Assessing the Economics of Specialty Healthcare Chains: Beyond the Illusion of Beauty

How the Capital Market Views Specialty Hospital Chains

Is Healthcare a Good Business?

Since 2015, the healthcare services sector, particularly specialized chain clinics, has remained highly active. In the primary market, fields such as dentistry, medical aesthetics, ophthalmology, and pediatrics have secured substantial private equity financing. Listed companies have begun establishing healthcare services M&A funds or directly transitioning into the broader health industry, while a variety of new players—such as real estate developers, financial institutions, and internet companies—have flocked to enter the market.

The general sentiment toward healthcare services is optimistic, with the sector viewed as counter-cyclical and characterized by ample, stable, and sustained cash flows. However, the specialized chain clinic segment of the healthcare services industry, despite its appealing appearance, has unique characteristics and is subject to stringent regulation. Compared with other industries, it faces four major challenges:High investment, slow returns, long cycles, and difficult exit。

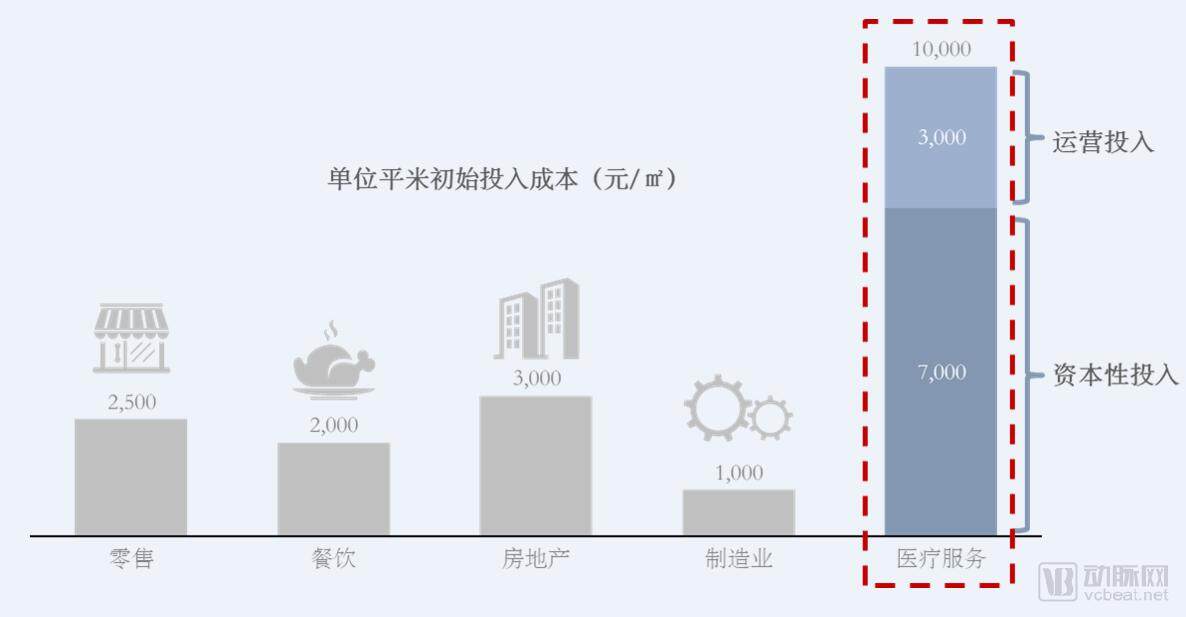

1. High investment:In terms of investment per square meter across different industries, the healthcare services sector requires significantly higher capital outlay per square meter than retail, food and beverage, real estate, and manufacturing. Establishing medical institutions entails substantial one-time capital expenditures (CAPEX), including renovation and equipment procurement (with even higher per-square-meter costs if land acquisition and construction are factored in). Meanwhile, ongoing operational management is equally critical, necessitating sustained operational expenditures (OPEX) such as rent, labor, and marketing and sales expenses. For instance, setting up a specialized outpatient clinic in a prime area of a first-tier city requires an investment of approximately RMB 8,000–10,000 per square meter, with 70% allocated to capital expenditures and 30% to operational expenditures. Compared to other industries, specialized healthcare chains are characterized by high asset intensity and significant operational demands at the initial investment stage.

