Domestic OCT Devices Lead Import Substitution with Over RMB 1 Billion in Capital Inflows—How Far Is Full Disruption of Foreign Monopoly?

“Over the past two years, the development of OCT devices in China has been rapid. We have made estimates that the total market investment should now exceed 1 billion yuan,” an investor told VCBeat.

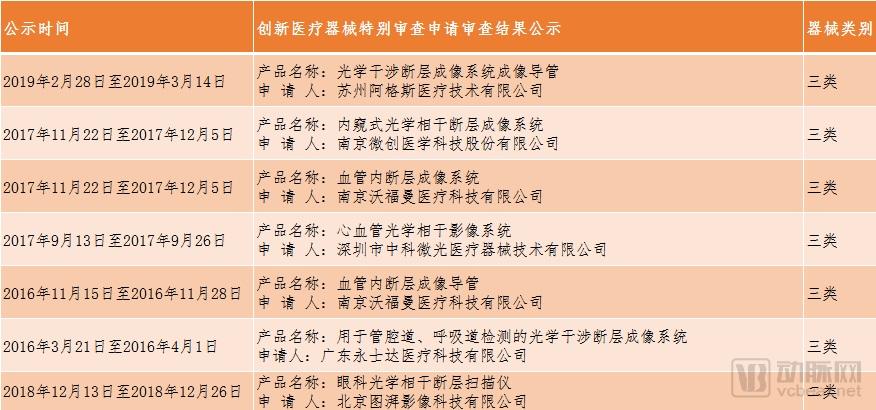

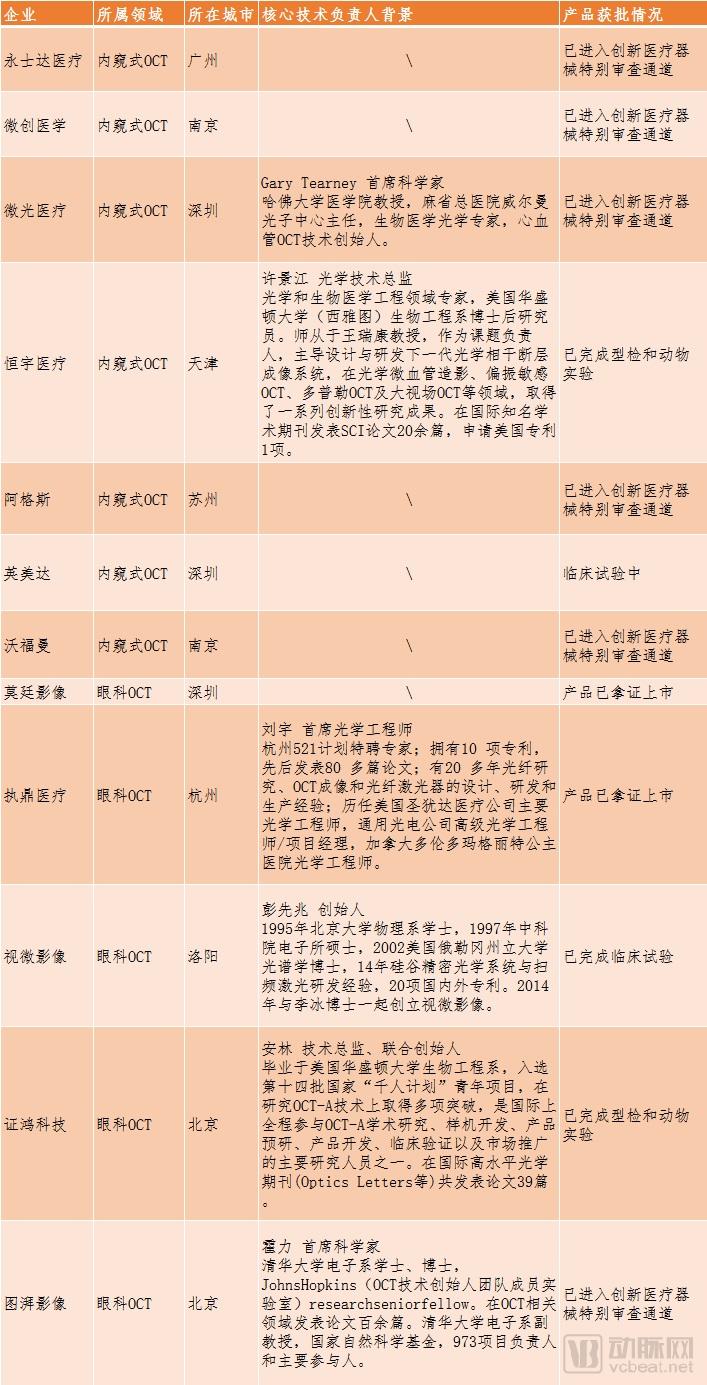

Between 2016 and 2019, a total of seven OCT (Optical Coherence Tomography) projects entered the special approval process through the innovative medical device special review channels administered by the Center for Medical Device Evaluation of the National Medical Products Administration and local drug regulatory authorities:

