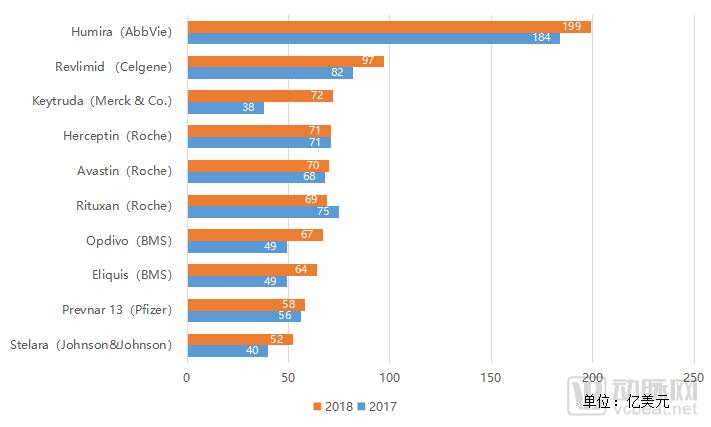

2018 Top 10 Best-Selling Drugs: Humira Secures Seventh Consecutive Crown, Keytruda Breaks into Top Three

Recently, EvaluatePharma compiled sales data for the top 10 best-selling drugs of 2018 based on annual reports from major pharmaceutical companies, and VCBeat’s biobeat1 provided an analysis of the data. Among the top ten drugs, seven are antibody-based therapies. The remaining three include two small-molecule drugs (Revlimid and Eliquis) and one vaccine (Prevnar 13). In terms of therapeutic areas, five of these drugs are primarily indicated for oncology, three for autoimmune diseases, one for cardiovascular disease, and one is a pneumococcal vaccine.

1. Humira (generic name: adalimumab)

Manufacturer: AbbVie

2018 Sales: $19.936 billion

Humira (Adalimumab) is a recombinant fully human monoclonal antibody against tumor necrosis factor alpha (TNF-α) developed by AbbVie. It is indicated for the treatment of various autoimmune diseases, including rheumatoid arthritis, ankylosing spondylitis, and psoriasis. In 2018, Humira unequivocally retained its title as the world’s best-selling drug, with sales nearing $20 billion—more than twice that of the second-place product. According to AbbVie’s 2018 annual report, the company’s total net revenue for the year was $32.733 billion, meaning Humira accounted for 60% of AbbVie’s total revenue. Since succeeding Plavix in 2012, Humira has remained the world’s best-selling drug for seven consecutive years.

As a drug that has been on the market since 2002, Humira is facing imminent expiration of its patent protection. At the end of 2016, the core U.S. patents for Humira expired, but AbbVie reached agreements with multiple generic drug manufacturers, successfully delaying the threat of biosimilars in the U.S. market until 2023. In 2018On October 16, the patent for Humira expired in the European market. To safeguard its position in the world’s second-largest pharmaceutical market, AbbVie decided to reduce Humira’s price in Europe by 80% through government tender procedures to compete with biosimilars. As a result, it is foreseeable that Humira’s sales volume in 2019 will likely be impacted by developments in the European market. Nevertheless, by maintaining its stronghold in the U.S. market, Humira is highly likely to retain its title as the world’s top-selling drug, although it may no longer sustain its growth trajectory.

2. Revlimid (generic name: lenalidomide)

Manufacturer: Celgene Corporation

2018 Sales: $9.685 billion

Revlimid (Lenalidomide) is a small-molecule drug developed by Celgene. Its mechanism of action involves targeting the inflammation-mediated factor TNF-α to inhibit tumor angiogenesis and stimulate T-cell activation, thereby achieving anti-tumor effects. Revlimid generated nearly $10 billion in sales in 2018, maintaining its position among the top-selling drugs. According to Celgene’s 2018 annual report, the company’s total net revenue for the year was $15.281 billion, with Revlimid accounting for two-thirds of this amount.

