2019 China Healthcare Outlook: Capital Retreat, Evolution for Survival

Editor’s Note: This article is republished from China Renaissance, authored by the Huaxing HC Team. VCBeat has been authorized to republish it.

In early spring, as usual, we provide our analysis of the trends in the five major sectors and funding landscape of China’s healthcare investment market in 2018.

In this unforgettable year of capitalization in China’s healthcare industry, as we predicted, the landscape was reshaped by the pioneers of the “Age of Discovery,” with private equity transaction volume in the new healthcare economy breaking through the unprecedented $9 billion “ceiling.” However, the journey has not been smooth sailing. In the turbulent second half of the year, the capital market faced severe headwinds, plunging abruptly into winter.

We pay tribute to investors, whose insight and patience have empowered innovation and entrepreneurship to navigate challenges and thrive; even more, we honor entrepreneurs, who fear no hardships, set sail with courage, and pioneer new frontiers in technology and markets.

In the aftermath of upheaval, a silent struggle for capital and time is unfolding. The courage and luck that defined the Age of Discovery have given way to core competencies and evolution. On one hand, enterprises are spontaneously iterating and restructuring to rejuvenate themselves; on the other, investors are banding together for warmth while scrutinizing value. As capital recedes, the market reverts to its “jungle” nature—survival through evolution, with every entity striving for self-reliance.

In 2018, China’s pharmaceutical and biotechnology sectors, driven by a combination of industrial policies, scientific research advancements, and capital market dynamics, were undergoing a rapid evolution from the 1.0 to the 2.0 era.

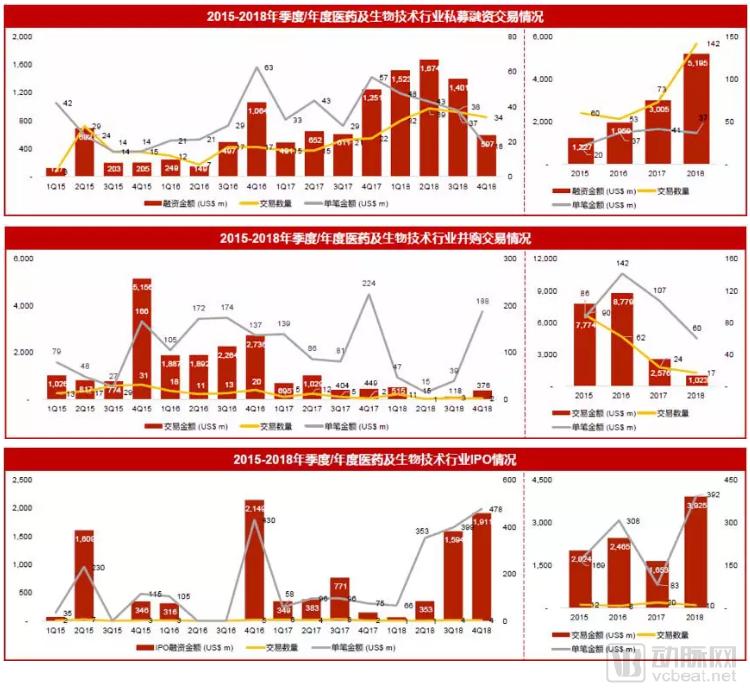

Huaxing Healthcare and Life Sciences Team summarized the transaction landscape in the pharmaceutical and biotechnology sectors in 2018:

Private equity financing boomed, with 142 transactions in 2018, nearly doubling year-on-year. The total amount raised reached nearly $5.2 billion, a year-on-year increase of approximately 73%, while the average size per transaction was about $37 million, representing a year-on-year decrease of around 10%.

There were 17 M&A transactions throughout the year, a year-on-year decrease of approximately 30%. The total transaction value was approximately $1 billion, down about 60% year on year, while the average deal size was approximately $60 million, representing a year-on-year decline of around 44%.

There were 10 IPOs, half the number recorded in 2017, yet total IPO proceeds reached $3.9 billion, a year-on-year increase of approximately 137%. The average size per IPO was around $400 million, representing a year-on-year surge of approximately 372%. Driven by the Hong Kong Stock Exchange’s new IPO regulations, BeiGene (BENE, 6160.HK) became the first Chinese biopharmaceutical company to conduct simultaneous public offerings in both the U.S. and Hong Kong markets.

At the regulatory level, 2018 witnessed an unprecedented density of policy releases in the pharmaceutical industry.

Since its inception, the National Healthcare Security Administration has firmly implemented volume-based procurement, bringing an end to the era when companies could secure easy wins simply by being the first to successfully launch generic alternatives. A series of policies have been introduced, including the acceptance of overseas clinical trial data and accelerated approval processes for imported drugs, posing significant challenges to enterprises that previously relied on profiting from the time lag between domestic and international market launches. In the field of rare diseases, new policies have emerged frequently: the release of the first national list of rare diseases, allowing dozens of rare disease drugs already marketed abroad to apply for marketing authorization without conducting additional clinical trials, and imposing a 3% value-added tax on the first batch of rare disease drugs. These new policies have prompted domestic pharmaceutical and biotechnology companies to rethink their strategies, considering what approaches they should adopt to achieve ultimate success in a rapidly changing external environment.

