Assisted Reproductive Technology Industry Report: Exploring 7.42 Million Potential Patients and a RMB 572 Billion Underserved Market

Having children is the most sincere expectation of every couple. Couples who have not conceived after one year of unprotected intercourse are generally classified as infertile and may require medical treatment. Reproduction is such a complex issue that the advent of assisted reproductive technologies does not always bring joy and warmth. The emergence of each new technology inevitably raises a series of ethical, legal, social, and resource-allocation considerations.

Across the healthcare industry, assisted reproductive technology (ART) is a specialized vertical sector with relatively low levels of marketization and maturity, encompassing multiple subfields such as treatment services, consumables, biopharmaceuticals, and diagnostic testing. Within the ART industry chain, “supply” and “demand” are inextricably linked.

Amid the persistently high infertility rates and the backdrop of China’s “two-child” policy, what is the true supply-and-demand dynamic in China’s assisted reproductive technology (ART) industry? How can infertility be treated with precision? What is the current state of the entire ART sector? What is the actual demand for infertility treatment in China? What is the genuine market potential of the ART industry? And how should the ART industry move forward in the future?

WeDoctor Beilian Research Institute for Assisted Reproduction and VCBeat VBInsight jointly released the “2018 Report on the Assisted Reproduction Industry.” Through comprehensive and systematic research, the report provides insights into the development of the assisted reproduction services sector, deconstructs the industry’s ecological chain, interprets the current status of assisted reproduction medical institutions from a data-driven perspective, and incorporates an overview of the cross-border assisted reproduction industry. It offers judgments and recommendations for future development, thereby facilitating the next stage of growth in the assisted reproduction industry.

This paper primarily compiles multiple industry research reports, expert papers, and data from authoritative domestic and international institutions. Through systematic organization and data cleaning, it conducts an analytical study of the assisted reproductive technology (ART) industry. The research encompasses six major dimensions: industry insights, technological interpretation, deconstruction of the industrial chain, market analysis, examination of cross-border ART services, and assessment of future industry trends. It covers more than fifteen secondary indicators, including public health, ethics, policy, consumption potential, technology, treatment protocols, industrial chain dynamics, and market size.

I. Incidence Rate of 12.5%–15%: Identifying the “True” Demand Side

The World Health Organization predicts that infertility will become one of the three major diseases affecting humanity in the 21st century, second only to cancer and cardiovascular and cerebrovascular diseases. In China, due to factors such as environmental degradation, increased work-related stress, and delayed childbearing age among women, the incidence of infertility has been rising year by year. According to data from Ping An Securities Research Institute, the national prevalence of infertility is approximately 12.5%–15%, meaning that about 12 to 15 out of every 100 women of reproductive age suffer from infertility, with around 20% of these cases requiring treatment through assisted reproductive technologies (ART).

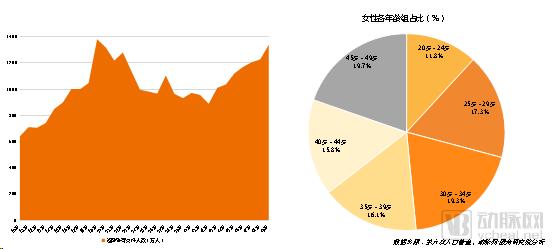

Based on data from the Sixth National Population Census, we project that, after excluding 32.28 million females aged 15–20 who are below the legal marriage age, the number of Chinese women of childbearing age (21–49 years) amounted to approximately 308 million by the end of 2019. Among all female age groups, those aged 45–49 accounted for the largest proportion at 19.7%, while women outside the optimal childbearing age (aged 35 and above) constituted 50.6%.

As women age, although they maintain normal menstrual cycles, their fertility begins to decline gradually. This is primarily due to factors such as diminished ovarian function, reduced endometrial receptivity, follicular atresia, telomere shortening, and decreased telomerase activity. The main physiological manifestations include reduced pregnancy and live birth rates, along with an increased miscarriage rate.

1. Based on incidence rates, it is estimated that by the end of 2019, approximately 38.5 to 46.2 million women of childbearing age in China were affected by infertility of varying degrees;

2. Assuming that all women of childbearing age have fertility needs (including patients who are already undergoing treatment), calculated at 20%, approximately 7.7 to 9.24 million women of reproductive age require assisted reproductive technology (ART) for treatment, indicating a rigid demand for ART;

3. From the perspective of the proportion of women of childbearing age across different age groups, the share of women not in their optimal reproductive age due to China’s aging trend stands at 50.6%. In the future, the proportion of advanced maternal age pregnancies will grow rapidly. The rising proportion of pregnancies among women of advanced maternal age indicates that well over 20% of individuals require assisted reproductive technology (ART) for treatment, meaning the actual number of people with a need for ART far exceeds 7.7 to 9.24 million.

II. Patient Profile of Infertility: The Largest Group Consists of Women with Infertility Caused by Thin Endometrium

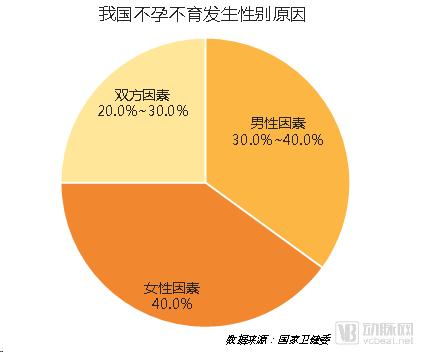

Infertility factors may lie with the female partner, the male partner, or both. Data from the National Health Commission of China indicate that among infertility cases attributable to gender-specific factors, male factors account for 30%–40%, female factors account for 40.0%, and combined factors account for 20.0%–30.0%.

