Global Biopharma 2018 Year in Review: Biotech Stocks Declined Overall, Success Hinged on Pipeline Assets

In February 2019, Evaluate published its annual report, “Review of the Pharmaceutical, Biotechnology, and Medical Technology Industries in 2018.” The report analyzes the ups and downs of the global pharmaceutical, biotechnology, and medical technology sectors in 2018 from a global perspective and across multiple dimensions. VCBeat New Medicine (WeChat ID: biobeat1) has compiled and translated the report. The full text is provided below:

Looking back at 2018, it is evident that this was a turbulent year for biopharmaceutical companies. In contrast, the medical technology industry remained relatively calm.

For many pharmaceutical companies, the disappointments of 2018 included stalled acquisition initiatives planned at the beginning of the year; a surge in clinical trials within the booming field of immuno-oncology, yet without significant breakthroughs; and for companies with commercialized products, mounting pressure from drug price cuts as well as the growing negative repercussions associated with high drug prices.

By the end of last year, significant macroeconomic challenges emerged, erasing the stock market gains achieved by the biotechnology sector over the first nine months. However, large pharmaceutical companies remained a safe haven, while health technology firms also successfully avoided most losses.

In 2018, the year following 2017, the number of completed acquisitions in the medical device industry also declined significantly, with private equity firms leading the transactions. The subdued M&A activity in the medtech sector has had a ripple effect on other aspects of the industry. Since the beginning of this year, the number of venture capital deals has been steadily decreasing, both in terms of financing rounds and total amounts raised. This year’s financing data reveal strong investor interest in digital health companies, a trend evidenced by their relatively rapid growth and their emergence as key acquisition targets for large corporations.

In contrast to the drug development sector, the venture capital industry experienced a banner year in 2018, investing $16.8 billion in biopharmaceutical companies worldwide. By the end of 2018, investment growth had slowed significantly, yet the private equity sector continued to grow healthily, largely driven by robust market demand for initial public offerings (IPOs).

Last year, biotech IPOs also set new records, with equity investors showing strong interest in healthcare technology companies. Interestingly, despite the broader stock market slump in the fourth quarter, transactions in the medical device sector reached an all-time high.

In 2018, the number of innovative drugs approved by the FDA set a new record. Meanwhile, the number of high-risk medical devices approved dropped significantly compared to the total in 2017, corresponding to the FDA’s repeated emphasis on strengthening regulatory oversight for such devices. However, this shortfall was partially offset by an increase in approvals of low-risk devices marketed through the de novo pathway.

The report summarizes key data on the development of biopharmaceutical and healthcare technology companies over the past year. Overall, the industry shows signs of healthy rather than weak growth. Although some benchmarks set in 2018 are difficult to surpass, companies in many sectors have laid a solid foundation for strong growth in the coming year.

Biotech stocks performed relatively steadily before September this year. As the broader market indices declined in the fourth quarter, high-risk stocks such as biotech suffered significant setbacks: the Nasdaq Biotechnology Index (NBI), closely tied to the sector, dropped by one-fifth over the past three months, making it a particularly painful year-end for investors in the industry.

The year-end recession turned NBI’s 15% gain over nine months into a 9% decline by year’s end. Large pharmaceutical companies have thus resumed their traditional role as safe havens.

Of course, everything is relative. For instance, the S&P Pharmaceuticals Index rose by only 5% for the full year—a modest gain that is nonetheless impressive, given that all other key biopharmaceutical indices were either flat or in negative territory at the end of 2018.

Moreover, although investors successfully avoided risks, macroeconomic issues also led to declines of more than 10% in both the FTSE 100 Index and the Euro Stoxx 50 Index. By the end of September, Japanese stocks had cumulatively risen by 17%, but in fact, this merely recovered from the peak decline of 18% during the stock market plunge in the fourth quarter of last year.

If any single company should bear responsibility for this, it is one of the index’s largest constituents—Takeda Pharmaceutical. Takeda’s $64 billion acquisition of Shire has made it the biggest destroyer of market value outside the ranks of major pharmaceutical companies, with its share price falling 42% this year and $20 billion wiped off its market capitalization.