From a scientific and technological perspective, innate immunity has emerged as another hot area in tumor immunology. As a critical component that addresses the limitations of adaptive immunity, innate immunity plays an indispensable role. New targets such as CD47, CD40, and CSF-1 have already emerged in this field, attracting close attention from multinational pharmaceutical companies, with an imminent boom in these specialized segments expected.

In China, innovative companies such as Tianjing and Keymed Biosciences have also made early strategic moves to gain a competitive edge in the next generation of cancer immunotherapy. Bispecific antibodies and antibody-drug conjugates (ADCs) have demonstrated significant potential in clinical trials. Amgen’s BCMA/CD3 bispecific antibody challenges CAR-T therapy, showing efficacy in treating multiple myeloma with a superior safety profile. Chinese biotechnology firms such as BiMap Therapeutics, Alphamab Oncology, and Akeso, which possess core platform technologies for bispecific antibodies, are actively developing their own bispecific antibody pipelines.

The third-generation antibody-drug conjugates (ADCs) developed by Ambrx’s site-specific protein conjugation platform have demonstrated exceptional safety in early-stage clinical trials, addressing the most significant challenge plaguing ADC development. In addition, universal cell therapies are beginning to emerge, while gene therapy has achieved breakthroughs in the treatment of rare diseases.

In the capital markets, winter anxiety set in. Starting from the third quarter of 2018, both the number of private financing transactions and the total amount raised in the pharmaceutical and biotechnology industries showed a downward trend. Nevertheless, leading venture capital firms remained active during this downturn, albeit with increasingly stringent requirements for the innovative capabilities of target companies. Sequoia China made nine investments in the biopharmaceutical sector throughout the year, focusing on antibody drugs and targeted therapies, and showing a preference for overseas-returnee entrepreneurs with stronger innovation capabilities. Lilly Asia Ventures executed eight deals during the year, primarily in the pharmaceutical field, aiming to identify innovative enterprises with leadership potential.

Policies, science, and capital markets are jointly driving Chinese pharmaceutical and biotechnology companies to continuously explore their evolutionary paths. Chinese pharmaceutical enterprises, having achieved remarkable successes, are enthusiastically embracing innovation with the aim of sustaining their longstanding leadership. Hengrui Medicine invested nearly RMB 2.7 billion in R&D in 2018, accounting for approximately 15% of its revenue, making it the largest R&D spender among Chinese pharmaceutical companies. Betta Pharmaceuticals is not content with relying on a single product; it currently has 36 drug candidates in development, and its new potential blockbuster drug, ensartinib, has received priority review for its marketing application.

Innovative pharmaceutical companies that have carried an innovative DNA since their inception, such as BeiGene, I-Mab, and Biotheus, have firmly implemented the corporate development strategy of “In China, For the World,” earning strong recognition from the capital markets. In today’s environment, where the Matthew Effect is becoming increasingly pronounced, only pharmaceutical and biotechnology enterprises that continuously evolve and prioritize innovation can remain at the forefront and ultimately prevail.

2018 was a landmark year for mergers and acquisitions (M&A) in China’s medical device sector. Unlike the previous focus on IPOs as the primary exit strategy, M&A has become a key pathway for capital exits and for listed companies to expand their product portfolios.

Three major M&A deals have drawn significant attention: Blue Sail Medical’s acquisition of Biosensors International for nearly RMB 6 billion, MicroPort’s $190 million acquisition of LivaNova, and Grand Pharma’s joint acquisition with CDH Investments of Australian liver cancer treatment device manufacturer Sirtex Medical for $1.4 billion—all underscoring Chinese companies’ determination to expand into the global market.

