Global MedTech 2018 Year in Review: MedTech Stocks Rise Overall, IPO Activity Surges

In February 2019, Evaluate published its annual report, “Review of the Pharmaceutical, Biotechnology, and Medical Technology Industries in 2018,” which analyzed the ups and downs of the global pharmaceutical, biotechnology, and medical technology sectors in 2018 from a global perspective and across multiple dimensions. VCBeat New Medicine (WeChat ID: biobeat1) has compiled and translated the report. Below is the section describing the medical technology sector:

Generally speaking, when a large number of healthcare stocks encounter problems, healthcare technology stocks remain a safe haven. In 2018, healthcare technology stocks indeed outperformed biotechnology stocks and even pharmaceutical stocks. However, the sluggish stock market in the fourth quarter still had a certain impact on healthcare technology stocks.

From the index of U.S.-listed health tech stocks, we have identified a common pattern: stock prices rise consistently until late September, followed by a significant decline at year-end. The European stock market presents a different picture: while stocks also declined in the fourth quarter, performance in the first three quarters was lackluster. It should be noted that our analysis covers only health tech companies whose revenue from diagnostic or innovative therapeutic sectors accounts for more than 40%.

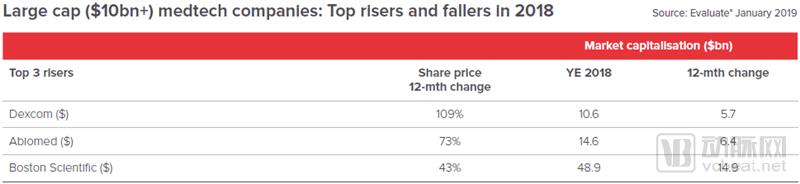

Dexcom, listed on the Nasdaq, recorded the largest single-stock price gain among large-cap companies, as its third-quarter market surge far outweighed the contraction in the fourth quarter. At the end of last year, the blood glucose sensor manufacturer saw its stock price rise by 109%, propelling it from a mid-cap to a large-cap company.

Dexcom’s stock price rise is mainly attributed to the launch of its G6 glucose monitor. Last March, the device became the second FDA-approved continuous glucose monitor that does not require regular manual calibration.

Top 3 Gainers and Losers in the Stock Market Among Large Healthcare Technology Companies (Market Capitalization > $10 Billion) in 2018

Generally, if a company engages in continuous acquisitions, shareholders need to consider whether this is a sign of declining sales. However, this is not the case with Boston Scientific. Over the past 12 months, the company has completed nine acquisitions, yet investors do not appear concerned; instead, they view these acquisitions favorably.

Even the acquisition of BTG at a $2.4 billion valuation did not unsettle Boston Scientific’s supporters. The deal’s valuation exceeded BTG’s 17-year historical average.

Surprisingly, Align Technology’s stock price was also among those declining. Since Evaluate began tracking the share prices of these major medtech companies, Align recorded the largest gain among large medtech firms in 2017, with its valuation more than doubling. However, last year could be described as one of the years marked by a significant drop in the company’s stock price. Align’s share price fell by 47% in the fourth quarter, whereas at the beginning of last year, it had declined by only 6%.

Overall, in 2018, the gains of large healthcare technology companies outweighed their losses. Only five companies saw a decline in market capitalization, with an average drop of 9%, which was lower than the 25% average gain observed in the rising group. Furthermore, compared to biopharmaceutical stocks, healthcare technology stocks experienced larger gains and smaller losses. Although 2018 remained a challenging year for large healthcare technology companies, their status as a “safe haven” in the stock market remained firmly intact.

Healthcare Technology Companies with Significant Stock Price Gains or Losses in 2018 (Ranked by Market Capitalization)

Tandem Diabetes Care, a small medical technology company, has seen its stock surge far outpace those of large pharmaceutical and tech firms, with an almost unbelievable record gain over the past 12 months. In 2018, the insulin pump manufacturer’s stock price soared by more than 1,500%, a milestone unlikely to be surpassed in the coming years.

Mid-cap stocks posted relatively steady gains. Haemonetics, a representative company in this segment, recorded a growth rate of only 75%, lagging behind large pharmaceutical and technology firms. However, by 2019, the market dynamics of this group may become more intriguing, as Tandem is likely to join the ranks of mid-sized medical technology enterprises.

Many factors have contributed to Tandem’s rise, but whether these are the fundamental drivers remains debatable. The company’s most significant product achievement last year was the U.S. approval of its t:slim X2 insulin pump in June, which drove a 25% surge in its stock price.