On the other hand, Shire’s market capitalization rose by $6 billion as a result. Clearly, Takeda Pharmaceutical is facing a broader crisis of confidence. Meanwhile, Bayer has also suffered a severe blow due to its acquisition of Monsanto.

Celgene’s performance was disappointing. In January, Bristol-Myers Squibb acquired the large biotechnology company for $74 billion, a price 35% below Celgene’s peak valuation. This indicates that, despite the fourth-quarter decline in its stock price, the acquisition remained within the financial reach of some companies.

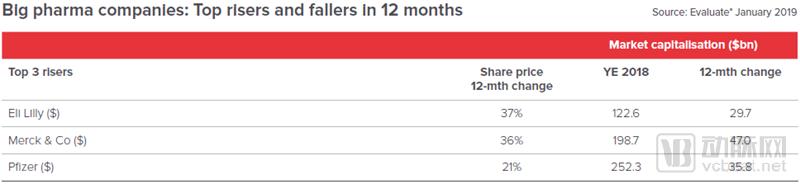

Top 3 Gainers and Losers in December Among Large Pharmaceutical Companies (Market Cap Above $25 Billion)

Among large-cap companies with declining market values, Gilead and Novo Nordisk fell 13% and 11%, respectively, this year. Amgen, buoyed by a $10 billion share repurchase program, ranked among the top three in terms of stock price gains. However, its market capitalization actually shrank by 1% in 2018.

What about the large pharmaceutical companies that serve as safe havens? Once-dismissed firms such as Lilly and Pfizer have now become the industry’s “lighthouse” companies, delivering the highest investment returns. Even GSK saw its market capitalization rise by 13% this year.

Meanwhile, the stock price movements of Merck & Co. also indicate that the company’s dominance in the field of immuno-oncology for lung cancer treatment is increasingly strengthening. This is, of course, closely related to Bristol-Myers Squibb’s acquisitions and Roche’s decline. The former was compelled to undertake a large-scale merger, while the latter’s continued decline, despite possessing high-potential growth drivers such as Ocrevus and Hemlibra, remains surprising.

Johnson & Johnson’s stock price fell 8% due to a catastrophic event last December, when a Reuters report accused the company’s consumer division of concealing the presence of asbestos in its baby powder.

As we entered 2019, the key question for these largest pharmaceutical companies was: How long can rising drug prices continue to boost corporate performance?

2018Top 3 Biopharmaceutical Giants by Market Cap Gains and Losses

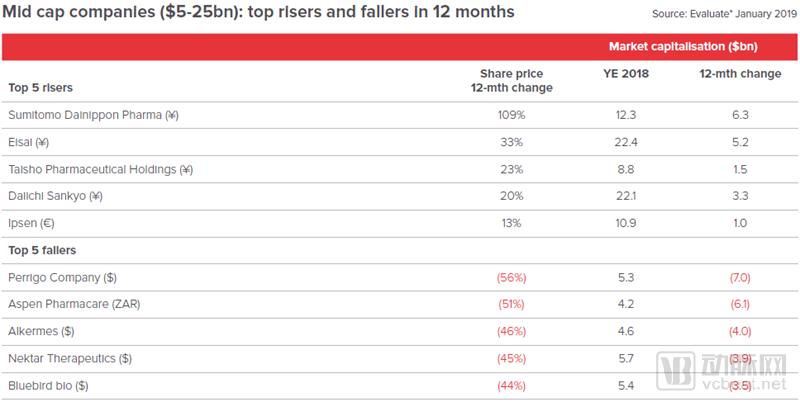

Year-end stock market volatility propelled some unexpected companies to the top of the small- and mid-cap biopharma rankings. Among them, Japan’s Sumitomo Dainippon Pharma led the pack as the mid-cap stock with the largest gain in 2018.

The resolution of the patent dispute over Latuda, a medication for depression, has pushed potential generic competition to 2023, driving up Sumitomo Dainippon Pharma’s stock price in late November. This positive development propelled the company’s shares to outperform even Eisai, which had been the top performer over the previous nine months. In 2018, despite controversies surrounding data from Eisai’s Alzheimer’s disease candidate BAN2401, recently disclosed optimistic findings from the program have also boosted Eisai’s stock price.