Source: Center for Medical Device Evaluation, National Medical Products Administration, and Local Medical Products Administrations

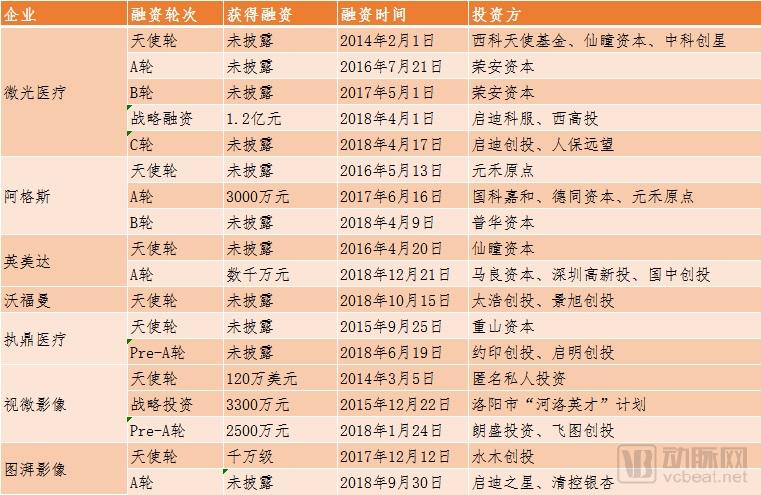

Correspondingly, over a three-year period, mainstream companies in the OCT sector secured 14 rounds of financing. Public records indicate that seven companies received funding. Notably, Weiguang Medical raised RMB 120 million in a strategic financing round in April 2018.

Data sources: VCBeat database, Tianyancha, and the companies themselves

It is evident that OCT is emerging as a significant force in the field of innovative medical devices. Capitalizing on this momentum, many companies have championed the cause of import substitution, aiming to capture market share from overseas giants such as Heidelberg Engineering, Carl Zeiss Meditec, and Topcon. However, this path is far from smooth. How can domestic OCT manufacturers break through the strong hold of foreign brands in terms of technology and market presence? After conducting extensive consultations, VCBeat has uncovered some answers.

What Exactly Is OCT?

Before delving into the specifics of the OCT market, it is essential to first understand the historical background behind the emergence of this technology.

As light-sensing organs, the eyes form images by projecting light onto the light-sensitive retina, where it is received and converted into signals that are transmitted to the brain via the optic nerve. It is through this mechanism that humans are able to read, appreciate visual art, and navigate the vast world around them.

The eyeball comprises the ocular coats, intraocular cavities and contents, nerves, blood vessels, and other tissues. It is a complex and delicate structure, yet vulnerable to disease. This small organ is frequently affected by various conditions, including glaucoma, optic neuropathy, and cataracts.

To study ophthalmic diseases, ingenious humans have invented various fundus examination tools.

In 1851, the German scientist Hermann von Helmholtz invented an instrument called the ophthalmoscope, which can be regarded as the first-generation device for fundus examination. Prior to this, physicians could only examine the eye using a magnifying glass. With this new instrument, doctors were able to clearly visualize the blood vessels on the retina and the optic nerve (which transmits information between the eye and the brain) located at the back of the eyeball. It was precisely the invention of the ophthalmoscope that truly established ophthalmology as an independent medical discipline.

In the early 1990s, the direct ophthalmoscope became an important tool for ophthalmologists in fundus examination.

In 1955, Zeiss (Carl Zeiss) developed the Zeiss-Nordenson Netzhautkamera, a novel ophthalmoscope capable of capturing authentic and clear fundus photographs, thereby evolving the ophthalmoscope into the fundus camera. This innovation can be regarded as the second-generation tool for fundus examination.