When it comes to Celgene, one cannot overlook the news revealed earlier this year that Bristol-Myers Squibb (BMS) intended to acquire Celgene for $74 billion. This acquisition is now facing opposition from some BMS shareholders. One of the reasons cited by these dissenting shareholders is the impending patent expiration of Revlimid. The U.S. patent for Revlimid is set to expire in 2024, meaning that BMS would only be able to benefit from Revlimid’s profits for five more years after acquiring Celgene. Given the lack of standout performance in Celgene’s other pipeline assets, some BMS shareholders believe that Celgene is not currently worth such a hefty acquisition price.

3. Keytruda (generic name: pembrolizumab)

Manufacturer: Merck & Co.

2018 Sales: $7.171 billion

Ranked third is Merck & Co.’s blockbuster drug, the PD-1 inhibitor Keytruda, a humanized monoclonal antibody. Since its initial approval, Keytruda has received FDA approval for 14 oncology indications. In February of this year, Keytruda was further approved as a treatment for renal cell carcinoma. As a first-line therapy for patients with advanced renal cell carcinoma, the FDA granted priority review to the combination regimen of Keytruda and Inlyta, with a decision expected by June 20, 2019. Since its market launch in 2017, Keytruda’s sales achieved breakthrough growth in 2018, generating $7.171 billion in revenue for Merck & Co., nearly double the $3.8 billion recorded in 2017. Keytruda also entered the Chinese market in September 2018.

Keytruda’s most significant competitor is BMS’s Opdivo. Although Opdivo was launched earlier, its sales have been surpassed by Keytruda due to a lag in approved indications.

4. Herceptin (generic name: Trastuzumab)

Manufacturer: Roche

2018 Sales: CHF 6.982 billion (approximately USD 7.1 billion)

Herceptin (trastuzumab) is a monoclonal antibody-based targeted therapy developed by Roche that targets the human epidermal growth factor receptor 2 (HER2). The FDA has approved it for the treatment of HER2-overexpressing metastatic breast cancer. As a blockbuster anticancer drug underpinning Roche’s performance, Herceptin has seen steady sales growth since its launch, reaching $7.1 billion in 2018. The biggest challenge facing Herceptin is patent expiration. The FDA has successively approved four biosimilars: Ogivri (Mylan/Biocon, December 1, 2017), Herzuma (Celltrion/Teva, December 14, 2018), Ontruzant (Merck/Samsung Bioepis, January 21, 2019), and Trazimera (Pfizer, March 12, 2019). Roche has employed combination therapies to mitigate the sales decline of its flagship product.

In the early days of the targeted therapy era, Roche shone brightly in the anti-tumor market, driven by the outstanding performance of three monoclonal antibodies: rituximab, bevacizumab, and trastuzumab. Since the launch of these three core monoclonal antibodies, sales have grown steadily, consistently ranking among the top five oncology products globally. This has generated substantial revenue for Roche and solidified its dominant position in the industry. However, due to multiple factors—including patent expirations, the market entry of biosimilars, and the rise of tumor immunotherapy—the growth of Roche’s three flagship products has slowed significantly, lagging far behind the 12% growth rate of oncology prescription drugs. Notably, Keytruda, a PD-1 inhibitor, has surpassed Herceptin to claim one of the top three spots.

5. Avastin (generic name: bevacizumab)

Manufacturer: Roche

2018 Sales: CHF 6.849 billion (approximately USD 7 billion)

Ranked fifth is Roche’s blockbuster drug, Avastin. Approved by the FDA in February 2004, it was the first anti-angiogenic agent approved for marketing in the United States.

Avastin was approved by the U.S. FDA on February 22, 2008, as a treatment for a range of cancers, with indicated indications including colorectal cancer, non-small cell lung cancer, glioblastoma, ovarian cancer, renal cell carcinoma, and cervical cancer. Due to its broad spectrum of indications and strong efficacy against multiple tumor types, Avastin rapidly became a blockbuster drug, generating over RMB 1 billion in revenue during its first full year on the market. Since 2013, its annual sales have hovered around USD 7 billion.