Among mid-cap growth companies, the only non-Japanese firm is Ipsen, which has benefited from its collaboration with Exelixis on Cabometyx (cabozantinib). There are signs that the company intends to expand its oncology pipeline and extend its business into the U.S. market.

Companies with significant share price declines typically face issues such as clinical trial failures or strategic missteps. Perrigo led the decline, becoming the mid-cap company with the largest drop in stock price due to unexpected management changes, the spin-off of business units, and a year-end tax bill from Irish authorities.

Alkermes’ depression drug ALKS 5461 has suffered repeated setbacks, with the most recent being the FDA advisory committee’s vote against approval during its November drug review. Additionally, Nektar’s stock price plummeted following the failure of its promised launch candidate, NKTR-214.

Top 5 Mid-Cap Pharmaceutical Companies (Market Cap: ~$5B–$25B) by Market Value Increase and Decrease in 2018

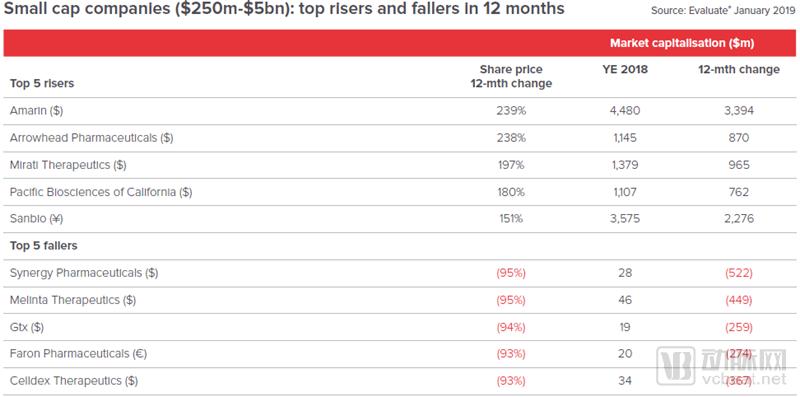

Among small pharmaceutical companies, Amarin is clearly the winner: its product Vascepa has seen unexpectedly strong sales, demonstrating significant efficacy in treating cardiovascular disease in the REDUCE-IT trial, which has added more than $3 billion to the company’s market capitalization.

Sanbio’s investigational data indicate that its stem cell therapy candidate, SB623, demonstrates favorable efficacy in patients with traumatic brain injury. The company serves as a prime example of why substantial gains in the biotechnology sector can be short-lived: the failure of a stroke trial in January erased nearly three-quarters of Sanbio’s market capitalization, making it likely to rank among the companies with the steepest market value declines in 2019.

Last year, this phenomenon also affected companies that experienced failures in clinical trials and commercialization. For instance, after the development failure of its core drug Trulance, a treatment for constipation, Synergy Pharmaceuticals went bankrupt; Faron Pharmaceuticals’ core drug Traumakine failed to demonstrate satisfactory efficacy in treating respiratory distress syndrome; and Celldex Therapeutics’ glembatumumab vedotin failed in clinical trials for triple-negative breast cancer, forcing the company to halt all R&D activities.

Top 5 Small Pharmaceutical Companies (Market Cap: $250 Million–$50 Billion) by Market Capitalization Gains and Losses in 2018