Third-generation fundus detection tools emerged in the 1990s. At the 1990 ICO-15 SAT conference, a two-dimensional image of the horizontal meridian of the living human fundus, based on the principle of white-light interferometric depth scanning, attracted widespread attention. In 1990, Professor Naohiro Tanno of Japan conducted further research on this approach, followed by a professor at Yamagata University in Japan. These studies enabled Optical Coherence Tomography (OCT) technology to achieve micrometer-level resolution and millimeter-level penetration depth, as well as the capability to generate cross-sectional images. Since then, it has become an important imaging technique for biological tissues.

In 1993, the first-ever in vivo imaging of retinal structures using optical coherence tomography (OCT) technology was achieved in human history.

OCT can acquire surface and subsurface images of transparent or opaque materials, with image resolution comparable to that of a miniature microscope. It is an optical technique analogous to ultrasound imaging, providing cross-sectional images by detecting light reflected from tissues.

Compared with other imaging technologies, OCT can provide morphological images of living tissues with micron-level resolution; therefore, it has become a highly attractive cutting-edge technology in the medical field.

How large is the OCT market?

According to an OCT industry practitioner, ophthalmic OCT currently accounts for approximately 65% of the total OCT market. This is because OCT was applied in ophthalmology about 10 years earlier than in cardiology. The imaging depth and resolution of OCT are well-suited to ocular structures, resulting in a higher degree of compatibility with the diagnosis of eye diseases, while also being a non-invasive examination. Therefore, in the diagnosis of ophthalmic conditions, ophthalmic OCT is difficult to replace by other devices in many aspects.

As early as 20 years ago, Carl Zeiss introduced ophthalmic OCT devices to the Chinese market and conducted market education. Currently, nearly all tertiary hospitals in China are equipped with OCT devices, and their adoption is gradually expanding to secondary hospitals.

According to an OCT practitioner, the price of ophthalmic OCT equipment ranges from 300,000 yuan to 2 million yuan, with significant price differences depending on product positioning.

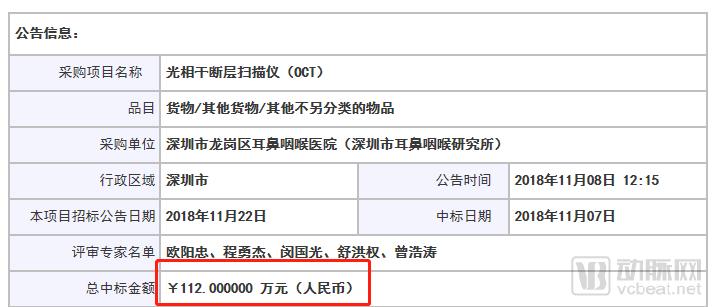

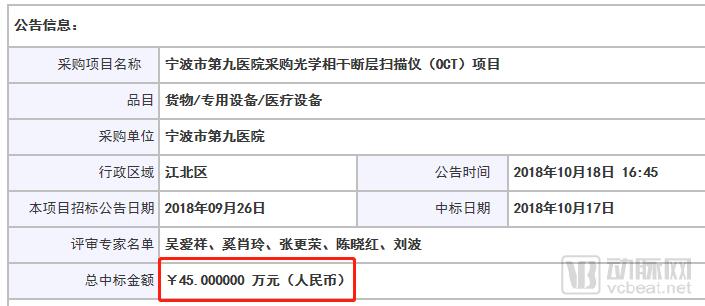

A glimpse can also be gained from the public information on the China Government Procurement Network:

Currently, imported equipment accounts for 95% of the ophthalmic OCT market share, holding an absolute monopoly. The suppliers with the largest market shares include Zeiss, Optovue, Topcon, and Heidelberg.

Based on the current usage in tertiary hospitals, we have roughly estimated the market size for ophthalmic OCT devices:

From the perspective of the existing market, the total installed base of OCT systems in China was approximately 7,500 units in 2018, with annual sales volume ranging from 1,500 to 2,000 units.

From the perspective of incremental market growth, current hospital demand for ophthalmic OCT devices exhibits two major characteristics:

1. Multiple growth drivers: the markets for Tier 1 and Tier 2 hospitals, private hospitals, and health checkup centers are expanding rapidly.

2. Rapid equipment turnover, with tertiary (Grade A) hospitals replacing equipment every 4–5 years and secondary hospitals every 6–7 years.

Therefore, we project that the total installed base of OCT systems in China will exceed 35,000 units in 2025, with annual sales surpassing 6,000 units.

With the continuous innovation and development of human medical technology, interventional therapy is being adopted by an increasing number of patients and healthcare providers. Interventional therapy refers to a procedure in which a small puncture is made in an artery in the patient’s hand or leg, through which a guidewire and microcatheter are inserted. The guidewire is advanced through the blood vessels to the site of occlusion within the coronary arteries. A balloon or mesh stent is then deployed over the guidewire to dilate the obstructed segment, restore blood flow to the heart, and thereby achieve therapeutic cure.