Among Roche’s three blockbuster drugs, Avastin is the only one originally developed by Genentech. However, in 2011, the U.S. Food and Drug Administration (FDA) withdrew its approval for the treatment of breast cancer because Roche failed to provide sufficient safety assessment data and the drug did not significantly improve overall survival in cancer patients. Despite this setback, Avastin still achieved $7 billion in sales in 2018, making it the only drug among Roche’s three major blockbusters to register sales growth. The FDA has already approved Amgen’s biosimilar to Avastin, which will soon face significant competition. Nevertheless, legal disputes surrounding Amgen’s Avastin biosimilar are still pending, with hearings scheduled for late 2019 or 2020; therefore, a market launch in 2019 is unlikely.

6. MabThera (generic name: Rituxan, rituximab)

Manufacturer: Roche

2018 Sales: CHF 6.752 billion (approximately USD 6.9 billion)

Roche’s other blockbuster product, Rituxan, experienced a decline in sales in 2018 and currently ranks sixth. Rituxan is the first monoclonal antibody for cancer treatment, targeting CD20, and is a chimeric IgG1 antibody. Rituximab was originally developed by IDEC Pharmaceuticals, which signed a collaboration agreement with Genentech in 1996 to jointly develop the product. It received FDA approval for market launch in 1997.

Rituximab has a broad range of indications, including non-Hodgkin lymphoma, chronic lymphocytic leukemia, rheumatoid arthritis, Wegener’s granulomatosis, and microscopic polyangiitis. Approximately five-sixths of rituximab’s sales revenue comes from oncology, while one-sixth comes from immunology. Its peak annual sales occurred in 2014, reaching $7.55 billion. To date, cumulative sales of rituximab have exceeded $90 billion (with data since 2002 reflecting only Roche’s figures).

The drug’s annual sales in 2018 amounted to $6.9 billion, down from $7.5 billion in 2017. As the key patent for this medication in the treatment of hematologic malignancies expired in the United States at the end of 2018, price-based competition is expected to intensify further in 2019.

It is reported that Teva’s and Celltrion’s Truxima received approval from the EMA and the FDA in July 2017 and November 2018, respectively. According to an agreement reached between the companies, Truxima is expected to be officially launched in the first half of 2019, although specific details of the agreement have not been disclosed. In China, Henlius’ rituximab biosimilar has also been approved for marketing. As of 2018, approximately 27 MabThera/Rituxan biosimilars were under development globally. In 2017, MabThera/Rituxan generated $4.4 billion in sales in the United States, nearly equal to the combined sales of Avastin and Herceptin. Compared with these two drugs, the patent expiration of MabThera/Rituxan is likely to impose the greatest financial impact on Roche in 2019.

7. Opdivo (generic name: Nivolumab)

Manufacturer: Bristol-Myers Squibb

2018 Sales: $6.7 billion

Opdivo is a PD-1 immune checkpoint inhibitor co-developed by Bristol-Myers Squibb of the United States and Ono Pharmaceutical of Japan. It is the first PD-1/PD-L1 agent marketed globally and the first PD-1 monoclonal antibody approved for marketing in China. The drug initially received FDA approval in April 2014 for the treatment of melanoma. To date, the FDA has approved nine oncology indications for Opdivo, including malignant melanoma, non-small cell lung cancer, head and neck cancer, renal cell carcinoma, classical Hodgkin lymphoma, urothelial carcinoma, colorectal cancer, gastric cancer, and hepatocellular carcinoma.

Bristol-Myers Squibb’s 2018 financial report revealed that Opdivo generated $6.735 billion in sales, accounting for 30% of the company’s total revenue. Leveraging its first-mover advantage, Opdivo initially captured a significant share of the oncology market and maintained a lead in sales volume. However, during the 2018 competition between PD-1/PD-L1 inhibitors, it was overtaken by Keytruda. This shift was primarily attributed to Keytruda’s rapid expansion of indications over the preceding two years, whereas Opdivo’s most recent indication update had been for metastatic colorectal cancer in September 2017.