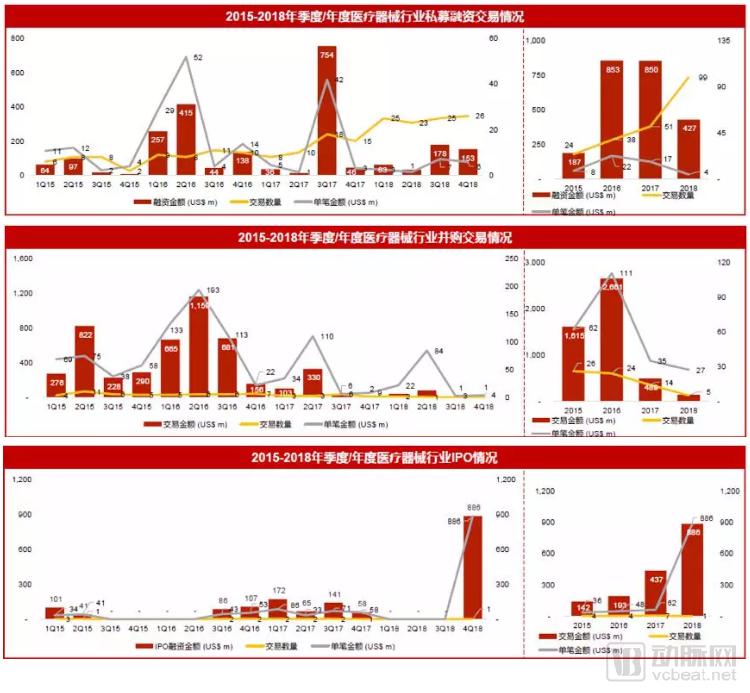

Huaxing Medical and Life Sciences Team summarized the transaction activities in the medical device industry in 2018:

In 2018, there were 99 private equity financing transactions, representing a nearly two-fold year-on-year increase. The total amount raised was approximately $430 million, a year-on-year decrease of about 50%. The average size per transaction was around $4 million, marking a significant year-on-year decline.

A total of five M&A transactions were completed throughout the year, with a total transaction value of approximately USD 136 million and an average deal size of approximately USD 27 million, both showing a downward trend compared to 2017.

There was one IPO. Mindray Medical completed an IPO in the fourth quarter of 2018, raising nearly USD 900 million.

The tightening of A-share listing standards, along with institutional changes such as the “Two-Invoice System,” transparent bidding, and medical insurance price caps, has slowed the growth rate of the medical device industry. Moreover, since 2014, the time and financial costs associated with new product registration have risen significantly, raising the barriers to entry and exit for medical device companies. This has compelled Chinese startups to naturally follow the path taken by their counterparts in Europe, the United States, and Israel—where acquisitions, mergers, and incubation of adjacent product lines have become essential acceleration strategies that entrepreneurs and investor shareholders must consider. Some funds also seek rapid expansion through acquiring new product lines to build corporate platforms; however, with companies already at high valuations, it has proven difficult to align the interests of buyers and sellers.

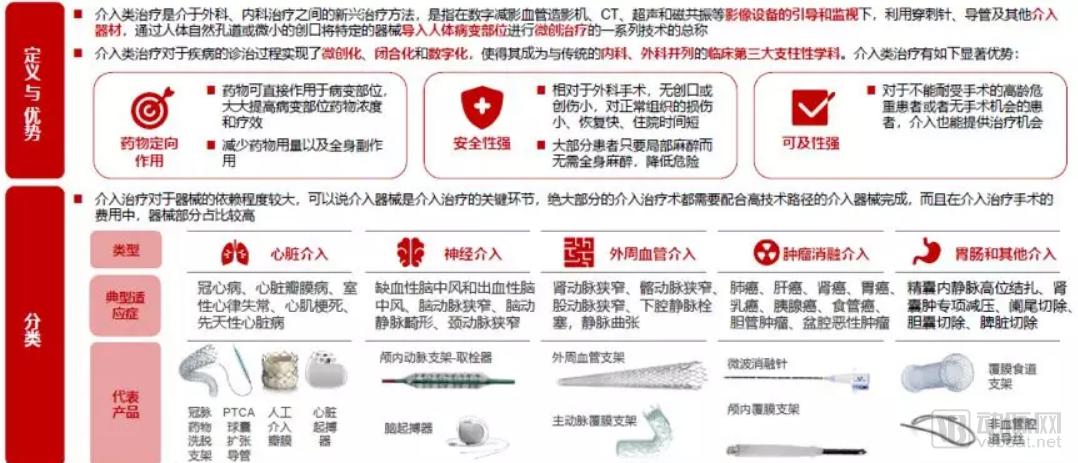

From a sub-sector perspective, cardiovascular and interventional high-value consumables remain the most attractive area for investors. This sector already boasts numerous successful listed companies, including MicroPort (Shanghai), LifeTech Scientific (Shenzhen), Weigao Group (Shandong), and Lepu Medical. While attracting top-tier talent, the field has also seen the emergence of many experienced startups. Among them, Venus Medtech secured $100 million in strategic financing, signaling the countdown to its IPO. In 2018, a cohort of promising startups—including Jinshi, Nuonuo Medical, GuiChuang Medical (Hangzhou), Xinmai, Innolife, Jian Shi Technology, Dingke, Batai, and Nuomai—also garnered favor from private equity and venture capital (PE/VC) firms.

Moreover, minimally invasive surgery was among the earlier sectors to embrace the trend of “domestic substitution for imports.” In addition to the increasingly mature stapler market, ultrasonic scalpels and surgical robotics companies (such as Baihui Weikang, Timi, Tinavi, and Huazhi Minimally Invasive) attracted significant capital attention in 2018. Recently, Johnson & Johnson Medical announced its acquisition of Auris for $3.4 billion in cash, thereby entering the surgical robotics field. This move further demonstrates that robotics and automation represent the future direction of development. It also presents an opportunity for surgical device manufacturers to overtake competitors by challenging the market dominance of Intuitive Surgical’s da Vinci surgical robot system.

