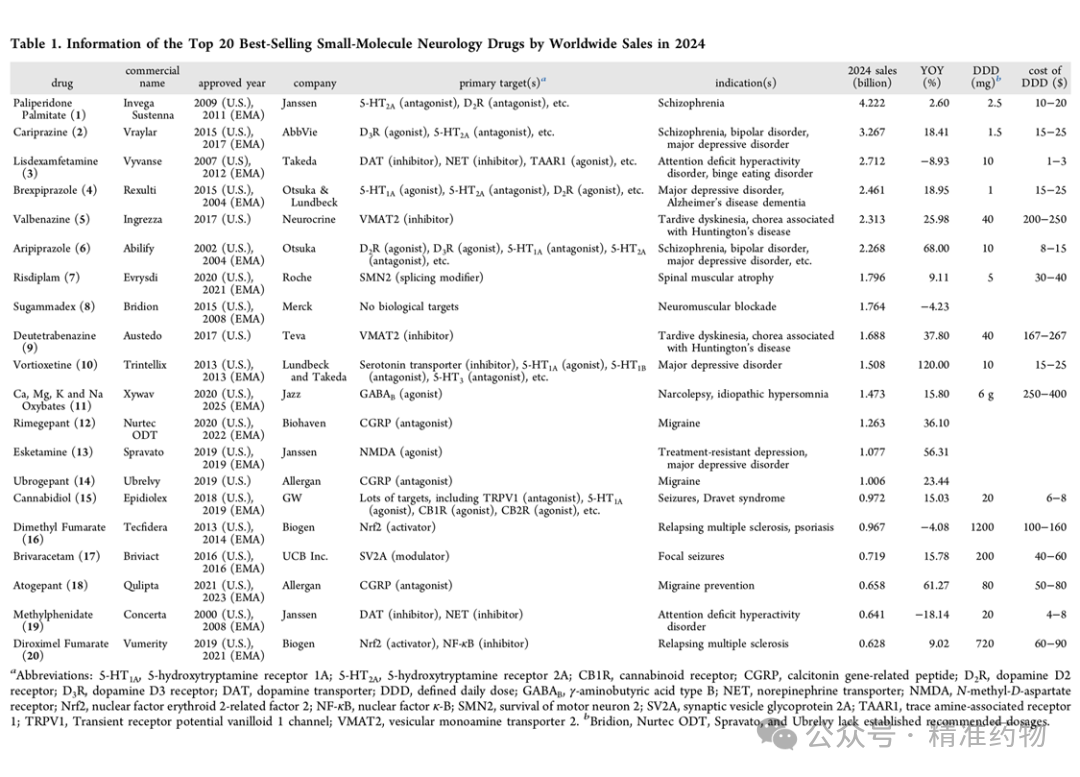

Top 20 Best-Selling Small-Molecule CNS Drugs of 2024: Market Landscape, Indications, Pharmacological Profiles, Discovery Histories, and Synthetic Strategies

Johnson & Johnson

Medical Device R&D and Manufacturer

Click the blue words ↑ to follow the Pharma Research Perspective Official Account

PharmaView

JMCOverview

2026.01.02

Recently,Prof. Chenzhong Liao from Hefei University of Technology & ShenzhenMicroCore Biotech Wang XinhaoPublished in the authoritative journal of medicinal chemistry, "Journal of Medicinal Chemistry," titledTop 20 Global Small Molecule Neurological Drugs Sales in 2024: Analysis of Market Landscape, Indications, Pharmacological Characteristics, Discovery Process, and Synthetic StrategiesThe research paper systematically reviews and deeply analyzes the top 20 small-molecule nervous system drugs by global sales in 2024. From multiple perspectives such as market landscape, indication expansion, mechanisms of action, medicinal chemistry origins, and synthetic routes, the paper provides a comprehensive review of the success paths of these "blockbuster" drugs, revealing the value logic driven by the dual engines of "efficacy and commerce," offering a reference model and inspiration for the development of new drugs for the central nervous system.

01

Research Background

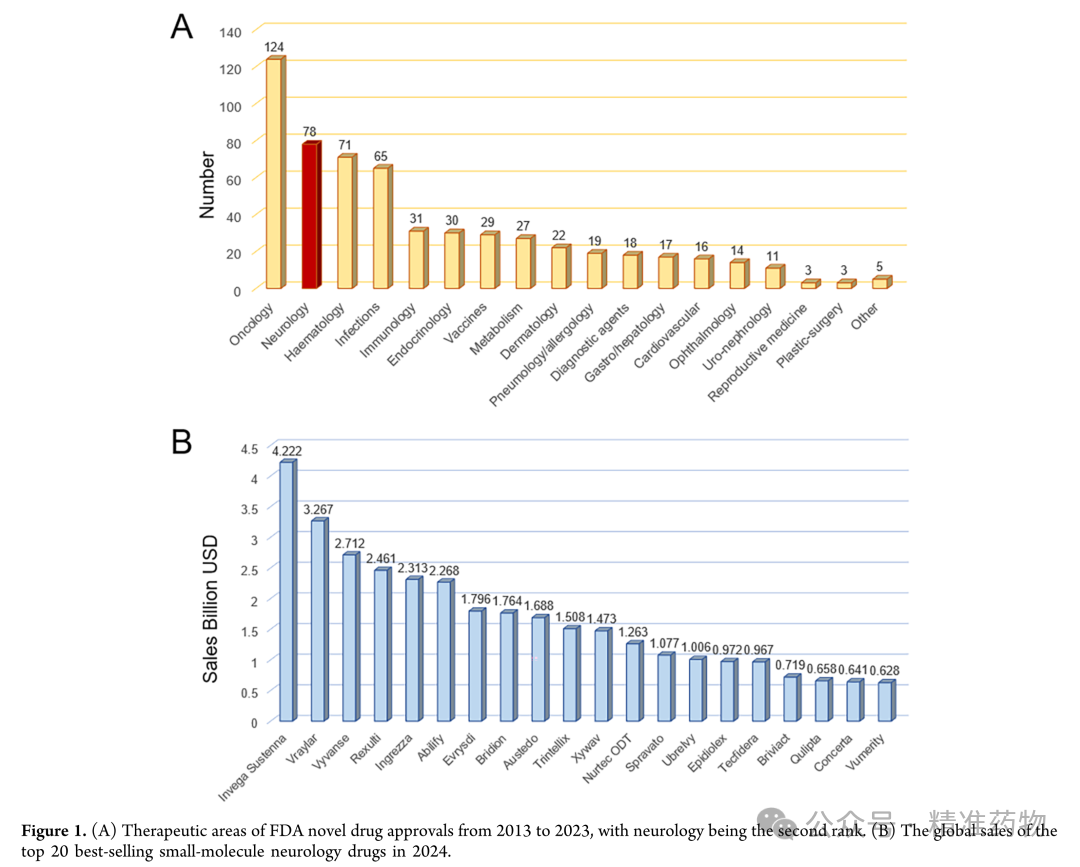

Global neurological disorders affect approximately 3.4 billion people, accounting for 43% of the global population. Since 1990, the burden of disability, disease, and premature death caused by these disorders has surged by 18%, making them the leading cause of global disease burden, surpassing cardiovascular diseases. Driven by this trend, the neurology drug market is projected to grow from $98.1 billion in 2025 to $152.3 billion by 2030, with a compound annual growth rate (CAGR) of 7.6%. Despite long-standing R&D barriers such as the blood-brain barrier, target validation challenges, and high clinical failure rates, neurology remains the second-largest therapeutic area in the global R&D pipeline, second only to oncology. Among the 55 new drugs approved by the FDA in 2024, 7.3% were for neurological indications. From 2013 to 2023, a total of 78 novel neurology drugs were approved, representing 13.15% of all new molecular entities during the same period. In terms of drug modalities, small molecules continue to dominate due to their high drug-like properties and convenient administration. However, monoclonal antibodies, gene therapies, and protein-based drugs are increasingly entering the field, creating a diversified competitive landscape. Biologics such as Ocrelizumab and OnabotulinumtoxinA have demonstrated critical value in indications like multiple sclerosis and chronic migraine, highlighting unmet clinical needs and commercial returns that continue to attract capital, technology, and policy resources to the neurology sector.