In October 2017, Animas, a subsidiary of Johnson & Johnson, exited the insulin pump market. This allowed Tandem to capture market share alongside numerous other diabetes device developers. However, Tandem secured a relatively high market share; among every 15,000 former Animas users with diabetes in the United States, approximately 3,000 became new Tandem customers.

Moreover, the primary reason for Tandem’s sharp stock surge may be its rebound from a trough. In November 2016, Medtronic’s artificial pancreas, the MiniMed 670G, received approval, causing Tandem’s share price to plummet by 60%. Tandem’s stock continued to decline thereafter, hitting rock bottom in early 2018. Although Tandem’s share price surged by 1,500% in 2018, it still had not returned to its peak level.

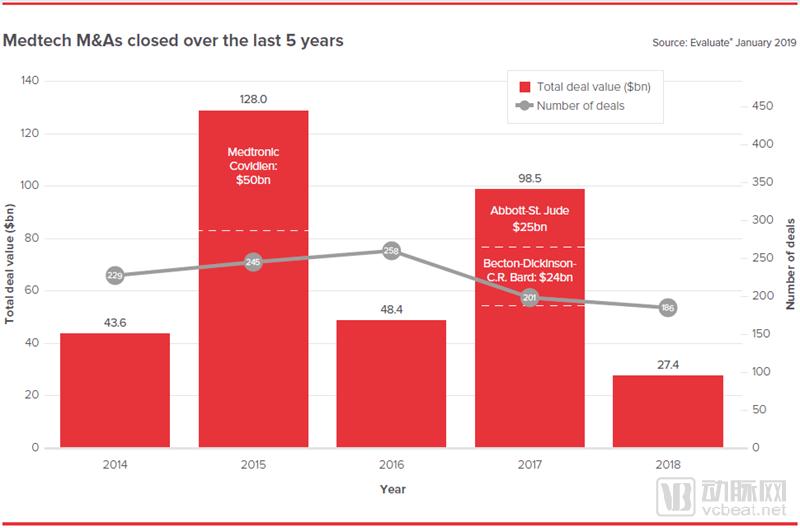

In 2018, M&A activity in the medical technology sector remained relatively subdued, with listed companies’ stock prices fluctuating in line with their market performance. M&A transactions in the medtech field dropped to their lowest level since 2013. Previously, in 2009, amid the outbreak of the global financial crisis, only 186 M&A deals were completed, marking the lowest level in a decade.

The total value of M&A transactions in 2018 amounted to only $27.4 billion, representing a significant decline from the nearly $100 billion recorded in 2017. Four of the top 10 M&A deals in 2018 were private equity acquisitions, further underscoring the sluggish performance of the large-scale M&A market for healthcare technology companies in the previous year.

M&A Scale in the MedTech Sector from 2014 to 2018 (Including Deal Count and Value)

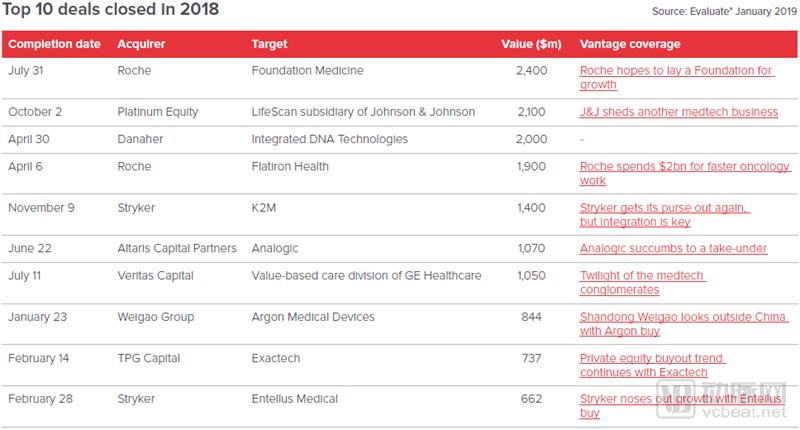

Private equity firms appear to be filling the void in the market for large-scale mergers and acquisitions in health technology. When selecting acquisition targets, large health technology companies are most averse to the high valuations and synergy challenges associated with such deals. Roche’s $2 billion blockbuster transactions for Foundation Medicine and Flatiron Health serve as typical examples. Both Foundation Medicine, a cancer diagnostics company, and Flatiron Health, an electronic health records analytics firm, possessed technologies that aligned well with Roche Group’s oncology portfolio.

However, the pickiness of healthcare technology companies regarding acquisition targets does not mean that more small-scale M&A deals will replace fewer large-scale M&A transactions.