This therapy offers numerous advantages, including rapid action, non-invasiveness, minimal trauma, quick recovery, low cost, and repeatability. It can promptly address coronary artery stenosis and alleviate myocardial ischemia, thereby significantly reducing patient mortality. Cardiovascular patients undergoing interventional therapy experience fewer complications, benefit from convenient postoperative hemostatic compression, and are able to walk out of the operating room immediately after the procedure, with minimal impact on their daily lives thereafter.

It is also understood that the significant curative effects of interventional therapy rely on the support of high-performance imaging technologies. Currently available imaging modalities include coronary angiography (CAG), coronary CT, cardiac MRI, intravascular ultrasound (IVUS), and intravascular optical coherence tomography (OCT), with OCT being the latest generation and most cost-effective option among them.

Although not as widespread in ophthalmology, endoscopic OCT represents another important direction for future development. Currently, the use of OCT is primarily centered around percutaneous coronary intervention (PCI). The number of PCI procedures has increased year by year, reaching nearly 670,000 cases in 2016 (data source: The 20th National Forum on Interventional Cardiology, National Health Commission).

During PCI procedures, OCT catheters and OCT systems are required. According to survey data from Probe Capital, taking 2016 as an example, assuming a 5% penetration rate of OCT catheters in PCI procedures, the market size for OCT catheters would approach RMB 500 million. Assuming a 50% penetration rate for OCT systems, the market size could reach RMB 1 billion.

Chart source: Probe Capital

Who are the major OCT players in China?

Based on their respective disciplines, domestic OCT companies are primarily divided into two major categories: ophthalmic OCT and endoscopic OCT. The following provides an overview of the major OCT companies in China:

Weiguang Medical, founded in 2012 and headquartered in Nanshan District, Shenzhen—known as China’s Silicon Valley—specializes in optical coherence tomography (OCT) technology. With over a decade of technical expertise, the company holds multiple patents in sub-millimeter endoscopic optical imaging. Currently, Weiguang Medical has established strategic partnerships with the Chinese Academy of Sciences and Harvard Medical School, focusing on cutting-edge research in interventional imaging technologies. It is a national high-tech enterprise integrating R&D, manufacturing, and sales.

Weiguang Medical has been dedicated to innovation in imaging devices for cardiovascular interventional procedures, boasting over a decade of technical expertise in laser medicine and interventional devices. The company launched China’s first clinical-grade cardiovascular Optical Coherence Tomography (OCT) system and venous visualization instrument, and has established long-term strategic partnerships with the Chinese Academy of Sciences, the Chinese PLA General Hospital, and Harvard Medical School. Currently, multiple products have entered the registration application and clinical trial stages. Its flagship cardiovascular OCT device targets the lack of precise imaging solutions for cardiac surgeries in the Chinese market, striving to accelerate the localization of high-end medical imaging equipment.

The company’s core team comprises top-tier scientists, engineers, and medical professionals from Tsinghua University and the Chinese Academy of Sciences. As a pioneer in intravascular imaging for cardiovascular diseases in China, founder Zhu Rui was honored as the “Annual Technological Innovation Figure” at the 2017 CCTV Science and Technology Awards Ceremony. Since its establishment, the company has secured over RMB 40 million in funding from multiple domestic venture capital firms.

Weiguang Medical’s Cardiovascular 3D-OCT System and Surgical Guidance Interface

Currently, the clinical trials for Weiguang Medical's flagship products have been successfully completed, and multiple other intravascular imaging and interventional therapy products under development are progressing as scheduled. Construction of the Xi'an Silk Road Headquarters is set to commence, with official operation expected by June 2019.

Tianjin Hengyu Medical Technology Co., Ltd. (hereinafter referred to as “Hengyu Medical”) is an innovative company focused on intravascular imaging. The company specializes in the research and development, production, and sales of cardiovascular optical coherence tomography (OCT), intravascular ultrasound (IVUS), and intravascular multimodal imaging technologies. It is reported that Hengyu Medical possesses over 2,700 square meters of laboratory and production facilities, including more than 600 square meters of Class 10,000 cleanrooms compliant with Good Manufacturing Practice (GMP) standards.