02

Best-Selling Neurological System Drugs

2.1 Paliperidone Palmitate (Invega Sustenna)

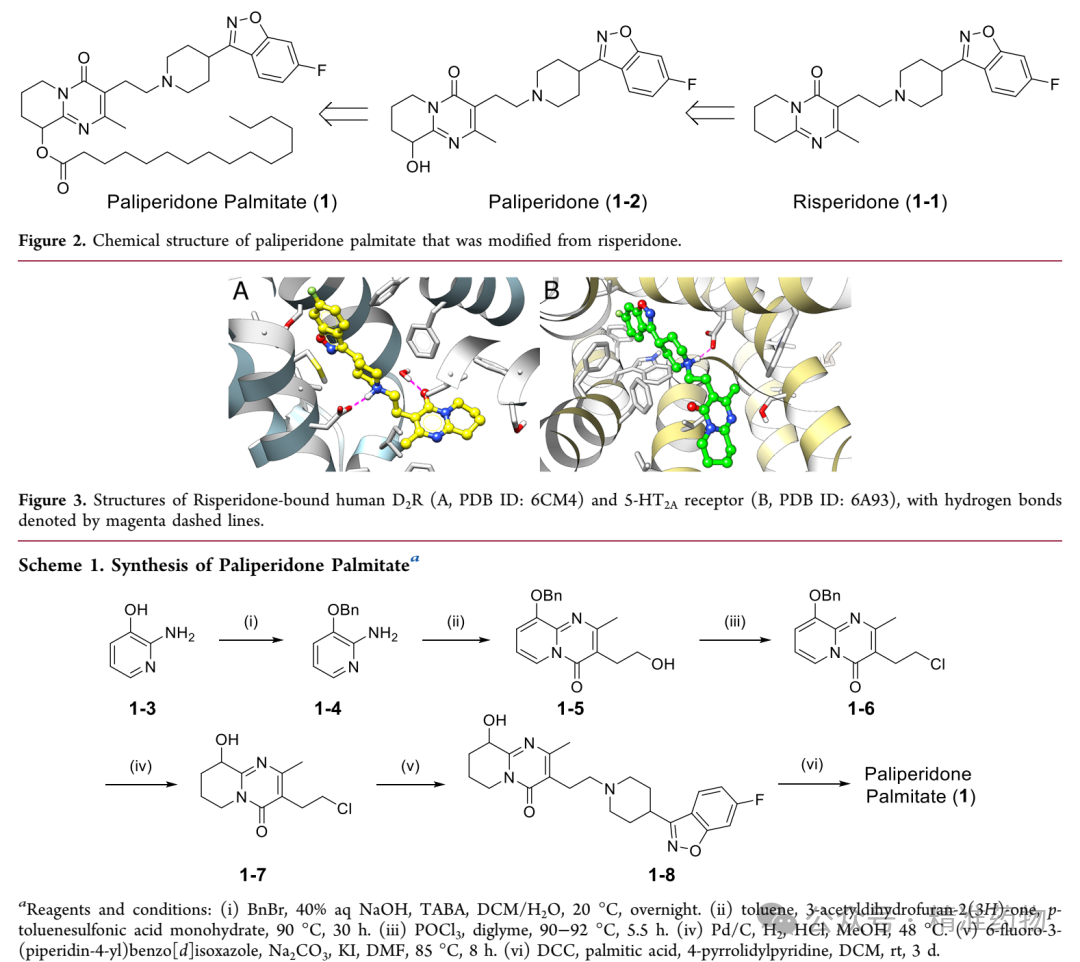

Paliperidone Palmitate: Johnson & Johnson's Janssen developed this long-acting water-soluble suspension injection, which was approved by the FDA in 2009 for adult schizophrenia and schizoaffective disorder. It can be administered once every three months or even six months. In 2024, its sales reached $4.22 billion, ranking first among neuro-psychiatric small molecule drugs for four consecutive years. The design concept involves esterifying the active metabolite of risperidone, 9-hydroxyrisperidone (paliperidone), with palmitic acid to reduce water solubility, forming a prodrug that slowly hydrolyzes after intramuscular injection, releasing paliperidone to maintain steady-state plasma concentration and reduce relapse. Pharmacologically, it maintains an antagonistic balance on 5-HT2A and D2 receptors while avoiding M1 cholinergic and β-adrenergic receptors, minimizing extrapyramidal and metabolic side effects. With the expiration of core patents, Janssen has extended its lifecycle by upgrading ultra-long-acting formulations such as the six-week dosing Invega Hafyera and exploring combinations with psychosocial interventions, continuing to dominate the schizophrenia maintenance therapy market.

2.2 Cariprazine (Vraylar)

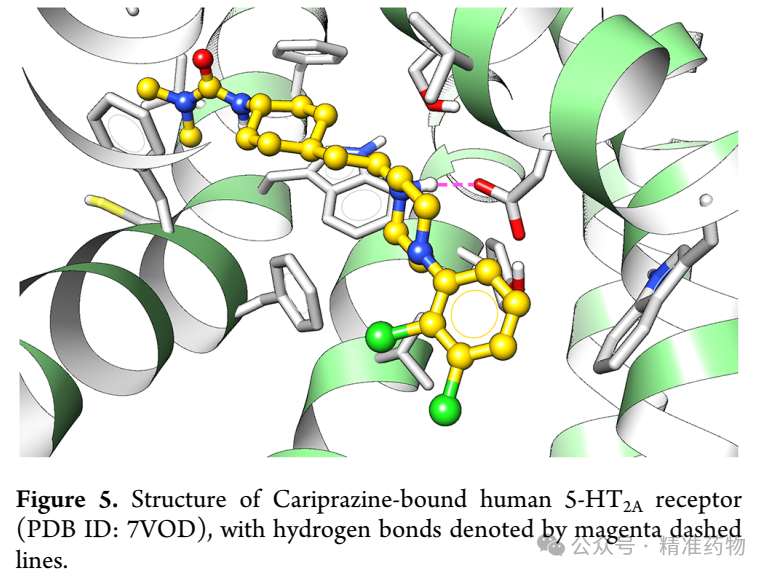

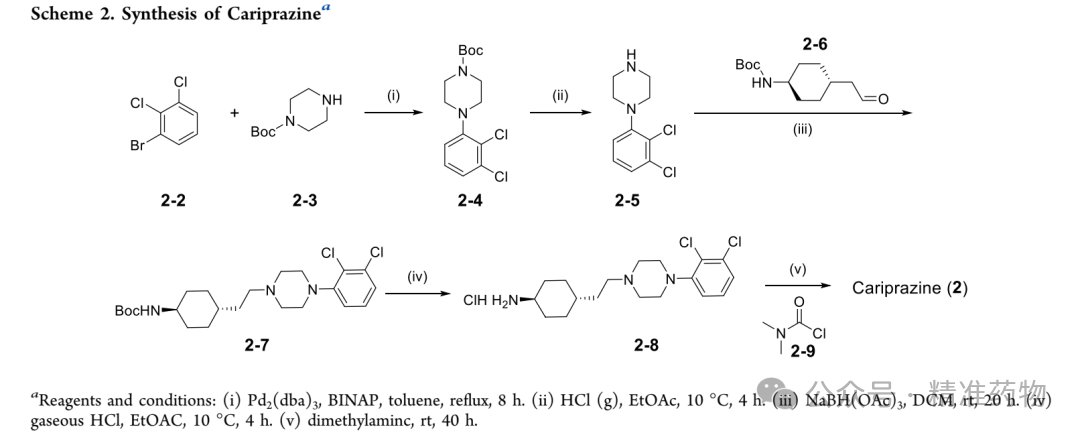

Cariprazine, a multi-target antipsychotic discovered by Hungarian pharmaceutical company Gedeon Richter in 2002 and later acquired by AbbVie through its purchase of Allergan, was approved by the FDA in 2015 for the treatment of schizophrenia in adults. Its use was expanded to bipolar mania/depression in 2016 and further extended to include adjunctive treatment for major depressive disorder (MDD) in 2022. In 2024, global sales reached $3.27 billion, representing an 18.4% year-over-year increase. Structurally derived from a benzisothiazole backbone, cariprazine shares homology with ziprasidone but achieves "dopamine system stabilization" through a combination of high selectivity partial agonism at D3 receptors, partial agonism at 5-HT1A receptors, and antagonism at 5-HT2A receptors, thereby reducing side effects such as akathisia, insomnia, and metabolic syndrome. Its long half-life (2–4 days) supports once-daily oral administration, and new indications, including anxiety and obsessive-compulsive disorder, are currently under investigation. With its patent set to expire around 2029, generic drug manufacturers have already posed challenges. However, Vraylar continues to exhibit robust growth driven by therapeutic differentiation and expanding indications.

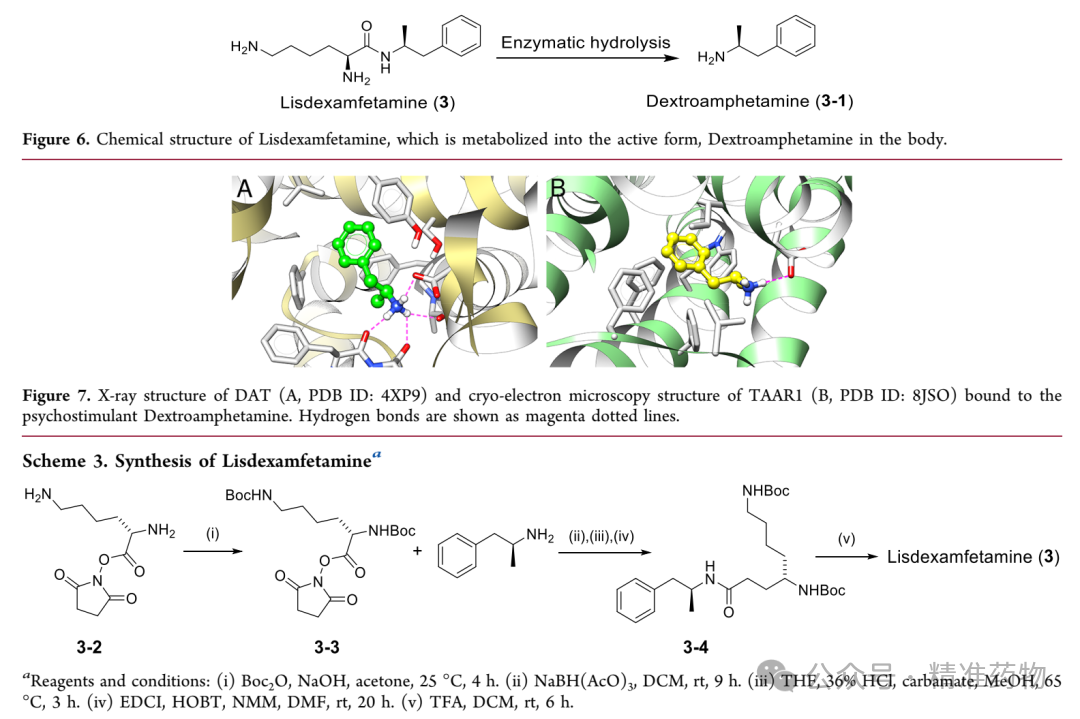

2.3 Lysine Amphetamine(Vyvanse)

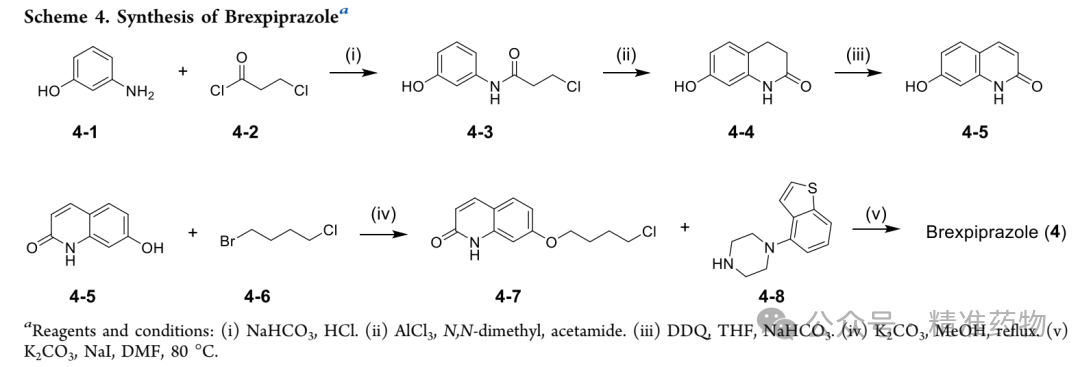

LaiAmphetamine AspartateVyvanse, an oral prodrug acquired by Takeda through the purchase of Shire, was approved by the FDA in 2007 for attention deficit hyperactivity disorder (ADHD) in patients aged 6 and above, and later approved in 2015 for moderate to severe binge eating disorder in adults. In 2024, its sales reached $2.71 billion, a year-on-year decrease of 8.9%, primarily due to the expiration of its core patent in 2023, which led to the launch of multiple generic drugs. The molecular design connects dextroamphetamine with natural lysine via an amide bond, resulting in high water solubility and low central activity. After oral administration, it is slowly hydrolyzed by red blood cells, gradually releasing dextroamphetamine, prolonging its action time, and reducing abuse potential. Its active component enhances prefrontal neurotransmitters by inhibiting dopamine/norepinephrine reuptake, activating TAAR1, and other multi-target mechanisms, improving attention and impulse control. Clinically, it is considered a first-line central stimulant for ADHD and is currently being explored for new indications such as methamphetamine dependence and multiple sclerosis-related fatigue. However, the impact of generic drugs has caused its sales to decline annually since peaking at $3.22 billion in 2022.

