Insurance Sector Startups Secure Repeated Funding: Investors Reveal Key Success Factors

In the previous two articles (An In-Depth Analysis of Innovation in the Health Insurance Sector: Unicorns Will Emerge from These Directions,Understanding the Health Insurance TPA Landscape: From Service Outsourcing Providers to Drivers of Industry Innovation), we systematically introduce the innovative opportunities and startups emerging in the insurance and payment sectors, such as insurance product innovation, channel expansion, insurtech enablement, and third-party services.

Many companies in these sectors are startups, making capital support indispensable. In this article, we focus on investment and financing trends in the insurance and payment industries. We conducted interviews with five investors to gain insights into their perspectives on the insurance and payment tracks. More importantly, we uncovered their “investment secrets” in the insurance sector, providing a vivid analysis of emerging entrepreneurial opportunities by examining specific investment cases.

The relationship between innovative enterprises and investment institutions is akin to that between a swift steed and Bo Le, the legendary judge of horses. High-quality projects always share consistent keywords: cross-disciplinary integration, passion, and focus, while discerning investors possess the keen eye to recognize such potential. Of course, unlike the sequential dynamic between the steed and Bo Le, the venture capital relationship is not strictly ordered; outstanding investment institutions are highly likely to identify high-potential projects, and excellent innovative ventures will likewise secure institutional support that offers sustained companionship.

From the VCBeat (WeChat ID: vcbeat) knowledge base, we extracted venture capital events related to insurance and payment. The extraction criteria were based on the “attributes” of the funded companies: they must be health insurance companies (e.g., with names containing terms such as “insurance” or “payment”), or have health insurance as a significant component of their core business (e.g., Ping An Good Doctor, WeDoctor). As a result, we obtained the following table:

Table 1: Overview of Insurance-Related Projects Invested in by Prominent Domestic Capital Groups (Partial)

Data Source: VCBeat Knowledge Base

*Due to the large number of projects, not all could be fully displayed. Additionally, owing to time constraints in database construction, project coverage is incomplete, and the classification of certain companies’ business activities involves a degree of subjectivity. This information is provided for reference only.

We recorded a total of 96 venture capital events in the medical insurance sector, involving 40 investment institutions and 33 companies. Of course, these figures do not capture the full picture of financing and investment in the medical insurance industry, but they offer a glimpse into the broader landscape.

First, we observed a pronounced “enrichment” effect in investment and financing within the health insurance industry, whereby the majority of capital was siphoned off by leading and well-known enterprises. Companies such as Ping An Good Doctor, Ping An Health Technology, ZhongAn Online, WeDoctor, and Xinmei Mutual Life Insurance secured substantial—indeed, astronomical—levels of funding, both in their early stages and in later phases of development.

Companies operating in areas such as online insurance channel platforms, insurance brokerage services, and TPA (Third-Party Administration) typically secure relatively small financing amounts, yet their numbers are substantial. This phenomenon can be attributed to the operational requirements of the insurance industry: companies requiring insurance licenses face high registered capital thresholds and significant upfront costs, necessitating large-scale capital injection, whereas service-oriented companies are not subject to such requirements.

Secondly, investment institutions prefer to make continuous investments in insurance projects, meaning they participate in multiple financing rounds of a given project. For instance, Tencent Industrial Win-Win Fund and Fosun Group’s capital arm participated in WeDoctor Group’s Series C, D, and E funding rounds; Meituan Dianping followed up its investment from the seed round of Shuidi Mutual Aid through to post-Series A; and IDG Capital and DT Capital supported Qingsongchou throughout its Series A, B, C, and D rounds. Such long-term, steadfast investment strategies are uncommon in other segments of the healthcare industry.

Furthermore, the synergy of “capital + business” implies that investment and financing in the health insurance industry place greater emphasis on industrial background, focusing on the introduction of industrial resources and synergy across the upstream and downstream value chains. The most representative examples are Ping An Good Doctor and Ping An Health Technology, both incubated by Ping An Group, which demonstrate multi-party collaboration between the group and its incubated enterprises. Additionally, ZhongAn Insurance, jointly invested in by the “Three Mas,” also exemplifies business interactions with its strategic investors.

Finally, it is worth noting that, whether in terms of establishment date, funding rounds, or financing scale, most projects remain in the early stages, with the exception of a few companies boasting “prominent backgrounds.” This indicates that the industry’s growth potential continues to be viewed favorably.