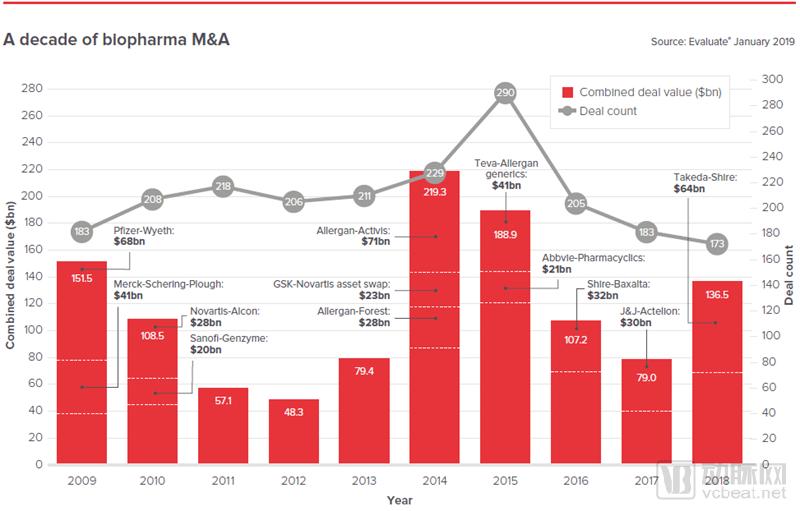

The significant acquisitions of Celgene and Loxo Oncology in the first few weeks of 2019 may have led many to forget the quiet biopharmaceutical M&A market of the previous year. Undoubtedly, the M&A market in 2018 was sluggish: even in the years following the financial crisis, the number of mergers, acquisitions, and licensing deals in the pharmaceutical industry exceeded that of 2018.

A review of historical data from EvaluatePharma reveals the extent to which M&A activity slowed in 2018. Admittedly, mega-deals can create bubbles. In 2018, Takeda’s acquisition significantly contributed to the refinement of biopharmaceutical M&A frameworks. However, transaction volume is the true indicator of M&A activity levels.

Mergers and Acquisitions in the Biopharmaceutical Sector (2009–2018)

As can be seen from the chart above, the biopharmaceutical industry entered a downturn in 2016, which is not surprising given the economic bubble of 2014 and 2015. Notably, recent M&A transactions appear to have been concentrated in the first few months of this year. The J.P. Morgan Healthcare Conference, held every January, attracts significant media attention, which may be one of the reasons for the surge in M&A activity at the beginning of the year.

Those who believe that mergers and acquisitions will once again surge in volume would do well to take heed: the past three years have seen a remarkable blossoming of M&A activity, only to be followed by a harsh market winter.

The most significant M&A news of 2018 was Takeda’s acquisition of Shire. Although it took place in the first quarter, it was not officially recognized until May.

In 2019, it was widely believed that the market capitalization of pharmaceutical companies would undergo a reassessment. However, the acquisition of Celgene, one of the most active players in biopharmaceutical M&A, by BMS had a somewhat negative impact: the biotech company had completed its two largest deals in 2018, namely the acquisitions of Juno Therapeutics and Impact Biomedicines.

There may be many other companies in the biopharmaceutical market with intentions to merge or acquire. However, a key indicator to watch is the number of M&A transactions occurring in the coming months. Only this will demonstrate whether latent demand is truly rebounding.

The Largest Mergers and Acquisitions Completed in 2018

Among last year’s investor cohort, venture capital firms delivered reasonably satisfactory performance: most of the startups they invested in were acquired.

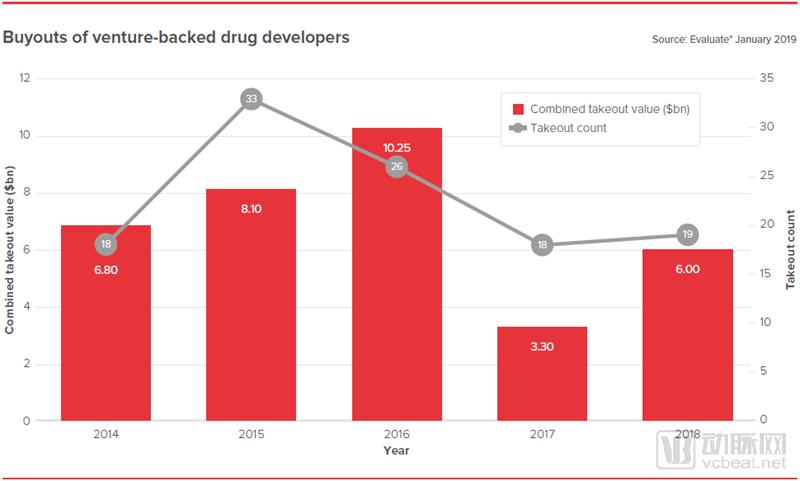

Compared with 2017, more drug development projects were acquired at higher prices in 2018, although the volume of such acquisitions remained below the peak levels seen in 2015–2016. Nevertheless, given the M&A market trends in 2018, this is still a positive development and serves to some extent as validation that venture capital firms made the right bets by pouring substantial funds into this sector.