A further deconstruction of the causes of infertility reveals that the primary etiologies in male patients are sperm and semen abnormalities, sexual dysfunction, prostatitis, and varicocele. Among these, sperm abnormalities constitute the leading cause, accounting for 57%, indicating a concerning status of male sperm quality. In female patients, the five main causes are thin endometrium, menstrual irregularities, polycystic ovary syndrome (PCOS), poor follicular development, and fallopian tube obstruction. Infertility caused by thin endometrium is the most prevalent, representing 40.0% of cases, followed by menstrual irregularities, which account for 30.0%.

III. Industry Tailwinds Are Evident: New Consumer Healthcare Choices Driven by Policy

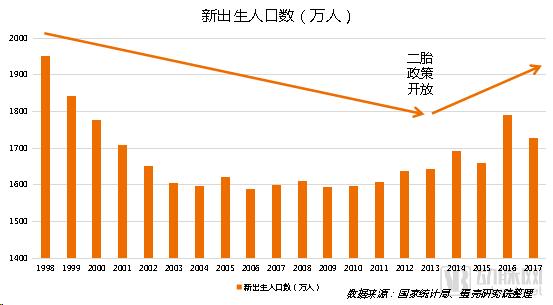

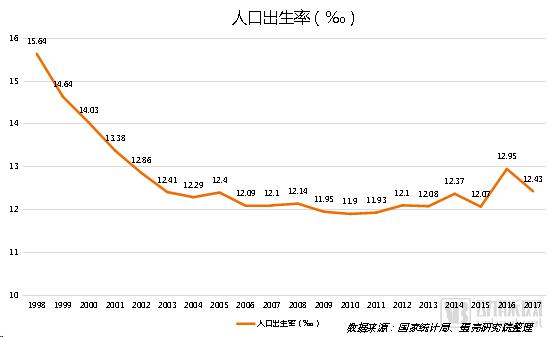

Data from the National Bureau of Statistics shows that China has experienced a long-term decline in its newborn population. Before the formal implementation of the “two-child” policy in 2013, the number of newborns decreased from 19.51 million in 1998 to 16.44 million in 2013, while the birth rate dropped from 15.64‰ to 12.07‰.

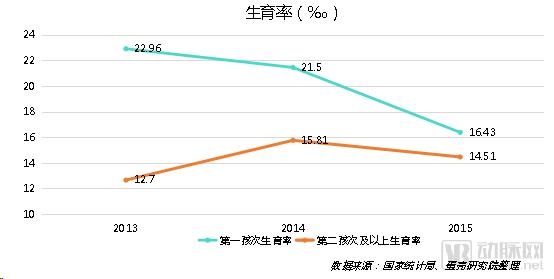

A further breakdown of the data reveals that since the implementation of the two-child policy, the first-child birth rate has continued to decline, dropping from 22.96‰ to 16.43‰; meanwhile, the increase in the birth rate for second and higher-order children has made the largest contribution to the growth in the overall birth rate, rising from 12.70‰ to 14.51‰.

We conducted statistical analysis and data cleaning on the 2014–2015 data following the formal implementation of the “Two-Child Policy.” The current status of women of childbearing age reveals a decline in fertility rates among women of optimal childbearing age, alongside a substantial increase in the number of advanced maternal age pregnancies.

2. The significant rise in the age of late marriage and delayed childbearing has severely impacted fertility.

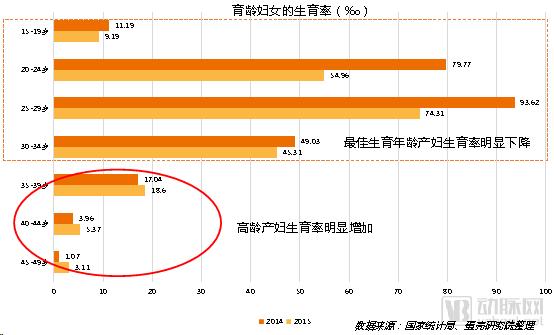

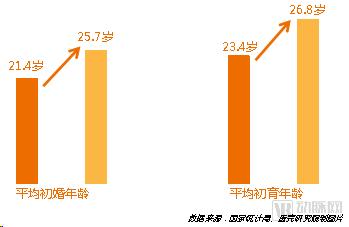

The latest data from the National Bureau of Statistics shows that from 1990 to 2017, the average age at first marriage for women of childbearing age in China was delayed by more than four years, rising from 21.4 years to 25.7 years, with a continuing upward trend; the average age at first childbirth also increased from 23.4 years to 26.8 years. Fertility rate data for women of childbearing age indicates a significant decline in fertility rates among mothers aged 15 to 34, with the most pronounced decrease observed in those aged 25 to 29, dropping from 79.77‰ to 54.96‰, a reduction of 24.81‰.