In 2017, there were 19 M&A deals valued at over $1 billion, whereas this figure dropped to 7 in 2018, marking a significant decline in the number of such transactions. On the other hand, the number of smaller-scale M&A deals also decreased. In 2018, there were 34 deals valued at under $100 million, compared with 50 in the previous year. Of course, the above analysis only includes M&A transactions for which deal values were disclosed. Therefore, the actual number of transactions may differ. Nevertheless, it is undeniable that there has been a downward trend in the number of small-scale M&A deals since 2010.

In contrast, the number of M&A deals valued between $100 million and $1 billion has remained relatively stable over the past decade, with the 2018 M&A deal volume standing at a moderate level.

Number of M&A Transactions in the MedTech Sector from 2014 to 2018 (by Deal Value)

M&A trends are believed to be cyclical to some extent. As large-scale M&A deals are completed and the number of target companies declines, the M&A market gradually cools down. However, this does not fully explain the dramatic drop in both the volume and size of transactions in 2017 and 2018.

On the one hand, venture capital exits in the medical device industry are relatively easy, which means that private equity firms can appropriately delay large-scale M&A transactions.

On the other hand, private equity firms have been rapidly raising capital. Four major investment firms—Platinum Equity, Altaris Capital Partners, Veritas Capital, and TPG Capital—were the acquirers in ten of the largest M&A deals in 2018. In 2017, no M&A transactions by investment firms ranked among the top ten, while only one such transaction appeared in 2016. Among the acquisitions made by these four firms, the companies acquired by Platinum Equity and Veritas Capital were subsidiaries of large corporations, whereas Altaris Capital Partners encountered significant challenges in its acquisition of Analogic.

Given that private equity funds typically have a five-year investment exit horizon, it is reasonable to anticipate another wave of similar M&A transactions by private equity firms in approximately five years.

Top 10 M&A Deals Completed in 2018

However, in 2019, the business activities of two major imaging companies, Siemens Healthineers and GE Healthcare, were also worth watching. Siemens Healthineers has already spun off from its diversified industrial parent company, and GE Healthcare is also on the verge of a spin-off. We speculate that part of the reason for these companies’ separation from their parent organizations is to allow more specialized groups greater freedom to pursue acquisitions.

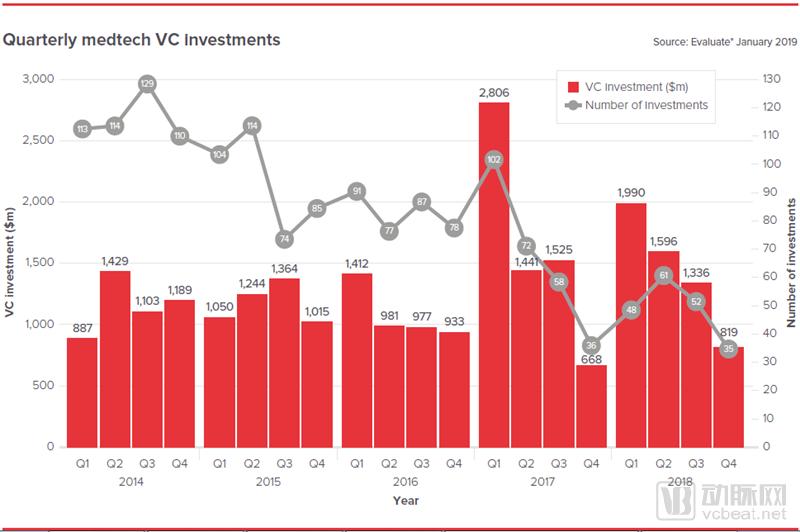

In 2018, fewer than 200 venture capital financing deals were completed in the health tech sector. Just as large health tech companies have raised their bar for evaluating potential acquisition targets, so too have investors tightened their criteria for corporate investments. In 2018, the number of venture capital deals by investment institutions fell below 200 for the first time.

The 196 venture capital deals closed in 2018 marked the lowest level in over a decade. However, the total funding amount remained relatively stable at $5.7 billion, second only to 2017 in the past five years. Notably, in early 2019, healthcare technology company Verily completed its first round of venture financing worth $1 billion, suggesting that the total value of venture capital deals in 2019 may surpass that of 2018.

Venture Capital Financing Secured by Healthcare Technology Companies, 2014–2018

Grail topped the 2018 rankings of healthcare technology company financings, securing $315 million in its Series B round and $300 million in its Series C round, ranking first and second, respectively. Also on the list was Helix, a consumer-focused genetics company whose flagship product is a $160 genetic test developed in partnership with the Mayo Clinic.