Image Source: ACS

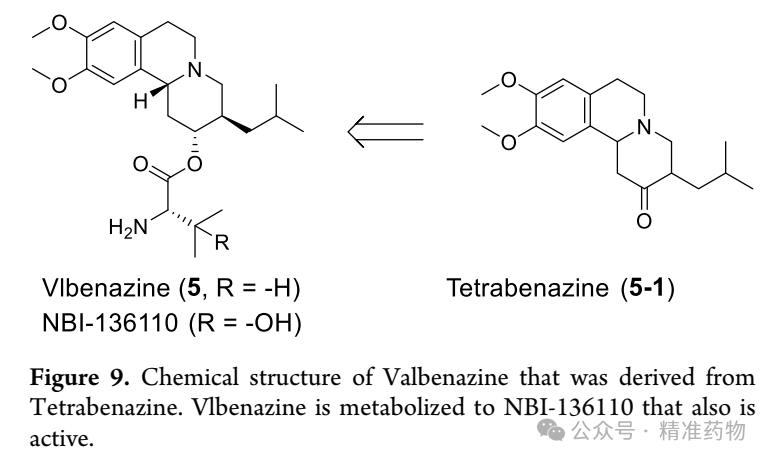

2.4 Brexpiprazole (Rexulti)

In 2015, the FDA first approved it as an adjunctive treatment for adult major depressive disorder (MDD) and schizophrenia. In 2023, it gained an additional indication for agitation associated with Alzheimer's disease dementia, becoming the first drug approved in this field. In 2024, global sales reached $2.46 billion, a year-over-year increase of 18.95%. Its design started with aripiprazole, and through structural fine-tuning, reduced D2 receptor intrinsic activity, enhanced 5-HT1A partial agonism, and 5-HT2A antagonism, achieving antipsychotic efficacy while reducing side effects such as activation, insomnia, and akathisia, and improving negative symptoms and cognition. The main patent in the United States expires in 2032 and currently faces generic drug patent challenges. Ongoing clinical research is expanding into bipolar depression, alcohol use disorder, and pregnancy safety evaluations. The anticipated expansion of indications and internationalization is expected to further boost sales.

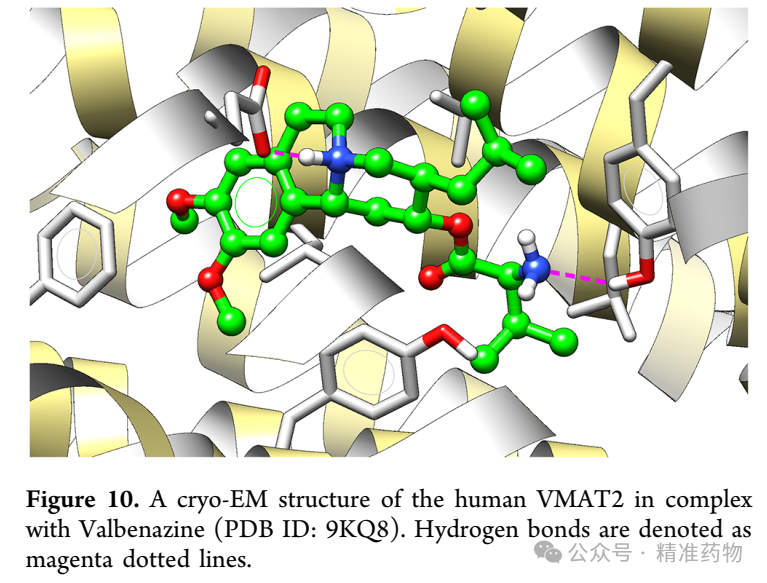

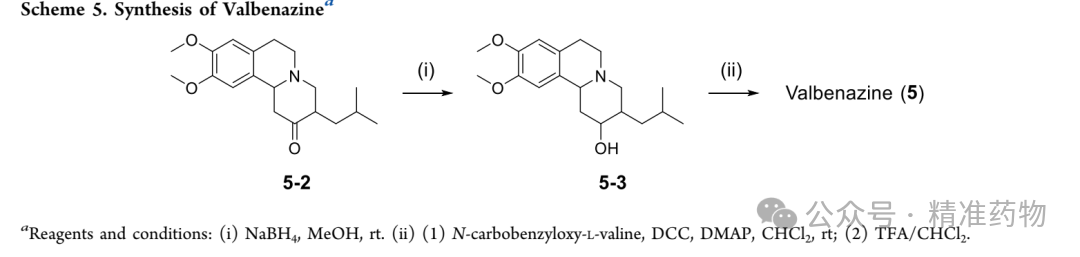

2.5 Valbenazine (Ingrezza)

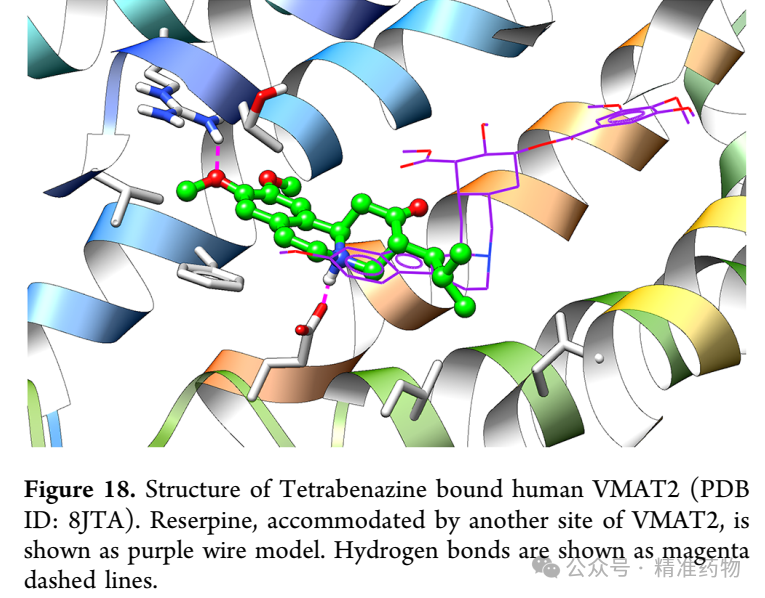

Valbenazine, developed by Neurocrine Biosciences, was approved by the FDA in 2017 as the first specific VMAT2 inhibitor for treating tardive dyskinesia (TD). In 2023, its indications were expanded to include Huntington's chorea. In 2024, its sales reached $2.31 billion, representing a year-on-year increase of 25.98%. The molecule is an optimized prodrug of the α-HTBZ subtype of tetrabenazine, selectively inhibiting vesicular monoamine transporter 2 (VMAT2) and reducing presynaptic dopamine release, thereby avoiding sedation and extrapyramidal reactions associated with D2 antagonism. It is metabolized in vivo into active α-HTBZ and secondary active metabolite NBI-136110, both of which maintain high inhibitory activity against VMAT2. With a simple initial clinical dose and no need for complex titration, it significantly improves involuntary movements within 6 weeks. Due to its efficacy and safety advantages, it maintains a dominant position in the TD/HD field and is exploring extended indications such as Tourette syndrome and Parkinson’s disease to sustain growth.

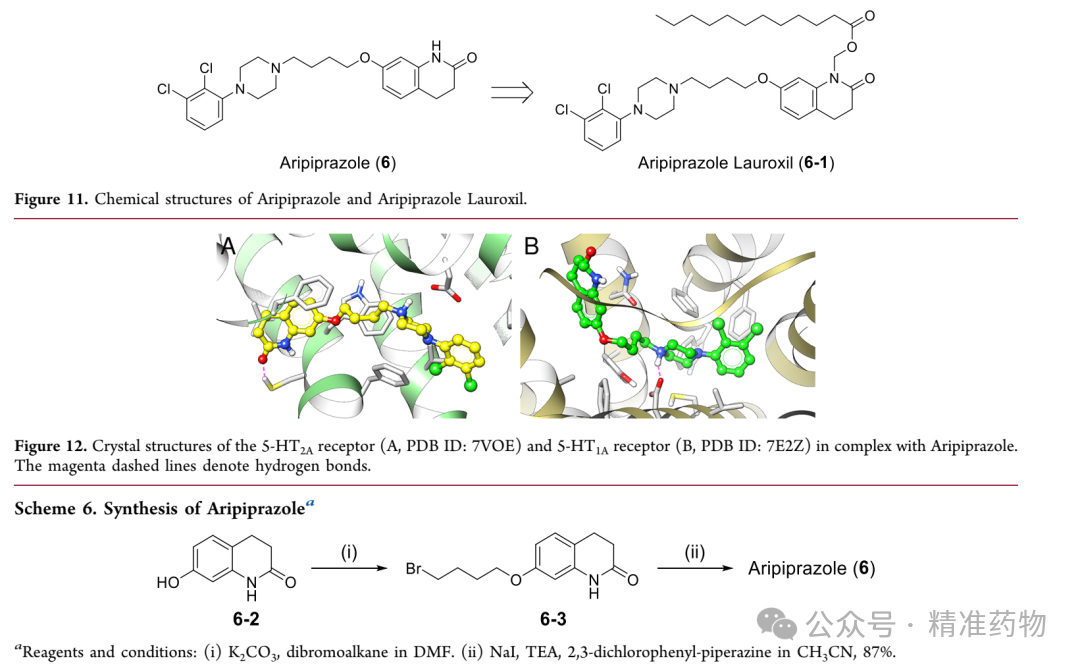

2.6 Aripiprazole (Abilify)

In 2002, the FDA approved it for schizophrenia, later expanding to bipolar disorder, major depression, irritability associated with autism, and Tourette syndrome. Global sales reached $2.27 billion in 2024, significantly down from the peak of $4.66 billion in 2009. The main reasons include a black box warning in 2007 about increased mortality risk in elderly patients with dementia-related psychosis and market diversion caused by the launch of the long-acting injectable aripiprazole lauroxil prodrug Aristada in 2015. As a "third-generation" antipsychotic, aripiprazole is quinoline-based and achieves "dopamine system stabilization" through partial agonism of D2/D3 and 5-HT1A, as well as antagonism of 5-HT2A, reducing extrapyramidal and metabolic side effects. Its crystalline long-acting injection is administered every 4–8 weeks. In 2024, Aristada's sales were approximately $1.2 billion, projected to reach $2.5 billion by 2033. After patent expiration, numerous generics entered the market, but thanks to its long-acting formulations and multi-indication advantages, the aripiprazole series still maintains a significant market share.