Mindray Medical completed its initial public offering (IPO) on the ChiNext board in the fourth quarter of 2018, raising nearly RMB 6 billion and setting a record for the largest IPO in the history of ChiNext. This milestone propelled it to become a medical device enterprise with a market capitalization exceeding RMB 100 billion. As a China-based company listed overseas, whose international sales accounted for half of its total revenue in 2016, Mindray’s return to the A-share market may enable another surge in growth, fueled by enhanced access to capital.

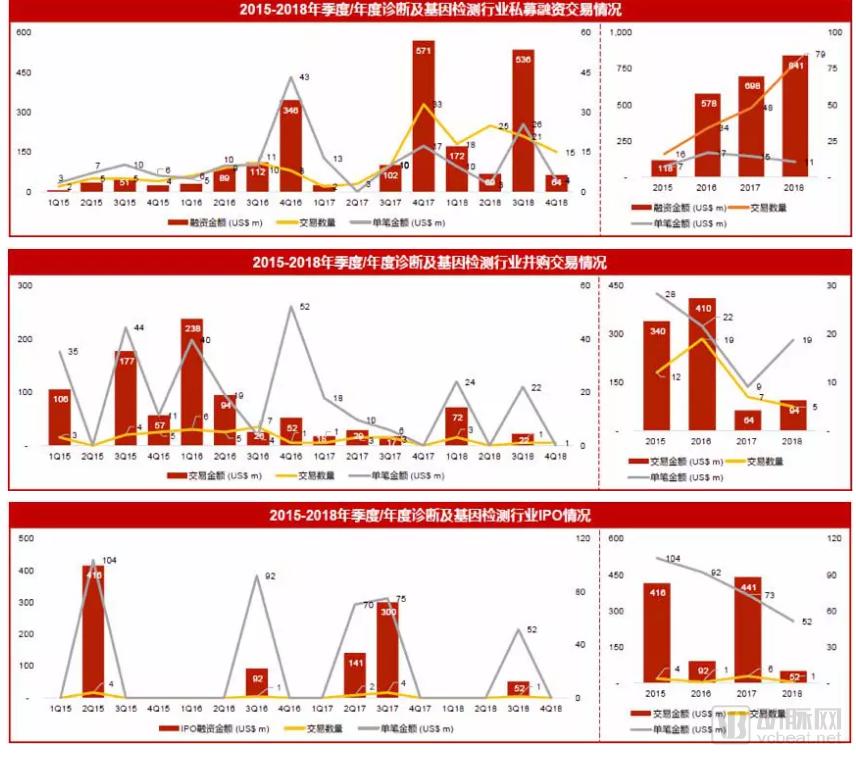

Huaxing Medical and Life Sciences Team summarized the transaction landscape of the diagnostics and genetic testing industry in 2018:

In 2018, there were a total of 79 private equity financing transactions, representing a year-on-year increase of approximately 65%. The total amount raised was approximately US$840 million, up by about 20% year on year, while the average size per financing round was approximately US$11 million, down by about 27% year on year.

A total of 5 M&A transactions were completed throughout the year, representing a slight year-on-year decline. The total transaction value amounted to nearly $100 million, an increase of approximately 47% year on year, while the average deal size was about $19 million, up by roughly 100% year on year.

Regarding the IPO, Mingde Biology completed its initial public offering in the third quarter of 2018, raising approximately USD 52 million.

Amid the “capital winter,” the overall trend among investment institutions is evident: they are exercising greater caution in their investments and imposing higher standards on the quality of target companies. In terms of specific sectors, testing services for tumor companion diagnostics (targeted therapy and immunotherapy) remain a key focus of investment, while emerging areas such as early cancer screening and consumer-grade genomics are also gaining favor with capital.

Tumor Companion Diagnostics

The next three years will be a critical period for the development of companies in the tumor companion diagnostics sector. Amid an overall tightening of financing, these enterprises face dual pressures: they must continue to make substantial market investments to remain competitive, while also allocating significant capital to the regulatory submission and approval processes for diagnostic kits as the market moves toward greater compliance and standardization under stricter oversight. Consequently, the efficiency and speed of fundraising will determine the survival or failure of these companies.

Following the substantial capital inflow into this sector in recent years, investment institutions have developed heightened expectations for higher revenues, or even profitability, from such enterprises. Consequently, these companies are under urgent pressure to diversify their revenue streams, transitioning away from a reliance on expanding sales teams toward a direct-to-patient charging model.

