The Next Decade of Explosive Growth: Remote Orthodontics and Digital Dentistry Innovation in China

Contributing Author: Huang Jianan holds a bachelor’s degree in Pharmacy from Zhejiang University and has participated in mergers, acquisitions, and investments at a globally leading dental company.

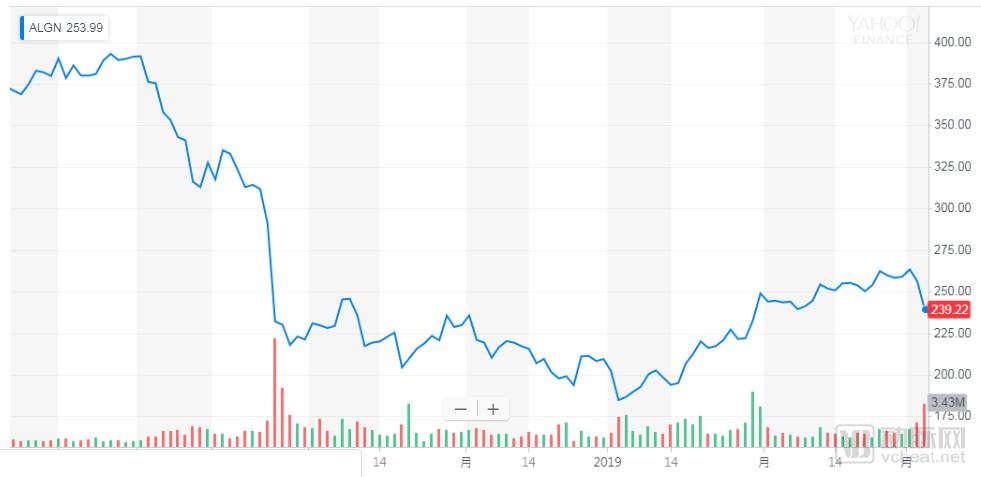

In early March, Align Technology was forced to shut down all of its offline Invisalign stores due to an unfavorable position in its litigation with SmileDirectClub. As the pioneer of clear aligner orthodontics and the world’s third-largest dental company by market capitalization, Align Technology’s stock price has gradually declined amid its dispute with SmileDirectClub. This development has once again brought SmileDirectClub and the teledentistry orthodontic model it represents into the spotlight.

Align Technology’s Stock Price Over the Past Six Months, Source: Yahoo Finance

SmileDirectClub is an innovative U.S. company that advocates the concept of remote orthodontics. The company aims to connect licensed dentists or orthodontists with patients seeking dental alignment correction through remote dental diagnosis, enabling them to prescribe and supervise treatment. This was reported in articles last year (See also: After Four Years in Remote Dentistry, Valuation Reaches $3.2 Billion—Is This How the Industry Can Be Played?) has already been introduced.

However, there has been a lack of analysis regarding three core issues concerning SmileDirectClub: (1) its core technological barriers, (2) the essence of its business model, and (3) the competitive landscape of the industry. Furthermore, can we gain insights into the next decade of innovation in dentistry, particularly in orthodontics, through the case of SmileDirectClub? These are the key questions this article aims to present to readers.

Teledentistry is not a new topic. Initially, teledentistry was primarily developed to address healthcare challenges in remote and underserved areas. This has been implemented in Australia, a vast and sparsely populated country (Sabesan, 2014), as well as in France (Petcu et al., 2016). A book titled Teledentistry (Springer, 2015) is dedicated to this subject, and articles on tele-orthodontics frequently appear in the Journal of Telemedicine and Telecare.

The emergence of SmileDirectClub and other teledontic orthodontics companies has, most significantly, steered the application of teledentistry in a new direction. Due to the persistent inefficiencies plaguing traditional healthcare, highly commercialized dental and ophthalmic sectors have begun actively seeking solutions. The essence of teledentistry lies in saving time to varying degrees. However, teledentistry comprises numerous sub-processes, and no single company has yet achieved a fully remote end-to-end workflow; nevertheless, all have made concerted efforts to reduce time burdens for patients.