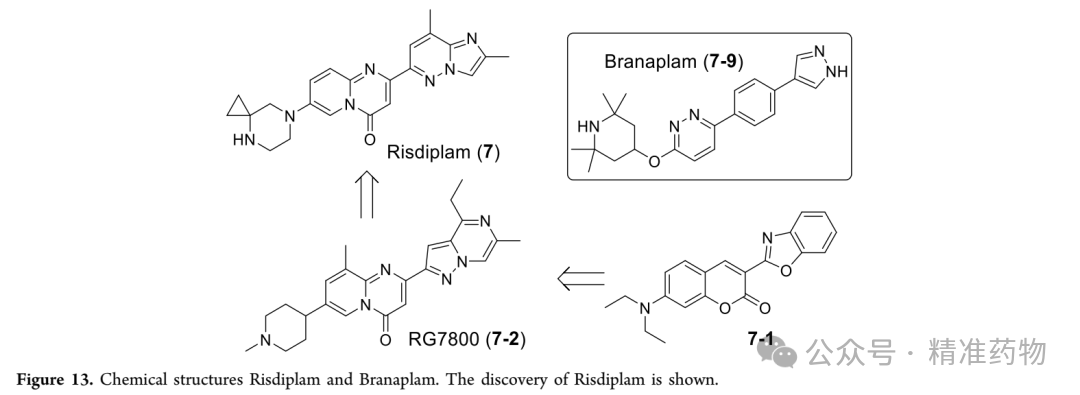

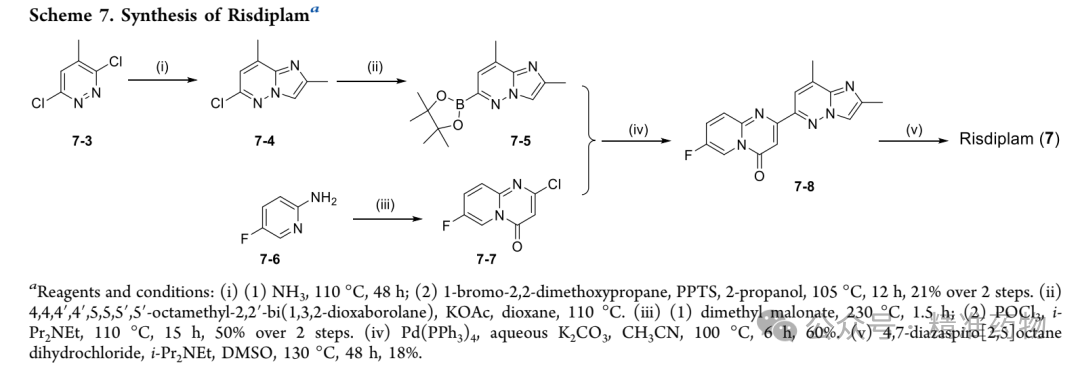

2.7 Risdiplam (Evrysdi)

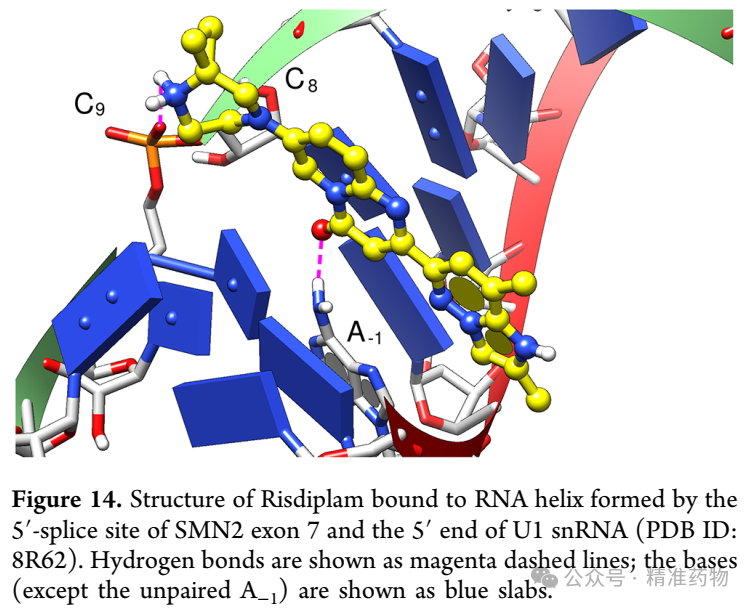

Risdiplam, co-developed by Roche, PTC Therapeutics, and the SMA Foundation, became the first approved oral small-molecule SMN2 splicing modifier for the treatment of spinal muscular atrophy (SMA) in August 2020. In 2024, its global sales reached $1.796 billion, a year-on-year increase of 9.11%. Its discovery originated from coumarin derivatives identified through high-throughput screening, followed by multiple rounds of optimization to eliminate phototoxicity and hERG inhibition, ultimately yielding an orally bioavailable dihydropyridine-pyrimidine structure capable of penetrating the blood-brain barrier. The drug promotes the inclusion of exon 7 into mRNA by binding to the major groove of the RNA double helix formed by SMN2 exon 7 and U1 snRNA, enhancing the systemic expression of functional SMN protein and thereby improving motor neuron survival. Clinical trials demonstrated that 40% of infants could sit independently for ≥30 seconds after 23 months of treatment. It can be administered orally at home or via a feeding tube, establishing it as the third standard treatment following Nusinersen and gene therapy. Its patent protection extends until 2037, and it is currently available in over 30 countries. Efforts are underway to explore earlier interventions and combination regimens to sustain growth.

