SanYi Linkage Enters a New Phase with Clearer Strategies: Company Submits IPO Prospectus

Original: Xiangyun Manbi (Subscription Account: LuckCloudsnotes), reposted with authorization from VCBeat.

Jack Ma asked Wu Xiaobo, “Do you know what the most profitable business model is?” Wu replied, “What is it?” Jack Ma answered, “The national model.” — From *The Mistakes Jack Ma Has Made Over the Years* by Wu Xiaobo

It has been ten years since the State Council issued the “Implementation Plan for Key Tasks in the Recent Phase of Healthcare System Reform (2009–2011)” in 2009. The reform measures and explorations outlined in the plan are still ongoing, and new challenges have emerged. However, in recent years, new and clearer solutions have also emerged in the areas of health insurance, healthcare delivery, and pharmaceuticals.

“The Implementation Plan for Key Tasks in the Recent Phase of Healthcare and Pharmaceutical System Reform (2009–2011)” states:

V. Advancing Pilot Reforms of Public Hospitals: (18) Promoting the Reform of the Compensation Mechanism for Public Hospitals. Advance the reform of the compensation mechanism for public hospitals by gradually shifting from a three-channel model—comprising service fees, drug markups, and fiscal subsidies—to a two-channel model consisting of service fees and fiscal subsidies. … Strictly control the scale, standards, and borrowing practices of public hospital construction. Promote the separation of medical services from pharmaceutical sales, gradually eliminate drug markups, and prohibit the acceptance of drug discounts. The resulting reduction in revenue or losses incurred by hospitals shall be offset through measures such as introducing pharmaceutical care service fees, adjusting fee standards for certain technical medical services, and increasing government funding. Pharmaceutical care service fees shall be included in the scope of basic medical insurance reimbursement. Actively explore various effective approaches to separating medical services from pharmaceutical sales.

Healthcare Insurance: The Transmission of Pressure; The Visible Hand and the Invisible Hand

Amid rapid population aging and an explosive rise in chronic diseases, the national medical insurance system faces immense pressure to control costs. In response, the National Healthcare Security Administration was established, implementing the “4+7” centralized volume-based procurement program and a suite of related policy measures, including payment standard policies, while strengthening monitoring and oversight of the procurement and use of both winning and non-winning drugs from the “4+7” initiative. From a profitability perspective, hospitals are incentivized to standardize the use of selected products, thereby reducing expenditures from the medical insurance fund; a proportion of the resulting savings is returned to the hospitals, providing motivation for hospitals and physicians to comply. From an assessment standpoint, selected drugs will gradually be incorporated into the newly implemented Diagnosis-Related Group (DRG) payment system.

The essence of healthcare lies in service and exchange; even among supply-side entities such as the state, hospitals, and enterprises, and demand-side stakeholders including the National Healthcare Security Administration and patients, the interaction remains fundamentally a commercial activity. Payers in the healthcare sector require new roles to play within these commercial dynamics. From the perspective of insurance fundamentals, insurance services must meet three prerequisite conditions:

1. Insurable events must be probabilistic in nature and cannot be certain;

2. The risk probabilities associated with each policyholder are mutually uncorrelated. Claim events must be probabilistic, uncorrelated, and independent;

3. Insurance is a self-sustaining business activity. To compete, insurance companies must employ two fundamental strategies: segmentation and aggregation. Segmentation involves categorizing individuals with different risk profiles into distinct groups to prevent cross-subsidization or free-riding. Aggregation entails increasing the number of policyholders within groups of similar risk. By leveraging the Law of Large Numbers, insurers can reduce the variance caused by these risks, thereby enabling more accurate risk assessment and minimizing the premiums payable by policyholders.

Because it fails to meet the three aforementioned prerequisites, national health insurance is not, in reality, a sustainable insurance model but rather a subsidy system that relies continuously on new enrollees for its maintenance.

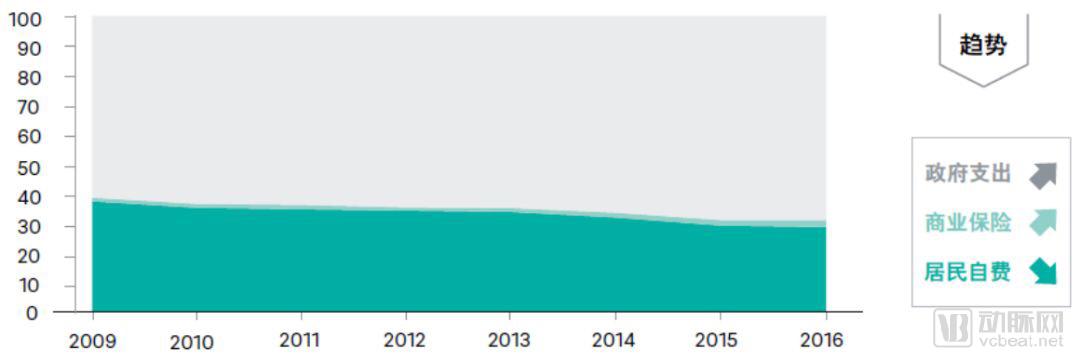

Controlling government healthcare expenditures, reducing the out-of-pocket medical burden on residents, and vigorously developing commercial health insurance are among the key tasks of the new healthcare reform.