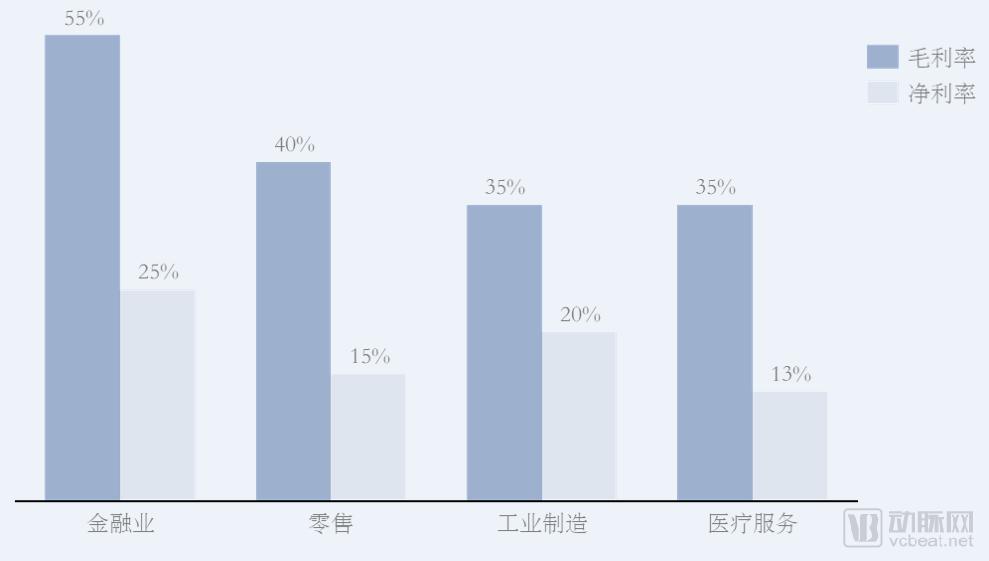

2. Slow onset of action:Specialized medical chains demand high operational capabilities and rely on professional medical staff to deliver services. Their operating costs are difficult to effectively reduce through economies of scale in later stages, resulting in lower gross and net profit margins compared to other industries. In the mature stage, their profit margins are roughly on par with those of the retail and food & beverage sectors.

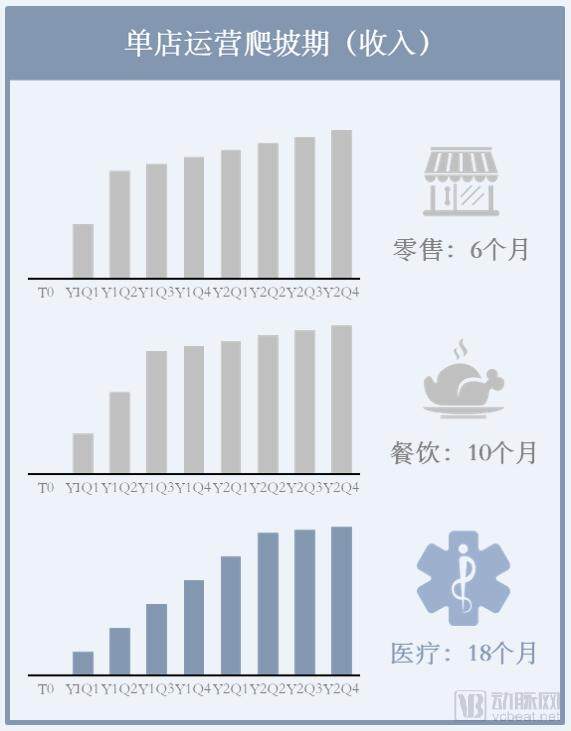

3. Long cycle:In terms of payback period, small and medium-sized medical outpatient clinics typically have a payback period of around three years, while large general hospitals generally require 6–8 years or even longer. These figures are significantly higher than those in the retail sector (6 months) and the food and beverage industry (10 months).