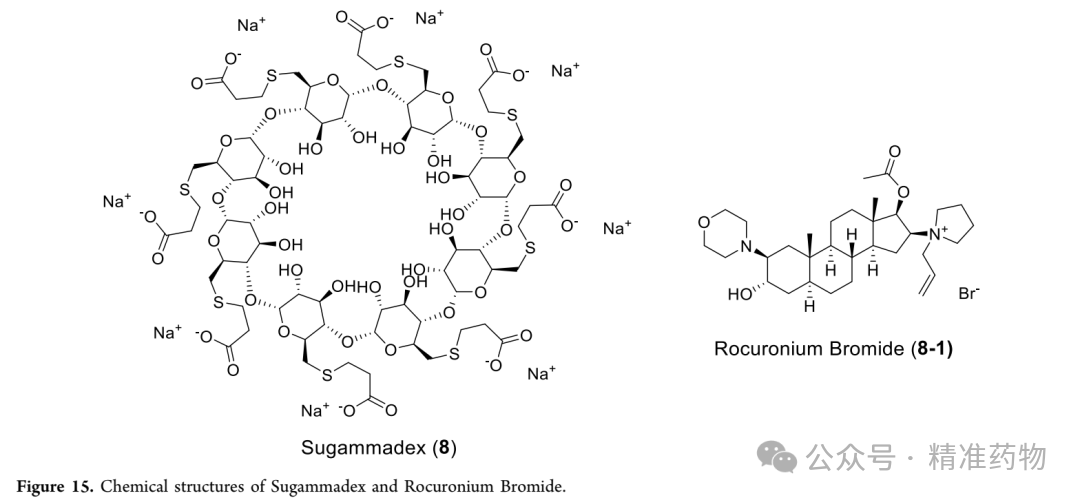

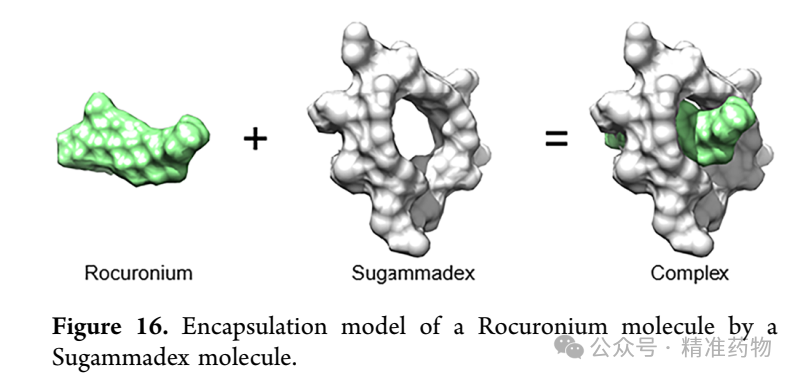

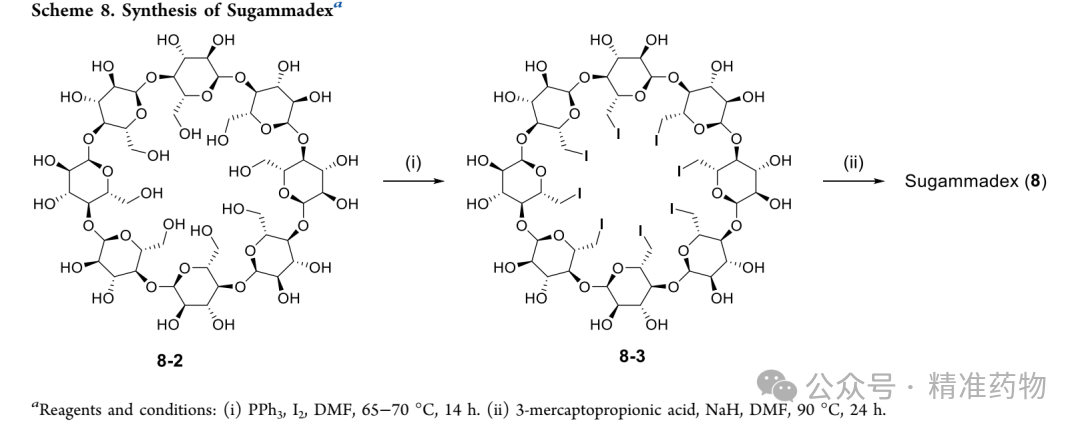

2.8 Sugammadex (Bridion)

Sugammadex, developed by Merck, is the world's only selective muscle relaxant antagonist. It was first launched in Europe in 2008 and received FDA approval in 2015 for the rapid reversal of neuromuscular blockade induced by rocuronium or vecuronium. In 2024, its sales reached $1.764 billion, nearly doubling from $917 million in 2018. The molecule is a γ-cyclodextrin derivative, with a hydrophilic outer shell and a hydrophobic cavity that can encapsulate steroid-based muscle relaxants in a 1:1 ratio. Through a "chelation" mechanism, it pulls free drugs from the neuromuscular junction back into the plasma for renal excretion, avoiding common side effects of neostigmine such as bradycardia without the need for anticholinergic drugs. As a result, it has been listed as the preferred reversal agent by anesthesia societies in Europe and America. With the recovery of global surgical volumes and continuous guideline recommendations, Bridion’s penetration rate in enhanced recovery after surgery (ERAS) scenarios is increasing. Future research will explore its combination with the new muscle relaxant gantacurium and strategies to reduce the risk of postoperative residual block.

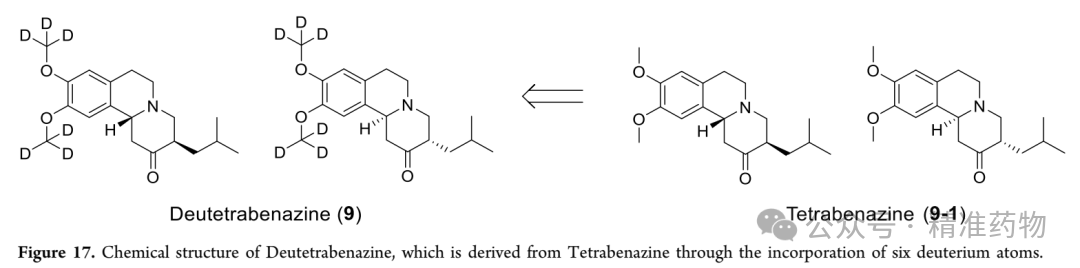

2.9 DeuterationTetrabenazine(Austedo)

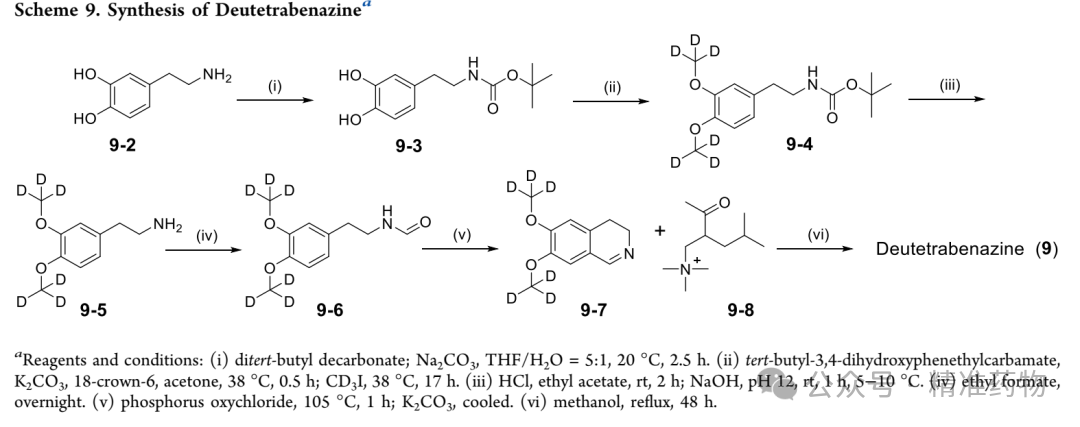

DeuterationTetrabenazineDeveloped by Teva, it became the world's first approved deuterated drug in 2017, used for Huntington's disease and tardive dyskinesia. In 2024, its sales reached $1.688 billion, a year-on-year increase of 37.8%. The drug introduces six deuterium atoms on the two methoxy groups of the parent nucleus tetrabenazine, reducing the CYP2D6 metabolic rate, thereby extending the half-life of the active metabolites α-HTBZ and β-HTBZ, reducing fluctuations in blood drug concentration, allowing for lower doses, twice-daily administration, and significantly reducing sedation and Parkinson-like side effects. As a reversible VMAT2 inhibitor, it reduces presynaptic dopamine storage and release, improving involuntary movements. Its patent extends to 2031, and it has been launched in the United States and Europe. It is currently conducting expanded indications such as Tourette syndrome, continuously capturing market share from tetrabenazine and valbenazine with the advantages of the "deuterated" technology platform.

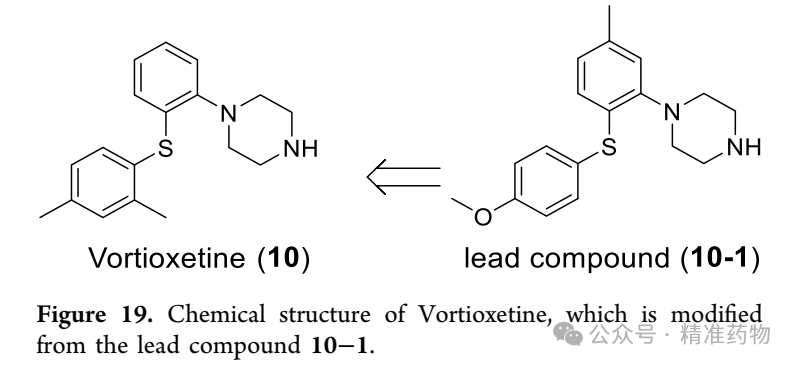

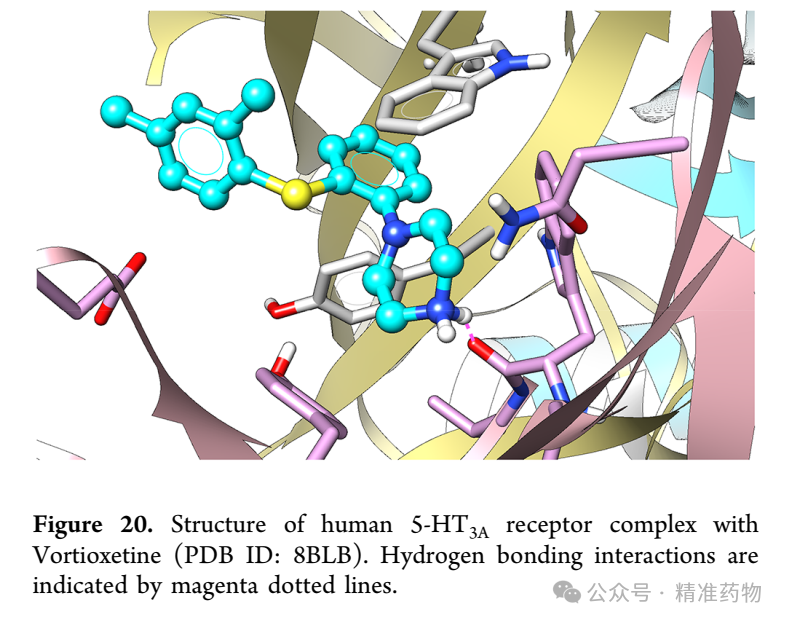

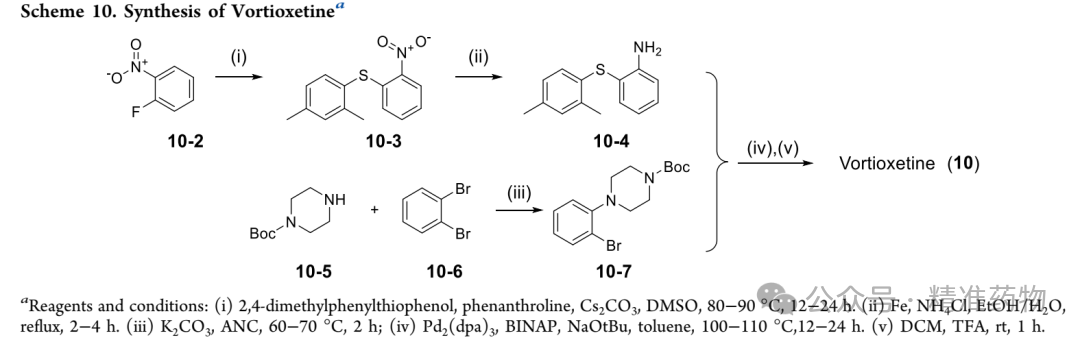

2.10 Vortioxetine(Trintellix)

Approved in both the US and Europe in 2013 for adult major depressive disorder, global sales reached $1.508 billion in 2024, a significant year-over-year increase of 120%, mainly driven by inclusion in emerging markets' medical insurance and continued patent validity in Europe and the US. The drug was derived from a benzothiophenylpiperazine lead compound screened by Dr. Kusumi, optimized for CYP2D6 metabolism and metabolic stability, featuring a multimodal action that combines 5-HT transporter inhibition, 5-HT1A/1B agonism, and 5-HT3/7 antagonism. It indirectly increases levels of 5-HT, NE, DA, Ach, and histamine in the prefrontal cortex, improving mood and cognition while reducing common SSRI side effects such as sexual dysfunction, nausea, and weight gain. Phase III trials demonstrated superior improvement in cognitive symptoms compared to placebo. Patent protection extends from 2026 to 2030, with ongoing extended studies in conditions like Parkinson’s gait freezing and emotional symptoms of frontotemporal dementia, maintaining strong growth momentum through its differentiated mechanism.