8. Eliquis (generic name: apixaban)

Manufacturer: Bristol-Myers Squibb

2018 Sales: $6.4 billion

Eliquis is an oral Factor Xa inhibitor jointly developed by Bristol-Myers Squibb and Pfizer. By inhibiting Factor Xa, a key clotting protein, Eliquis reduces the production of thrombin and the formation of blood clots. Approved by the FDA in January 2013, Eliquis is indicated to reduce the risk of stroke and systemic embolism in patients with non-valvular atrial fibrillation. Considered an alternative to warfarin, the current standard of care, Eliquis reduces the risk of major bleeding by 31% and lowers the risk of death by 11%.

Pfizer’s 2018 financial report showed that Eliquis generated $3.434 billion in sales, while Bristol-Myers Squibb recorded $6.438 billion in sales for the same year, totaling $9.872 billion. Since its launch, Eliquis has seen continuous growth in sales volume, and its market share has surpassed that of rivaroxaban. According to the Eliquis patent information disclosed by Bristol-Myers Squibb, patents in the United States, Europe, and China are expected to expire in September 2022, indicating several more years of growth potential.

9. Prevnar 13 (Pneumococcal 13-valent Conjugate Vaccine)

Manufacturer: Pfizer

2018 Sales: $5.8 billion

Prevnar 13 is indicated for active immunization. It is the successor to Prevnar (the 7-valent pneumococcal vaccine launched in 2000) and prevents invasive disease caused by 13 pneumococcal serotypes (1, 3, 4, 5, 6A, 6B, 7F, 9V, 14, 18C, 19A, 19F, and 23F), as well as otitis media (ear infection) caused by seven pneumococcal serotypes (4, 6B, 9V, 14, 18C, 19F, and 23F).

In February 2010, Prevnar 13 received its initial FDA approval for use in infants and young children aged 6 weeks to 5 years. Subsequently, Pfizer expanded the indicated age range for Prevnar 13 to include adults, making it the first pneumococcal vaccine approved for use across the entire lifespan. Prevnar 13 entered the Chinese market in 2016.

Prevnar 13 is the most significant product Pfizer acquired when it purchased Wyeth Pharmaceuticals for $68 billion in 2009. Since its launch, it has become the best-selling vaccine in history and the most widely used pneumococcal conjugate vaccine globally, with 102 countries including it in their national childhood immunization programs. Meanwhile, Prevnar 13 has long been regarded by external observers as a blockbuster drug for Pfizer following the patent expiration of Lipitor. Although its sales performance has fluctuated across different countries, it has overall maintained a stable annual growth rate of approximately 3%.

10. Stelara (generic name: Ustekinumab)

Manufacturer: Johnson & Johnson

2018 Sales: $5.2 billion

Stelara is Johnson & Johnson’s blockbuster anti-inflammatory drug and a core product in its expansion into the autoimmune disease sector. It was first approved for marketing in the United States in 2009. As a monoclonal antibody-based anti-inflammatory agent, Stelara targets interleukin-12 (IL-12) and interleukin-23 (IL-23). Its currently approved indications include: (1) adolescent and adult patients aged 12 years and older with moderate-to-severe plaque psoriasis who are candidates for phototherapy or systemic therapy; (2) adult patients aged 18 years and older with active psoriatic arthritis, as monotherapy or in combination with methotrexate; and (3) adult patients aged 18 years and older with Crohn’s disease (CD) who have had an inadequate response to, lost response to, or were intolerant of prior therapies.

Stelara’s primary indication is psoriasis, a market crowded with competitors, including AbbVie’s blockbuster drug Humira, which has topped the global best-selling drug list for multiple consecutive years. Additionally, Novartis’s Cosentyx and Eli Lilly’s Taltz have also been approved for the treatment of psoriasis in adults. Despite this competition, Stelara has maintained strong market performance, achieving a sales growth rate of over 30% in 2015. In 2017, Stelara generated $4.011 billion in sales. According to forecasts by the pharmaceutical market research firm EvaluatePharma, Stelara’s global sales are projected to reach $6.466 billion in 2024.