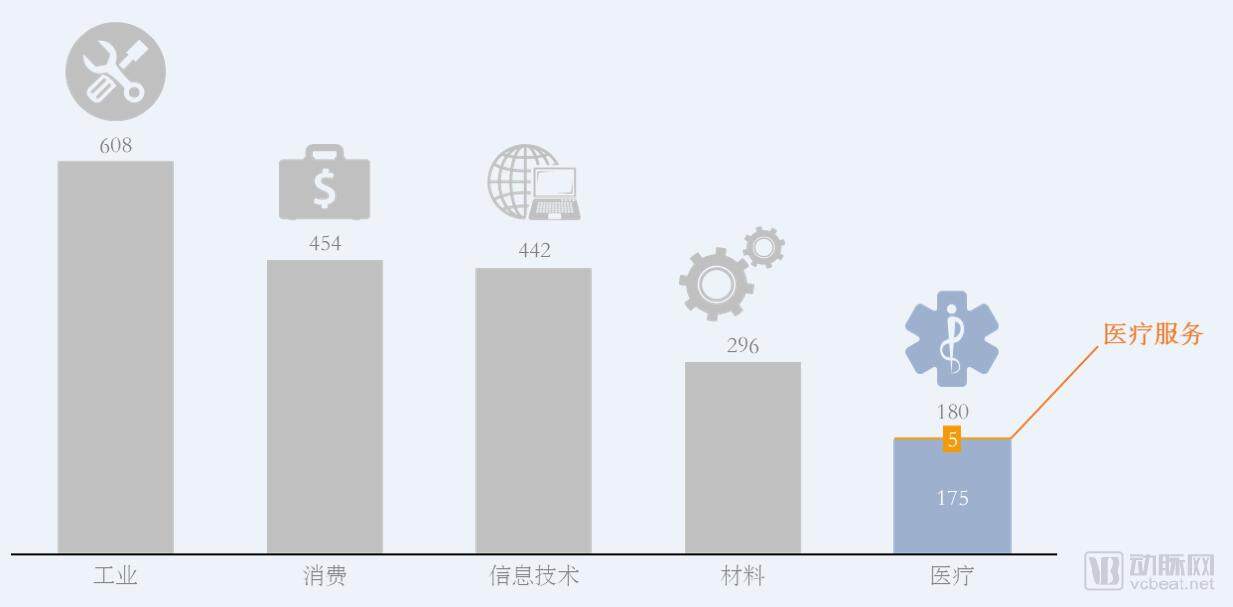

4. Difficult Exit: Over the past decade, a total of 2,097 companies have gone public through initial public offerings (IPOs) on China’s A-share market. Among them, only 180 were healthcare-related enterprises, accounting for 8.6%, and merely five were specialized chain providers of medical services. This indicates that regulatory review authorities have maintained a cautious stance toward specialized chain medical service providers, resulting in considerable uncertainty for capital exit. Consequently, in recent years, most chain medical service providers have chosen to list in Hong Kong as an exit strategy; however, secondary market trading in Hong Kong is relatively inactive, and valuations tend to be low.

In addition to the four major challenges mentioned above—namely, high capital investment, slow return on investment, long operational cycles, and difficult exit strategies—specialized chain medical service providers also face stringent regulatory and market access barriers. Furthermore, the economies of scale inherent in chain operations are often difficult to realize, leading to a common issue where groups are “connected but not integrated.”

How to Evaluate the Benefits of Specialized Medical Service Chains?

Economic Benefit Analysis of Specialty Chain Hospitals Through Economic Modeling

Given that specialized medical service chains are not as straightforward as commonly perceived, measuring their economic performance becomes critically important. Is there a universal quantitative model capable of guiding the analysis and assessment of the economics and benefits of specialized chains through multi-dimensional quantitative analysis?