Collaboration with pharmaceutical companies is a key factor in diversifying and stabilizing revenue streams. Such collaborations include supporting patient screening and enrollment for clinical trials, as well as developing companion diagnostic products for drugs. Consequently, the right to partner with pharmaceutical firms will naturally become a focal point of competition among companies in the future. While expanding externally, companies must also strengthen their internal capabilities by improving the quality of their testing products and services, rather than solely focusing on cost reduction. Rigorous quality control and ensuring data reliability are not only responsible practices toward patients but also essential safeguards for the long-term, healthy development of the company.

Another urgent industry challenge is how to integrate patient genomic data with clinical diagnosis and treatment data. Currently, companies only possess patients’ tumor genotypic data, while phenotypic data—including basic patient information, medical history, diagnosis and treatment records, and follow-up information—resides within hospitals. Only by combining patients’ clinical and follow-up data with genomic data can the true value of tumor companion diagnostics be realized, enabling an assessment of whether patients genuinely benefit from testing and treatment, and making the discovery of new therapeutic regimens possible. How to achieve bidirectional data flow and what cooperation models to adopt remain areas for industry exploration. For instance, there is potential for collaboration between tumor companion diagnostic companies and electronic medical record (EMR) system vendors, as well as questions regarding how data sharing can create synergies that strengthen both parties’ businesses.

Early Screening and Diagnosis of Tumors

The field of early cancer screening and diagnosis remains a vast “blue ocean,” targeting a much larger population of relatively healthy individuals, with a market size several times that of the companion diagnostics market for cancer. For certain cancer types where early detection and intervention can significantly improve patient prognosis—such as lung cancer, colorectal cancer, breast cancer, cervical cancer, and liver cancer—early screening and diagnostic products have clear application prospects.

Multiple technical pathways exist for early screening and diagnosis, including imaging, as well as blood, bodily fluids, exfoliated cells, and even breath analysis. Based on the sampling setting, these methods can be categorized into those performed at healthcare institutions and those conducted at home.

We believe that to determine whether an early screening product can succeed, there must first be a clear medical scenario where existing technologies fail to meet clinical needs. Equally important is the balance between the product’s detection markers and its cost-effectiveness, while ease of sampling serves as an added advantage.

Leading domestic companies in this sector include Boercheng and ClearBlaze Biotech, some of whose early screening and diagnostic products have already obtained registration certificates from the National Medical Products Administration (NMPA). In the future, we will see an increasing number of products from early screening and diagnostic companies entering clinical trials to demonstrate their clinical efficacy and commercial value.

Consumer-Grade Genomics

Another area garnering increasing attention is the consumer-grade genomics sector. Leading international players include 23andMe and Ancestry.com. In addition to providing “entertainment”-oriented information such as ancestry, genetic testing services targeted at the general public are increasingly penetrating into the medical field. For instance, certain 23andMe products approved by the U.S. Food and Drug Administration (FDA) can report genetic variants associated with pathogenicity or susceptibility to specific diseases. In China, representative companies in this space include 23Mofang, WeGene, and Jellyfish Genomics. Although market penetration of their products remains low domestically, we anticipate rapid industry growth over the next few years, driven by rising demand for health management among Chinese consumers, deeper market education, and the trend of domestic manufacturers transitioning toward the development of clinical-grade applications.

Certainly, the industry still urgently needs to address quality control issues in testing and data analysis, as well as the challenge of integrating genotypic and phenotypic data. Only by resolving these two key issues can we truly obtain high-quality, application-worthy genetic “big data,” thereby unlocking its monetization potential and ensuring the industry’s long-term development.

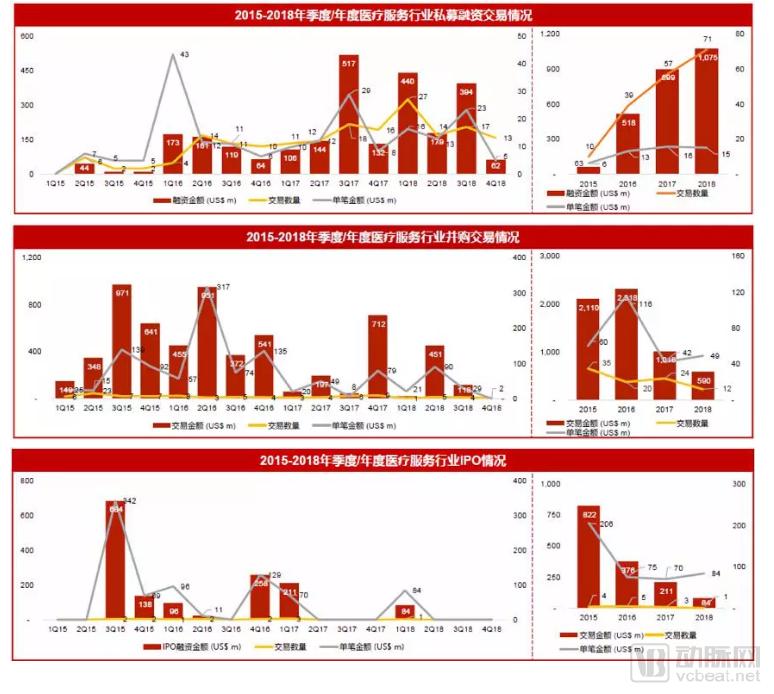

Huaxing Healthcare and Life Sciences Team summarized the transaction activities in the healthcare services industry in 2018:

In 2018, there were a total of 71 private equity financing transactions, representing a year-on-year increase of approximately 25%. The total financing amount reached approximately US$1 billion, a year-on-year increase of about 20%, while the average size per financing round was approximately US$15 million, remaining largely flat compared to the previous year.

