Tencent-Led Funding Round Fuels Waterdrop's Surge as Alibaba, JD, and Didi Enter the Fray Amid Fierce Competition in China's Lower-Tier Markets

Recently, Shuidi Inc. announced the completion of its Series B financing round, led by Tencent, with participation from GaoRong Capital, IDG Capital, BlueRun Ventures, and other investors, raising nearly RMB 500 million. Reportedly, this is the largest financing deal in the internet health insurance and health protection sector since 2018. Shuidi’s substantial fundraising has reignited industry discussions on online mutual aid and internet insurance businesses.

When an industry suddenly captures attention, it is usually due to one or more of the following factors: entry by major players that invigorates the market; massive financing rounds that signal an emerging high-growth sector; innovative business models that reconfigure resources; significant policy initiatives reflecting top-level design priorities; or high-profile events that amplify the industry’s visibility. The online mutual-aid model appears to align with several of these criteria simultaneously, sparking intense discussion among both business-to-business (B2B) and consumer-facing (B2C) stakeholders.

Online mutual aid platforms, a model that is not exactly “new,” emerged around 2014. Pioneered by innovative companies such as Anti-Cancer Commune, e-Huzhu, Quark Alliance, and Bihu Huzhu, which have persisted for many years, and later joined by tech giants like Alibaba, Tencent, JD.com, and Didi, the sector has once again become a hotspot in the “Internet + Healthcare” industry.

How Online Mutual Aid Models Work; Which Companies Are Entering This Sector, What Their Business Forms and Operational Data Look Like; How to Address Platform Homogenization and Implement Viable Business Models; How Ordinary Individuals Should Choose Mutual Aid Plans and How They Compare to Commercial Health Insurance. A Comprehensive Guide to the Evolution of Online Mutual Aid Platforms.

For those new to online mutual aid platforms and mutual insurance, the first step is to clarify the definitions of both.In simple terms, a mutual aid plan is a form of grassroots mutual assistance and solidarity; it is not insurance.Mutual insurance is an insurance product operated by insurance companies and sold to specific groups or individuals.

The Origins of the Mutual Aid Platform Model: Ancient examples can be found both in China and abroad, representing a contract imbued with humanitarian spirit. In ancient times, when clan consciousness was strong, ancestral halls served as the basic units of social operation. Clans possessed ancestral assets used to provide livelihood support for widows and orphans within the community. Abroad, maritime peoples engaged in long-term offshore operations faced high risks; before setting sail, crew members would pool a certain amount of money. If a member failed to return, these funds were used to support their children. These practices can all be regarded as the origins of the mutual aid model.

In the internet era, netizens have replaced “ancestral halls” and “fishermen,” forming communities of shared interest that embody the functions of social assistance and public welfare charity, while also enabling members to receive compensation for losses when necessary. Online mutual aid platforms first emerged in China in the form of QQ groups and forum-based groups, lacking established management structures and relying solely on administrators for operation. Kang’ai Gongshe (Anti-Cancer Community) and e-Huzhu were among the earliest online mutual aid platforms in China.

Furthermore, regarding mutual insurance, the law has long provided explicit provisions. The "Interim Measures for the Supervision of Mutual Insurance Organizations," issued in February 2015, states that mutual insurance refers to an insurance activity wherein entities or individuals with homogeneous risk protection needs become members by entering into contracts and paying premiums to form a mutual aid fund. This fund assumes liability for compensating losses caused by incidents specified in the contract, or assumes the responsibility of paying insurance benefits when the insured dies, suffers disability or illness, or meets other conditions agreed upon in the contract, such as reaching a certain age or time period.

Mutual insurance holds a significant share in the global insurance market. Sun Zhengcheng, a master’s supervisor at Yunnan University of Finance and Economics, cited statistics from the International Cooperative and Mutual Insurance Federation (ICMIF), stating that from 2007 to 2015, the premium growth rate of mutual insurance organizations reached 20.02%, far exceeding the global average premium growth rate of 8.3%. Their market share increased from 24.1% to 26.3%. In 2015, the total assets of global mutual insurance organizations amounted to US$7.8 trillion, providing insurance services to 988 million policyholders worldwide and creating 300,000 jobs.