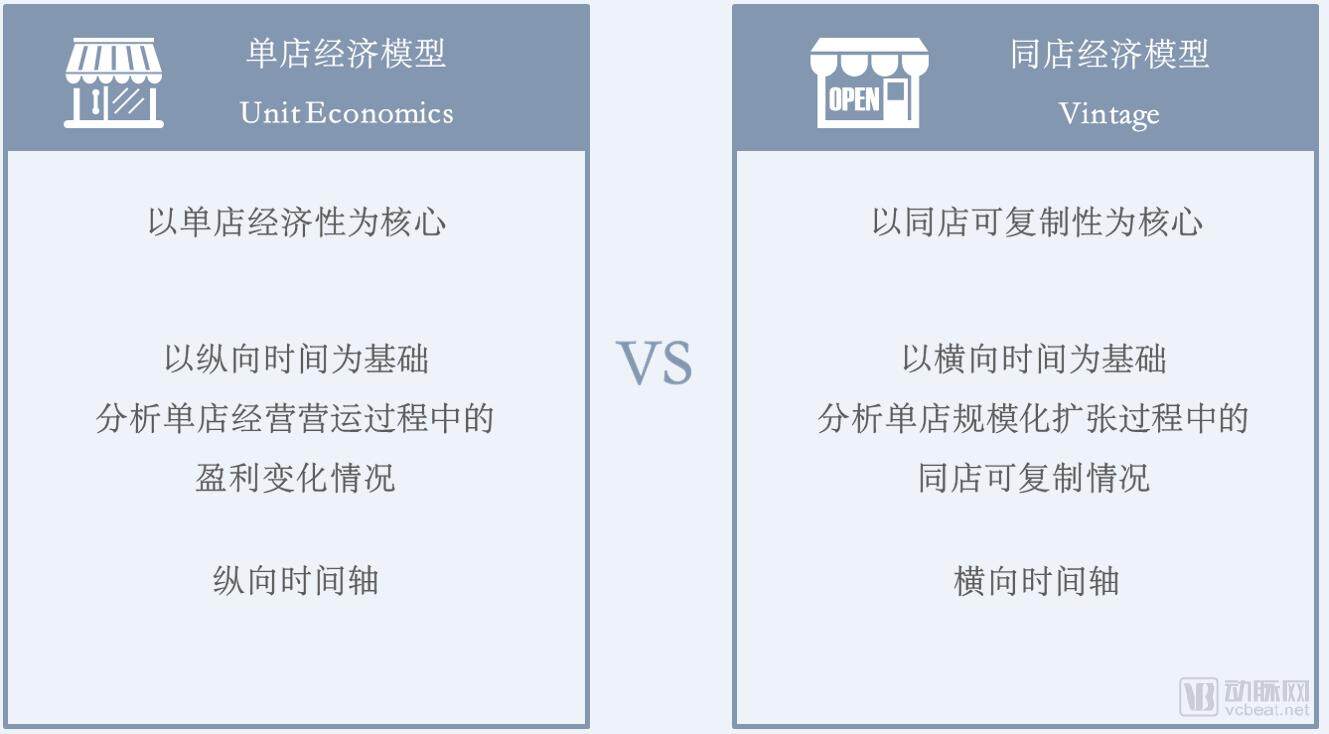

We have identified two commonly used models for evaluating the economic performance of specialized medical chain institutions:

(1)Unit Economics (UE) Model for a Single Store:The Single-Store Unit Economics (UE) Model is used to analyze which single-store format is the most cost-effective and efficient. For example, should a medical institution be built with an area of 300 or 3,000 square meters? Should it be equipped with 10 or 20 dental chairs? Would an investment of RMB 10 million or RMB 30 million yield the best returns? The UE model takes a single store as the unit and uses a longitudinal timeline as the coordinate system to analyze the benefit comparison between initial investment and final output, as well as to examine operational performance, financial profits and losses, and cash flow changes during the store’s operation.

(2)Vintage Same-Store Economic Model:Another core issue for specialized chain operations is how to verify replicability. The Vintage model, based on horizontal time analysis, examines the replicability of same-store performance during the scaled expansion of individual outlets. By analyzing and comparing data metrics, it assesses the performance of multiple stores along the same timeline, thereby verifying replicability.

1. Single-Store Economic Model: What Store Format Is the Most Cost-Effective?

A complete unit economics (UE) model for a single store comprises five components:

(1) Core Variables and Assumptions: Typical variables and assumptions generally include institution type, facility size, geographic location, and staffing configuration;

(2) Initial Investment Estimation: One-time Capital Expenditure and Recurring Operational Expenditure;

(3) Profit and Loss and Cash Flow: Revenue forecasts and the derivation of cash flow changes from revenue drivers;

(4) Return on Investment Metrics: such as Break-even Point, Payback Period, and Internal Rate of Return (IRR);

(5) Visual Representation: Display operational status, changes in financial profit and loss, and cash flow variations through visual means.