There were 12 M&A transactions throughout the year, a 50% year-on-year decrease. The total transaction value amounted to nearly $600 million, representing a year-on-year decline of approximately 42%. The average transaction size was around $49 million, showing a slight year-on-year increase.

The Chinese healthcare services industry faces several significant challenges: first, there is a shortage of physicians relative to demand; second, the financial burden on the medical insurance system is increasing year by year; and third, integration with the capital market remains fraught with difficulties. Nevertheless, the vast and growing market demand continues to attract numerous stakeholders to enter the industry, aiming to deliver better healthcare service products to society through capital investment, business model innovation, and technological advancements.

In 2018, the National Healthcare Security Administration was officially established, enabling more effective direct regulation of pharmaceutical pricing and medical practices.

Regulators have been strengthening oversight of hospital operations, strictly controlling the use of medical insurance funds and ensuring compliance in procurement processes to improve the efficiency of fund utilization. Meanwhile, in early 2019, the assessment requirement for the drug-to-revenue ratio in tertiary public hospitals was abolished, replaced by indicators evaluating prescription rationality and the quality and safety of patient medication, thereby enabling more refined management of pharmaceutical expenditures.

In the capital markets, we are witnessing a landscape of exploration. Throughout 2018, not a single company in the healthcare services sector successfully listed on the A-share market. Mergers and acquisitions of hospitals by A-share listed companies appear to have subsided, while valuations of healthcare services companies listed in Hong Kong have also been gradually declining.

At the same time, we have also seen foreign private equity firms such as General Atlantic and KKR actively investing in or acquiring domestic hospitals; specialized medical institutions like Malo Clinic, United LiGe, and Boner Orthopedics have further secured additional investments from investors.

Healthcare services constitute a long-term business, making quick profits unlikely; meanwhile, hospitals require substantial upfront investment and indeed need capital support. However, established hospital brands wield profound influence and generate stable cash flows, while specialties related to aging populations and consumer healthcare boast broad future prospects. How healthcare service enterprises can collaborate with capital for mutual benefit remains to be seen, and we look forward to industry participants setting successful examples.

Furthermore, we have witnessed continuous efforts to integrate online platforms with offline hospitals. iKang Healthcare Group successfully completed its delisting from the New York Stock Exchange and brought in Alibaba as a strategic investor. JD.com has achieved systematic integration between its services, offline hospitals, and the urban medical insurance system in Suqian.

Internet companies represented by them value offline institutions as traffic entry points, high-value in-hospital data, and the ability to provide more tangible services to online users. Meanwhile, offline hospitals are also attempting to establish online platforms and better integrate in-hospital data, aiming to gain a deeper understanding of diseases, improve efficiency, and strengthen post-consultation patient engagement.

Visionary industry players envision a healthcare landscape characterized by shifting patient care-seeking behaviors, the deep integration of internet and big data technologies, and significantly enhanced service efficiency and quality. We believe this future will be realized in the near term.

By leveraging advanced Internet of Things (IoT) technology, smart healthcare enables interaction among medical institutions, healthcare professionals, medical devices, and patients, progressively achieving informatization. As new technologies such as Artificial Intelligence (AI) and sensing technologies continue to be integrated, the healthcare industry will move toward genuine intelligence. From a commercial application perspective, the healthcare industry has become one of the sectors where AI can achieve practical technological implementation. The Healthcare and Life Sciences Team at China Renaissance is currently focusing on niche areas within the smart healthcare industry, including AI applications in healthcare and healthcare big data.

Huaxing Medical and Life Sciences Team compiled and analyzed transaction data from the smart healthcare industry in 2018:

In 2018, there were 66 private equity financing transactions in China’s smart healthcare sector, representing a year-on-year increase of approximately 113%. The total financing amount reached nearly USD 1.5 billion, up by about 260% year on year, with the average financing amount per transaction standing at approximately USD 22 million, a year-on-year increase of around 70%.

Looking at the financing situation in the overseas smart healthcare industry, there were a total of 75 financing deals throughout 2018, with a total financing amount of approximately $2.2 billion and an average deal size of nearly $30 million.

Overall transaction data shows an upward trend in the number of transactions, total financing amount, and average financing amount per deal.