Global Leaders in Teledentistry on Optimizing Orthodontic Treatment

As a key component of the dental industry, orthodontics consists of three critical stages: intraoral scanning, aligner printing, and clinical treatment. Technological innovations in these three stages are all centered on time efficiency: adopting faster 3D dental printing technologies (e.g., Stratasys, Shining 3D), enabling remote matching and communication between dentists and patients (e.g., Uniform Teeth, Orthly), and providing rapid “chairside” diagnosis and treatment solutions (e.g., Phitax, HeyGears).

Technological Evolution Across Orthodontic Environments

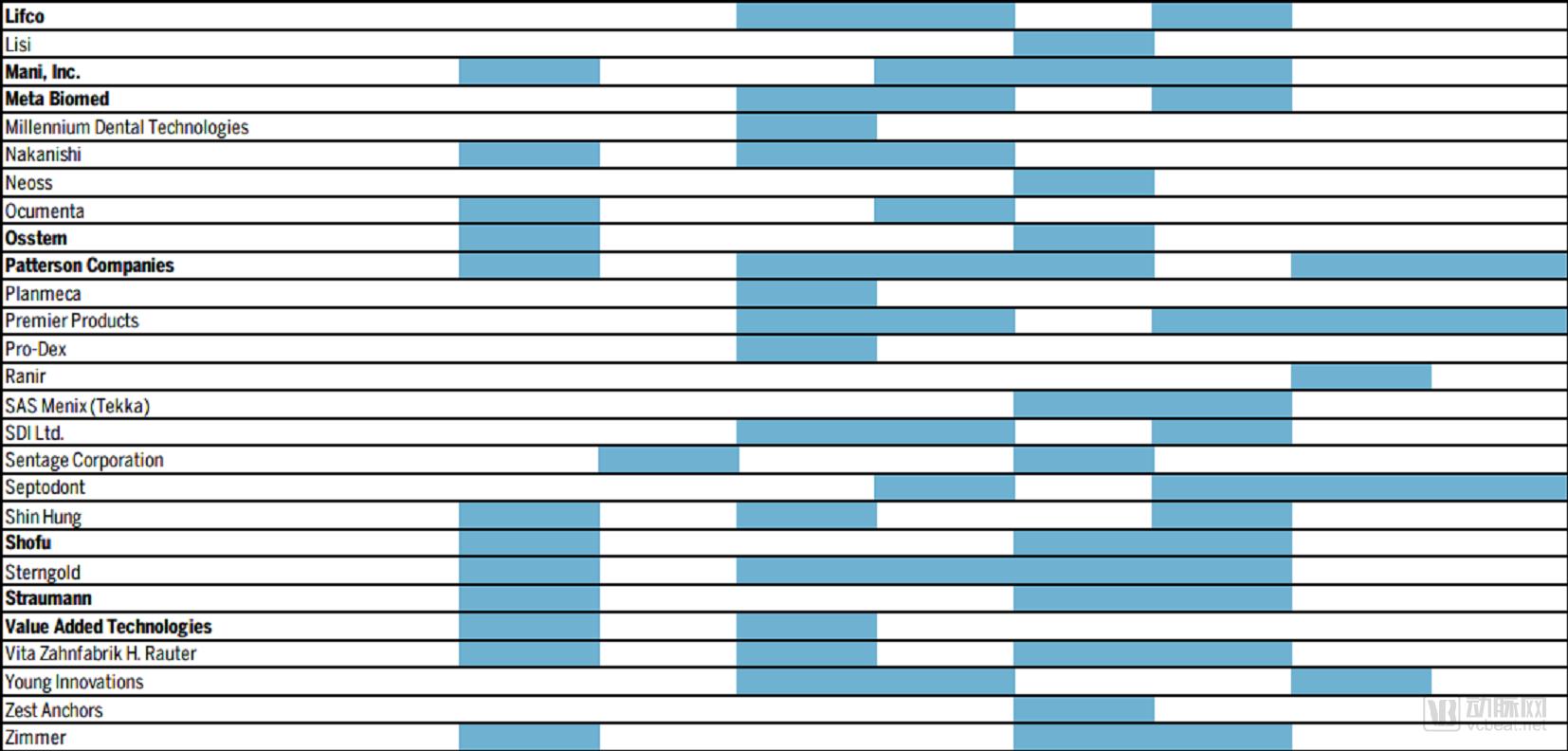

Remote orthodontics demands a high degree of coordination and comprehensive innovation across scanning, 3D printing, and treatment processes. This particularly necessitates the integration of new digital technologies—a capability often lacking among traditional dental industry giants. Currently, the major dental players we frequently refer to are primarily focused on dental medical services in China, while their counterparts abroad concentrate mainly on dental medical devices. Even upon further segmentation, virtually no single company covers all sub-segments of the dental medical device industry.

The table above outlines the coverage landscape of the dental medical device subsector, sourced from Brocair Partners.

As indicated by the chart above, a fully closed-loop business model appears unsuitable for most dental device companies. Consequently, in the realm of orthodontic solutions, most multinational giants choose to collaborate with other companies in one or two of the three key stages: aligners, scanning, and printing. This trend is even more pronounced among Chinese companies; for instance, 3Shape serves as the oral scanning partner for the vast majority of orthodontic solution providers.

Orthodontic Solutions Providers: In-House Development vs. Compatibility Choices Across Business Segments

However, not every component is compatible. For instance, in the diagram above, the aligners are all independently developed by their respective companies. This aspect is even more critical for remote orthodontics, as the remote nature of the service often introduces new and distinct challenges. In traditional orthodontics, for example, the primary focus for tooth-aligning appliances is precision. Major players in dental orthodontics, such as Straumann, ClearCorrect, Align, and Specialty Appliances, almost uniformly use thermoformed polycarbonate materials, according to their FDA-registered product information.