Example of a Typical Single-Store Unit Economics (UE) Model

In addition to evaluating the investment and return of individual stores, it is also necessary to analyze their operational performance during business operations, primarily covering:

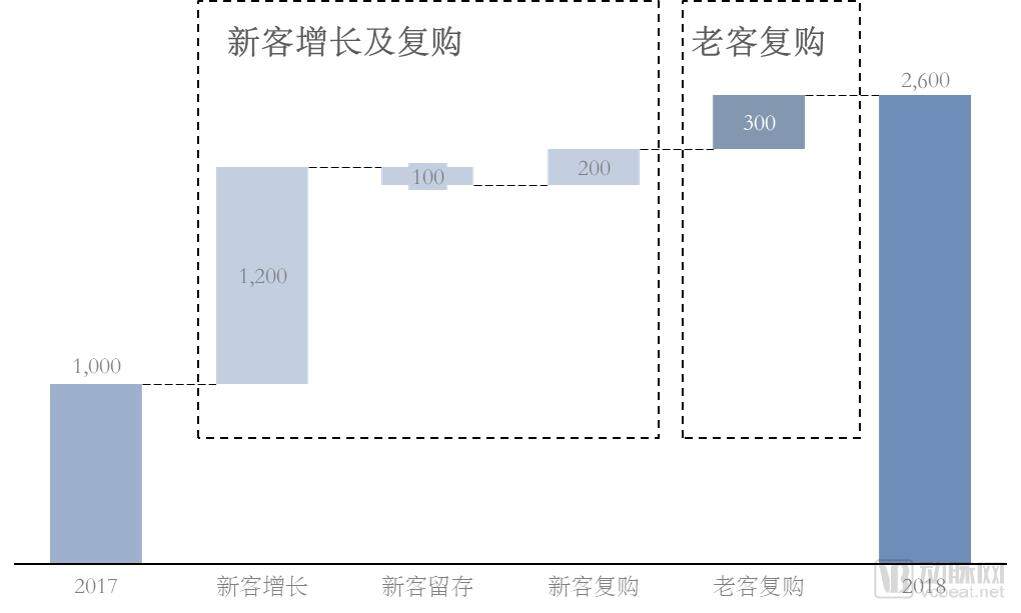

Analysis of Revenue Drivers

Single-Store Operational Efficiency Analysis

Revenue Driver Analysis

Revenue drivers primarily assess and analyze the core sources of revenue growth, such as whether increased revenue stems from an increase in new customers, repeat purchases by new customers, or repeat purchases by existing customers. Through the analysis of these drivers, one can identify areas in single-store operations that warrant attention and improvement. For instance, as shown in the chart above, revenue growth is mainly driven by an increase in new customers, which may largely be attributed to precise targeting and expansion efforts directed at new members.

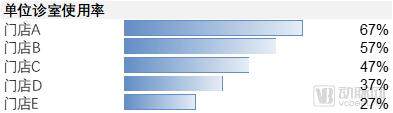

Analysis of Single-Store Operational Efficiency

Analysis of Single-Store Operational Efficiency Primarily Includes Analysis of Consultation Room Utilization Rates and Physician Efficiency:

Clinic efficiency is primarily analyzed by calculating the service duration of a clinic under full-load conditions and comparing it with the actual service duration, thereby assessing clinic utilization efficiency. This approach enables management to benchmark clinic performance and supports future improvements and growth.

Similarly, physician utilization efficiency is calculated by comparing the average scheduled consultation time with the actual consultation duration, thereby quantifying physicians’ consultation efficiency. This facilitates comparative assessments across different physicians and serves as an indirect indicator of their popularity.