3. Assisted Reproductive Technology Is the Last Resort for Advanced Maternal Age Pregnancies

The introduction of the two-child policy has reignited the desire for another child among many families, particularly those born in the 1970s and 1980s who enjoy stable careers and higher incomes. However, due to physiological factors, it is an immutable fact that female fertility gradually declines with age after 35, making assisted reproductive technology (ART) the ultimate option for these families. Data on fertility rates among women of childbearing age show a significant increase in birth rates among older women aged 35–49, with the rate for women aged 45–49 rising by nearly 300%.

1. The full relaxation of the “two-child” policy was theoretically expected to drive population and birth rate growth. In practice, the policy dividends were effectively realized during the first three years after its official implementation, leading to a certain degree of increase in both population and birth rates. However, after 2017, the population and birth rates declined sharply again. The beneficial impact of the “two-child” policy fell short of expectations, with the number of newborns in 2018 dropping further to 15.23 million and the birth rate standing at only 10.94‰.

2. The long-term decline in newborn population and birth rate is a challenge China is currently facing; where there are challenges, there are opportunities, and assisted reproductive technology (ART) treatment is one of the most effective solutions to this issue;

3. The postponement of the age at first marriage and first childbirth has led to an expanding proportion of women missing their optimal reproductive window, thereby increasing the risk of potential infertility; this is one of the major factors contributing to the decline in the first-child birth rate.

4. The “Two-Child” Policy has, in a true sense, stimulated the growth in birth rates for families with more than two children; however, the postponement of first marriage and first childbirth has led to delayed childbearing among women, resulting in an increase in the number of advanced maternal age pregnancies.

5. Driven by the combined effects of delayed age at first marriage and first childbirth, along with the “two-child” policy, women of childbearing age are exhibiting a decline in fertility rates among those at the optimal reproductive age, alongside a substantial increase in advanced maternal age pregnancies. The industry’s growth window has emerged, poised for takeoff.

IV. International Landscape: The Global Assisted Reproductive Technology Market Awaits a New Surge

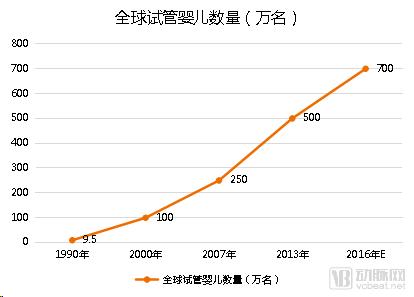

Research by the International Committee for Monitoring Assisted Reproductive Technology (ICMART) shows that from 1990 to 2013, the global number of IVF babies grew from approximately 95,000 to over 6 million, representing an overall increase of more than 6,400% and a compound annual growth rate (CAGR) of 19.8%. Although the growth rate is projected to decline to 11.9% starting in 2013 due to factors such as market saturation, the report estimates that the global number of IVF babies will still reach 7 million by the end of 2016.

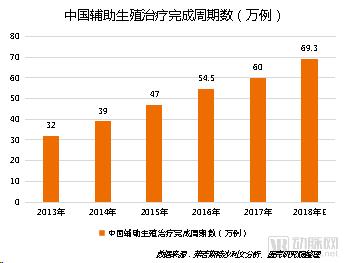

Frost & Sullivan analysis indicates that from 2013 to 2017, the number of completed assisted reproductive technology (ART) treatment cycles in China increased from 320,000 to 693,000, representing an overall growth of over 216% and a compound annual growth rate (CAGR) of 16.7%.

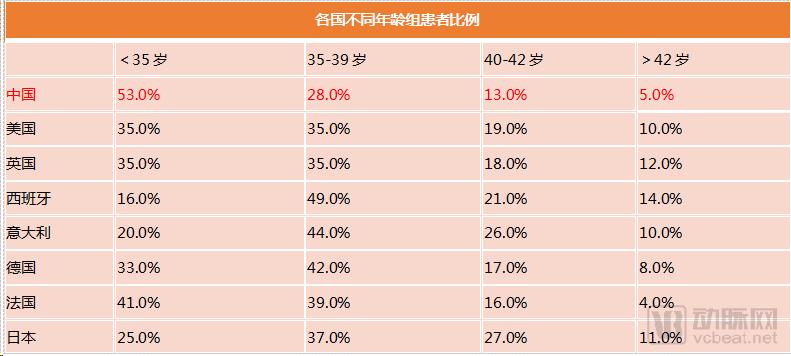

Reproductive Biology and Endocrinology compiled statistics on assisted reproductive technology (ART) patients worldwide. The data indicate that in most countries, ART patients are primarily distributed across two age groups: under 35 years and 35–39 years, with slight variations in proportions among different countries. In China, however, the patient population is predominantly concentrated in the under-35 age group, accounting for 53.0%, a proportion higher than that of other countries. Patients aged 35–39 constitute 28.0%, while those aged 42 and above represent the smallest share at 5.0%. Studies show that, based solely on 2015 data, China had a significantly larger number of infertility patients under 35 years of age compared to other developed countries, whereas the number of patients in other age groups was lower than in those countries.

