multimodal technology; and miniaturization design technology;

2) Key components: new types of probes such as high-density single-crystal material probes and 2D matrix array probes;

3) Key Indicator: Number of physical channels ≥ 128.

Table: Classification of Color Doppler Ultrasound Equipment by Tier

Source: Compiled by Siyu Think Tank, Shenzhen Huasheng Medical

The transmit frequency of the probe is primarily determined by the thickness of the crystal, while the shape of the crystal element defines key characteristics such as the beam profile and acoustic field distribution. Higher probe frequencies yield higher resolution, but penetration depth is inversely proportional to frequency. Therefore, high-frequency probes are used for examining superficial organs, whereas low-frequency probes are employed for imaging deep-seated viscera.

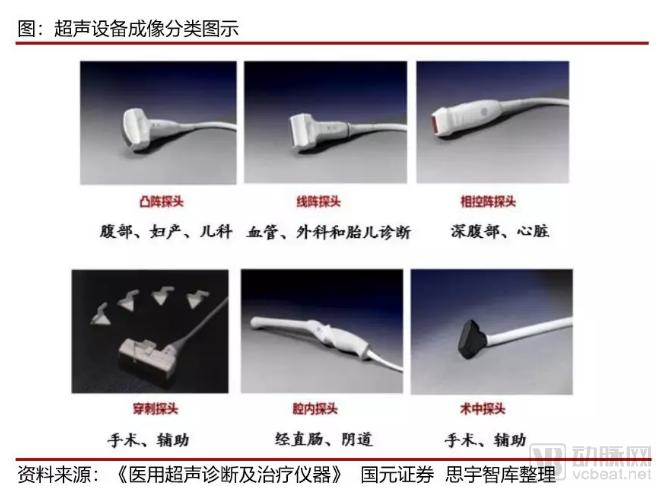

Ultrasound probes are classified in various ways. Based on the diagnostic site, they include ophthalmic probes, cardiac probes, abdominal probes, intracranial probes, endocavitary probes, and pediatric probes. According to beam steering methods, they are primarily categorized into the following types:

1) Convex array probe: Mostly 3.5MHz, with sector imaging, mainly used for abdominal diagnosis of liver, gallbladder, pancreas, spleen, and kidney, as well as gynecology, obstetrics, and pediatrics;

2) Linear array probe: Mostly 3.5 MHz, with rectangular imaging, primarily used for vascular, surgical, and fetal diagnostics;

3) Phased array linear probe: Mostly 3.0MHz, sector imaging, mainly used for deep abdominal and cardiac-related diagnosis;

4) Endocavitary probes: mostly 6.5 MHz, including transrectal and transvaginal probes;

5) Puncture probes and intraoperative probes: Used for surgery or adjuvant therapy.

Piezoelectric crystals are the core of imaging. The probe utilizes the piezoelectric effect of these crystals to convert high-frequency electrical energy into ultrasonic waves for external radiation, and receives returning ultrasound echoes, converting them back into electrical energy via the piezoelectric effect. Currently, the most commonly used piezoelectric crystals are made of PZT material, a composite consisting of zirconium, titanium, and lead. Variations in manufacturing processes—such as crystal growth, cutting, and sintering methods—applied to the same base material yield diverse final products, resulting in differences in frequency bands, imaging clarity, and overall image quality.

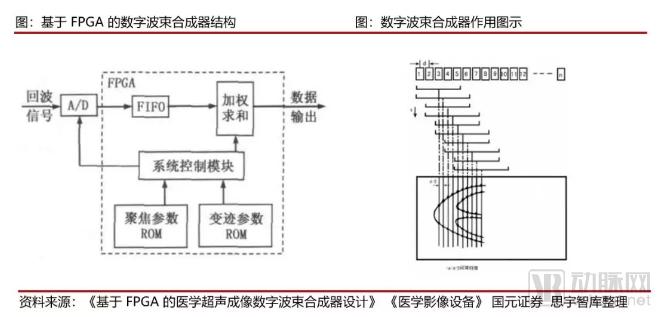

Ultrasound imaging also requires beamforming technology, which employs techniques such as electronic focusing, apodization, and steering to generate acoustic beams with well-defined directivity when using array transducers. Current digital beamformers are primarily composed of electronic components such as chips and integrated circuits. China’s domestic chip technology lags behind, necessitating substantial reliance on imports. While microcontroller units (MCUs) used in some low-end models can now be sourced domestically, the field-programmable gate array (FPGA) chips required for mid- to high-end models must be imported and are controlled by only four overseas companies: Xilinx, Altera, Lattice, and Microsemi. Other electronic components are relatively commonplace, and domestic manufacturers can basically meet the demand.