Tian Min, Partner at Yuanjing Capital

Ms. Tian Min joined Yuanjing Capital in early 2017, focusing on areas such as digital healthcare and consumption upgrades. Her lead investments include Yiyong Health, Yitong Health, Drug Research Club, Yunhu Technology, and Yaoli. She holds an MBA from the UCLA Anderson School of Management and previously served as Vice President at GGV Capital, where her investment portfolio included Ruibao Pediatrics, Meinian Onehealth, and Malo Clinic.

Regarding China’s healthcare security landscape, Tian Min pointed out that the current system is dominated by social medical insurance, which boasts extensive coverage in terms of both geographic reach and demographic structure. In contrast, commercial health insurance has a low penetration rate and primarily consists of high-end products. Amid increasing operational pressures on the basic medical insurance scheme, the government has proposed the goal of building a multi-tiered and diversified healthcare security system, encouraging the development of commercial insurance—a move that will significantly benefit the expansion of the commercial insurance sector.

In terms of innovation directions in the field of commercial medical insurance, there are three main aspects: the first is the development of new products, specifically differentiated commercial medical insurance products based on high-quality medical data. In particular, collaboration with healthcare institutions is promising, as the reform of health insurance payment methods (such as DRGs) necessitates a transformation of hospitals’ previously extensive financial management practices, thereby creating opportunities for the efficient utilization of hospital data.

Second, it is necessary to create new sales scenarios for commercial medical insurance and explore new channels. Traditional distribution channels for commercial medical insurance rely primarily on agents, particularly those affiliated with life insurance divisions. However, because commission rates for life insurance are significantly higher than those for health and medical insurance, agents lack incentive to actively promote medical insurance products. While internet-based channels have contributed some incremental growth, their e-commerce-driven logic makes them resemble consumer goods platforms rather than insurance providers, rendering them unsuitable for selling complex insurance products.

Future opportunities lie in integrating with specific scenarios, such as hospital and pharmacy channels, to stimulate consumer demand. Meanwhile, group insurance business is also a key growth area. In the United States, commercial health insurance is predominantly offered through group plans. In China, insurers can target corporate clients by focusing on supplemental employee insurance and employee health management solutions.

Third, commercial health insurance services must keep pace, such as by building medical service networks and establishing direct/fast claim settlement systems. This will enhance the consumer experience of health insurance and promote customer stickiness. Additionally, the "insurance + incentives" model, which encourages healthy lifestyles and physical activity, can not only increase customer engagement but also create opportunities for in-depth development.

Yuanjing Capital’s key investment in the commercial health insurance sector is Yi Yong Health. In early 2017, Yuanjing Capital led the Series A financing round for Yi Yong Health and also participated in its RMB 50 million Series B financing round completed in August 2018. Founded in 2013, Yi Yong Health entered the market as a third-party administrator (TPA) for health insurance. On one hand, it assists insurance companies with precise cost control and product innovation; on the other, it connects with high-quality hospitals to enhance medical services. This service-driven approach effectively aligns the needs of users, hospitals, and insurance companies.

Tian Min told VCBeat that the optimism toward YiYong Health is mainly based on the following reasons: Founder Zheng Yong has a senior industry background, with many years of experience in the medical insurance industry and involvement in several projects, giving him abundant industry resources. More importantly, YiYong Health introduced a mature cost-control system already validated in the U.S. market and carried out localization efforts, which have proven effective.

Yiyong Health has launched a provincial-level commercial insurance settlement platform in Henan Province. Patients can be admitted to hospitals connected to the commercial insurance direct billing settlement platform without paying a deposit. Upon discharge, the medical insurance and commercial insurance adjudication systems operate synchronously, allowing patients to leave the hospital after paying only the out-of-pocket expenses not covered by medical or commercial insurance.

This model creates a closed-loop insurance service, enabling YiYong Health to stand out from the traditional TPA models characterized by price wars and labor-intensive competition. The direct-billing medical network model was previously seen only in high-end medical insurance; YiYong Health is the first to apply this model to mid-tier medical insurance, gaining a certain first-mover advantage. After successful regional validation, the model can be gradually replicated across China.

Zhao Yang, Managing Partner at Weilai Capital

Weilai Capital is a “young” investment firm established in 2018, with By-Health as its primary limited partner (LP). Zhao Yang told VCBeat that By-Health has long been active in the insurance sector, serving as one of the founding sponsors of Trust Mutual Life. Public records also show that Trust Mutual Life included Ant Financial, Tianhong Asset Management, By-Health, and Newland Digital Technology among the investors in its RMB 1 billion angel financing round completed in June 2016.