The most significant differences between mutual aid platforms and mutual insurance lie in the nature of coverage and cost structure. Funds contributed by members of mutual aid platforms constitute unilateral donations; consequently, when a member seeks compensation, there is no guarantee of receiving the anticipated risk protection. In contrast, mutual insurance provides legally binding coverage, ensuring that policyholders receive the insured amount as stipulated in the contract.

Regulators have also focused their oversight on non-compliant advertising and inducement practices by online mutual aid platforms. They pointed out that, on one hand, these platforms seriously mislead consumers, make compensation promises that are difficult to fulfill, and fail to safeguard consumer rights; on the other hand, inadequate risk control measures can easily trigger financial risks.

The development of online mutual aid platforms is driven by two fundamental factors: First, medical expenses, particularly those for critical illnesses, represent a significant financial burden for Chinese households. Many families are overwhelmed by these costs, leading to poverty caused or exacerbated by illness, which in turn drives them to seek hope through social assistance. Second, the advancement of the internet and mobile internet has accelerated information dissemination, improved capital management efficiency, and bridged the distance between individuals.

China’s current healthcare security system features a structure with urban and rural medical assistance as the safety net, basic medical insurance as the primary component, and commercial health insurance as supplementary coverage. While basic medical insurance provides fundamental coverage for over 95% of the population, its limited scope fails to fully meet people’s healthcare needs. Meanwhile, although commercial health insurance is emerging rapidly, it accounts for less than 5% of total medical expenditures, indicating significant room for future growth.

During his press conference, the Premier also stated, “It must be recognized that while our basic medical insurance system provides universal coverage, its benefit levels remain modest. This is particularly challenging for farmers, whose per capita annual income is less than RMB 15,000, making it extremely difficult for them to bear the financial burden of serious illnesses on their own. Therefore, the government and society must join forces to alleviate this hardship affecting people’s livelihoods.”

The 2019 Government Work Report also stated: Continue to raise the coverage levels of basic medical insurance for urban and rural residents and critical illness insurance; increase the per capita fiscal subsidy for resident medical insurance by RMB 30, with half allocated to critical illness insurance; lower and standardize the deductible threshold for critical illness insurance, and raise the reimbursement rate from 50% to 60%, thereby further alleviating the medical burden on patients with critical illnesses and individuals in financial difficulty.

Major Disease Medical Insurance is funded by the government, which allocates a certain proportion or amount from the Basic Medical Insurance for Urban Residents and the New Rural Cooperative Medical Scheme funds as capital for Major Disease Insurance. In accordance with the principles of balancing revenue and expenditure and ensuring break-even operations with minimal profits, commercial insurance institutions are, in principle, selected through government tendering to administer Major Disease Insurance. Premiums are accounted for separately to ensure fund security and solvency.

Miao Jianguo, Deputy Director of the Medical Consortium Office at Baotou Central Hospital, mentioned in an interview with VCBeat that local authorities are currently engaging with commercial insurance providers to purchase critical illness insurance for residents, thereby alleviating the operational pressure on the basic medical insurance system. Plans are also underway to establish dedicated service windows within medical institutions to facilitate the settlement of critical illness medical insurance claims.

In fact, whether in countries with national health insurance systems (such as the UK and Germany) or in those where commercial health insurance dominates (such as the United States), commercial health insurance constitutes an important component of social security. Meanwhile, online crowdfunding and charitable donations are also widespread. Similar to Chinese platforms such as Aixin Chou, Shuidichou, and Qingsongchou, the United States has GoFundMe, where medical-related fundraising accounts for approximately one-fifth of total funds raised (with other categories including education, charity, and public welfare).