(IV) Advantages and Main Application Areas of Color Doppler Ultrasound

Color Doppler ultrasound offers advantages such as accuracy, intuitive visualization, non-invasiveness, and ease of operation in disease diagnosis, making it the preferred diagnostic method for many conditions in clinical practice. Its primary applications in disease management can be broadly categorized into the following areas:

Table: Major Application Areas of Color Doppler Ultrasound

Source: Compiled by VBInsight from CNKI

However, ultrasound technology still has some limitations that are difficult to overcome:

1) Ultrasound has limited penetration depth, making it difficult to reach deep structures through bone or air. Consequently, it is challenging to examine gas-containing organs such as the lungs and gastrointestinal tract, and its diagnostic capability for adult cranial conditions is inferior to that of X-ray and CT. Sonographic images reflect differences in acoustic impedance among organs and tissues, which lack specificity. Therefore, determining the nature of lesions in these areas requires comprehensive analysis, integrating findings from other imaging modalities and clinical data.

2) The accuracy of ultrasound remains limited; currently, tumor tissues smaller than 1 cm are difficult to detect. Consequently, a negative ultrasound result does not exclude the possible presence of tumor lesions under 1 cm. Due to the small size of the lesions and minimal differences in acoustic impedance, there is insufficient variation in reflection to be visualized on sonograms.

3) Ultrasound reflections may undergo multiple repeated reflections and interference, resulting in artifact echoes that can lead to partial misdiagnosis.

4) Ultrasound examination is a dynamic procedure and is less standardized than X-ray or CT. The performance of the ultrasound equipment, as well as the technical skills and experience of the operator, also influence the diagnostic results.

(I) The Development History of Color Doppler Ultrasound Internationally

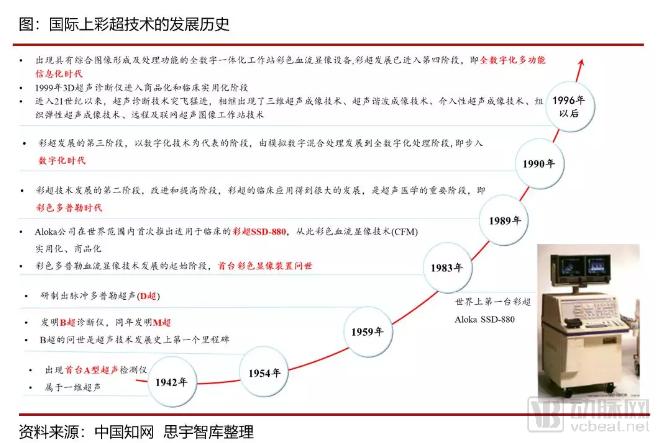

In 1880, the piezoelectric effect of crystals was discovered. In 1917, ultrasound detection was performed using the piezoelectric principle, and ultrasound transducers were developed during the same period. In 1942, the first A-mode ultrasound detector (a type of one-dimensional ultrasound) was invented. In 1954, B-mode ultrasound diagnostic equipment and M-mode ultrasound were invented; the advent of real-time two-dimensional cross-sectional grayscale ultrasound imaging devices (B-mode) marked the first milestone in the history of ultrasound technology development. In 1959, pulsed Doppler ultrasound (D-mode) was developed.

In November 1983, Aloka Corporation launched the SSD-880, the world’s first clinically applicable color Doppler ultrasound system, marking the practical application and commercialization of Color Flow Mapping (CFM) technology. The advent of CFM technology represented another new milestone in the history of ultrasound development, signifying that ultrasound diagnostics had entered the era of color Doppler imaging.

The period after 1989 marked the second phase in the development of color Doppler ultrasound technology—the stage of improvement and enhancement. During this time, clinical applications of color Doppler ultrasound advanced significantly, ushering ultrasonic medicine into a pivotal era: the age of color Doppler.