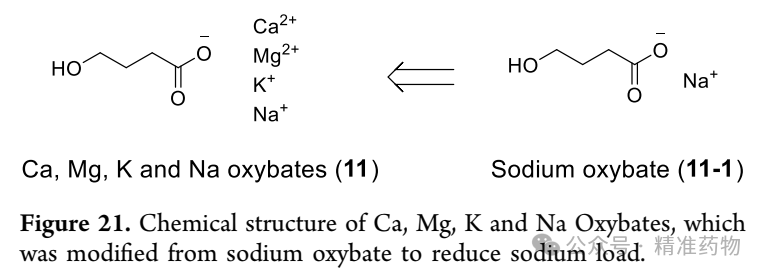

2.11 Calcium Magnesium Potassium Sodium Oxybate (Xywav)

Xywav is a low-sodium oxybate compound developed by Jazz Pharmaceuticals, containing four cations: calcium, magnesium, potassium, and sodium. It was first approved by the FDA in 2020 for narcolepsy in patients aged 7 years and older, and later expanded in 2021 to include adult idiopathic hypersomnia. In 2024, its sales reached $1.473 billion, representing a year-over-year increase of 15.8%. The design goal was to reduce the risk of hypertension and cardiovascular issues caused by the high daily sodium load (9 g) of the original oxybate formulation (Xyrem), while maintaining the efficacy of gamma-hydroxybutyrate (GHB) in activating GABA_B receptors and enhancing GABA_A inhibition after being metabolized into GABA, thereby promoting deep sleep and preventing cataplexy. The new formulation reduces sodium content to 8% of the original formula, with a pH of 7–8, while still maintaining the twice-nightly dosing regimen. With patent protection, insurance coverage, and patient support programs, Xywav has rapidly replaced Xyrem as the company’s flagship product and is currently exploring new indications related to sleep architecture to sustain growth.

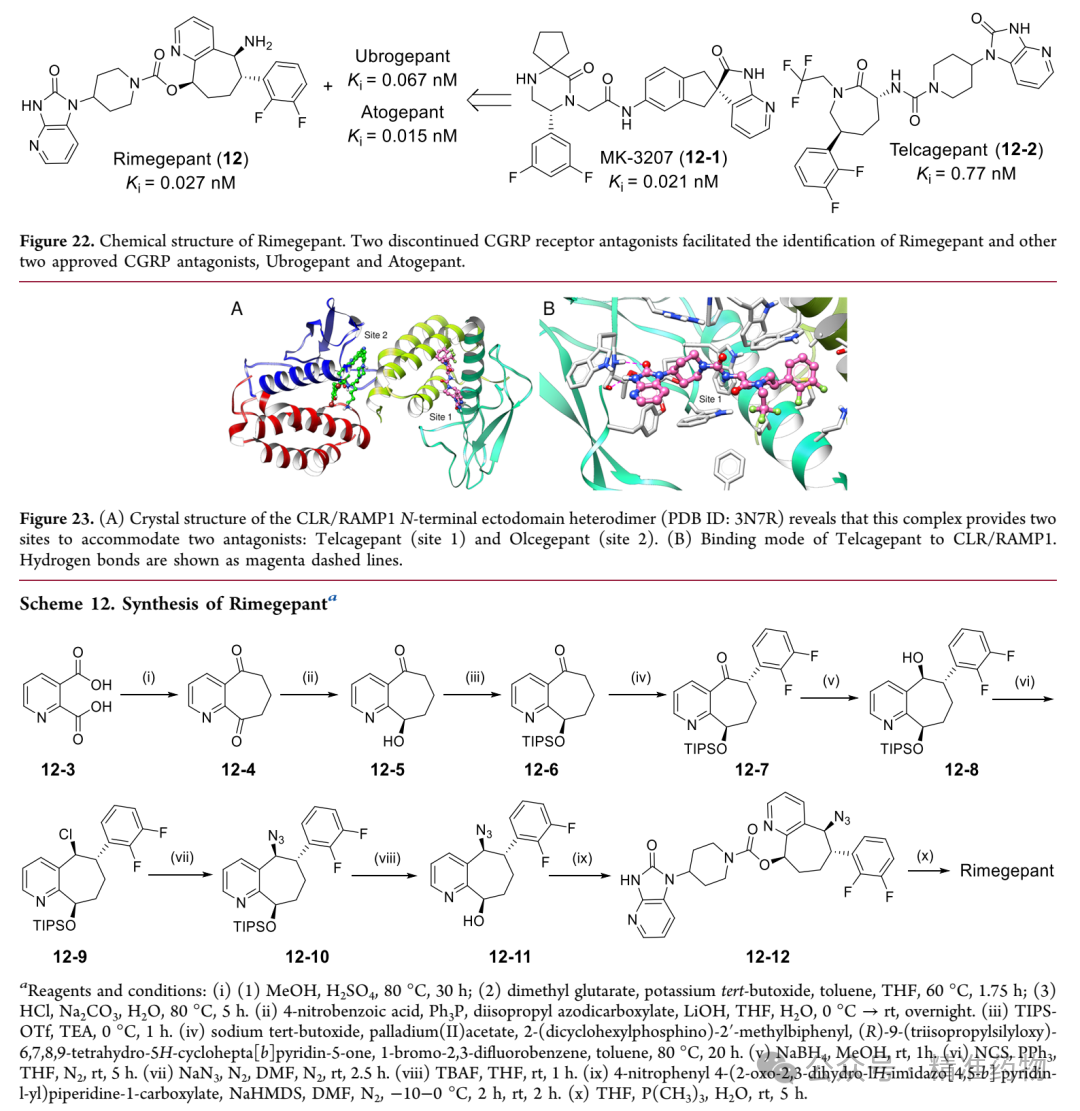

2.12 Rimegepant (Nurtec ODT)

Rimegepant, originally developed by Biohaven and approved by the FDA in 2020 as an oral lyophilized tablet CGRP receptor antagonist, is indicated for both the acute treatment of migraine attacks in adults and the prevention of episodic migraine with ≤15 headache days per month. Following Pfizer's acquisition of Biohaven for $11.6 billion in 2022, rimegepant achieved sales of $1.263 billion in 2024, representing a year-over-year increase of 36.1%. The molecular structure originated from Telcagepant, which was discontinued by Merck due to hepatotoxicity concerns. By replacing the cyclic amide backbone with a planar tetrahydro-5H-cyclohepta[b]pyridine and introducing a seven-membered primary amine ring, the compound retains competitive blockade of the CLR/RAMP1 heterodimer receptor while enhancing oral bioavailability and dissolution rate. Clinical studies show that a single 75 mg dose relieves pain within two hours, with superior sustained pain-free rates at 24 hours compared to placebo. It has no vasoconstriction-related contraindications, making it suitable for individuals at high cardiovascular risk. Patent protection extends until 2037, and the company is advancing subsequent research on combination therapy with monoclonal antibody CGRP drugs for refractory migraine, aiming to consolidate its dual advantage in "acute + preventive" indications.

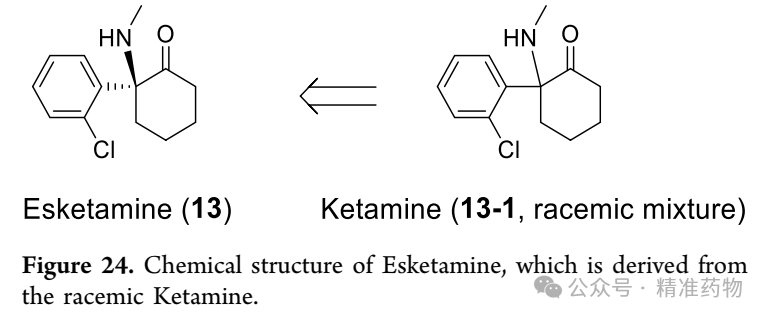

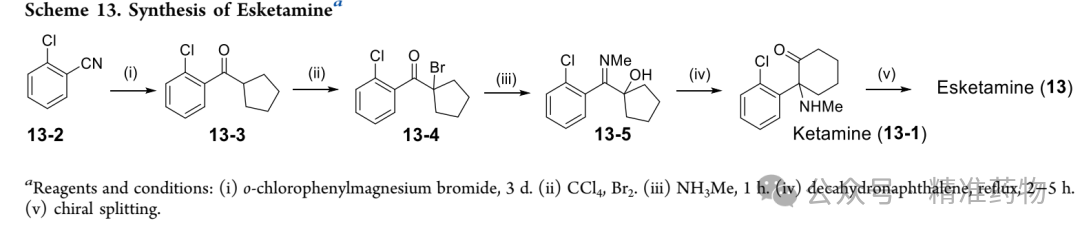

2.13 Esketamine (Spravato)

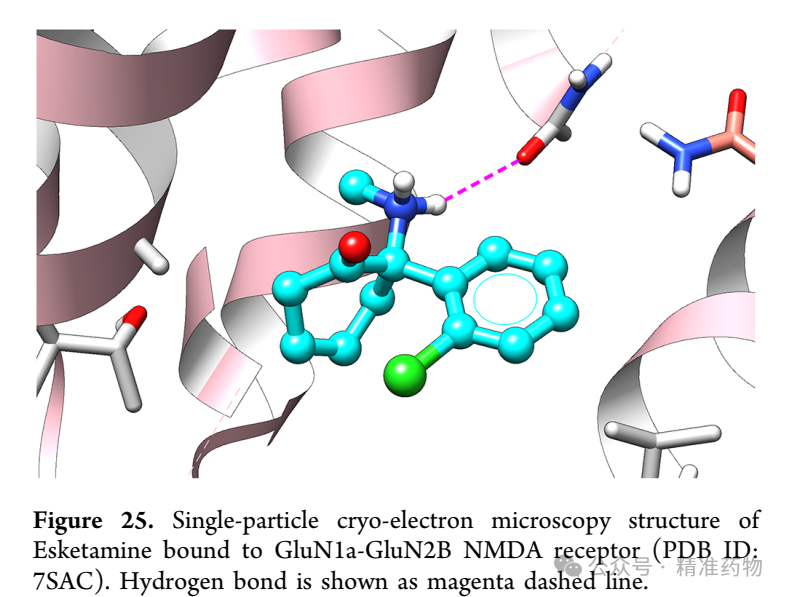

Esketamine, the S-enantiomer of ketamine developed by Johnson & Johnson as a nasal spray, was approved by the FDA in 2019 for use in combination with oral antidepressants to treat adults with treatment-resistant depression (TRD). In 2022, its indication was expanded to include major depressive disorder with acute suicidal ideation. By 2024, global sales reached $1.077 billion, marking a year-over-year increase of 56.3%, making it the first novel mechanism antidepressant in nearly a decade. It selectively blocks NMDA receptors to reduce excessive glutamate release, activates the mTOR pathway, and upregulates BDNF, rapidly enhancing synaptic plasticity. Significant reductions in MADRS scores are observed within 24 hours post-administration. The molecule is obtained via chiral separation, with analgesic potency three times and anesthetic potency 1.5 times that of the racemic mixture. The nasal spray avoids first-pass metabolism in the liver, with a bioavailability of approximately 48%. Common adverse effects include transient dissociation and elevated blood pressure, requiring supervised administration in medical settings. The patent extends until 2032 and has been included in medical insurance systems in multiple countries. Further exploration into expanded indications such as PTSD and obsessive-compulsive disorder is ongoing to maintain its leading position in the "rapid-acting antidepressant" niche market.