1. Since 2013, China’s assisted reproductive technology (ART) industry has experienced rapid growth exceeding the average growth rate of the overall healthcare sector, indicating that the ART industry is rapidly evolving into a highly marketized and mature vertical subsector within the medical industry;

2. Based on cycle data and IVF data, China's assisted reproductive technology industry entered a new phase of rapid marketization after 2013, with its growth rate surpassing the global average;

3. The rapid development of China’s assisted reproductive technology (ART) industry is primarily attributable to the surge in market demand, the increasing maturity of ART technologies, the gradual improvement of national regulatory frameworks, and a significant increase in investment within the related industries;

4. From a consumption perspective, prior to 2015, patients under the age of 35 accounted for 53% of those with infertility, while patients aged 35 and above accounted for approximately 47%. Compared with the current demographic structure in China, where women of optimal childbearing age (under 35) make up 49.4% and women of non-optimal childbearing age (35 and above) account for 50.6%, the market penetration among consumers aged 35 and above is slightly insufficient. However, the overall alignment is relatively good, indicating that the current consumer development structure in the market is fairly healthy.

5. The analysis presented earlier in this report indicates that among women of childbearing age, fertility rates are declining for those in the optimal childbearing age group, while there is a significant increase in advanced maternal age pregnancies. In light of this trend, the current consumption structure needs to be restructured, and future patient acquisition strategies should place greater emphasis on the market for older mothers.

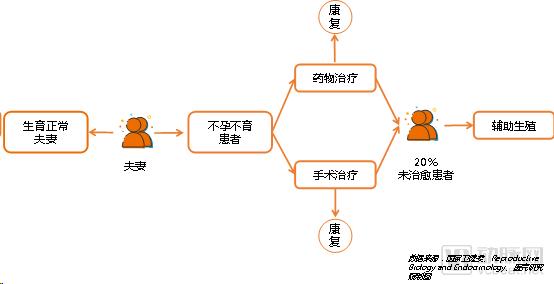

I. Three Major Treatment Pathways for Infertility: Assisted Reproductive Technology Becomes the First Choice

Based on the treatment pathways for infertility, there are currently three main approaches: conventional pharmacological therapy, surgical intervention, and assisted reproductive technology (ART). Pharmacological therapy is suitable for couples with mild conditions in whom no organic abnormalities have been identified in either partner; it primarily involves ovulation induction medications and traditional Chinese medicine (TCM) regulation. Surgical intervention is indicated when organic abnormalities are present in one or both partners, such as varicocele in males or intrauterine adhesions in females.

For infertility cases that cannot be resolved through pharmacological or surgical interventions, assisted reproductive technology (ART) is considered the ultimate treatment option. Data from the National Health Commission of China and the authoritative journal *Reproductive Biology and Endocrinology* both indicate that more than 20% of couples require ART to address their fertility issues.

Meanwhile, compared with the other two treatment approaches, assisted reproductive technology (ART) achieves an overall pregnancy rate of approximately 40%–60%, significantly higher than that of other treatments. Currently, the pregnancy rates at China’s top ART hospitals exceed 60% (for instance, the average pregnancy rate at CITIC-Xiangya Hospital reached 62.4% in 2017).

Meanwhile, the journal also compiled statistics on the proportion of reproductive specialists employing various assisted reproductive technology (ART) treatments. The results indicate that in China, the proportion of physicians utilizing assisted reproductive methods such as intrauterine insemination (IUI)/ovulation induction (OI) and ART has reached 52%, with IUI/OI accounting for 14% and ART for 38%. Thus, assisted reproduction has genuinely become the primary approach for treating infertility in China.