Pharmaceutical R&D Acquisitions from 2014 to 2018

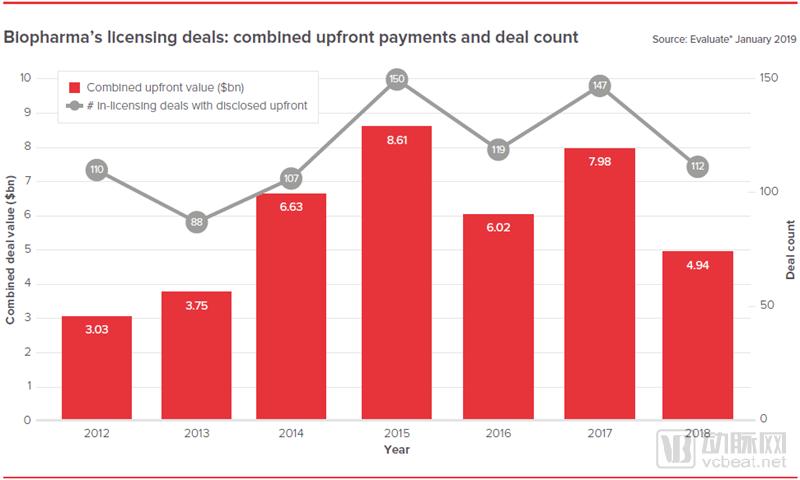

Licensing agreements are a byproduct of the M&A market and serve as a significant source of non-dilutive equity financing for small pharmaceutical companies. However, what concerns these small pharma firms and their investors is that the number of contracts dropped to a five-year low last year.

Moreover, M&A activity has declined because such transactions can lead to overvaluation of the acquirer’s assets. However, this analysis only covers licensed deals with pre-disclosed values, particularly major licensing agreements reached by biopharmaceutical companies. Such licensing transactions typically overlook the unrealized “biobucks” value and focus solely on the initial total cash consideration.

Although the trend in authorized transactions shown in the figure below largely represents the overall market, the transaction volume depicted underestimates the true level of licensing agreements reached due to the exclusion of the value of “bio-dollars.”

Licensing Deals Reached by Biopharmaceutical Companies from 2012 to 2018 (Including Upfront Payments and Number of Transactions)

The emergence of blockbuster deals will inevitably affect data trends. For example, in 2017, AstraZeneca partnered with Merck & Co. on its PARP inhibitor Lynparza, with an upfront payment of $1.6 billion—the highest since 2010. In 2018, Bristol-Myers Squibb acquired Nektar’s immuno-oncology asset NKTR-214 for $1 billion, tying with Merck & Co.’s 2014 acquisition of partial ownership of several cardiovascular projects from Bayer as the second-largest pipeline acquisition deal.

Such large-scale transactions can rapidly boost the valuation of a company’s early-stage pipeline, with oncology products often attracting substantial capital: three of the five largest upfront payments over the past decade were for cancer drugs. In 2018, upfront payments in the highly competitive biopharmaceutical sector declined compared with previous years, offering another explanation for the downturn in licensing deals.

If M&A transactions in 2019 fail to recover from the downturn as hoped, companies and investors can only pray that the marked slowdown in licensing deal volume this year is merely temporary.