With this foundation, Weilai Capital has naturally prioritized the insurance and payment sectors, conducting extensive research and analysis. Weilai Capital believes that the most significant future changes in the insurance and payment fields will revolve around traffic entry points, sales scenarios, and the integration of medical services and health products.

Zhao Yang explained to VCBeat that, compared with markets dominated by commercial health insurance such as the United States, China’s health insurance market still has substantial room for growth. According to a research report by Minsheng Securities, conservative estimates project that the premium volume of health insurance will reach RMB 997.2 billion to RMB 1.4103 trillion in 2022, with compound annual growth rates (CAGR) of 17.8%–26.3%. However, actual data show that the CAGR of gross written premiums for health insurance in China from 2012 to 2018 was approximately 35%, exceeding the projected growth rate.

Zhao Yang believes that the primary task for China’s health insurance industry at present is to “scale up volume,” which aligns precisely with the three key themes of traffic, scenarios, and services. In terms of specific pathways, the first step is to accurately identify needs and acquire customers quickly and efficiently. In this regard, internet-based insurance and the development of insurance products tailored for individuals with pre-existing conditions represent highly promising initiatives.

Next is the exploration of new insurance scenarios. The core logic of health insurance is preventive protection; however, demand for health insurance is often triggered by medical-related scenarios, such as when friends or family members are diagnosed with critical illnesses. Therefore, health insurers should capitalize on key scenarios like medical consultations and prescription purchases, embedding insurance products into these contexts to fully stimulate consumer demand.

After completing the first two steps, the focus shifts to establishing strong connections and high-frequency interactions with policyholders. Here, we can draw on the logic of the consumer goods industry—namely, whether the service cycle is sufficiently long and the consumption frequency is sufficiently high. Traditional health insurance involves only sales and claims settlement, lacking medical services and health management; the future lies in the deep integration of insurance and services. Building on these deep interactions, an platform can be established leveraging the connective power of insurance to provide diversified products and services based on user needs.

Zhao Yang believes that although insurtech and managed care insurance are currently hot topics in the health insurance industry, their market potential and business models have not yet taken shape in the short term. For instance, in the realm of insurtech, system development costs are excessively high; if market scale fails to keep pace, there will be a lack of paying customers. In terms of managed care, difficulties in accessing medical data and challenges in controlling costs within public hospitals constitute institutional barriers. These issues require improvements in the broader environment and cannot be overcome through the innovations of one or two companies alone.

An Ke, Investment Manager of the Direct Investment Department at GTJA Capital

An Ke, with a background in public administration and hospital management, possesses in-depth knowledge of comparative healthcare systems across different countries, reforms in healthcare payment methods—particularly Diagnosis-Related Groups (DRGs)—as well as hospital management, benchmarking, and operations. He points out that, based on international experience, China’s healthcare security system shares more similarities with Germany’s, characterized by social health insurance as the primary component and commercial health insurance as supplementary. In such a system, where funding is primarily sourced from the state and society, there is a strong crowding-out effect on commercial health insurance. In contrast, the United States operates under a model dominated by commercial health insurance, with national health insurance playing a secondary role. Therefore, under differing healthcare security systems and medical frameworks, there are numerous obstacles and difficulties for China in learning from and adopting the U.S. model of “managed care insurance.”

Anke believes that although domestic health insurance has experienced rapid growth over the past five years, true health insurance products in China still suffer from limited variety, small scale, and inconvenient renewal processes. In the long run, the main development trajectory of China’s health insurance industry will be to identify genuine needs, reduce insurance costs, and ultimately achieve accurate risk pricing, thereby creating a win-win situation for both insurers and policyholders. The identification of new demands and innovation in insurance products represent the future growth potential of the health insurance industry. By leveraging high-quality data from medical institutions or strong demand in high-frequency scenarios, companies can build data platforms and risk control models to develop new insurance products, such as health insurance tailored for individuals with chronic diseases and the elderly population.