Image source: Hengyu Medical

Hengyu Medical has fully mastered the core technologies of intravascular optical coherence tomography (OCT) systems through technological accumulation and collaboration. These technologies include miniature optical probe technology, endoscopic catheter technology, high-sensitivity interferometer systems, high-speed optical drivers, and core algorithms tailored for cardiovascular OCT imaging, for which relevant patents have been filed. Compared with other products, Hengyu’s system offers advantages such as rapid scanning speed, excellent catheter trackability, and suitability for transradial artery procedures.

It is reported that Hengyu Medical’s OCT system has completed type testing and animal studies. As the lead research institution, the Second Affiliated Hospital of Harbin Medical University has obtained ethical approval and will formally begin patient enrollment in the near future.

Toupai’s Sigma series of OCT products are domestically produced swept-source OCT devices developed entirely with Toupai Imaging’s proprietary technology, supporting OCT angiography (OCTA) functionality. Compared to previous-generation spectral-domain OCT, swept-source OCT offers faster scanning speeds and greater imaging depth, resulting in improved patient experience, clearer choroidal imaging, and fewer motion artifacts in OCTA images. The product is expected to obtain regulatory approval and be officially launched this September.

Since 2017, TopEye Imaging has successively established academic collaborations with renowned medical institutions such as Beijing Tsinghua Changgung Hospital and Peking Union Medical College Hospital, continuously refining the functional details of its products. After more than two years of market research and feedback, TopEye Imaging has formulated a practical and feasible market operation strategy and assembled an expert-level team of market operation consultants.

In addition to establishing long-term and amicable partnerships with downstream medical institutions, Topview Imaging is also continuously refining its collaborations with upstream suppliers of raw materials and components. These experiences are invaluable and constitute another significant advantage for Topview Imaging over other market entrants in the future.

Overtaking on the Bend: Technology Follow-up – Swept-Source OCT, IV-OCT

To capture market share from foreign companies, it is essential for domestic OCT enterprises to achieve leapfrog technological development and even surpass their competitors. Based on the current R&D status of various players, Chinese-made OCT has already achieved parity in core technologies and leads in certain areas.

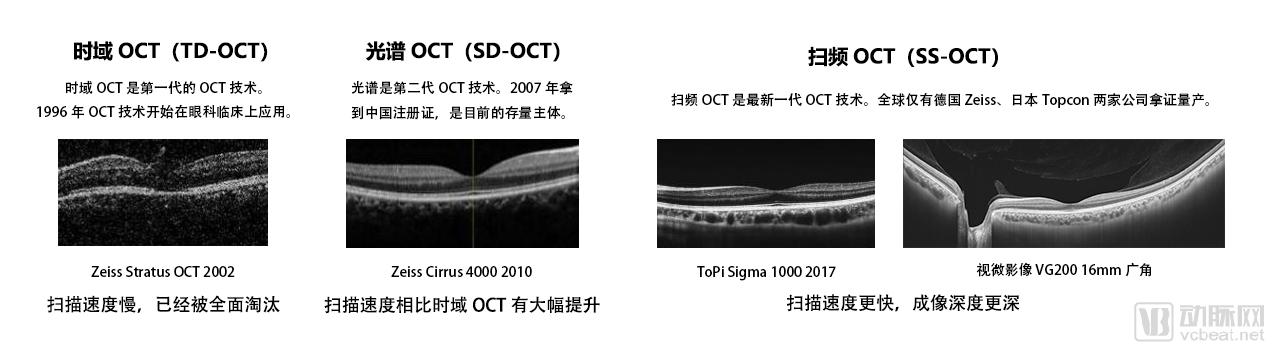

Academically, OCT is typically classified into three generations: the first generation is time-domain OCT (TD-OCT); the second generation is spectral-domain OCT (SD-OCT), a type of Fourier-domain OCT; and the third generation is swept-source OCT (SS-OCT), also belonging to Fourier-domain OCT. Swept-source OCT is the technology employed in the latest-generation products from major international companies such as Carl Zeiss and Topcon. To remain competitive, Chinese OCT manufacturers—including MicroView Medical, ToupTek Imaging, and SightMicro—have independently developed and adopted this technology.

Comparison of Three Generations of OCT Technology

The low level of integration between optical systems and software algorithms has resulted in mediocre imaging quality for existing domestically produced OCT devices. Data provided by Vismed Imaging indicates that its products utilize the latest swept-source technology, surpassing Carl Zeiss’s high-end OCT product, the Cirrus 5000, in core parameters such as scanning speed, scan range, and imaging depth, with significantly superior imaging quality.