Since 1990, the development of color Doppler ultrasound has entered its third phase—the era characterized by digital technology, marking the transition from analog-digital hybrid processing to fully digital processing, i.e., stepping into the digital age.

After 1996, fully digital integrated workstations with comprehensive image formation and processing capabilities for color flow imaging emerged. This represents the new face of “color Doppler ultrasound.” It marks the entry of color Doppler ultrasound development into its fourth stage—the era of full digitization, multifunctionality, and informatization.

In 1999, 3D ultrasound diagnostic systems began to enter the stages of commercialization and clinical practical application.

Since the beginning of the 21st century, ultrasonic diagnostic technology has witnessed rapid advancement, with the successive emergence of new technologies and functionalities: three-dimensional (3D) ultrasound imaging, harmonic ultrasound imaging, interventional ultrasound imaging, tissue elasticity ultrasound imaging, and remote and networked ultrasound image workstation technology.

(II) The Development History of Domestically Produced Color Doppler Ultrasound Systems

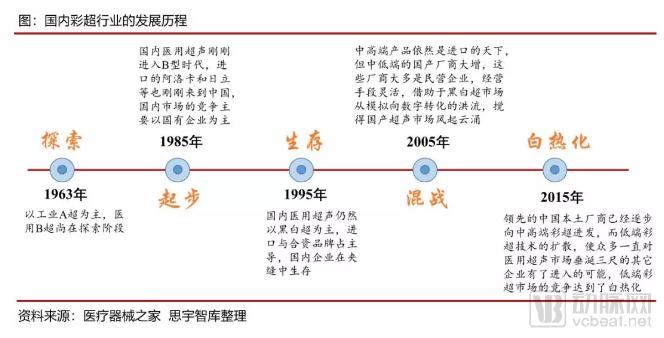

It has been 50 years since the first domestically produced ultrasound machine was introduced. In 1963, China primarily relied on industrial A-mode ultrasound, while medical B-mode ultrasound was still in its exploratory stage. In 1983, the Shantou Ultrasound Instrument Research Institute developed the CTS-18 model, which was hailed as the “Chinese B-ultrasound.” By 1985, medical ultrasound in China had just entered the B-mode era, around the time when imported brands such as Aloka and Hitachi were just entering the Chinese market. Competition in the domestic market was then dominated by state-owned enterprises.

In 1995, black-and-white ultrasound still dominated the domestic medical ultrasound market in China, but imported and joint-venture brands held a leading position, leaving Chinese companies struggling to survive in a narrow niche. At that time, Shantou Ultrasound and Haiying remained major players in the market, while ultrasound manufacturers in Tianjin and Wuhan faded into obscurity due to ineffective reforms, particularly under the impact of new competition from newly established private enterprises.

In 2005, the domestic mid-to-high-end color Doppler ultrasound market was still dominated by imported products, but there was a significant increase in Chinese manufacturers focusing on the low-to-mid-end segment. Most of these manufacturers were private enterprises. Ultrasound companies competing in the market at that time included Shantou Ultrasound, Sonoscape, Uniplex, Landwind, Anke, Zhonghui, Well.D, Belsen, Kaixin, Tianhuihua, and Zhuhai Will. In 2001, Mindray officially launched China’s first fully digital black-and-white ultrasound diagnostic system, the DP-9900, which possessed complete independent intellectual property rights, marking the transition of domestic black-and-white ultrasound from the analog era to the digital era. In 2002, Mr. Yao Jinzhong, known as the “Father of Chinese Ultrasound,” left Shantou Ultrasound to found SonoScape, which successfully launched the world’s first 15-inch LCD large-screen, full-featured portable color Doppler ultrasound system in 2004. During this period, foreign brands represented by GPS (GE, Philips, and Siemens) occupied more than 95% of the color Doppler ultrasound market, holding an absolute monopoly.

In 2015, leading Chinese domestic manufacturers had begun to advance into the mid-to-high-end color Doppler ultrasound market. Foreign brands, represented by GPS (GE, Philips, and Siemens), accounted for 75% of the color Doppler ultrasound market, establishing a relatively monopolistic position. During this phase, color Doppler ultrasound technology evolved from traditional morphological diagnosis to functional diagnosis (including imaging, single-point tracking, contrast-enhanced ultrasound of blood vessels, and microscopic research). For instance, ultra-high-end cardiac color Doppler ultrasound emerged, marking a qualitative leap in the industry. Meanwhile, the proliferation of low-end color Doppler ultrasound technologies enabled many other companies, which had long coveted the medical ultrasound market, to enter the field, intensifying competition in the low-end segment to a fever pitch.