Comparison of Aligner Performance Among Leading Orthodontic Companies

However, for remote orthodontics, because aligners must be shipped via courier, attention must be paid to various properties such as water absorption (a longstanding issue that can now be addressed with a three-layer film design), toughness, resilience, and chemical resistance. Official information from Smilie Xiaoshu in China indicates that its aligners utilize a patent for attachment-free aligner design developed in Taiwan, containing acrylic and ethylene vinyl acetate; however, the specific efficacy is not elaborated upon. SmileDirectClub in the United States does not place significant emphasis on these aspects; instead, it highlights that the vinyl polysiloxane (VPS) used in its Impression Kit can effectively mitigate the impact of temperature fluctuations during transportation.

In the preceding discussion, we began with aligner technology—the segment with the highest rate of independent R&D across various stages of remote orthodontics—and offered some insights from a micro perspective. However, from a macro standpoint, why has remote dentistry emerged? What particular significance does it hold, especially in the Chinese market? By screening publicly available investment and financing databases in China, we can obtain a list of investment and financing activities in the Chinese dental equipment (and informatization) sector over the past two years (2017–2018):

Investment and Financing Events in China’s Dental Instrument (and Informatics) Sector (2017–2018)

An analysis of this list reveals that nearly all companies involved in financing are related to digital dentistry. The macro trend driving this shift is the slowing growth of the medical device sector across global emerging markets, including China. According to statistics from the NYU Stern School of Business, the changes in EV/EBIT multiples for medical devices in global emerging markets are as follows:

15.70 in 2011

18.55 in 2012

20.43 in 2013

25.82 in 2014

32.11 in 2015

28.73 in 2016

Although the EV/EBIT multiples for medical device companies in global emerging markets have declined since peaking in 2015, market sentiment remains bullish toward the intersection of IT and healthcare. Based on a screening of market report summaries from Giiresearch, the four fastest-growing subsectors within the global oral health industry are as follows:

1. Intraoral Scanning (Market Size: $189M, Growth Rate: +11.94%);

2. 3D Dentistry (Market Size: $903M, Growth Rate: +10.24%);