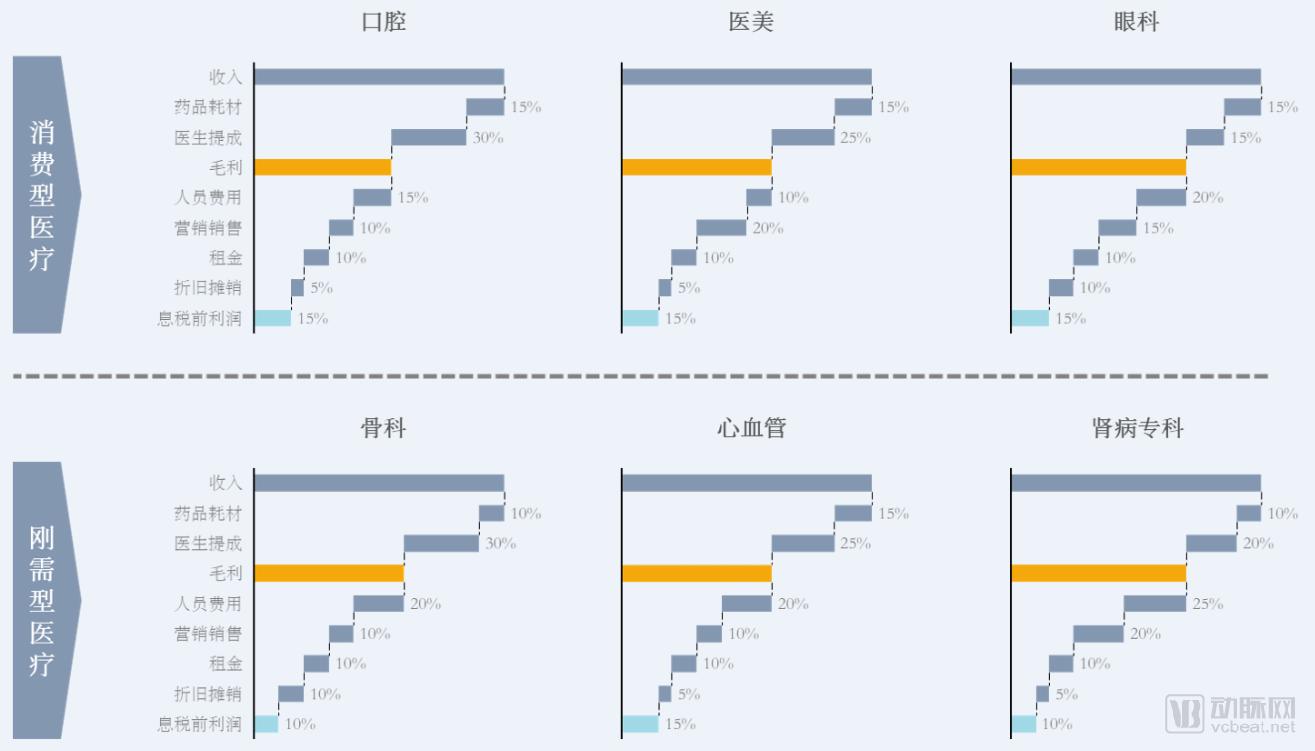

P&L of Mature Single Stores by Specialty

A key characteristic of specialized medical service chains is that each clinic requires a 2–3 year ramp-up period before reaching maturity, at which point different specialties exhibit distinct profit-and-loss models.

Specialty medical chains are broadly categorized into consumer-driven healthcare and essential healthcare. Consumer-driven healthcare refers to specialty services that individuals can choose at their discretion, with representative examples including dentistry, medical aesthetics, and ophthalmology. Essential healthcare denotes specialty medical services that meet consumers’ basic needs, such as orthopedics, cardiology, and nephrology. The three indicators most sensitive to the profit-and-loss performance of specialty medical chains are physician commissions, marketing expenses, and rental costs. Significant differences can be observed across specialty fields in terms of reliance on physicians, customer acquisition costs, and rental expenses. For instance, in the typical consumer-driven medical aesthetics sector, high customer acquisition costs result in a relatively high proportion of marketing expenses.

2. Vintage Same-Store Economic Model: How to Verify Replicability?

What Is a Vintage Model?

“Vintage” in English refers to the concept of age or year, originally applied in the wine-brewing industry. In winemaking, variations in weather, temperature, humidity, and other conditions each year differently affect wine quality. Therefore, people distinguish wine quality by the year the grapes were harvested, such as “Lafite 1982.” In 1982, the soil temperature and grape varieties in the Bordeaux region were optimal, resulting in the highest quality for Lafite from that year.

Later, this metric was applied to the assessment of bank credit quality. Banks made varying credit approval decisions across different periods based on considerations such as sales strategies and market conditions. By tracking assets from accounts opened in different periods and conducting synchronous comparisons and analyses of customer asset quality by age of account, banks found that account age is a core indicator reflecting credit quality.