In March last year, the unicorn company Oxford Nanopore completed a new round of financing worth $140 million. In October, Oxford Nanopore again secured $66 million in equity financing from Amgen. However, the company’s business volume for 2018 is projected to be only $75 million, indicating that its push into the sequencing market still needs to gain significant momentum.

Top 10 MedTech Venture Capital Deals Completed in 2018

Sequencing technologies have attracted significant capital investment due to their relatively low development costs and lighter regulatory burden. Meanwhile, advances in machine learning enable rapid data screening, thereby delivering valuable insights. For instance, Roche acquired the genomic sequencing company Foundation Medicine for $2.4 billion; despite the substantial acquisition price, venture capitalists do not believe this deal will result in losses.

Since June 2016, Philips alone has acquired ten companies specializing in imaging, informatics, and other software services, while GE Healthcare has partnered with Nvidia.

Imaging technology has also remained a sector of strong interest to investors. In recent years, driven by AI, it has evolved from a relatively conservative field toward greater flexibility, advancement, and integration.

Due to the lower number of venture capital deals last year, the average funding amount per deal for healthcare technology companies reached as high as $30 million. In January this year, Verily secured a massive $1 billion venture capital round, indicating that there is virtually no chance of this average figure declining in 2019. Traditional medical device manufacturers and data-driven diagnostic companies demonstrate roughly equal capability in attracting venture capital investment.

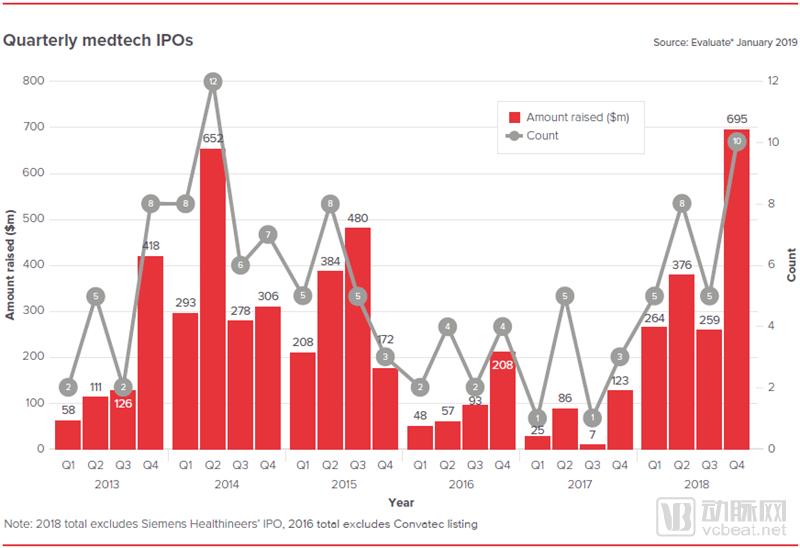

Last year, Siemens Healthineers set a new record for the largest IPO in the history of the healthcare sector, raising $5.1 billion. However, Evaluate’s analysis of medical device company IPOs excluded this mega-deal to provide a clearer view of the industry’s underlying trends, revealing some more intriguing patterns in the process.

Despite a sharp decline in stock prices at the end of last year, IPOs for health tech companies have set a new record. Medical device companies completed $695 million in IPOs, marking the highest quarterly total since we began tracking health tech company IPOs in 2013.

The summary of healthcare technology IPOs in the figure below focuses primarily on smaller companies with significant room for financing growth, excluding both Siemens Healthineers and Convatec, which went public in 2016 with a $1.9 billion valuation.

IPOs of Healthcare Technology Companies, 2013–2018

Last October, liquid biopsy company Guardant Health and neuromodulation-focused Axonics went public on the Nasdaq, ranking as the second and third largest IPOs among healthcare technology companies in 2018, respectively.

However, Guardant’s performance has significantly outpaced that of Axonics. Since its public listing, Guardant’s stock price has doubled. This success is attributed to the company’s partnership with AstraZeneca to develop Guardant360 as a companion diagnostic for the lung cancer drug Tagrisso. In early 2019, the FDA was set to review Guardant360 for diagnosing cancers of unknown primary origin, a development that also warrants anticipation.

Compared with Guardant, Axonics’ stock price has seen little change. Nevertheless, Axonics’ share price remains higher than that of most healthcare technology companies that went public in 2018: in 2018, 28 healthcare technology firms listed on the market, but only 12 saw their stock prices rise.

Top 10 Global Listed Medical Technology Companies in 2018

Among medical technology companies that went public in 2018, Inspire Medical Systems saw the largest stock price increase (164%). The company primarily provides systematic solutions for patients with sleep apnea. Last November, when releasing its third-quarter financial report, the company raised its full-year sales forecast. This growth was partly driven by insurance provider Aetna’s coverage of Inspire therapy. Although Aetna is not yet profitable, its net loss has narrowed since 2017.