What exists is reasonable. From charity fundraising to online mutual aid, and further to mutual insurance and even commercial insurance, these models have a foundation for creating value because they meet the needs of different groups. In terms of user composition, these models share overlapping audiences while also reflecting iterative demand. For instance, individuals who contribute to charity fundraising may also be users of mutual insurance or commercial insurance.

Therefore, we observe that platforms such as Waterdrop and Qingsongchou offer both charitable fundraising and mutual aid programs. Charitable fundraising provides emergency financial relief, while mutual aid programs serve as a preventive measure. At a higher level, commercial medical insurance offers more comprehensive protection. This structure aligns with Maslow’s hierarchy of needs, progressing from basic survival to security assurance, and finally to loss compensation.

Table 1: Overview of Domestic Charity Fundraising and Online Mutual Aid Platforms

Data Source: VCBeat Database, Business Registration Records

From a developmental timeline perspective, the online crowdfunding model emerged earliest. The aforementioned U.S.-based platform GoFundMe was launched in 2008, while domestic platforms such as Aixin Chou, Shuidi Chou, and Qingsong Chou were established around 2013. The core of the online crowdfunding model lies in “authentic personal stories” and “empathy.” Both in the United States and China, fundraising campaigns are disseminated through social networks, which not only provide endorsement of authenticity but also evoke empathy by highlighting the fundraising needs of people within one’s social circle.

Following the online fundraising model, mutual aid plans emerged as the next major trend, with operating entities often being the same platforms that previously facilitated fundraising. 2016 marked the inaugural year for the development of the mutual aid model; business registration data showed that at that time, there were as many as one hundred platforms operating mutual aid plans.

Among the most lauded stories is that of Water Drop Mutual: in April 2016, even before preparing a business plan, Water Drop Mutual secured RMB 50 million in financing, with investors including Tencent, Meituan, IDG, Gaorong Capital, and ZhenFund.

2017 was a period of continued deep cultivation for the mutual aid model, and by the second half of 2018, the entry of industry giants had once again brought this model into the spotlight.

l On October 16, 2018, Trust Mutual Life Insurance Society joined forces with Alipay to launch “Xianghubao,” which later transitioned into the mutual aid platform “Xianghubao.”

l On November 13, 2018, JD.com and Zhonghui Property Mutual Insurance Association (hereinafter referred to as “Zhonghui Mutual”) launched “JD Mutual Insurance,” which was taken offline after a gray-scale test.

l On January 2, 2019, Didi launched "Dian Di Xiang Hu," entering the online mutual aid business.

It is worth noting that Alibaba and JD.com initially launched “mutual insurance” products rather than online mutual aid plans; however, they subsequently changed their nature or delayed their launch due to regulatory, operational, and other factors. Currently, the mutual insurance institutions approved in China are Trust Mutual Life Insurance, Zhonghui Mutual Property Insurance, and Huiyou Mutual Property Insurance. The former focuses on life insurance, while the latter two specialize in property insurance, forming the foundation of mutual insurance products.

He Bin, a special researcher at the Center for Public Policy Research of the Chinese Academy of Social Sciences, pointed out to VCBeat that Ant Financial should be a competitive market player by leveraging Trust Mutual Life’s mutual insurance license. However, the launch of “Xianghubao” indeed involved regulatory violations conflicting with the Insurance Law, as it resembled more of an online mutual aid platform endorsed by insurance. Therefore, he considers its transformation into “Xianghubao” under timely regulatory intervention to be a relatively reasonable outcome.

As for the differences between “Xianghubao” and platforms such as Shuidi Huzhu and Qingsong Huzhu, He Bin believes that there is no essential distinction between them, as they are all mutual aid plans. Of course, from a product perspective, there are indeed some differences in scale, technology, or operational aspects. However, they all belong to the same category of mutual aid platforms. Apart from differences in insurance endorsements and funding backgrounds, the only other distinction is that Shuidi Chou adopts a pre-payment model, whereas Xianghubao uses a post-payment model.