Source: China Health Statistics Yearbook 2016; China Insurance Yearbook 2016

Government introduction of market forces and the prosperity of commercial health insurance will, to some extent, address the payment gap. In the future, the integration of chronic disease management with commercial health insurance will constitute a critically important component of medical insurance. The state should encourage the development of commercial health insurance products that are segmented and aggregated based on medical thinking, rather than continuing to promote the current individual tax-advantaged health insurance model. The latter suffers from insufficient policy incentives, limited product appeal, and cumbersome enrollment processes. Its product design lacks the segmentation and aggregation grounded in medical rationale. As the benefits it offers to both commercial insurers and consumers are marginal, it has failed to gain widespread adoption since the policy was implemented in 2015.

Healthcare: Value Chain Extension and Integration of Medical Services

The WeChat article “Endless Smoke: The Fifteen-Year Tug-of-War in Healthcare Reform” notes that the establishment of super-hospitals is not encouraged by the state, which prefers a tiered diagnosis and treatment system. It states, “After more than RMB 6 trillion in government funding has been injected, suppliers and demand-side stakeholders have finally reached a consensus: healthcare reform cannot be achieved simply by throwing money at it.”

Some netizens have expressed persistent skepticism about the internet industry’s transition to B2B models, arguing that its foundational DNA is rooted in consumer-facing (C-end) operations. If an entity can only comprehend “points” and “lines” but fails to grasp “planes” and “volumes,” then when presented with a cube, it will perceive merely a single line.

The General Office of the State Council issued the “Guiding Opinions on Strengthening Performance Appraisal of Tertiary Public Hospitals,” which replaced the sole reliance on the drug cost proportion with a performance appraisal system encompassing four dimensions: medical quality, operational efficiency, sustainable development, and satisfaction evaluation.

Since the release of three key documents, including the State Council’s “Opinions on Promoting the Development of ‘Internet + Healthcare’” and the “Administrative Measures for Internet Hospitals (Trial),” the development of internet hospitals has entered a brand-new phase. Breaking through the narrow definition from three years ago that encompassed only the consultation and treatment stage, internet hospitals have gradually evolved to cover the entire continuum of medical services, spanning “consultation–in-hospital care–out-of-hospital management.” By coordinating with medical consortia, family doctors, and pharmaceutical distribution channels, they have achieved genuine upward and downward flow of medical resources centered on patients.

Regulation.The “Administrative Measures for Internet Hospitals (Trial)” explicitly stipulates that the establishment of a provincial-level regulatory platform for internet hospitals is a prerequisite for approving their practice licenses. Currently, most provinces and municipalities have not yet established a comprehensive regulatory system for internet hospitals. According to feedback from multiple internet hospitals, the approval process for newly established internet hospitals has been prolonged, and review standards have become more stringent. Automated intelligent supervision should be implemented for contracted and onboarded internet hospitals; meanwhile, efforts must be accelerated to build nationwide unified trusted digital medical identities and electronic real-name authentication systems for healthcare professionals and medical institutions. This means that the development of internet hospitals must strictly adhere to the standards published by relevant authorities. In the recruitment of healthcare professionals, rigorous screening criteria and evaluation systems must be established to ensure the quality of medical services.

On the other hand, for physicians, driven by the policy allowing multi-site practice, obtaining certification means they can serve at multiple internet hospitals, thereby expanding their patient volume and increasing personal income. Third-party institutions must ensure that the qualifications of service providers comply with relevant regulations and assume responsibility for the services provided. This embodies the principle that “whoever provides the service bears the responsibility.” Therefore, when recruiting physicians, enterprises should establish diversified cooperation models, such as partnership systems, to align physicians’ interests with those of the platform, strengthen their sense of ownership, and encourage them to proactively prioritize medical service safety. Meanwhile, this trend highlights the importance of physicians’ personal brands; those with high patient satisfaction and few medical disputes will become key targets of competition among major platforms.

Online Prescription.Electronic prescriptions refer to medical documents issued by registered physicians for patients during online diagnosis and treatment activities, which are reviewed, dispensed, and verified by pharmacists with professional pharmaceutical technical qualifications, serving as proof of medication for patients. Before prescribing, physicians must obtain prescription privileges at their registered internet hospital and must accurately enter their unique digital credentials to complete the submission of the prescription, ensuring that it is issued by them personally. Each prescription shall not contain more than five types of medications; traditional Chinese medicine prescriptions must be written separately from Western medicines and proprietary Chinese medicines. Upon completion, the prescription requires an electronic signature (the signature style and special seal should be kept on file at the Pharmacy Administration Center for reference). The prescription is valid only on the day of issuance; in special cases where an extension of validity is required, the issuing physician must specify the extended validity period, but the maximum validity period shall not exceed three days.