3. Oral Imaging (Market Size ~$2,000M, Growth Rate +8.38%);

4. Dental CAD/Computer-Aided Design (Market Size ~$450M, Growth Rate +8.10%).

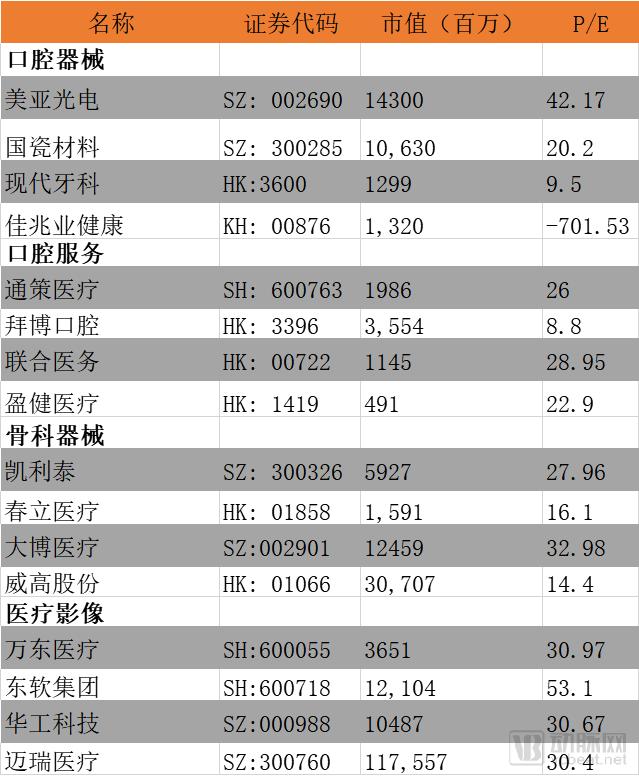

These four areas are almost all related to digital dentistry. A similar phenomenon is also evident in China’s secondary market: the average P/E ratio of medical imaging companies is approximately 50% higher than that of traditional medical device companies.

P/E Ratios of Chinese Medical Device Companies (as of End-2018)

The internal driver propelling the oral care device industry to embrace the Internet is its substantial profit margin: The application of digital technologies has enabled emerging dental giants like Align Technology to achieve gross margins of 75.98%, approaching those of the innovative drug industry. By contrast, Dentsply Sirona and Danaher (Dental Platform), the two leading companies in traditional dental manufacturing, have consistently maintained gross margins around 55%.

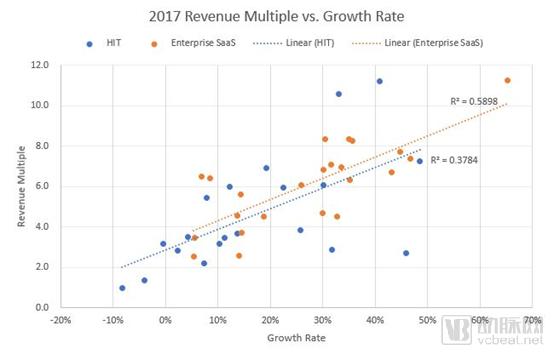

Yet, will embracing digitalization while drifting away from clinical technology define the next decade in dentistry? We can examine the valuation trends of healthcare IT companies to gain insights into the prospects of digital dentistry. According to statistics from Healthcare Growth Partners, the revenue multiple used to value healthcare IT firms decreased by 10%, from 4x in 2016 to 3.6x in 2017. This indicates that despite having equivalent revenue-generating capabilities, these companies are receiving diminishing market recognition. Furthermore, among companies with identical growth rates, healthcare IT firms typically command lower revenue multiples than the average for SaaS enterprises.

Trends in Revenue Multiples for Valuing Healthcare IT (HIT) Companies

These data indirectly reflect the waning enthusiasm for digital healthcare overseas. In the United States, in particular, startups represented by Sonendo’s root canal treatment technology have witnessed a gradual resurgence of clinical technologies in dental innovation. As for China, while we should not arbitrarily assume that the trend toward digital innovation in the dental industry will weaken, there are good reasons to be optimistic about a more diversified innovation landscape—one that is not limited to digital dentistry as seen in the past two years.

Note: The data cited in this article are current as of the end of 2018 or the date of publication. The views expressed herein represent solely those of the author.