II. Atlas of Assisted Reproductive Technology

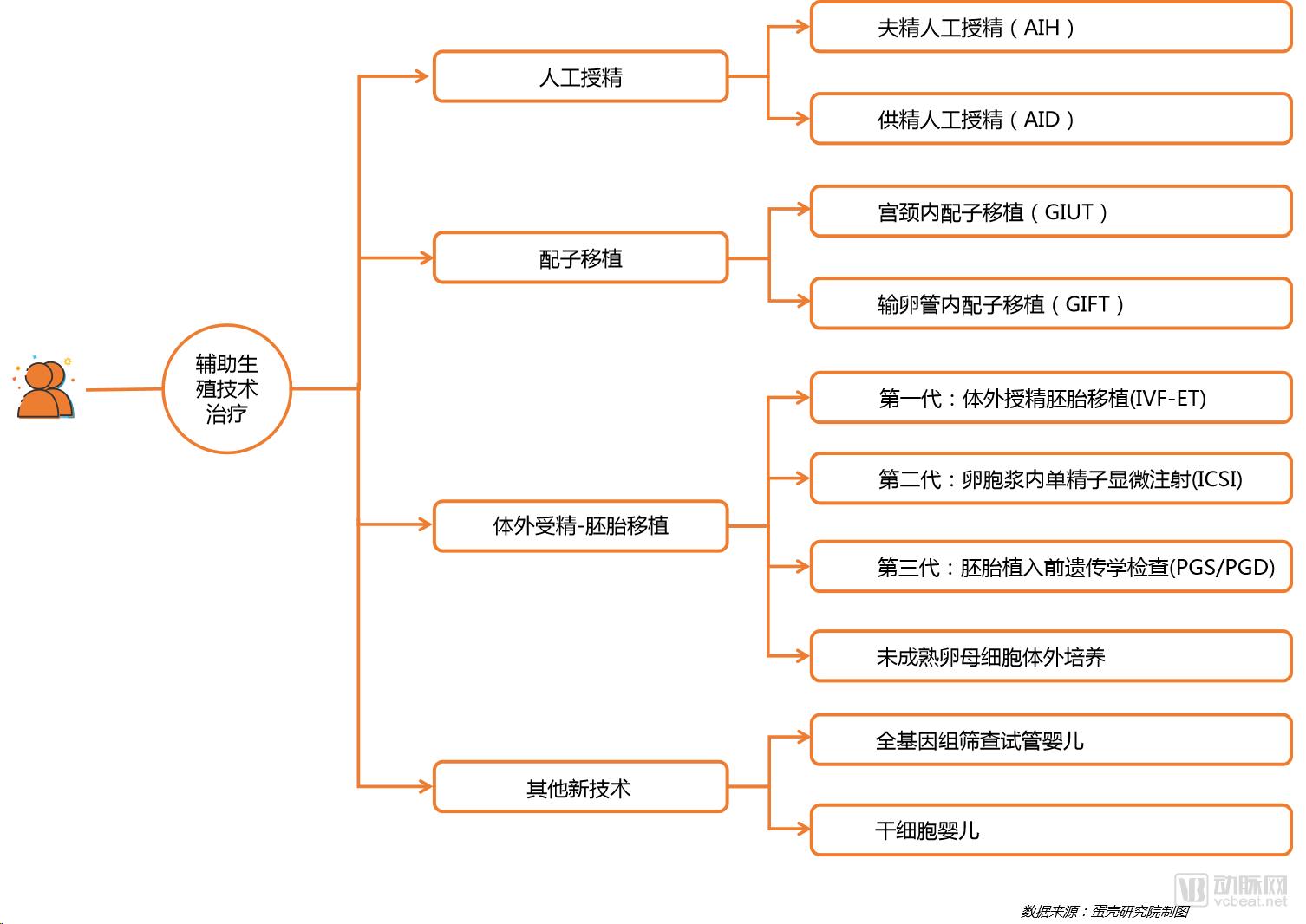

Assisted reproduction is an abbreviation for Assisted Reproductive Technology (ART), which refers to techniques that employ medical assistance to help infertile couples achieve pregnancy. Based on the level of technological advancement, these methods are primarily categorized into: artificial insemination (AI), oocyte/gamete intrafallopian transfer, in vitro fertilization-embryo transfer (IVF-ET), and other derived technologies. Additionally, there are emerging techniques still in the experimental stage, such as preimplantation genetic testing for aneuploidy (PGT-A) in IVF and “stem cell-derived embryos.”

As infertility becomes increasingly prevalent in China, the assisted reproductive technology (ART) industry has emerged as one of the fastest-growing segments within the Chinese healthcare sector. After years of development, the ART industry has established a clear division of labor, forming an industrial chain structured around “medical device/pharmaceutical supply + internet-based ART medical platforms + end-user services.” The upstream segment primarily covers medical devices, diagnostic reagents, and biopharmaceuticals; the midstream segment mainly comprises two types of enterprises: “Internet+” ART companies that provide generalized menstrual health management and specialized infertility services; while the downstream segment consists of domestic and overseas ART medical institutions and organizations offering derivative services.

I. 7.42 million in potential demand, a RMB 572 billion existing market, a RMB 26.2 billion end-user market, and an 87.3% untapped market

Driven by multiple factors such as environmental conditions, work-related stress, and dietary habits, the number of patients with infertility is expected to continue rising, leading to rapid expansion in the terminal market growth potential of the assisted reproductive technology (ART) industry. While numerous analyses exist regarding the market size of the ART sector, each employing different logical frameworks, we have cleaned and studied data from multiple sources to minimize factors that could distort market interpretation. From four distinct dimensions, we present a unique industry blueprint to reveal where the “true patient population” and “real market” of the assisted reproductive technology industry truly lie.

1. Demand is here: 7.42 million “real” demand-side users

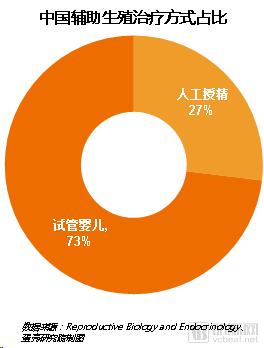

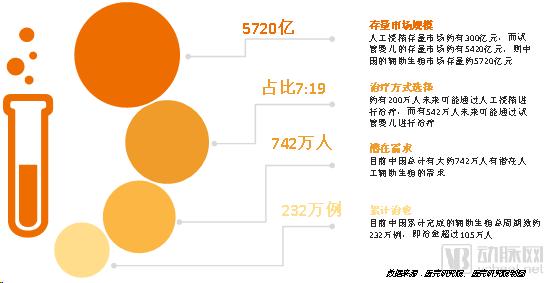

Our study shows that by the end of 2019, a cumulative total of approximately 7.7 to 9.24 million women (i.e., 20%) of childbearing age (20–49 years) in China required assisted reproductive technology (ART) for fertility treatment (with an average of 8.47 million patients used for calculation). Meanwhile, according to research published in Reproductive Biology and Endocrinology, the proportion of treatments administered by Chinese experts using intrauterine insemination (IUI) and in vitro fertilization (IVF) was 27% and 73%, respectively (a ratio of 7:19).

As of 2017, China had completed approximately 2.32 million cycles of assisted reproductive technology (ART), resulting in the successful treatment of around 1.05 million individuals. With an estimated 8.47 million people requiring ART for treatment and excluding the 1.05 million already successfully treated, there are currently approximately 7.42 million individuals in China with potential demand for artificial assisted reproduction.