The Chinese government is continuously promoting the innovative development of medical AI technologies. In recent times, we have witnessed a series of latest industry developments, including the preliminary establishment of specialized databases for conditions such as fundus diseases and pulmonary nodules, the approval of numerous medical AI products as Class II medical devices by the National Medical Products Administration (NMPA), and the imminent rollout of the regulatory approval pathway for Class III medical devices.

From the corporate perspective, in order to obtain approval as quickly as possible, many companies have submitted their products for review to both the NMPA and the FDA. Among them, Lepu Medical’s AI-based automatic ECG analysis and diagnostic system has received FDA clearance, making it the first ECG AI product from China to be approved by the FDA.

Currently, domestic medical AI products are primarily focused on medical imaging. The most significant challenges remain commercial implementation (including effective integration with hospital information systems and unclear payers), the lack of unified industry standards, and insufficient industry talent.

Some companies are already exploring alternative commercialization models that do not require regulatory certification, such as providing data to pharmaceutical manufacturers and collaborating with health examination institutions. We have found that leading domestic medical AI companies in China, including Infervision, Deepwise, and Huiyi Huiying, which entered the market through medical imaging, possess strong fundraising capabilities and have each completed two to three rounds of private equity financing over the past two years.

However, in fields such as new drug development and hospital management, the application of AI remains largely unexplored. Companies like Silicon Therapeutics, which leverage industry-leading quantum supercomputing platform technology to develop previously undruggable targets, possess significant technical barriers. In their case, AI serves merely as a minor auxiliary component within their broader technological platform. Consequently, achieving revolutionary breakthroughs with AI technology in the field of new drug development still has a long and arduous road ahead.

At present, the primary monetization pathway for AI-driven pharmaceutical companies is to deliberately design high-quality molecular structures and sell drug leads to large pharmaceutical firms. Currently, the industry is driven by three major forces: (1) the maturation of scientific advances such as free energy perturbation (FEP) and water thermodynamics, complemented by the surge in computational power enabled by GPUs and FPGAs since 2010; (2) the continuous enrichment of data reserves on target structures and protein allostery; and (3) breakthroughs in new therapies and drug design approaches, including innate immunity, allosteric binding, and agonists. Over the next decade, an opportunity window will exist for high-quality emerging pharmaceutical enterprises leveraging computer simulation, AI, and other technologies, allowing them to benefit from the cyclical dividends of the pharmaceutical industry.

From the perspective of clinical applications, medical imaging will be the first field to achieve AI technology translation and initial commercialization. As industry standards continue to improve, AI products with good stability, high precision, high safety, and ease of use will better empower clinical endpoints.

Furthermore, we believe that medical AI will continue to expand into new application areas and business models, generating substantial industrial value in fields such as health insurance cost containment, tiered diagnosis and treatment, and medical big data management.

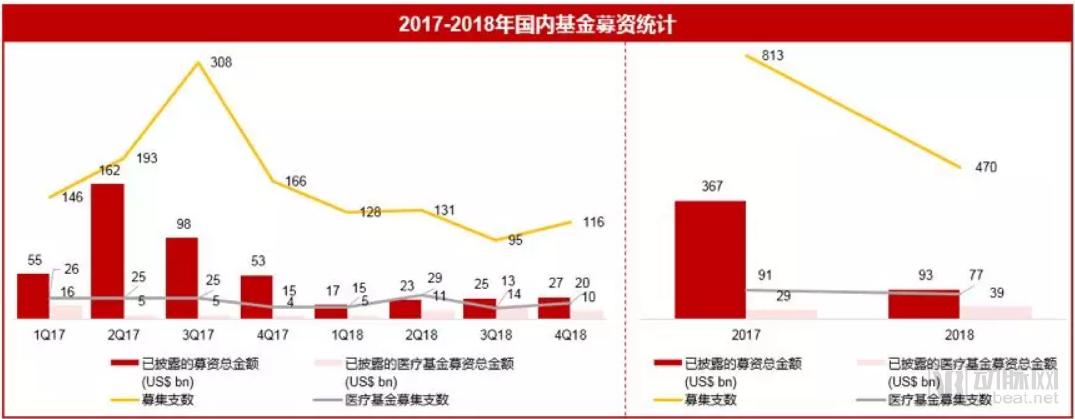

Based solely on the data, global fund fundraising volume experienced a precipitous decline in 2018, while the number of newly raised funds dropped by nearly half:

However, fundraising by professional healthcare institutions saw a significant increase (with the amount raised growing by approximately 24%). Meanwhile, some upstream major capital flows moved into well-known comprehensive funds, which allocated resources to the healthcare sector to balance investment risks in other areas. In terms of private equity financing and IPOs, transaction volumes continued to grow. Larger single-ticket financings occurred more frequently in the pharmaceutical and biotechnology sectors. Not only did the number of transactions double, but the financing scale also increased by about 73% year-on-year, a trend consistent with that of 2017. We believe that the optimistic data for 2018 represents a continuation of the surge in healthcare industry investments seen during 2016–2017.