The limited variety and small scale of health insurance products in the past were primarily attributable to two factors: First, property and casualty (P&C) insurance and life insurance experienced rapid growth, whereas health insurance policies involved smaller individual premiums, higher claim frequencies, and greater management complexity. Second, the lack of medical data and insufficient risk control capabilities led to inadequate oversight of medical practices, resulting in persistently high claims costs. However, this landscape is shifting due to several developments, such as policy mandates promoting the adoption of electronic medical records (EMRs) in public hospitals—with all tertiary hospitals required to achieve Level 4 EMR certification by 2020—the slowing growth rates of P&C and life insurance, and national policy support for commercial health insurance. Based on this logic, Anke is more optimistic about innovative companies that can leverage high-quality medical data generated by the upgrade in healthcare informatization to conduct next-generation risk identification and pricing, thereby introducing new types of health insurance products.

Another key focus is the control of commercial health insurance costs, such as leveraging artificial intelligence to handle administrative tasks and reduce labor expenses, and utilizing big data technology to identify insurance fraud and over-treatment. Additionally, it involves proactive intervention in insured customers’ behaviors—for example, promoting healthy lifestyles and managing medication adherence to lower the risk of disease progression, thereby reducing claim payouts.

Managed care health insurance, characterized by the synergistic “insurance + services” model, has garnered significant attention from major insurance institutions. Notable examples include the integration of Ping An Health Insurance with Ping An Good Doctor, Taikang’s initiatives in dental insurance, and WeDoctor’s exploration of the HMO model. While their approaches vary, all represent cases of synergy between health insurance and healthcare services. Additionally, the U.S. health insurance industry has recently witnessed trends toward vertical integration along the industrial chain, such as CVS’s acquisition of Aetna and Cigna’s acquisition of the PBM firm Express Scripts (ESI). These developments offer valuable insights for their Chinese counterparts.

Li Yang, Director at Puhua Capital & Zhang Bingjie, Investment Director

Previously, Li Yang, a director at Puhua Capital, authored an article providing an in-depth analysis of the development of China’s health insurance industry. (See details:Li Yang of Puhua Capital: Analyzing the Model of Insuring with Pre-existing Conditions, and New Opportunities in Health Insurance as I See It) She pointed out that, with improvements across the three dimensions of informatization, regulation, and data support, a large number of medical insurance service enterprises can provide support in areas such as innovative sales outreach, supplementary services, and actuarial rate setting.

Li Yang believes that the health insurance industry currently faces two major challenges: actuarial science and medical services. The primary difficulty in actuarial science is the lack of data, which hinders the design of new insurance products. As a complex financial betting product involving multiple parties, commercial health insurance cannot achieve true innovation without robust actuarial models.

The challenge in healthcare services lies in the insufficient number of private medical institutions aligned with commercial insurance in China, while public medical institutions hold disproportionately strong bargaining power, leaving commercial insurers unable to effectively control the quality and cost of medical services.

Therefore, policy is particularly crucial. Zhang Bingjie believes that if bottom-up cost containment proves difficult to achieve, the only recourse is to rely on policy measures to enhance the transparency of medical services. Meanwhile, data is of paramount importance. The vast majority of past health insurance products have been targeted at healthy populations, who generally exhibit weak demand for such coverage. With access to high-quality medical data, insurers can develop health insurance products tailored to individuals with pre-existing conditions and optimize the service delivery process for health insurance.

Puhua Capital’s key investment in the health insurance sector is Jianyibao. Founded in 2017, Jianyibao connects pharmaceutical companies, medication usage scenarios, and financial insurance providers. It develops innovative insurance products to address cross-industry pain points faced by these three parties, thereby addressing health coverage needs for individuals with pre-existing conditions and building a comprehensive insurance service platform.

Through in-depth collaboration with financial and insurance companies, Jianyibao has jointly developed insurance products for patients with pre-existing conditions, covering medication reimbursement as well as compensation for complications and adverse reactions, thereby alleviating patients’ medical payment burdens. As of February 2019, Jianyibao’s “Medication Coverage” program had provided insurance coverage to 255,000 individuals, with a total insured amount reaching RMB 344 million.

In addition, Puhua Capital has also invested in Zhanlue Data. Founded in 2016, Zhanlue Data is an insurtech company specializing in big data and artificial intelligence technologies. Its main products and services include an intelligent claims processing platform for health insurance, an intelligent risk control platform for medical insurance, and an intelligent management platform for long-term care insurance. The company has completed its angel and Series A financing rounds, with investors including Gaorong Capital, Fumu Asset Management, Danhua Capital, and Qihoo 360.