1. As of 2017, China had completed a cumulative total of approximately 2.32 million assisted reproductive technology (ART) cycles, including 625,000 cycles of artificial insemination and 1.695 million cycles of in vitro fertilization (IVF). Based on an average of three treatment cycles for artificial insemination and two treatment cycles for IVF, the cumulative number of individuals successfully treated to date is approximately 1.05 million;

2. Among the 7.42 million individuals with potential needs for assisted reproductive technology (ART), approximately 2 million may undergo intrauterine insemination (IUI) treatment in the future, while 5.42 million may pursue in vitro fertilization (IVF).

2. Here is the existing stock: a “true” existing market of RMB 572 billion

Our in-depth interviews with experts reveal that IVF typically requires two cycles, with each cycle costing approximately RMB 40,000–60,000; IUI generally requires three cycles, with each cycle costing around RMB 5,000.

1. Based on average costs and using successful pregnancy as the benchmark, each cycle of artificial insemination costs RMB 5,000, with a total cost of RMB 15,000; each cycle of in vitro fertilization (IVF) costs an average of RMB 50,000, with a total cost of RMB 100,000;

2. Starting from 2017, an estimated 2 million people may undergo treatment via artificial insemination in the future, with China’s existing market for artificial insemination valued at approximately RMB 30 billion;

3. Since 2017, an estimated 5.42 million individuals may potentially undergo in vitro fertilization (IVF) treatment, resulting in a cumulative market size of approximately RMB 542 billion for IVF services in China;

4. Using 2017 as the base year and the end-user market as the benchmark, the cumulative size of China’s assisted reproductive technology (ART) market was approximately RMB 572 billion;

5. However, given the combined effects of delayed age at first marriage and first childbirth, along with the “two-child” policy, the number of advanced maternal age pregnancies is expected to increase significantly in the future. Advanced maternal age implies a substantial rise—exceeding 20%—in the number of couples who can conceive only through assisted reproductive technology (ART). Among treatment options, preference for in vitro fertilization (IVF) will increase markedly, with the proportion of patients choosing IVF exceeding a ratio of 19:7. Meanwhile, pregnancy rates among women of advanced maternal age are significantly lower than those among women of optimal childbearing age. This decline in pregnancy rates will lead to a considerable increase in the number of treatment cycles for both IVF and artificial insemination. Therefore, in reality, the total addressable market size of China’s assisted reproduction industry should be substantially higher than RMB 572 billion.

3. Growth Here: 15.5% Year-on-Year Increase, Terminal Market Size of RMB 26.24 Billion

According to Frost & Sullivan data, the total number of assisted reproductive technology (ART) cycles reached 600,000 in 2017. In 2018, the ART industry is projected to complete approximately 693,000 cycles, representing a year-on-year growth of 15.5%. Based on a ratio of 7:19 for artificial insemination to in vitro fertilization (IVF), it is estimated that 187,000 artificial insemination cycles and 506,000 IVF cycles will be performed in 2018. The total end-market size of the overall ART industry in 2018 was approximately RMB 26.24 billion.

1. Among these, there were approximately 187,000 cycles of artificial insemination (with an average cost of RMB 5,000 per cycle), resulting in a market size of approximately RMB 940 million for artificial insemination within the assisted reproductive technology industry in 2018;

2. With 506,000 IVF cycles (at an average cost of RMB 50,000 per cycle), the terminal market size for IVF is approximately RMB 25.3 billion;

3. In the end-user market of the entire assisted reproductive technology (ART) industry, in vitro fertilization (IVF) accounts for 96.4% of the total market size. Going forward, IVF will remain the core business driving the expansion of the entire industry.

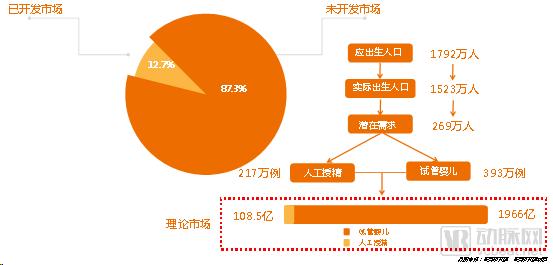

4. Theoretical market size of RMB 207.45 billion, with 87.3% of the market “awaiting” development

From the perspective of prevalence, we further deconstruct the scale of the assisted reproductive technology (ART) industry in 2018. The latest data from the National Bureau of Statistics shows that the number of live births in 2018 was 15.23 million, with a birth rate of 10.94‰, marking a further decline in both the number of births and the birth rate. Based on an infertility prevalence rate of approximately 12.5%–15%, the expected number of live births should have been 17.92 million. However, due to infertility, approximately 2.69 million infants were not born. This implies that in 2018, around 2.69 million couples with the desire to have children were unable to conceive due to infertility, representing a potential demand for ART treatment. Based on the average number of treatment cycles and associated costs, the theoretical terminal market size of the ART industry should be approximately RMB 207.45 billion, indicating that 87.3% of the potential market remains untapped.

1. Based on a 7:19 ratio of intrauterine insemination (IUI) to in vitro fertilization (IVF), among 2.69 million couples, approximately 724,000 may undergo IUI treatment, while 1.966 million may undergo IVF treatment;

2. Based on the average number of treatment cycles and associated costs, the theoretical market size for artificial insemination is 2.17 million cycles, equivalent to approximately RMB 10.85 billion; the market size for in vitro fertilization (IVF) is 3.93 million cycles, equivalent to approximately RMB 196.6 billion. Theoretically, the terminal market size of the assisted reproductive technology industry in 2018 should have been approximately RMB 207.45 billion.