He Bin further pointed out that online mutual aid platforms can and need to develop in compliance with regulations. They can address the personalized mutual aid needs of users. The background behind their emergence is quite simple: there has long been a lack of such service platforms in China, whereas these types of mutual aid platforms are very common abroad. Moreover, the mobile internet era has lowered customer acquisition costs and barriers to entrepreneurship.

Regarding external evaluations of mutual aid platforms, they should be divided into three parts:

First, professionals generally hold a relatively positive view of such organizations, provided they operate in compliance with regulations;

Second, the evaluation from government regulators. The current regulatory environment is relatively lenient, although the bottom line of regulation must be upheld. This was also reflected in the transformation of Alibaba’s “Xianghubao” into “Xianghubao.”

Third, public opinion is subject to varying interpretations; from the perspectives of institutional operations or industry management, it is generally treated as a factor influencing goodwill.

The operational model can be analyzed from two perspectives: first, whether the mutual aid plan itself carries a risk of insolvency; and second, whether the operating platform generates sufficient revenue to ensure sustainable operations. The sustainability of the platform’s operations warrants further elaboration. For instance, products backed by large institutions, such as Xianghubao, may face no financial distress. Moreover, they can generate revenue by driving traffic to other business lines, thereby offsetting losses in one area with gains in another.

Whether it is Water Drop, Qingsongchou, or Xianghubao, their specific operational models all involve members joining in advance and applying for mutual aid upon the onset of a disease. The mutual aid amount is shared equally among all members, while the platform retains a portion as investigation fees (management fees) to ensure the authenticity and validity of claims. For this model, two indicators are crucial: first, the number of members—the larger the membership base, the lower the individual share; second, the member morbidity rate or the mutual aid application rate—the lower this indicator, the lower the shared amount.

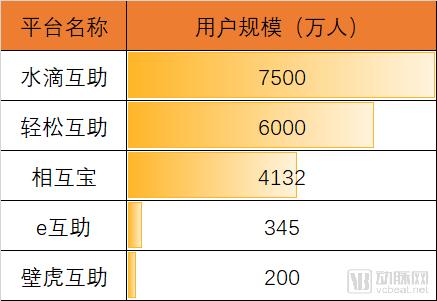

Table 2: Statistics on User Scale of Selected Mutual Aid Platforms

Data Source: Official websites of respective companies, as of March 2019

In terms of user base, Shuidi, Qingsong, and Xianghubao constitute the absolute first tier, with Shuidi holding a distinct leading advantage. Xianghubao’s ability to attract over 40 million users within just six months underscores its significant growth potential. When including smaller platforms, the total number of users enrolled in mutual aid plans in China is estimated to approach 200 million. Furthermore, mutual aid plans are mutually exclusive, meaning that members cannot claim benefits from multiple platforms simultaneously; consequently, there is limited user overlap among the major platforms.

To continuously attract new users to their programs, major platforms have adopted two primary strategies: one is the “one person, one family” model, whereby an individual enrollee can extend coverage to other family members (such as parents, spouses, and children); the other is targeting lower-tier markets, seeking opportunities in the vast third-, fourth-, and fifth-tier cities as well as township markets.

Regarding the development of lower-tier markets, Shen Peng, founder and CEO of Waterdrop Inc., once stated: “In a village with over 300 residents, if one person purchases Waterdrop’s services and receives compensation after falling ill, many others will come to trust it. Initially, only one or two people in the village might have signed up for Waterdrop Mutual Aid, but once a claim is paid out, the majority of villagers will accept it. This is the dissemination model, which exhibits certain network effects.”

For audiences in "lower-tier markets," basic medical insurance coverage is already extensive, yet out-of-pocket expenses for critical illnesses remain largely uncovered, often depleting decades of household savings. With market education and adoption of commercial health insurance still incomplete, mutual aid models offer a supplementary option beyond both public medical insurance and commercial health plans. In the future, third- and fourth-tier cities as well as township markets will be key areas for expanding membership in mutual aid programs.