(3) Continuous Intensification of Domestic Policy Support

To achieve long-term development, domestic color Doppler ultrasound manufacturers must closely align with national strategic directions. In recent years, the Chinese government has continuously introduced policies to encourage the development of color Doppler ultrasound technology. From "Made in China 2025" to the two editions of the "Three-Year Action Plan for Enhancing Core Competitiveness of the Manufacturing Industry," these initiatives strongly demonstrate the nation’s determination to vigorously promote domestically produced color Doppler ultrasound systems. Particular attention should be paid to the shift in policy support for color Doppler ultrasound equipment outlined in the "Three-Year Action Plan for Enhancing Core Competitiveness of the Manufacturing Industry," issued by the National Development and Reform Commission (NDRC) in 2015 and 2017. The focus shifted from key research and development in the 2015 version to promoting upgrades and performance improvements in the 2017 version. This change in wording is highly significant and warrants careful examination. It indicates that during the 2015–2017 cycle of the action plan, domestic color Doppler ultrasound equipment completed its foundational layout. Moving forward, national policy will encourage further development driven by expansion from the mid-to-low-end market into the high-end segment, as well as equipment upgrades among end-user clinical customers.

Table: Interpretation of Key Policies for the Domestic Color Doppler Ultrasound Industry

Source: Compiled by Siyu Think Tank from official government websites

III. Market Size Estimation

(I) Global Market Size of Medical Ultrasound Diagnostic Equipment

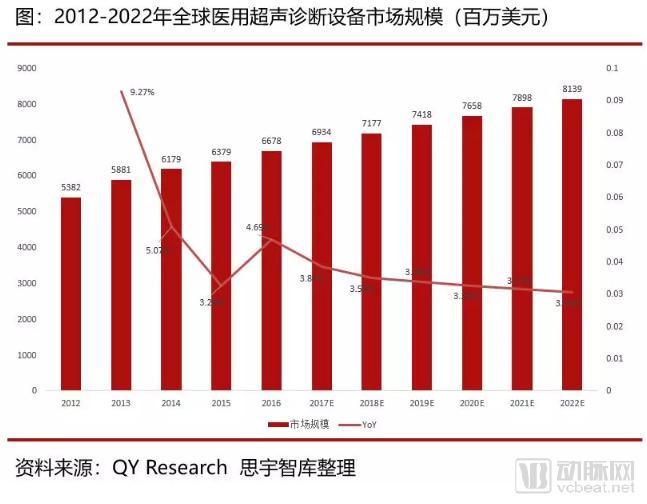

According to data from the “2016–2022 Global Medical Ultrasound Equipment Industry Analysis and In-Depth Market Research Report” published by market research firm QY Research, the global market size for medical ultrasound diagnostic equipment reached USD 6.7 billion in 2016. The market has maintained steady growth in recent years and is projected to sustain an annual growth rate of approximately 3% in the coming years, with its size expected to reach USD 8.1 billion by 2022.

(II) Market Size of Domestic Medical Ultrasound Diagnostic Equipment in China

Compared with the international market, China’s ultrasound diagnostic equipment industry started later. However, after years of development, it has initially formed an industrial system with comprehensive professional categories, a complete industrial chain, and a solid foundation. In 2016, the market size of ultrasound diagnostic equipment in China reached US$1.15 billion, and is expected to maintain an annual growth rate of around 6% in the coming years (higher than the global growth rate of 3%). It is projected that by 2022, the market size of medical ultrasound diagnostic equipment in China will reach US$1.58 billion.

(3) Estimation of the Market Size for Color Doppler Ultrasound in China

Under the current national conditions, the domestic color Doppler ultrasound market exhibits the following characteristics:

1) There are certain differences in the procurement prices of color Doppler ultrasound systems among hospitals of different tiers and regions;

2) The typical service life of color Doppler ultrasound equipment is 8 years, while large hospitals generally replace their units every 3 years; the replaced equipment is typically transferred to primary-care hospitals for continued use.