In 2018, the potential IPO of Siemens Healthineers may have been the year’s headline news, but the recovery of the healthcare technology IPO market after a sluggish 2017 was an even more compelling story.

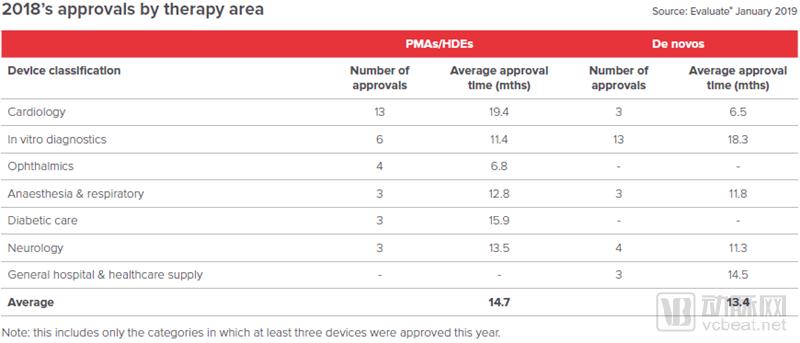

With the rise of de novo submissions, the number of high-risk medical devices approved by the FDA has also declined.

On the surface, only 35 new medical devices received FDA approval last year through the Premarket Approval (PMA) and Humanitarian Device Exemption (HDE) pathways, representing a significant decline from the 50 approvals granted in 2017. However, FDA approvals for low-risk devices have correspondingly increased.

U.S. regulators have actively encouraged manufacturers of novel medical devices to pursue the de novo classification pathway, and this approach appears to be yielding results: in 2018, the number of medical devices approved via the de novo route surpassed those approved through the more established Premarket Approval (PMA) and Humanitarian Device Exemption (HDE) pathways for the first time. As a new regulatory avenue, the de novo process has arguably accelerated the market entry of medical devices.

PMA is the primary pathway for FDA approval of high-risk or Class III medical devices; HDE is the main pathway for FDA approval of medical devices intended to treat rare diseases, which affect fewer than 8,000 patients annually in the United States; 510(k) requires only demonstrating that the device under review is substantially equivalent to legally marketed predicate devices; the De Novo pathway is applicable to more innovative medical devices with no prior predicates and moderate risk, thus exempt from PMA review.

However, although the FDA’s de novo pathway is intended to be faster than PMA approval, actual review times have far exceeded expectations. In 2018, the average time for FDA de novo approvals was 13.4 months, whereas approvals for PMAs and HDEs took approximately six weeks.

FDA Approval Times by Therapeutic Area in 2018

In the first few weeks of 2019, global stock markets remained relatively stable. However, whether this stability can be sustained for an extended period largely depends on macroeconomic issues beyond the industry itself.

Certainly, the continued heating up of M&A activity will be conducive to a rebound in biopharmaceutical stock prices. The large-scale acquisitions of Celgene, Loxo Oncology, and Tesaro have attracted significant attention from investors. However, whether M&A transactions can sustain their momentum largely depends on whether sellers are willing to accept lower valuations.

We anticipate an increase in mergers and acquisitions within the medical technology sector. Johnson & Johnson (J&J) acquired Auris Health for $3.4 billion in 2019, Siemens Healthineers has spun off from its parent company, and GE Healthcare is poised to do so shortly, meaning that two new potential acquirers will emerge in 2019.

But one thing is certain: the average size of venture capital financing in the medical technology industry will continue to rise in 2019. In January this year, Verily, a sister company of Google, completed a new round of financing worth $1 billion. Moreover, there are no signs of small-scale investments from venture capital; similarly, in the field of drug development, although VCs invested heavily in 2018, it does not affect their continued investment in this area in 2019.

The state of the IPO market will largely depend on broader stock market trends. To date, there has been little indication that investor interest in biopharmaceuticals and health technology is waning. Of course, given the stock market plunge last October, this situation could change rapidly, and companies seeking to go public will undoubtedly need to accelerate their pace.

This year, the issue of drug pricing will persist, with many executives at large pharmaceutical companies stating that raising drug prices will become increasingly difficult. Consequently, these major pharmaceutical firms are focusing on the size of their pipelines; companies with a greater number of innovative products will possess stronger market competitiveness. However, very few large companies boast robust pipelines. Therefore, those banking on this year’s M&A transactions to enrich their pipelines may have another reason for optimism regarding mergers and acquisitions.