2.14 Ubrelvy

Ubegipant, a small-molecule CGRP receptor antagonist introduced by Allergan (now AbbVie) from Merck, was approved by the FDA in 2019 for the acute treatment of migraine with or without aura in adults. In 2024, its sales reached $1.006 billion, marking a year-on-year increase of 23.4% and maintaining a continuous rise since its market launch. The molecule was optimized based on Telcagepant and MK-3207, which were terminated early at Merck due to hepatotoxicity. It retains competitive blockade of CLR/RAMP1 heterodimer receptors while reducing lipophilicity and enhancing metabolic stability through the introduction of polar groups. Lacking vasoconstrictive activity, it can be safely used in patients with coronary artery disease. Oral administration of 50 or 100 mg takes effect within 1.5 hours, with sustained relief of pain and associated symptoms over 24 hours superior to placebo. Its core patent extends until 2034. Already launched in the U.S., it is now advancing European expansion, positioning itself with a differentiated "acute analgesic without vasoconstriction" profile to form sequential therapy with subsequent preventive CGRP small molecules, further capturing market share in the acute treatment of migraine.

2.15 Cannabidiol (Epidiolex)

Epidiolex: An Oral Cannabidiol Solution Developed by GW Pharmaceuticals

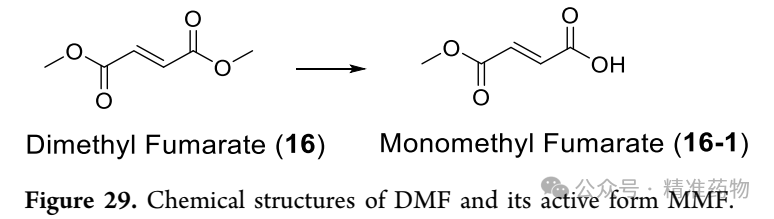

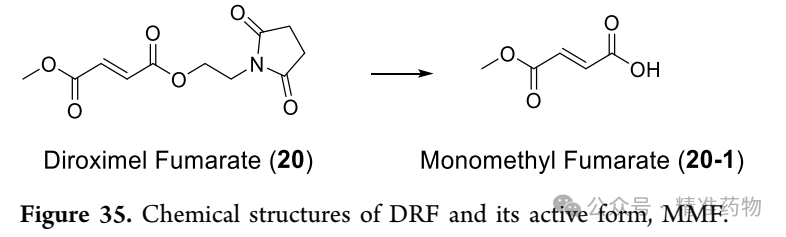

2.16 Dimethyl Fumarate (Tecfidera)

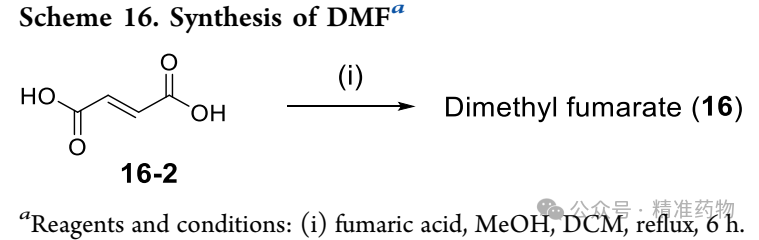

Dimethyl fumarate (DMF), an oral immunomodulatory prodrug developed by Biogen, was approved by the FDA in 2013 for the treatment of adults with relapsing multiple sclerosis (RMS). In 2024, its global sales reached $967 million, a year-on-year decrease of 4.45%, primarily impacted by the launch of generic drugs in the U.S. and Europe starting from 2020. In vivo, DMF is rapidly hydrolyzed into its active metabolite monomethyl fumarate (MMF), which activates the Nrf2 antioxidant pathway by covalently modifying Keap1-Cys151, while inhibiting NF-κB-mediated release of pro-inflammatory cytokines, reducing oxidative damage and lymphocyte infiltration in the brain. Phase III studies demonstrated an approximately 50% reduction in annualized relapse rate without the need for laboratory monitoring. With the expiration of core patents and the market entry of the self-developed upgraded version diroxime fumarate (Vumerity) causing market diversion, the company is maintaining its position as a first-line oral cornerstone drug for RMS through price adjustments, expansion into emerging markets, and potential combination therapies.

2.17 Briviact

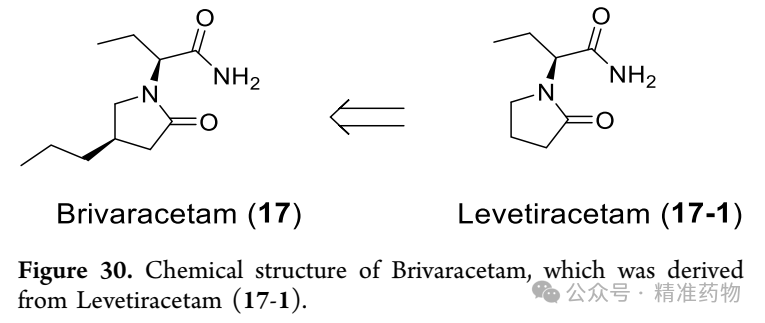

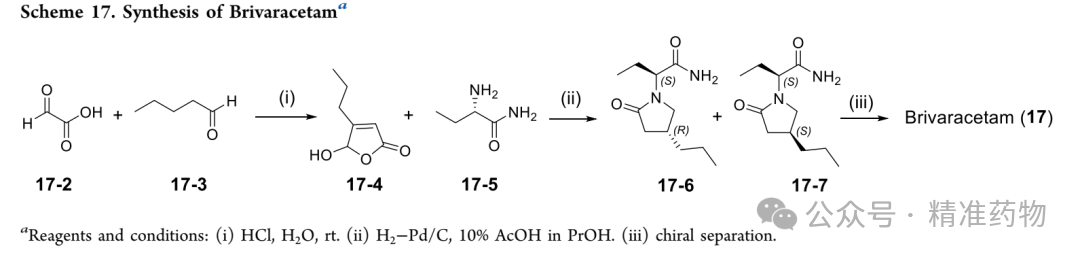

Brivaracetam, a third-generation antiepileptic drug launched by UCB, was approved by the FDA in 2016 for adjunctive therapy in focal seizures in patients aged ≥16 years. In 2024, its sales reached $719 million, marking a year-on-year increase of 15.78%. The growth momentum came from rising demand for treatment-resistant epilepsy and the approval of an intravenous formulation as an inpatient alternative. The molecule introduces a propyl group at the 4-position of the pyrrolidone ring of levetiracetam, enhancing affinity for synaptic vesicle protein 2A (SV2A) by approximately 20-fold, with faster brain penetration. This allows seizure control at lower doses (50–200 mg/day) while exhibiting fewer side effects like drowsiness and irritability compared to older drugs. Core compound patents will begin expiring from 2026. The company is expanding pediatric indications, advancing short-term intravenous use before surgery, and promoting medical insurance access in emerging markets to counter generic competition and maintain its differentiated positioning as a highly selective SV2A ligand.