3. Based on our forecast of a total market size of RMB 26.24 billion in 2018, the current level of market development stands at 12.7%.

5. Benefit Distribution Across the Entire Industry Chain

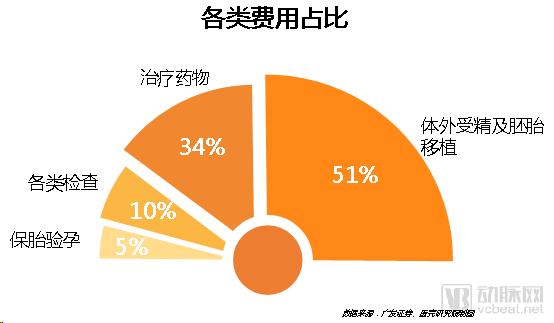

Meanwhile, within the entire assisted reproductive technology (ART) industry chain, the segments with the highest market value share are assisted reproductive pharmaceuticals in the upstream sector and ART medical institution services in the downstream sector. Industry survey data indicate that treatment costs primarily consist of four components: in vitro fertilization and embryo transfer (51%), therapeutic medications (34%), various examinations (10%), and luteal phase support and pregnancy testing (5%).

II. Domestic Support

Insights into the Current State of Assisted Reproductive Technology Institutions1. Dynamic Scan of 451 Assisted Reproductive Technology (ART) Medical Institutions

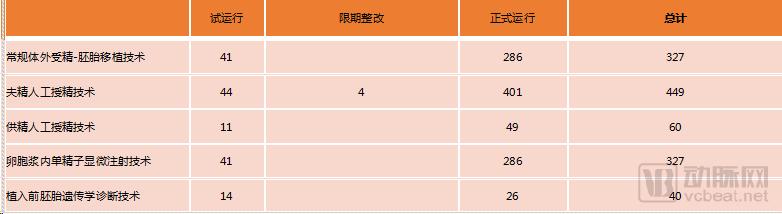

A total of 451 medical institutions have been approved to provide human assisted reproductive technology (ART) services. Excluding reproductive centers established by public hospitals, there are 41 reproductive centers affiliated with private hospitals or funded by private capital, accounting for only 9.1%. Based on the specific ART techniques each institution is authorized to perform, we have cleaned and organized all relevant data:

1. Currently, there are a total of 327 medical institutions offering conventional in vitro fertilization and embryo transfer (IVF-ET) for the treatment of infertility; among these, 286 institutions are operating formally, while the remaining 41 are in trial operation.

2. A total of 449 medical institutions provide artificial insemination with husband’s sperm (AIH) for treatment, among which 401 are in formal operation, 44 are in trial operation, and 4 are under rectification within a specified time limit;

3. A total of 60 medical institutions are authorized to provide artificial insemination with donor sperm (AID) services, among which 49 are in full operation and the remaining 11 are in trial operation;

4. A total of 327 medical institutions provide intracytoplasmic sperm injection (ICSI) for treatment, among which 286 have officially launched the technology, while the remaining 41 are in trial operation;

5. There are only 40 medical institutions offering preimplantation genetic diagnosis (PGD) technology, of which 26 are in full operation and 14 are in trial operation.

1. The vast majority of hospitals offer artificial insemination services. Among these treatment options, 99.6% of medical institutions provide husband’s sperm artificial insemination (AIH), while only 13.3% offer donor sperm artificial insemination (AID).

1. The vast majority of hospitals offer artificial insemination services. Among these treatment options, 99.6% of medical institutions provide husband’s sperm artificial insemination (AIH), while only 13.3% offer donor sperm artificial insemination (AID).

2. 72.5% of medical institutions offer first-generation (conventional in vitro fertilization and embryo transfer, IVF-ET) and second-generation (intracytoplasmic sperm injection, ICSI) assisted reproductive technologies for treatment; however, only 8.9% provide third-generation (preimplantation genetic diagnosis, PGD) IVF services. Therefore, there is substantial market potential for developing treatment services based on third-generation IVF technology.

2. List of 23 Human Sperm Banks

As of December 31, 2016, there were 23 medical institutions approved to establish human sperm banks.

In the full report“2018 Assisted Reproductive Technology Industry Research Report”In this section, we will continue to analyze the current state of China’s assisted reproductive technology (ART) industry and the “three core competitive factors” for ART medical institutions.

In Chapter 5,This report will scan the overview of the overseas assisted reproductive technology (ART) industry, with a focus on interpreting the “rise” of cross-border ART medical services and reviewing the business models of cross-border ART enterprises.

In Chapter 6,Will Make “Six Core Judgments” on the Future Development of China’s Assisted Reproductive Technology Industry

For more details, see:

"2018 Assisted Reproductive Technology Industry Research Report"

Below is the complete table of contents. The full text comprises six chapters, totaling over 36,000 words. To read the remaining chapters, please scan the QR code to become a VCBeat member and download the complete report, or purchase the report individually in the VCBeat Reports section.