Drug Acquisition.After completing an online consultation, patients may choose to purchase medications through either online or offline channels. For online purchases, once the physician issues a prescription, it requires the patient’s consent and online confirmation. The electronic prescription is then transmitted via the system to the internet-based e-commerce pharmacy contracted with the internet hospital. Upon payment completion by the patient, the e-commerce pharmacy delivers the medication in accordance with relevant national regulations. For offline purchases, patients may buy medications at physical pharmacies using the online electronic prescription and provide the necessary supporting documentation required for purchase to the physical pharmacy, as stipulated by relevant national regulations.

Payment Methods.Internet hospitals offer patients a variety of online payment options, enhance integration with public medical insurance and commercial health insurance, and strive to achieve real-time reimbursement of medical expenses at the earliest possible stage.

The development of internet hospitals is the result of multiple factors, including social demand, technological innovation, and policy support. The state has issued detailed regulations and guidelines covering all aspects of internet hospitals, such as application, construction, operation, and the evaluation of medical services provided by online physicians. In the future, internet hospitals may seize a significant growth opportunity, with chronic disease management and health management becoming their key development focuses. Furthermore, internet hospitals are poised to become a new traffic entry point for pharmaceutical and healthcare service providers.

Numerous internet healthcare enterprises have pursued incremental innovation based on their respective strengths and business orientations, gradually evolving diverse business models. Despite these differences, they all converge on a common paradigm: the integration of online and offline medical services, and the convergence of the entire industry chain encompassing healthcare services, insurance, pharmaceuticals, and medical devices—essentially, “all roads lead to Rome.” However, Rome was not built in a day; sustained efforts are still required to refine and optimize business processes over the long term.

Pharmaceuticals: Shifting from Channel Concentration to Channel Diversification

The lengthy WeChat article “Past Events of China’s Pharmaceutical Reform” states that lowering drug prices requires coordinated reforms and cannot be achieved by any single party alone.

The government’s “4+7” volume-based procurement (VBP) program and its associated policy “combo,” along with the impending expansion of VBP during the Two Sessions, will bring long-term, earthquake-like impacts to the pharmaceutical industry. Meanwhile, the National Health Commission issued the “Opinions on Accelerating the High-Quality Development of Pharmaceutical Care Services,” explicitly stating that “the public welfare nature of public hospital pharmacies must be upheld; public hospitals are prohibited from contracting out or leasing their pharmacies, and must not entrust pharmacy operations to for-profit enterprises.” From a market perspective, the majority of the pharmaceutical manufacturing sector will shift its focus to out-of-hospital channels. Direct-to-Patient (DTP) models, electronic prescriptions from internet hospitals paired with retail pharmacies, as well as community hospitals, county-level hospitals, and township health centers, will serve as key sources of growth.

DTP and Internet Hospital E-Prescriptions + Retail Pharmacies are not merely a change in drug sales channels; at the macro level, akin to the new retail concept in fast-moving consumer goods (FMCG), pharmaceutical companies and chain pharmacies need to collaborate with new business partners—including information service providers, modern logistics and distribution networks, pharmaceutical care service platforms, and professional institutions for patient and disease management (such as internet hospitals)—to build an innovative business model characterized by efficient, secure, and integrated operations.

At the meso level, pharmaceutical companies still need to establish new types of service relationships with physicians. This includes helping doctors understand new drugs, assisting them in using emerging tools such as internet hospitals for patient management, and guiding them to explore applications within new healthcare delivery models. After all, increasing prescription volume ultimately relies on individual prescriptions as the fundamental prerequisite.

At the micro level, pharmaceutical companies need to adopt a patient-centric approach—recommending suitable medication regimens and commercial health insurance plans for patients, providing “concierge services” such as home delivery of medications for long-term patients undergoing follow-up consultations at internet hospitals, and even offering more personalized services from the perspective of patients’ family members, thereby truly returning to the value that healthcare places on the “human” element.

Summary

Currently, government bodies, hospitals, enterprises, and other healthcare industry stakeholders are navigating through uncertainty, yet their paths will ultimately converge. The ultimate direction of China’s healthcare development will undoubtedly be an online-offline integrated model tailored to regional differences. In the future, each province and region will rely on different platform enterprises as the main entities to leverage the internet for achieving integrated healthcare solutions encompassing hardware, software, services, pharmaceuticals, and medical insurance payments. This will create a new healthcare service model—one that is grounded in information technology and data, truly patient-centric, and delivers a seamless experience by breaking down business and information silos.

References:

"Recent Key Implementation Plan for the Reform of the Medical and Health Care System (2009–2011)" General Office of the State Council

2018 Internet Hospital Report, VCBeat/VCBeat