Summary

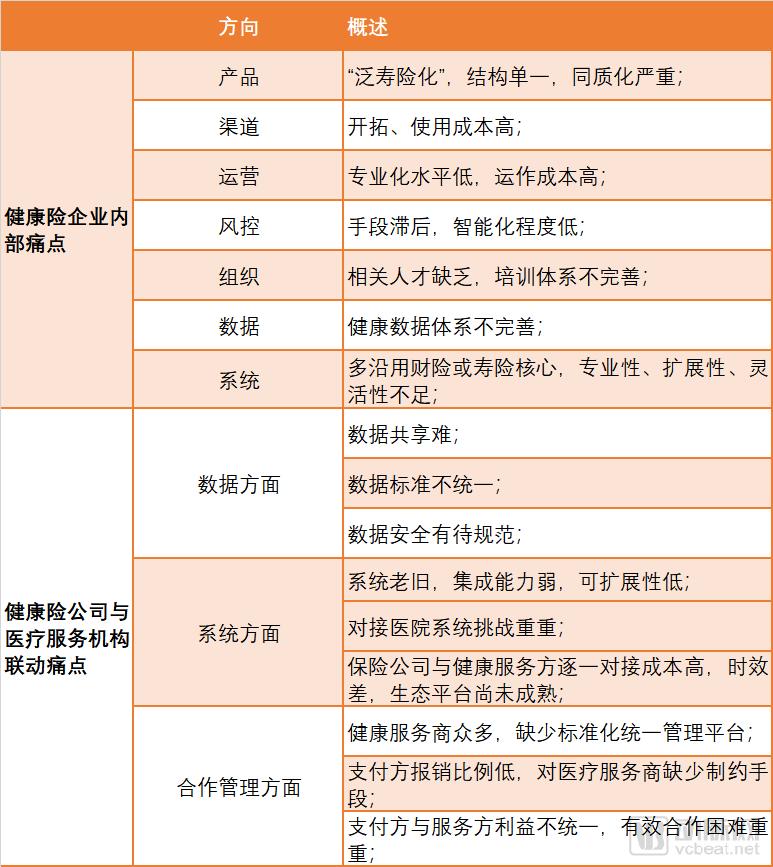

Pain points and challenges in the health insurance industry have been systematically reviewed previously, encompassing both internal operational issues within health insurance companies and difficulties in external collaboration. These are specifically manifested as follows: severe “life-insurance-ization” of products, characterized by a simplistic structure and high homogeneity; high costs for channel development, with customer acquisition costs rising sharply even in online channels; and systems that largely rely on property or life insurance core platforms, resulting in poor professionalism, scalability, and flexibility.

More importantly, there are significant challenges in the synergy between health insurance and medical services. For instance, hospital data silos make it difficult to access high-quality medical data; the one-on-one integration between insurers and healthcare service providers is costly and inefficient, while ecosystem platforms remain immature; furthermore, misaligned interests between payers and providers pose substantial barriers to effective collaboration.

Table 2: Major Operational Pain Points in the Health Insurance Industry

Source: EY China Commercial Health Insurance White Paper

These pain points have largely become an industry consensus. However, these challenges also serve as the starting point for entrepreneurship, giving rise to a wave of innovative companies that address problems and confront challenges head-on. Innovation opportunities can be identified across various stages of the business process, such as product design, channel platforms, healthcare service network development, and health management services. Driven by technology, this workflow is being restructured; for instance, insurance platforms can leverage data to collaborate with insurers in developing innovative insurance products. In fact, this is precisely the approach adopted by organizations such as Xiao Yu San and Da Te Bao.

“Data” is the key focus for the future. The development and operation of health insurance products rely on data. In the past, medical data was scarce; however, with the support of big data and artificial intelligence technologies, data can be better acquired and utilized. Data generated by AI technologies in areas such as image recognition, assisted diagnosis, and risk screening can also be integrated with health insurance.

The reform of China’s national healthcare payment methods presents a significant opportunity. On one hand, it enhances the transparency of medical services, shifting the payment model from fee-for-service to value-based or outcome-based reimbursement. On the other hand, it substantially advances the level of informatization in hospital clinical management. Reviewing the development trajectory of mature markets, the enhancement of healthcare informatization serves as the starting point for effective cost containment and managed care insurance.

From an investment perspective, whether through long-term partnership or short-term incubation, innovative companies are best served by having a well-established and complete business model. While innovative enterprises may harbor grand visions to transform industry ecosystems, it is more critical to maintain steadily growing revenue; sustainable success depends not only on going the distance but also on proceeding with stability.