3) County-level hospitals in primary care settings are mainly equipped with imported color Doppler ultrasound systems, while township and community healthcare institutions are primarily supplied with domestically produced color Doppler ultrasound systems distributed by the government.

Therefore, we selected several indicators—including the number of hospitals in China, the number of color Doppler ultrasound systems in hospitals, procurement prices for color Doppler ultrasound systems, the replacement rate of these systems, and the proportion of replaced units from higher-level hospitals that are taken over by primary-care hospitals—to conduct a sensitivity analysis on the scale of replacement and volume growth in China’s color Doppler ultrasound market. The key assumptions are as follows:

1) Based on data from the China Health and Family Planning Statistical Yearbook 2017, determine the number of hospitals at all levels in the eastern, central, and western regions;

2) Assume the number of color Doppler ultrasound systems in hospitals at all levels across various regions;

3) Estimate the procurement cost per color Doppler ultrasound unit for hospitals at various levels and in different regions, based on the 2018 domestic color Doppler ultrasound procurement data published by “Baiyi Zhaocai Wang”;

4) The replacement rate of color Doppler ultrasound systems in hospitals at all levels is assumed to be 10%-30%;

5) The proportion of color Doppler ultrasound systems replaced by higher-level hospitals and taken over by primary care hospitals is assumed to be 50%–90%. Primary care hospitals are assumed to be ungraded institutions. The annual actual number of color Doppler ultrasound systems required for procurement by primary care hospitals = the number of color Doppler ultrasound systems requiring replacement due to obsolescence − the number of color Doppler ultrasound systems taken over from higher-level hospitals.

By constructing a data model, we conducted sensitivity analysis on the replacement and volume growth scale of the domestic color Doppler ultrasound market. The results indicate that the annual market size for color Doppler ultrasound replacement and volume growth in Chinese hospitals is estimated to be between RMB 7 billion and RMB 20 billion.

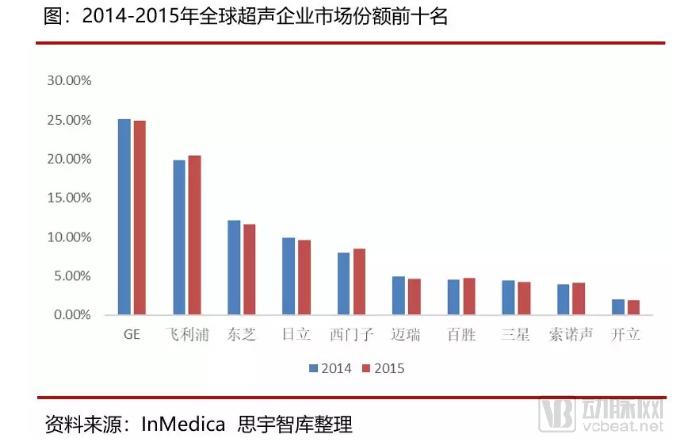

(1) Global Ultrasound Market Landscape

Europe, the United States, and Japan constitute the primary markets for ultrasound systems, collectively accounting for 70% of the global market. Demand in these regions is driven mainly by product upgrades and replacements, resulting in steady market growth. The international market is dominated by multinational giants such as GE, Philips, Siemens, and Hitachi, which firmly hold the majority share of the mid-to-high-end color Doppler ultrasound segment. In 2014–2015, Chinese brands Mindray Medical and Sonoscape Medical broke into the top ten global ultrasound companies by market share.

(II) Domestic Ultrasound Market Landscape

1) Foreign brands have shifted from absolute monopoly to relative monopoly

Prior to 2004, there were no domestically produced color Doppler ultrasound systems in China, and the domestic market was dominated by foreign brands. From 2004 to 2006, GE, Philips, and Siemens (collectively referred to as “GPS”) held a combined market share of 95%, maintaining an absolute monopoly. Between 2006 and 2012, Chinese brands continuously launched new color Doppler ultrasound products, capturing the mid-to-low-end market and driving down prices for low-end systems by more than 30%. During this period, GPS’s market share declined to 90%. Since 2012, domestic manufacturers represented by Mindray Medical and Sonoscape have intensified their efforts in the mid-to-high-end market, successively introducing mid-to-high-end products that reduced prices in this segment by 20%. Consequently, GPS’s market share has further decreased to 75%, reflecting a position of relative monopoly.