In the second half of 2018, influenced by the China-US trade war and the macroeconomic environment, both domestic and overseas secondary markets weakened. Pricing expectations for sectors such as innovative drugs and healthcare services became more conservative in the secondary markets, causing upstream capital and investment institutions focused on the healthcare sector to adopt a wait-and-see approach. This cautious sentiment is expected to persist through the first half of 2019, inevitably leading to a situation where investors show strong interest but make few actual investments.

Following a minor surge in healthcare investment between 2017 and 2018, 2019 will be a year of cooling and consolidation for investors as they wait for new opportunities to emerge. Investment firms urgently need to evolve their strategies and underlying logic to navigate the volatile and complex international landscape as well as ongoing industry transformations. This shift also places higher demands on fund managers’ professional judgment and their ability to accurately assess value.

Investors and entrepreneurs need to reexamine the coexistence between the two:

(1) In the aftermath of the investment frenzy, investors have placed greater emphasis on value reversion and risk awareness; blindly pursuing acquisition targets at high valuations may yield relatively limited returns upon exit.

(2) Investments made over the past 2–3 years have inevitably created an asset backlog, leaving companies still in their ramp-up phase facing pressure for subsequent financing and difficulties in exit strategies;

(3) Weakness in the secondary market has led to an inversion of valuations between the primary and secondary markets, raising concerns that “the flour is more expensive than the bread.”

Evidently, investing in the healthcare sector requires a certain degree of patience, as asset holding periods are relatively long. Consequently, capital tends to favor two types of investment models: either high-quality early-stage growth targets with the potential for higher returns, or mature enterprises in the mid-to-late stages that demonstrate strong monetization capabilities and have clear expectations for an initial public offering (IPO). As capital concentrates around top-tier fund managers and star enterprises, investors must conduct more in-depth and distinctive research into niche industries and target assets. Only by identifying high-quality teams and pipelines early can investors secure returns with higher premiums.

Some capital has already considered shifting allocations toward the secondary market for private investments in public equity (PIPE). Meanwhile, new funds have emerged in the market willing to acquire low-cost legacy shares and asset packages from the primary market, offering a new avenue for fund exits and “lifeline” extensions.

John Carreyrou’s investigative report on Theranos, Bad Blood: Secrets and Lies in a Silicon Valley Startup, was published in May 2018, turning the once-celebrated Silicon Valley darling into an infamous figure. Four months later, a domino effect triggered by developments on the Nasdaq drove down the global biopharmaceutical market, which plummeted to its trough by the end of 2018.

However, it gradually became clear that the pervasive chill we faced stemmed more from waning confidence triggered by deleveraging, the China-U.S. trade dispute, and a series of new pharmaceutical policies, which in turn led to a comprehensive contraction in investment.

Let’s take a guess at some minor trends in healthcare investment in 2019:

1. Niche positioning determines industry influence. Biopharmaceutical companies that achieve successful IPOs early, possess ample R&D capabilities and financial reserves, or ideally both, will secure a favorable position in international cooperation and transactions, thereby expanding their competitive advantage. Meanwhile, the investment potential in innovative models such as “license-in” is being compressed.

2. Restructuring of Valuation Systems: Companies That Previously Raised Capital at High Valuations Will Face Financing Difficulties. This may present a valuable opportunity for management and existing shareholders to overcome anti-dilution barriers, return to rational valuations, and pursue long-term development. Meanwhile, seizing the industry consolidation opportunities brought about by volume-based procurement (VBP) and strategically divesting at reasonable prices could offer another viable path to help shareholders exit their positions.

3. In an ecological environment with limited capital supply, the competitive landscape of 2018 is unlikely to be replicated. Growth-stage enterprises will increasingly concentrate in several niche sectors to compete for financing opportunities, leading to renewed homogenization and making it difficult to break the “Nash equilibrium.”

4. As mainstream institutions have largely completed their portfolio allocations, professional expertise has deepened, and investment granularity has become increasingly refined. The greater the homogenization, the stronger the demand for differentiation. Unique early-stage startups are poised to become the “new favorites” in healthcare investment; however, due to barriers in technological understanding and high-risk characteristics, this domain will inevitably remain the preserve of a select few professional players. Should these companies achieve steady growth, they are highly likely to emerge as new leaders spearheading the rise of China’s healthcare sector.

“Investment trends shift every 12–18 months, while companies undergo iteration every 36 months”—the cyclical patterns of China’s healthcare investment market are beginning to take shape. Regardless of how investment trends evolve, HuaXing Capital aims for its annual outlook not only to clarify the logic behind market shifts and outline the direction of emerging opportunities, but also to share insights with the industry and accompany entrepreneurs through their iterative growth.

Over the past year, China Renaissance has facilitated and completed the Hong Kong listings of BeiGene and WuXi AppTec, secured a $220 million private placement financing for I-Mab Biopharma, and established a strategic development collaboration between Zai Lab and Novocure, among other achievements. In 2019, we look forward to evolving and innovating together with you.