Currently, the world’s most advanced commercial ophthalmic OCT system is the Zeiss Plex Elite 9000, with a scanning speed of 100,000 A-scans per second. According to official data, Visum Imaging’s VG200, which is about to receive regulatory approval in China, offers twice that speed, achieving 200,000 A-scans per second, along with a wider scanning range. This advancement is akin to upgrading CT scanners from 64-slice to 128-slice models, or MRI systems from 1.5T to 3.0T.

In addition to the iteration of core technologies, dual-mode integration has also become a new direction for OCT technology in the past two years.

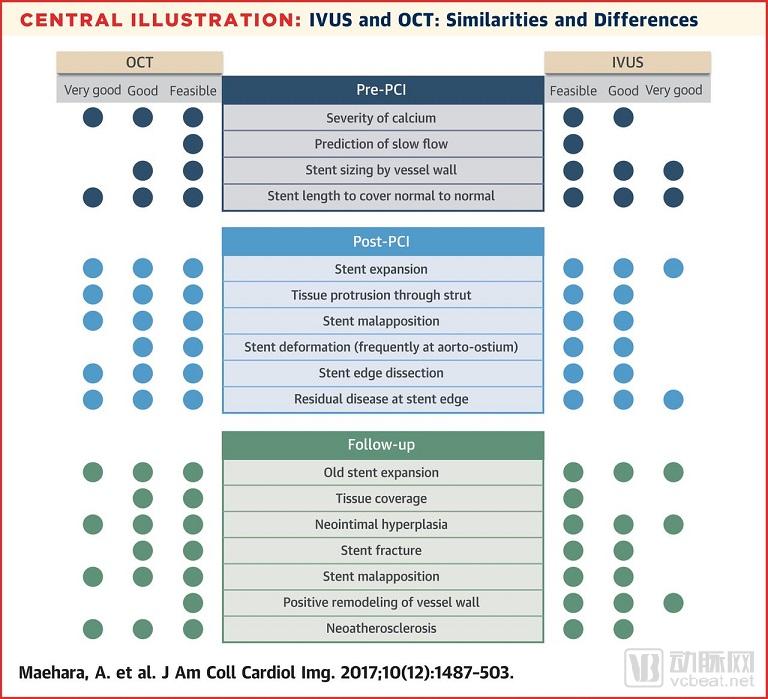

Both optical coherence tomography (OCT) and intravascular ultrasound (IVUS) are commonly used intravascular imaging modalities for guiding percutaneous coronary intervention, offering substantial clinical value. Their applications include: pre-procedural lesion assessment, selection of appropriately sized and lengthened stents, optimization of stent expansion, detection of acute complications, and follow-up to identify mechanisms of late stent failure (such as late stent thrombosis, neointimal hyperplasia, incomplete stent apposition/expansion, and stent fracture), among others.

Image source: Yingmeida official website

Due to the differing technical principles of these two imaging modalities, intravascular ultrasound (IVUS), which is based on ultrasound imaging, offers greater imaging depth and range but lacks image clarity; whereas optical coherence tomography (OCT), which is based on optical imaging, provides high-resolution images but has limited imaging depth and range. Their respective technical advantages in clinical applications also differ. IVUS demonstrates significant advantages in pre-PCI assessment of plaque burden, stent selection, post-PCI evaluation of stent expansion and edge assessment, as well as in follow-up for neointimal hyperplasia and positive remodeling. In contrast, OCT shows distinct advantages in pre-PCI assessment of calcified plaques, post-PCI evaluation of stent apposition and edge dissection, and monitoring of stent apposition during follow-up.

Clinical studies have demonstrated that IVUS and OCT each have their own advantages and disadvantages, exhibiting complementary characteristics. The advent of dual-modality IVUS-OCT systems enables physicians to acquire both types of images simultaneously, providing richer imaging information during percutaneous coronary intervention (PCI) and thereby enhancing the precision of diagnosis and treatment.