2) Domestic leader Mindray Medical’s annual sales volume of color Doppler ultrasound systems has surpassed that of GPS

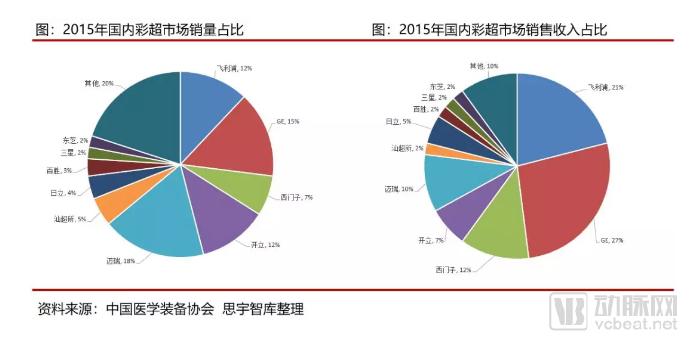

According to data released by the China Association of Medical Equipment, in 2015, domestic sales volume of color Doppler ultrasound systems saw the Chinese brand Mindray successfully surpass foreign companies such as GE, Philips, and Siemens. However, it is worth noting that in terms of sales revenue, the top three positions were still held by GE, Philips, and Siemens, with Mindray ranking fourth.

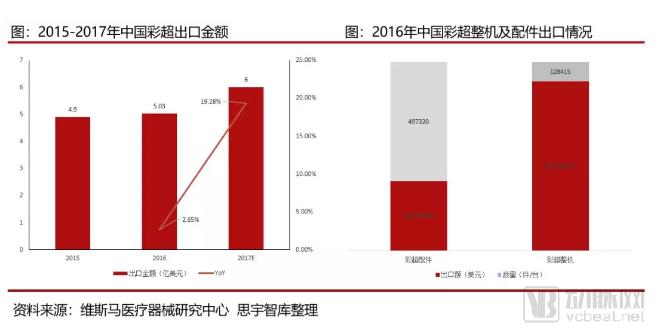

3) Export value of domestically produced color Doppler ultrasound systems rises year by year

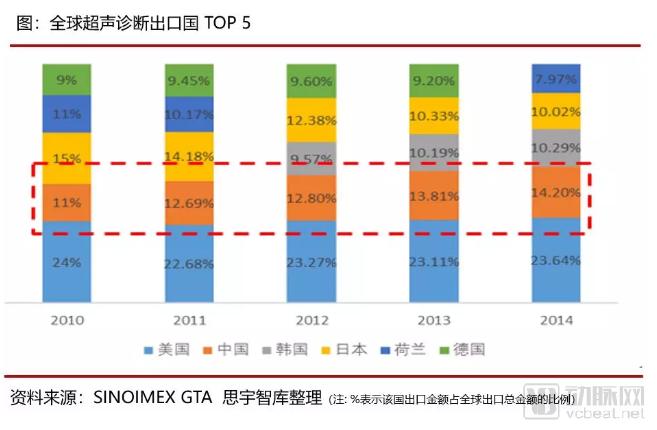

Although domestically produced color Doppler ultrasound systems have a history of only thirteen years, Chinese brands have grown from nothing to something, and from weak to strong. They have not only actively explored the domestic market but also ventured abroad to expand into international markets. From 2010 to 2014, China's ultrasound export volume continued to rise. As the proportion of export revenue increased, the international status of domestically produced color Doppler ultrasound systems also steadily improved.

According to data from the Weima Medical Device Research Center, the value of color Doppler ultrasound systems exported from China continued to rise between 2015 and 2017. In 2016, export revenue reached USD 503 million (USD 307 million for complete units and USD 196 million for accessories), with the total expected to reach USD 600 million in 2017, representing a growth rate of 19.28%.

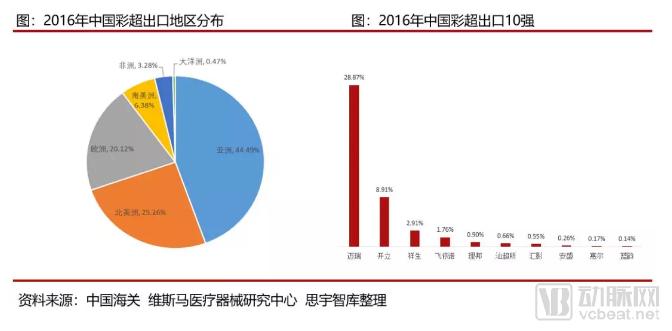

According to China Customs import and export data statistics, in 2016, domestically produced color Doppler ultrasound systems were exported to a total of 160 countries and regions, with Asia, North America, and Europe being the primary export destinations.