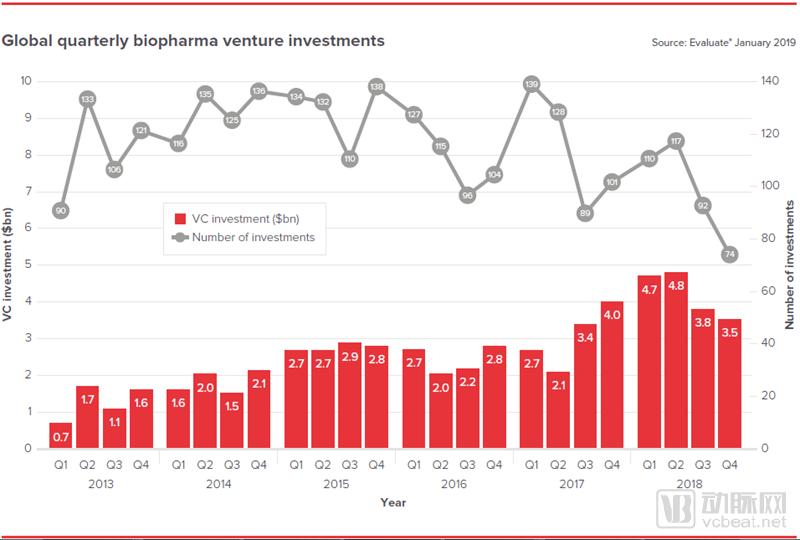

Anyone with a basic understanding of the venture capital industry can see that 2018 was a landmark year for venture capital. Driven by a surge in mega-round financings, global pharmaceutical companies secured nearly $17 billion in funding, even though the number of financing deals dropped to its lowest level in a decade.

In 2018, the venture capital sector witnessed unprecedented industry-wide investment fervor, and biopharmaceuticals were no exception. Nevertheless, many still believe that the historical trends of 2018 will not repeat in 2019, implying that the major concern for 2019 is a certain degree of economic slowdown.

EvaluatePharm’s analysis of the following pharmaceutical data includes only companies engaged in the development of therapies for human diseases—the highest-risk segment within biotechnology venture capital—and excludes subsectors such as medical technology or genomics.

Global Venture Capital Investment in the Biopharmaceutical Industry (2013–2018)

Investment activity is not expected to plummet this year. Venture capital firms still maintain ample cash reserves and are raising new capital. At least some companies have already initiated initial public offerings (IPOs), which is a positive sign for capital exit. Meanwhile, previous M&A analyses indicate that startups backed by these venture capital firms remain the primary acquisition targets for pharmaceutical companies.

However, it is not inconceivable that the volume of financing could return to the levels seen in 2015 and 2016; data indicate that financing activity during those two years remained quite substantial.

However, the recent surge in financing is unlikely to last. The stock market decline in October served as a timely reminder that the global bull market will not continue indefinitely. In light of this, investors appear to have adopted a more cautious stance, and the financing data for the first quarter of 2019 will be closely watched.

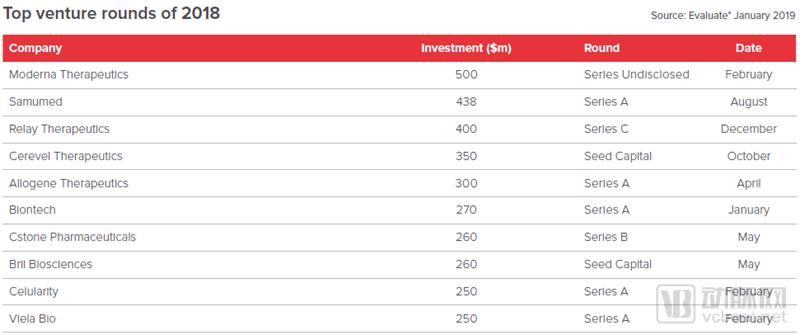

An analysis of pharmaceutical company financing in 2018 shows that 37 drug developers secured funding last year, with each raising over $100 million—more than double the figure for 2017. This indicates that investment institutions are spreading their capital across a larger number of startups, making it difficult for any single startup to secure large-scale financing. The scientific research quality of these startups remains another major unknown for 2019.

Of course, the answer to this question will take longer to unfold. In the meantime, the continued decline in Moderna’s stock price since its IPO suggests that not all investors hold sky-high expectations for privately held pharmaceutical companies.

Many believe that the excessive ease of capital access adversely affects investment quality. Perhaps in 2019, capital will return to rationality.