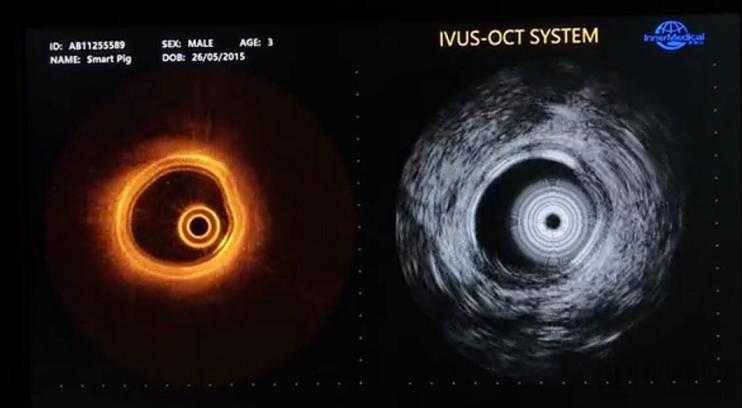

In March 2018, Shenzhen YMD Medical Technology Co., Ltd. developed an ultra-high-speed dual-modality imaging system combining intravascular ultrasound (IVUS) and optical coherence tomography (OCT). This system simultaneously enables both IVUS and OCT imaging modes, achieving a frame rate of 200 frames per second and completing a full scan in just 2–3 seconds. Reportedly, this imaging speed approaches the theoretical limit for dual-modality cardiovascular imaging systems, making it one of the fastest dual-modality imaging systems worldwide.

Image source: Angmed official website

Through independent R&D, Yingmeida has achieved technological breakthroughs in multiple core components, including disposable dual-modality imaging probes, high-speed ultrasound modules, laser optical modules, and high-speed imaging systems. Notably, the dual-modality probe used in this system has a diameter of only 1.05 mm (integrating both IVUS and OCT elements within it), which is consistent with the diameter of single-modality IVUS probes.

Image source: Yingmeida official website

Currently, China’s intravascular imaging equipment relies entirely on imports. Yingmeida’s IVUS-OCT dual-modality imaging system is poised to achieve technological leadership over existing foreign clinical devices, enabling domestically produced equipment to surpass international competitors through innovative advancement.

In addition to Intuitive, Hengyu Medical, mentioned earlier, is also engaged in the research and development of intravascular multimodal imaging technology.

According to Zhao Shiyong, General Manager and Co-founder of Hengyu Medical, OCT and IVUS each have their own advantages. OCT is currently the optimal method for identifying stent apposition, stent intimal tears, intimal coverage of stents, assessing plaque characteristics, and recognizing thin-cap fibroatheromas. However, the limitation of OCT lies in its shallow penetration depth, which is only 1 to 2 millimeters. In contrast, while IVUS has lower resolution, its penetration depth can reach 4 to 5 millimeters. Dual-modality imaging combines the respective strengths of OCT and IVUS, balancing high resolution with imaging depth, while also reducing the cost of combined OCT+IVUS imaging.

While dual-modal imaging is undoubtedly a hot topic, some industry practitioners have voiced differing opinions.

Zhu Rui, Associate Researcher at the Xi’an Institute of Optics and Precision Mechanics of the Chinese Academy of Sciences and Chairman of Weiguang Medical, stated, “I believe that the future direction is not to integrate OCT and IVUS into a single catheter. Although their functions are complementary, technical factors would lead to a compounding of their respective drawbacks—for instance, diminishing OCT’s high-speed scanning capability and IVUS’s contrast-agent-free advantage—while simultaneously increasing device costs and burdening patients.”

Zhu Rui believes that OCT and IVUS largely overlap in their clinical functions, making it difficult to achieve a synergistic “1+1>2” effect. Therefore, from the perspective of clinical needs, intravascular imaging should integrate structural and functional assessments. For instance, combining OCT with FFR or IVUS with NIRS to achieve an integrated approach of functional and structural imaging represents the future direction of intravascular imaging.

For innovative medical device companies, while keeping pace with technological advancements is important, self-sufficiency in core components is the key to controlling the market.

Taking ophthalmic OCT as an example, the equipment requires a wide variety of raw materials and components. The upstream industry is primarily the optical communications sector, which presents extremely high professional barriers and includes a range of optical components such as reflectors, filters, polarizers, and optical lenses. Downstream industries include hospitals, clinics, research institutions, and optical shops, among others. Hospitals represent the most core application scenario. According to industry insiders, China currently performs well in software algorithms, with the primary gap lying in hardware.

Wang Yingqi, CEO of Topvue Imaging, stated, “Compared with foreign companies such as Carl Zeiss, domestic OCT manufacturers lag behind in the finer aspects of optoelectronic technology. Currently, there is a general technological gap between domestic and overseas suppliers; while Carl Zeiss can achieve a score of 10, domestic suppliers may reach at most a 7. Consequently, there is a noticeable difference in user experience between the two. The root cause lies in the incomplete domestic optoelectronic industry chain and the scarcity of high-quality industry talent.”