Among the major manufacturers of Chinese-made color Doppler ultrasound systems for export, Mindray Medical and Sonoscape Medical hold the largest market shares. Mindray’s primary export brands include its proprietary brand Mindray (83%), Zonare (15.49%), and Konica (0.69%). Sonoscape’s main export brands are its proprietary brand Sonoscape (91%), Aeroscan (2.7%), and Medisono (2.5%).

(1) Foreign Brands: Actively Positioning in the High-End Color Doppler Ultrasound Market for Specialties Such as Cardiology and Obstetrics & Gynecology

1) GE Healthcare (USA)

GE Healthcare Systems is the world’s largest supplier of medical equipment, with a product portfolio that includes CT, MR, X-ray, ultrasound, nuclear medicine, ECG diagnostics, and patient monitoring systems, serving customers worldwide. In 1998, GE acquired the U.S.-based ultrasound company Diasonics and, leveraging its own R&D capabilities, developed the LOGIQ series of radiology ultrasound systems. That same year, it also acquired Vingmed, leading to the development of the VIVID series of cardiac ultrasound products. In 2001, GE acquired Kretztechnik, an Austrian ultrasound giant, from MEDISON. Capitalizing on Kretztechnik’s strengths in 4D imaging, GE established the VOLUSON series of ultrasound systems for obstetrics and gynecology.

GE’s color Doppler ultrasound products cover a wide range of fields, from obstetrics and gynecology to general imaging and cardiovascular ultrasound imaging. The product lineup primarily consists of three major series: the LOGIQ series for whole-body examinations, the Voluson series for obstetrics and gynecology, and the Vivid series for cardiovascular examinations. Additionally, GE offers portable ultrasound systems such as the Venue 50 and Vscan with Dual Probe for use in clinical departments, as well as the Invenia ABUS for volumetric breast ultrasound.

2) Royal Philips Healthcare Systems Group

Royal Philips of the Netherlands was founded in 1891 in the Netherlands and is one of Europe’s largest electronics companies. Its products span three major sectors: Healthcare, Personal Health (Lifestyle), and Core Technologies. The company entered the Chinese market as early as 1920. Philips’ medical systems portfolio includes computed tomography (CT) systems, magnetic resonance imaging (MRI) systems, oncology radiation therapy systems, X-ray and angiography systems, patient monitoring systems, ultrasound imaging systems, nuclear medicine and PET systems, clinical information systems, as well as repair services and technical support. The development of Philips’ ultrasound imaging systems has been driven by the successive mergers with two leading specialized ultrasound manufacturers: ATL and Agilent (formerly HP). ATL was a specialized ultrasound manufacturer renowned for its abdominal and small-parts ultrasound products, while Agilent held a leading position in cardiac ultrasound research.

3) Siemens Healthineers AG, Germany

Siemens Healthineers is one of the largest providers of medical equipment and solutions worldwide, with its business spanning imaging systems for diagnosis and therapy, as well as electronic medicine and hearing technologies. In 2001, Siemens AG acquired Acuson Corporation. Siemens’ color Doppler ultrasound systems are primarily based on the Acuson series, with applications covering general imaging, cardiovascular, obstetrics and gynecology, breast imaging, and clinical (portable) use.

Table: Technical Features and Advantages of Siemens High-End Color Doppler Ultrasound Systems

Source: Siemens Official Website, compiled by VBInsight

(II) Domestic brands: Building on the mid-to-low-end market, they are actively expanding into the high-end color Doppler ultrasound segment.

1) Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

Founded in 1991, Mindray is a global leading provider of medical devices and solutions. Its products and solutions cover four major areas: Patient Monitoring & Life Support, In-Vitro Diagnostics, Medical Imaging, and Surgical Products. They are applied in more than 190 countries and regions worldwide, serving nearly 110,000 medical institutions in China and over 99% of Grade A tertiary hospitals.