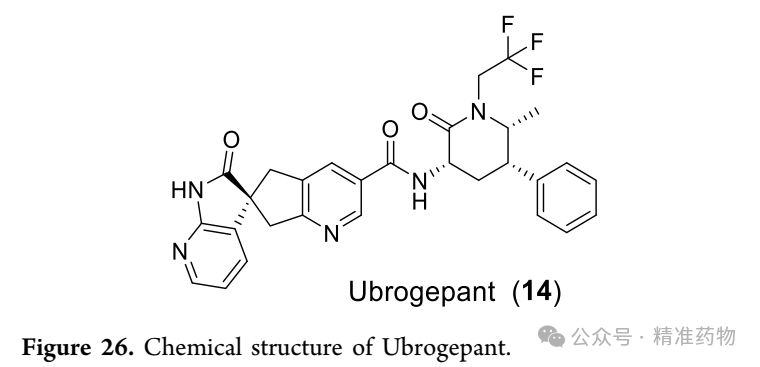

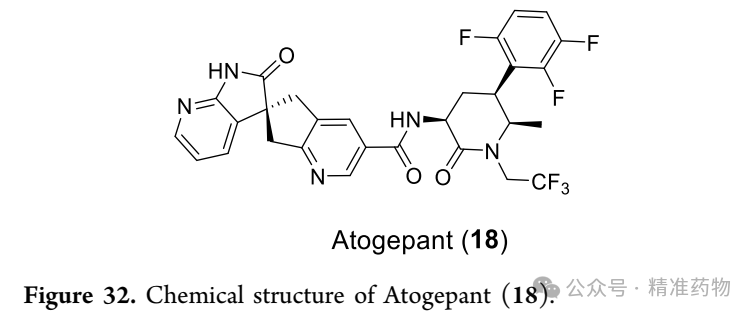

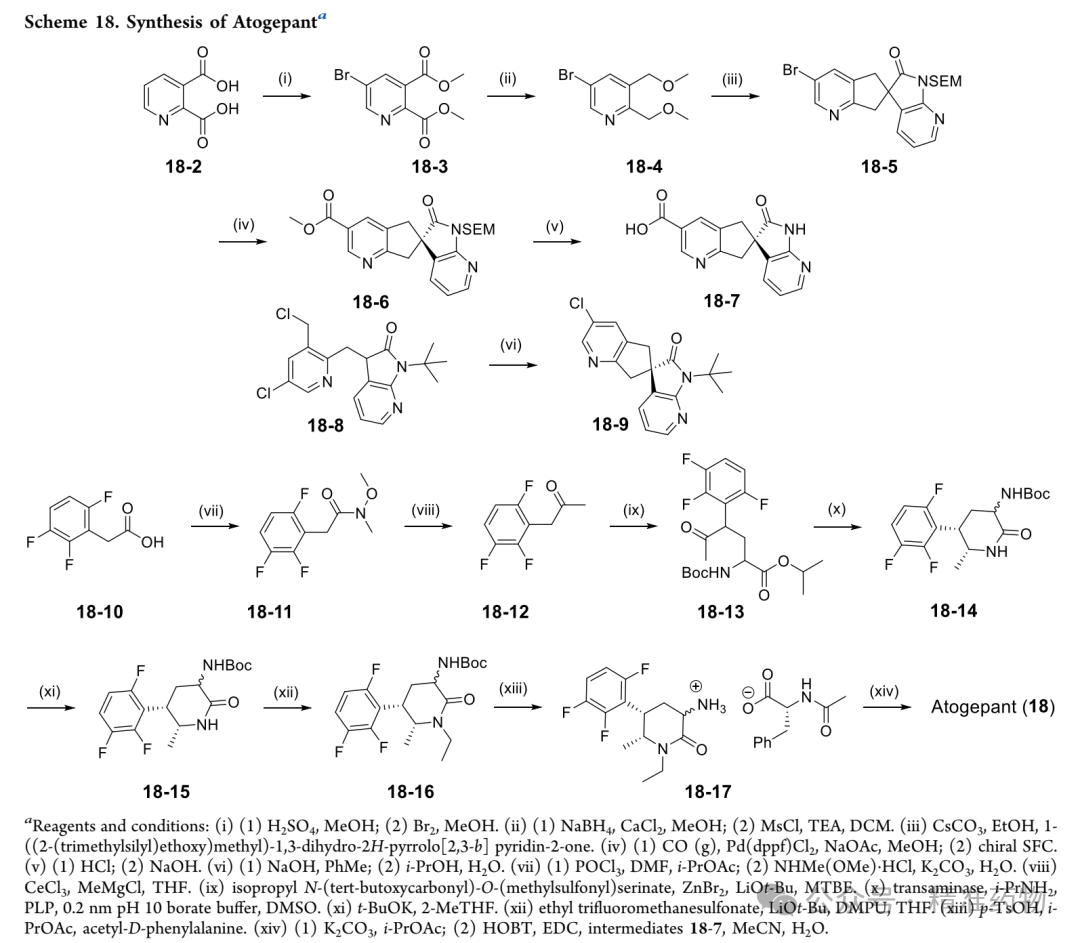

2.18 Atogepant (Qulipta)

Atogepant, an orally administered small-molecule CGRP receptor antagonist developed by AbbVie (formerly Allergan), was first approved by the FDA in 2021 for the preventive treatment of episodic migraine in adults. In 2023, its indications were expanded to include chronic migraine. By 2024, its sales reached $658 million, representing a year-over-year growth of 61.27%, ranking among the fastest-growing drugs in the CGRP class. The molecule maintains high-affinity blockade of the CLR/RAMP1 heterodimer receptor while improving oral bioavailability and metabolic stability through optimized spiro-piperidinone and cyclopropyl cyanobenzene structures. Available in three daily doses of 10/30/60 mg, a 12-week trial demonstrated a reduction of 4.0–4.2 monthly headache days from baseline, outperforming placebo without the need for titration. With no vasoconstriction contraindications, it can be safely used in patients with cardiovascular disease. Its core patent expires in 2034, and the company is advancing real-world studies, exploring higher-dose acute treatments, and developing sequential use strategies with biologics to consolidate its leading position in the "daily oral preventive treatment for migraine" niche market.

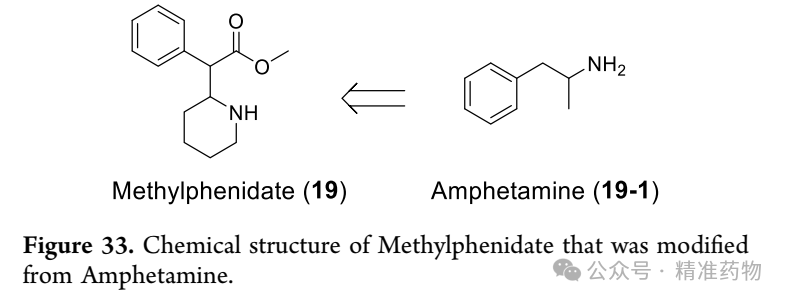

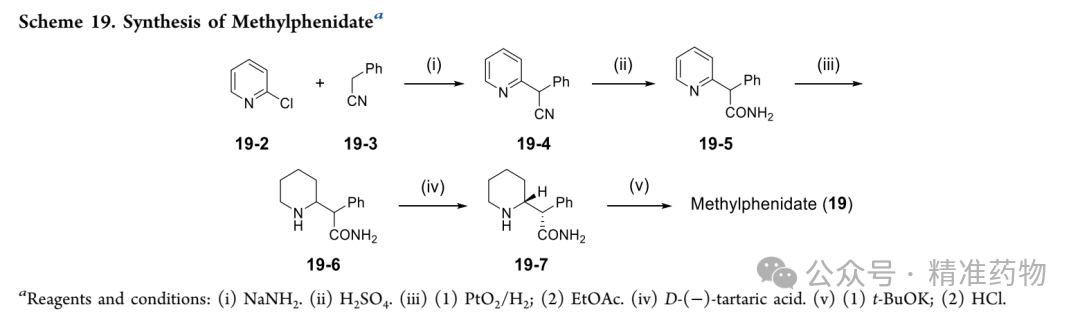

2.19 Methylphenidate (Concerta)

Concerta, a Johnson & Johnson osmotic pump-controlled long-acting methylphenidate formulation, was approved by the FDA in 2000 for attention deficit hyperactivity disorder (ADHD) in patients aged 6 and above. In 2024, its global sales reached $641 million, reflecting an 18.14% year-on-year decline primarily due to competition from high-quality generic drugs following the expiration of core patents, as well as the emergence of new non-stimulant alternatives. The molecule enhances prefrontal neurotransmitter levels by blocking the reuptake of dopamine and norepinephrine. Its OROS pump technology allows for once-daily morning dosing that sustains efficacy for 12 hours, improving symptom control throughout school/work while reducing rebound effects. Despite maintaining over 17 million prescriptions nationwide in 2022, ranking 32nd in the U.S., market growth has been pressured by the launch of generic dexmethylphenidate, lisdexamfetamine, and norepinephrine reuptake inhibitors. The company is leveraging its brand reputation, expanding indications from adolescents to adults, and implementing combination strategies with α2-agonists to slow market share decline while awaiting opportunities for differentiated extended-release improvements before certain dosage patents expire after 2027.

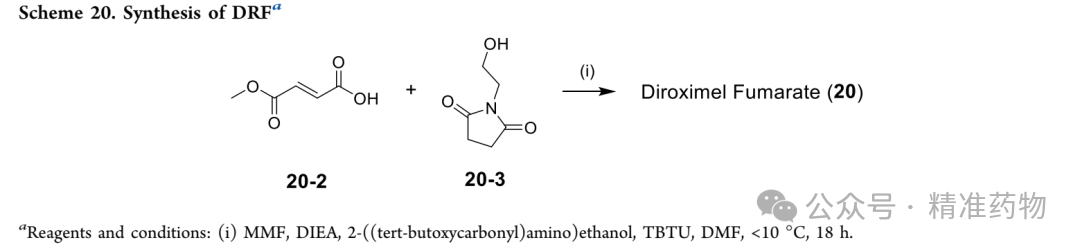

2.20 Dimethyl fumarate(Vumerity)

Dimethyl fumarateVumerity, an upgraded prodrug of dimethyl fumarate (DMF) launched by Biogen, was approved by the FDA in 2019 for relapsing multiple sclerosis (RMS). In 2024, its sales reached $628 million, a year-over-year increase of 9.03%, driven mainly by the substitution demand from patients intolerant to DMF. The molecular design esterifies monomethyl fumarate with branched-chain alcohol, which is then rapidly hydrolyzed by gastrointestinal esterases into the same active metabolite, MMF, while reducing local irritation caused by methanol and acrylic acid byproducts, decreasing upper gastrointestinal adverse events by 46% and lowering discontinuation rates by 75%. Phase III results showed that the annualized relapse rate was comparable to DMF, with superior cardiovascular safety, making it suitable for MS patients with hypertension or sodium intake restrictions. Core patent protection extends until 2034. The company is reinforcing its positioning as a "well-tolerated oral first-line DMT" through differentiated insurance coverage, real-world adherence data, and sequential strategies with novel high-efficacy therapies to delay generic competition.

Summary and Outlook

Neurological drugs offer both therapeutic value and commercial returns. The top 20 small molecule drugs by sales in 2024 are delivering efficacy to patients while providing companies with the funding needed for reinvestment in R&D. With the advent of patent cliffs and the iteration of next-generation high-efficacy drugs, the rankings will continue to evolve. New entries in 2024 include Trintellix, Briviact, Qulipta, and Vumerity, while former champions like quetiapine and fingolimod have exited the list. Looking ahead, unmet needs in Alzheimer's disease, Parkinson's disease, rare neurodegenerative conditions, and the intersection of oncology and neuroscience may give rise to new blockbuster molecules through platforms such as gene editing, RNA splicing modulation, deuterium technology, and targeted protein degradation. Meanwhile, policy changes in U.S. drug pricing and tariffs could profoundly impact the global market landscape, prompting companies to adopt more flexible strategies in innovation, cost control, and internationalization, thereby driving the evolution of neurological drug pipelines toward precision, safety, and affordability.

For detailed and comprehensive information, please refer to the original article.:

https://doi.org/10.1021/acs.jmedchem.5c03086

Disclaimer: The publication/reposting of this article is solely for the purpose of information dissemination, and does not represent the views of this WeChat Official Account or confirm the authenticity of its content. Any judgment made based on this content will be at your own risk.If there is any infringement, please inform us and we will delete it immediately!

Press and hold to follow this official account