TopRay is one of the very few companies in China that possesses the design and R&D capabilities for core components of OCT systems, including swept-source lasers, interferometry systems, and data acquisition cards. Wang Yingqi stated, “TopRay’s mid-range products have achieved full localization. However, certain core components of its high-end products still rely on imports.”

Overtaking on a Curve Market Strategy: Building Brand Equity in the High-End Segment, Driving Volume in the Mid-to-Low-End Segments

Many investors in the innovative medical device sector believe that, at the product level, the gap between Chinese and foreign companies will continue to narrow, akin to the smartphone industry, due to the globalization of supply chains. The primary disparity between domestic OCT companies and their international counterparts still lies in their operational and sales systems.

Yan Yi, Vice President of Shuimu Ventures, who has many years of experience in medical device investment, feels deeply about this point: “The current situation we have witnessed is that many early- to mid-stage innovative medical device projects often find it easy to secure financing before obtaining regulatory approval, but face greater difficulties after obtaining the certificate.”

The reason is that the market potential for a product before regulatory approval is full of imagination; whoever achieves the first domestic substitution seems to obtain a pass to the market. However, after obtaining the certificate, the sales channel of the product becomes a realistic issue.

It is understood that a mature medical device product typically requires a comprehensive marketing and sales system for support. Companies must not only employ professional marketing personnel for promotion and operations but also secure high-quality distributors across China. Otherwise, if the product fails to sell, the company will generate no cash flow, making it difficult to secure further financing. This represents a core gap between Chinese and foreign innovative medical device companies.

Yan Yi stated, “Distributors differ from agents in that they focus more on cultivating relationships with hospital management. Agents, by virtue of their financial capacity, also possess certain market promotion capabilities. For instance, agents in Hunan Province are responsible not only for maintaining expert relationships within the province but also for conducting brand promotion and publicity for relevant products throughout Hunan.”

Therefore, innovative medical device companies often need to establish a network of approximately 20 distributors across China, which poses a significant challenge for startups. In contrast, foreign enterprises, having entered the market earlier and possessing substantial financial resources, typically have well-established distributor networks. Furthermore, they employ mature management systems that effectively manage personnel and train sales teams on best practices for product promotion and related activities.

For these reasons, innovative medical device companies in China, including those specializing in OCT, must secure government support in addition to building robust operational and distributor teams if they are to truly scale up and strengthen their market position. Otherwise, engaging in direct head-to-head competition with foreign enterprises will be far from easy.

OCT is one of the essential diagnostic and screening devices for ophthalmic diseases. With the emergence of anti-angiogenic drugs in ophthalmology, the demand for OCT in this field continues to grow. After years of market cultivation by foreign companies, hospital acceptance is no longer an issue; the real challenge lies in brand building for domestic enterprises.

Peng Xianzhao, founder of Weimo Imaging, stated, “In the past, domestically produced medical devices often followed a low-end import substitution strategy. However, Weimo Imaging aims to provide Chinese physicians with high-end products that surpass the performance of imported equipment, enabling Chinese experts to showcase more advanced technologies from China on the international stage.”

In this regard, Wang Yingqi, CEO of Topview Imaging, expressed a similar view: “The medical sector in China is relatively closed, as evidenced by the fact that top-tier physicians and experts hold the vast majority of influence. Therefore, companies must adopt an expert-oriented mindset when developing products. Currently, most enterprises in the ophthalmic OCT field have underperformed, primarily due to issues with their own products, which encompass various factors including technology and user habits.”

Based on expert logic, the strategy previously employed by some companies to capture the primary-care hospital market with low-end products presents significant issues. Since key opinion leaders (KOLs) are primarily based in tertiary hospitals, they are generally less price-sensitive. Only by securing their acceptance and endorsement of a company’s products can manufacturers ensure that physicians at lower-tier hospitals are willing to adopt them.

Therefore, companies must have high-quality products to compete with imported flagship equipment. Products need to feature academically innovative functions so that experts will recognize the company’s technology and brand. Only with a strong brand image can effective promotion be achieved. Otherwise, the product will lack foundation, making it difficult to drive market adoption.

“Tier-2 hospitals and primary care facilities will never confidently purchase products from an unfamiliar brand, nor will they buy simply because the product appears to offer high performance at a low price,” said Wang Yingqi.

Given the current market landscape, OCT devices require a top-down marketing strategy. Companies should first penetrate select Tier 3A hospitals with high-end innovative products; leveraging the endorsement from these prestigious institutions, they can then drive volume through mid- or low-end products to capture a broader market. This approach has gained recognition among many domestic innovative medical device companies.