Mindray entered the imaging sector in 1996, successively launching China’s first fully digital black-and-white ultrasound system, desktop color Doppler ultrasound system, and portable color Doppler ultrasound system with independent intellectual property rights. Mindray possesses a suite of advanced technologies, including ZST+ imaging technology, 3T sensor technology, Echo Boost, iLive, and single-crystal sensor technology, providing advanced solutions for cardiology and obstetrics/gynecology applications and establishing itself among the leaders in high-end imaging technology. The company is committed to promoting the application of ultrasound technology globally, expanding its use into anesthesiology, emergency medicine, and sports settings, and providing ultrasound skills training to thousands of physicians worldwide each year.

The Company has actively expanded its Resona series of high-end color Doppler ultrasound systems, enhancing brand image and driving growth in sales revenue. At the end of 2015, the Company launched new products such as the Resona 7, formally entering the high-end ultrasound imaging sector; at the end of 2017, it introduced the next-generation high-end intelligent ultrasound system dedicated to obstetrics and gynecology, the Resona 8.

2) Shenzhen Sonoscape Medical Corp.

Sonoscape was established in 2002 under the leadership of Mr. Yao Jinzhong, a pioneer in the development of ultrasound instruments in China. The company is dedicated to the research, development, and manufacturing of clinical medical equipment, with a product portfolio covering ultrasound diagnostic systems, electronic endoscopy systems, and in vitro diagnostic series.

In 2004, the company launched the world’s first 15-inch LCD large-screen, fully functional portable color Doppler ultrasound system, and in 2008, it pioneered the release of domestically produced intraoperative probes. Between 2012 and 2016, it successively introduced a series of high-end and portable color Doppler ultrasound products. Meanwhile, its probe product line became the first in the industry to achieve full domestic production, comprehensive coverage across all clinical departments, and a complete product range. In 2015, the company unveiled China’s first multi-element single-crystal probe with independent intellectual property rights. Currently, the company offers more than 20 ultrasound imaging products, paired with self-manufactured probes, covering multiple medical fields suitable for ultrasound diagnostic imaging.

From 2012 to 2018, the company successively launched a series of high-end and portable color Doppler ultrasound products, such as the S60, a high-end whole-body application color Doppler ultrasound system. In 2015, it introduced China’s first independently developed multi-element single-crystal probe with proprietary intellectual property rights. The company has achieved a leading position in China in color Doppler ultrasound probe technologies, including high-frequency phased array technology, transesophageal probe technology, endoscopic probe technology, biplane probe technology, and 4D probe technology. The company offers more than 60 models of ultrasound probes, characterized by high density, high sensitivity, and wide bandwidth, with clinical applications basically covering organs throughout the entire human body.

Table: Technical Features and Advantages of KaiLi High-End Color Doppler Ultrasound

Sources: Sonoscape official website, Company Prospectus, compiled by Siyu Think Tank

Artificial intelligence has been a hot topic in recent years, and its future applications in the field of ultrasound are highly anticipated. However, compared to its application in other imaging modalities, the development of AI-powered ultrasound faces greater challenges:

1) The operation of ultrasound diagnosis is not standardized, and the number of standardized images available for machine learning is very limited;

2) Ultrasound imaging possesses dynamic characteristics; when leveraging deep learning for artificial intelligence training, it is akin to analyzing ultrasound image features from video data, which is more complex to process than the recognition of other static medical images;

3) Ultrasound diagnostics require real-time results, which imposes higher demands on the product.

Currently, most development efforts remain at the “sub-intelligent” stage, limited to the analysis of static images. Both domestic and international companies in the “AI + ultrasound” sector predominantly use still images as training data for their artificial intelligence models. Only Bay Labs in the United States employs dynamic video footage, with its achievements primarily focused on breast and thyroid applications. Integrated into conventional ultrasound systems, its technology provides auxiliary lesion delineation.

It is evident that artificial intelligence (AI) research in the field of ultrasound holds substantial room for advancement and significant practical value. By integrating AI-assisted tools into ultrasound equipment to help primary care physicians address diagnostic challenges in real time, it is possible to alleviate the issues of uneven expertise and shortage of medical specialists at the primary care level, thereby actively promoting the effective implementation of tiered diagnosis and treatment systems.