Top 10 Venture Capital Investments in 2018

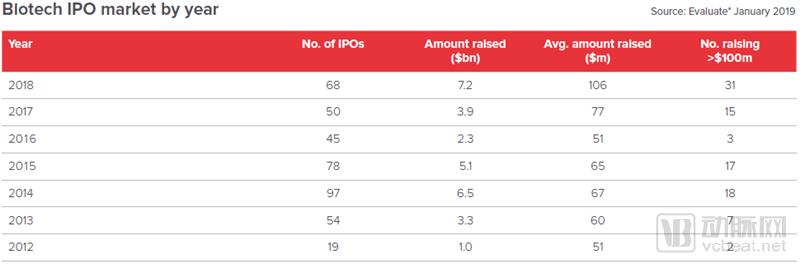

2018 was also a bumper year for biotechnology companies going public, with the active biopharmaceutical IPO market setting multiple new records: according to EvaluatePharma’s statistics on initial public offerings, newly listed companies raised a record high of $7.23 billion in total funding last year, and the average IPO size exceeded $100 million for the first time. This analysis covers all biotech firms listed on Western stock exchanges.

2012–2018 Biotech IPOs

Survey data on quarterly trends in 2018 showed little indication of the stock market turmoil that would unfold in the fourth quarter. Many believed that the October sell-off would burst the biopharmaceutical IPO bubble. Notably, Moderna and Allogene, the two largest companies to go public amid last year’s IPO frenzy, saw the bubble finally dissipate in the final months of the year.

Admittedly, the fourth quarter did experience a decline compared to previous quarters, with a few companies postponing their IPO plans due to market conditions. It is also worth noting that Moderna’s IPO accounted for one-third of the $1.8 billion raised in the fourth quarter last year; without this deal, the outlook would have appeared somewhat grim.

Moderna’s stock price has fallen sharply since its IPO last December, leaving the mRNA research company valued below the level of its last private financing round. However, it could also be argued that Moderna’s overvaluation is an isolated case rather than a broad market trend. For example, Allogene’s market capitalization has nearly doubled since its listing last October.

In fact, there is little evidence that the market cooldown has dampened investor interest in biotech IPOs. Many emerging pharmaceutical companies are preparing to go public in early 2019. Despite strict government controls, companies such as Alector and Gossamer Bio have achieved valuations exceeding $1 billion, indicating that public investors remain highly interested in the biotechnology sector.

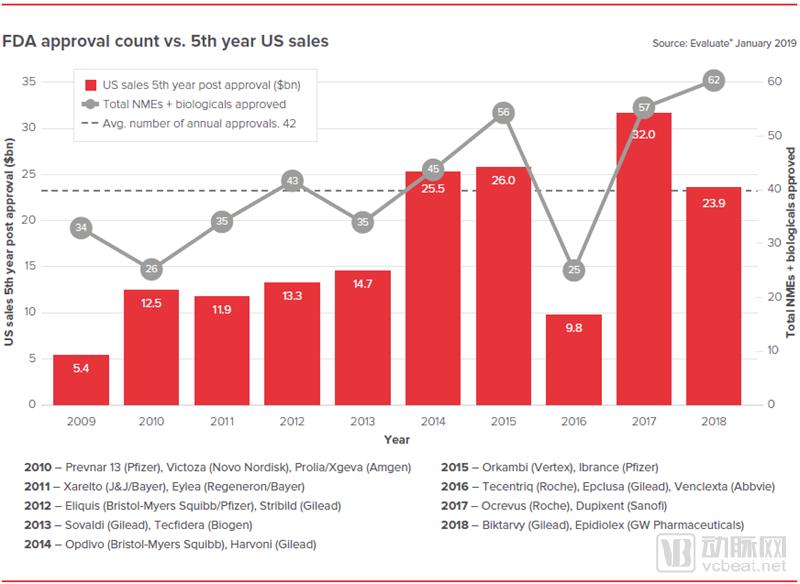

In 2018, the FDA approved 62 new drugs. Given the competitive market potential for similar products each year, this new approval record is slightly less impressive: 2017 remains the year with the highest total sales of new drugs in the past five years. Nevertheless, the market for new drugs approved in 2018 is still promising. We predict that the cumulative sales of these newly approved products will reach $24 billion by 2023, indicating that biopharmaceutical R&D remains robust.