For users looking to join mutual aid plans, there is little difference in the product systems of leading platforms, and no significant gap in costs. Shuidi Mutual Aid and Qingsong Mutual Aid operate on a pre-paid model with subsequent deductions; based on the author’s experience, the monthly per-person shared cost for Shuidi is approximately RMB 2. Xianghubao incurs even lower expenses, with reporters noting that total payments since its launch amount to only RMB 0.04.

Table 3: Product System of the Mutual Aid Platform

Data source: Company official website. Please refer to the specific terms for details.

Notably, mutual aid platforms have begun to establish a presence in the internet insurance sector. For instance, Shuidi Bao, under the Shuidi ecosystem, was launched in May 2015. By the end of October 2018, Shuidi Bao had established deep collaborative partnerships with nearly 50 well-known insurance companies in China, offering nearly 60 high-cost-performance premium insurance products and covering approximately 8 million users. Qingsong Company operates the “Qingsong e-Bao” internet insurance platform and has formed synergies with Xianghubao and Alipay’s “Hao Yi Bao” series of products.

We can view internet-based fundraising, mutual aid plans, and commercial medical insurance as a “three-stage rocket.” Internet-based fundraising generates traffic through networks of personal acquaintances; mutual aid plans retain this traffic and establish alliances based on shared risks; the retained traffic is further consolidated, ultimately generating revenue for the platform through commercial medical insurance and health products. Meanwhile, this can also be seen as a “funnel” model, progressing layer by layer to identify and fulfill user needs.

Regarding the sustainable operation of the mutual aid model, Wang Xi, Vice President of Wei Yi Bao, believes that there are significant challenges, mainly in two aspects: First, the platform itself has operating costs, such as marketing, verification of the authenticity of mutual aid applications, situation surveys, and claims processing; second, under the mutual aid model, as members age, the overall incidence of diseases increases, meaning that the shared cost will rise. At this point, younger individuals with lower disease incidence rates will withdraw from the mutual aid plan, making it impossible to achieve a virtuous cycle.

“Mutual aid plans are often associated with the essence or origins of insurance; however, mutual insurance is more commonly applied in property and casualty insurance rather than in life and health insurance. Medical and critical illness insurance is highly complex, and the level of sophistication in mutual aid plans still needs improvement. Small and medium-sized platforms lack sufficient risk resilience, which may challenge the future coverage provided to mutual aid members,” said Wang Qian.

As a senior expert in life insurance, Wang Xi advocates for insurance products with stronger coverage capabilities and clearer policy terms. However, she also points out that the mutual aid model has raised public awareness of disease risks at a minimal cost (just a few yuan or tens of yuan), which is commendable. In the future, platforms need to make greater efforts to promote correct insurance concepts. Meanwhile, relevant authorities should strengthen regulatory oversight of the mutual aid model.

Cao Weicai, a life insurance professional, told VCBeat that for online mutual aid platforms to achieve long-term operations, the core requirement is to ensure a sufficient membership base. According to the law of large numbers, a larger number of members results in lower individual contributions per incident, whereas a smaller membership base leads to significantly higher individual costs. To increase membership, mutual aid platforms must operate in a standardized, open, and transparent manner, strictly avoiding any black-box operations and ensuring they do not become tools for embezzling membership fees.

Specifically, first, it is recommended that third-party institutions participate in supervision to ensure reasonable expenditures and transparent fee structures, while regularly disclosing financial status, membership details, and other information required for public transparency. Second, it is advisable to charge operational fees on a proportional basis to guarantee the necessary operational expenses of the mutual aid platform. Third, the platform can leverage its membership resources to collaborate with merchants, provide value-added services, enhance interactive engagement with members, and improve member stickiness.

Whether through charitable fundraising, mutual aid plans, or commercial health insurance, the objective is to achieve psychological security and financial compensation for losses incurred in the event of illness. Only with robust regulatory frameworks, responsible operators, and sustainable business models can the goal of “ensuring medical access for all patients” be ultimately realized.