Table of Contents

Chapter 1: Insight into the Assisted Reproductive Technology Industry with Unlimited Potential

I. Incidence Rate of 12.5%–15%: Identifying the “Real” Demand Side

II. Patient Profile of Infertility: The Largest Group Consists of Women with Infertility Caused by Thin Endometrium

III. Emerging Industry Opportunities: New Consumer Healthcare Choices Driven by Policy

1. The birth rate for first children continues to decline, with second and higher-order births making the largest contribution

2. The significant increase in the age of late marriage and childbearing has severely impacted fertility.

3. Assisted Reproductive Technology Is the Last Resort for Advanced Maternal Age Pregnancies

IV. The Synchronous Rise in Willingness and Ability to Pay Makes Assisted Reproductive Technology No Longer Out of Reach

V. International Landscape: The Global Assisted Reproductive Technology Market Awaits a New Wave of Explosive Growth

VI. The Industry's Woes: A Gray Market Rife with Chaos

1. The Black Market for Eggs: The Significant Dangers of “Predatory” Egg Retrieval

2. Illegal Surrogacy: The Choice Between Money and Bloodline

3. Abuse of Ovulation-Inducing Drugs: Use with Caution

Chapter 2 Development: A Brief History of the Development of Assisted Reproductive Technology

I. Three Major Treatment Pathways for Infertility: Assisted Reproductive Technology Becomes the First Choice

II. Atlas of Assisted Reproductive Technology

1. Artificial Insemination

2. Gamete Transfer

3. In Vitro Fertilization-Embryo Transfer (IVF-ET)

III. A Comprehensive Guide to the Assisted Reproductive Technology Journey: Painful Yet Joyful

Chapter 3 Deconstructing the Industry Chain of Assisted Reproductive Technology

I. Upstream Industry Chain: Medical Devices, Diagnostic Reagents, and Biopharmaceuticals

1. Medical Devices

2. Diagnostic Reagents

3. Biopharmaceuticals

II. Midstream Industry Chain: “Internet+” Assisted Reproductive Technology

III. Downstream Industry Chain: Assisted Reproductive Technology (ART) Medical Institutions and Derivative Service Providers

Chapter 4: Decoding China's Assisted Reproductive Technology Market

I. 7.42 million in potential demand, a RMB 572 billion existing market, a RMB 26.2 billion end-user market, and an 87.3% untapped market

1. The demand is here: 7.42 million “real” demand-side users

2. Here’s the existing stock: a “true” stock market worth RMB 572 billion

3. Growth Here: 15.5% Year-on-Year Increase, RMB 26.24 Billion Terminal Market Size

4. The Potential Lies Here: A Theoretical Market of RMB 207.45 Billion, with 87.3% of the Market Awaiting “Blossom”

5. Benefit Distribution Across the Entire Industry Chain

II. Strengthening Regulatory Oversight to Establish Industry Order

1. Ethics and Morality That Cannot Be Ignored

2. Market Standardization Under Policy and Legal Regulation

III. Insights into the Current State of Domestic Assisted Reproductive Technology Institutions

1. Dynamic Scan of 451 Assisted Reproductive Technology (ART) Medical Institutions

2. Directory of 23 Human Sperm Banks

3. Leading Chinese Experts in Assisted Reproductive Technology

4. China’s Top IVF Hospital Rankings

IV. The “Three Core Competitive Factors” of Assisted Reproductive Technology (ART) Medical Institutions

1. IVF License: High Value = High Industry Entry Barrier

2. IVF Technical Proficiency: High Technology = High Pregnancy Rate = High Value

3. Market Development Potential: Low Level of Development = High Development Potential

Chapter 5: Overview of the Overseas Assisted Reproductive Technology Industry

I. China’s Industry Dilemma: The “Rise” of Cross-Border Assisted Reproductive Medical Services

1. Market development level is completely mismatched with the number of institutions, resulting in unbalanced development

2. Constraints of Ethics, Morality, Law, and Policy

3. Relatively slow technological development and implementation

II. Cross-Border Assisted Reproductive Medical Services: Building a Bridge to Parenthood

1. Clear Technological Advantages: Widespread Adoption of “Third-Generation Technology”

2. High Degree of Policy Openness: Diverse Forms of Maternity Care

III. Industry Chain of Cross-Border Assisted Reproductive Technology Subsectors

IV. Overview of Business Models for Cross-Border Assisted Reproductive Technology Companies

1. Operational Model: Traditional Model or “Internet+”

2. Product Structure: Single-Product or Diversified

3. Implementation Approach: Cross-border Collaboration or Self-built Hospital

V. Global Map of Destinations for Overseas Assisted Reproductive Technology

VI. Dynamic Scanning of Hotspot Regions

1. United States

2. Singapore

3. Thailand

4. Russia

5. Japan

6. Hong Kong, China

VII. Directory of Leading Assisted Reproductive Technology Hospitals in Popular Global Regions (Partial)

Chapter 6 Setting Sail: Development Trends in the Assisted Reproductive Technology Industry

I. Real-World Implementation of Third-Generation Assisted Reproductive Technology

II. Launch of Fourth-Generation Assisted Reproductive Technology

III. The Rise of “Internet+” in Assisted Reproductive Technology: Monetizing Traffic Through Offline Services

IV. Development in Unsaturated Cities/Provinces

V. Advanced Maternal Age Becomes a New Consumer Driver

VI. Further Opening of the Cross-Border Assisted Reproductive Technology (ART) Medical Market