Number and Sales of New Drugs Approved by the FDA from 2009 to 2018

According to EvaluatePharma’s forecast, the average sales of new drugs approved by the FDA in 2023 will reach $23.4 billion, equivalent to the total sales figure in 2018.

It will take some time to break the sales record set in 2017. That year saw the launch of Roche’s multiple sclerosis treatment Ocrevus and Dupixent, an autoimmune antibody developed by Sanofi and Regeneron, both of which significantly boosted full-year sales. This analysis includes all drugs approved by the FDA, encompassing both small-molecule chemical drugs and biologics.

In terms of individual approvals, the FDA approved an entire new class of migraine drugs—Aimovig, Emgality, and Ajovy—in 2018, along with 17 oncology-related drugs and the first RNA therapeutic, Onpattro.

The average approval time in 2018 decreased slightly (to approximately 10.6 months) due to a shorter average standard review cycle.

However, our analysis of these data reveals a potential and concerning trend in drug review: drugs granted Breakthrough Therapy Designation are not being approved with particular speed, and their average approval time is even longer than that of drugs granted Priority Review.

The significant slowdown in the review of highest-priority drugs may be attributed to the increase in volume: among 62 approved drugs, 31 received priority review and 13 were granted breakthrough therapy designation.

Nevertheless, the FDA’s accelerated operations have helped the biopharmaceutical industry significantly boost its productivity in recent years.

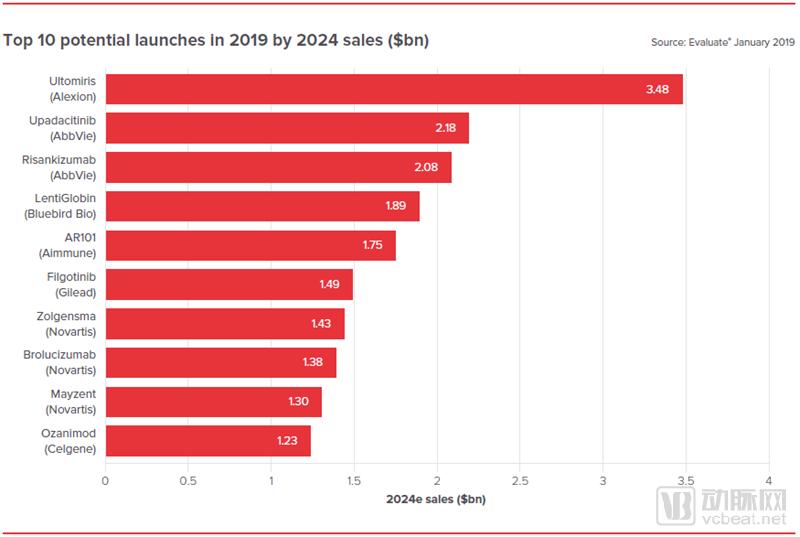

Several blockbuster drugs are awaiting review this year; in fact, the most anticipated drug of the year will be Ultomiris, another FDA-approved medication from Alexion.

Two gene therapies that merit particular attention as new drugs in 2019 are poised to deliver breakthrough advances in the treatment of previously difficult-to-cure diseases. In May, the U.S. Food and Drug Administration (FDA) will issue its final review decision on Novartis’s Zolgensma for the treatment of type 1 spinal muscular atrophy (SMA), while the European Union is scheduled to review Bluebird Bio’s Lentiglobin for the treatment of β-thalassemia in the second quarter.

If these gene therapies gain approval, the next issue will be pricing. The sales of both drugs are projected to surpass the million-dollar mark, sparking intense debate over drug pricing.

By 2019, drug affordability will remain a very real issue. Although biopharmaceutical companies are innovating and developing new treatments in areas with significant unmet needs, progress on pricing has been slow. If the healthcare industry wants consumers to accept these expensive new technologies and therapies, this situation must change.

Sales Forecast for the 10 Most Promising New Drugs (2019–2024)