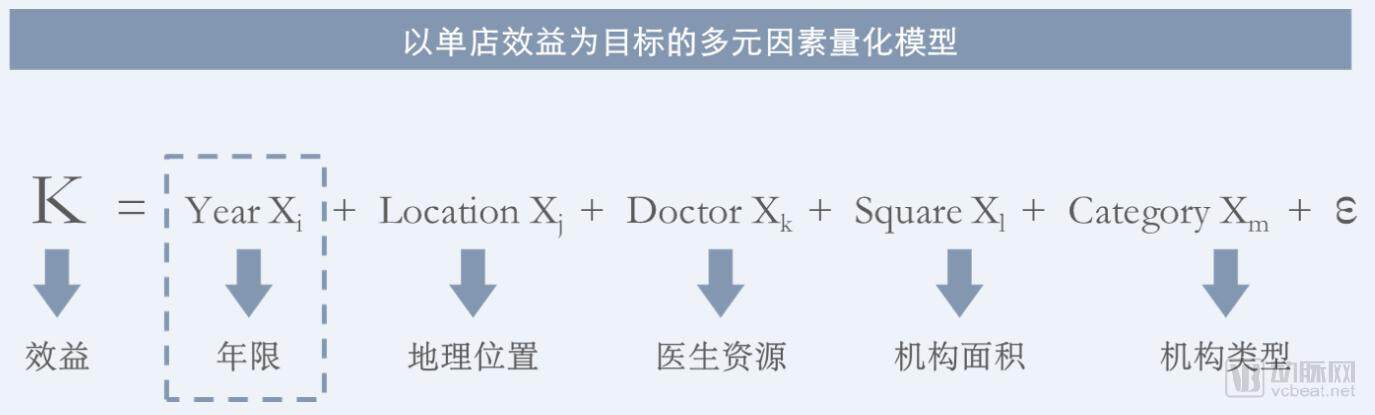

We attempted to apply this model to specialized medical service chains, as the operational efficiency of their outlets is influenced by numerous factors, including institution type, facility size, geographic location, and physician resources. However, similar to wine, the most significant factor affecting outlet performance is the number of years since opening.

Based on this conclusion, we designed a multi-factor quantitative model based on the efficiency of specialized chain medical institutions:

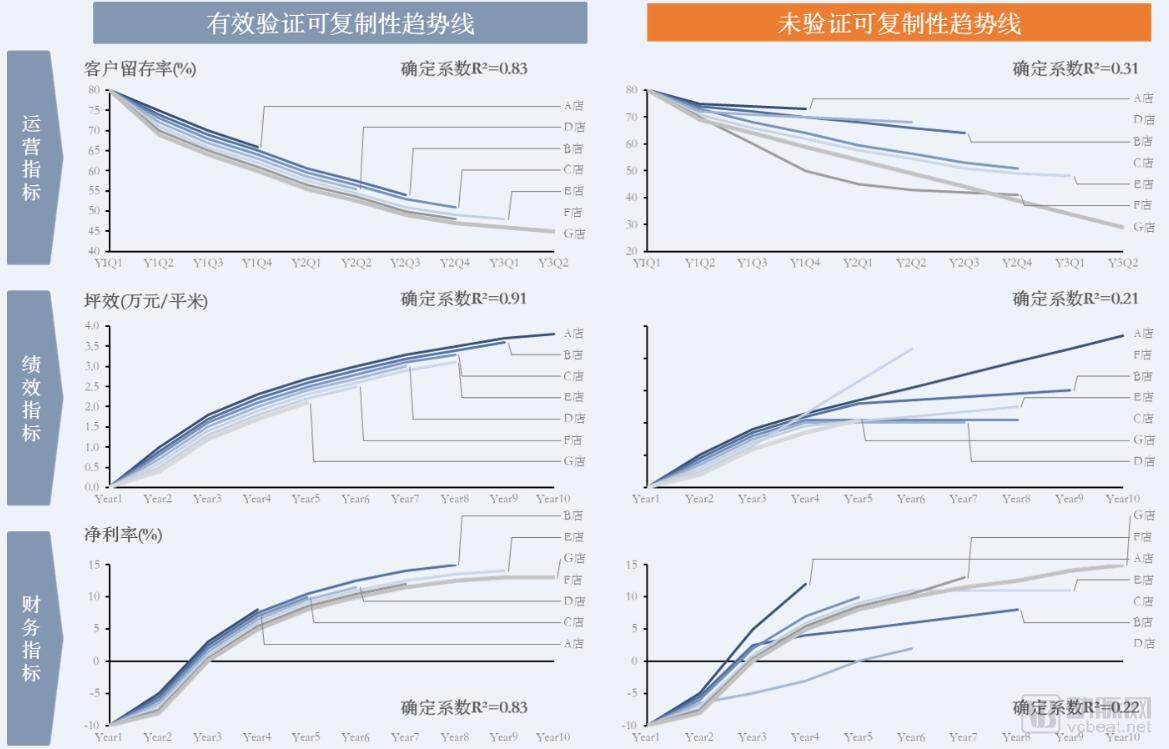

Meanwhile, we have established three core metrics to evaluate the performance of individual stores at the same point in time from operational, performance, and financial perspectives. The sub-metrics within each category are as follows:

Through these indicators, we can verify whether specialized medical chains are replicable:

In the chart above, each curve represents the performance of a single store under different metrics, while the length of the line indicates the duration since the store’s opening; the longer the curve, the longer the store has been in operation. By normalizing the performance curves of stores with varying operating durations to a common starting point, we can intuitively analyze their performance from the same baseline. As shown in the chart, the trend lines on the left side exhibit a high degree of fit (high overlap), effectively validating replicability. In contrast, the trend lines on the right side are relatively dispersed (low overlap), making it difficult to validate replicability. For a specialized healthcare chain, a higher degree of fit in its replicability trend lines indicates stronger replicability across its individual stores.

By examining various metrics, including gross profit margin, net profit margin, retention rate, and growth rate, it is possible to analyze whether the operational performance of individual stores validates their replicability. This model serves two purposes:

(1) To validate the replicability of the specialized chain business model in the capital market, specifically its degree of standardization and scalability. Higher replicability indicates a higher level of operational standardization at individual outlets, which facilitates the rapid expansion of the specialized chain.

(2) The operational performance of individual stores can assist operators in establishing key performance indicators (KPIs) to evaluate the efficiency and quality of single-store operations.

The optimal values derived from multi-store performance curve fitting can serve as effective benchmarks for chain operators to establish performance targets. For instance, if the fitted optimal value for sales per square meter in the third year of operation is RMB 33,000, this metric can be adopted as a key performance indicator (KPI) for individual stores. Through same-store comparisons, operators can identify performance gaps between high-performing and underperforming locations, analyze the underlying causes, and implement subsequent improvements.

In summary, although specialized medical service chains continue to attract strong interest from the capital market, their appeal is largely superficial. The business model of specialized chains requires sustained capital investment and refined, professional management, posing high demands on both operators and investors. Rapid expansion cannot be achieved simply through cash-burning marketing campaigns for customer acquisition or aggressive store rollout. As the market gradually returns to rationality, the true value of medical services will increasingly come to the fore.

Author Biography

Liu Zeyuan, Vice President of the Healthcare Group at CEC Capital, specializes in financing, investment, and mergers and acquisitions within the healthcare services sector. Liu He, Zhou Di, Gai Ruijie, Sun Qisong, and Jia Ruiyan all contributed to this article.

CEC Capital is a leading Chinese new-economy investment bank with nearly two decades of history, focusing on three key sectors globally: TMT, consumer, and healthcare. CEC Capital boasts the largest healthcare investment banking team in China and the most extensive track record of healthcare transactions. Its business scope covers four areas: pharmaceuticals and biotechnology, healthcare services, medical technology and devices, and digital health. The firm has served numerous industry-leading enterprises, including Penguin Doctor (Qi’e Xingren), Arrail Dental, United LiGe Medical Aesthetics, Aier Eye Hospital Group’s partner Ai’ge Ophthalmology, Xinkang Medical, Weirnuo Pediatrics, Qingmiao Children’s Dentistry, and Huahan Medical Aesthetics, accumulating rich project experience in specialized chain healthcare services.