Commercial Health Insurance in China: Navigating Product Iteration, Cost Control, and Service Excellence Amid Modest Market Scale

The health insurance market has witnessed rapid growth in annual new premium volume. In 2018, the original insurance premium income from health insurance business reached RMB 544.813 billion, representing a year-on-year increase of 24.12%. From 2013 to 2018, the compound annual growth rate (CAGR) of new health insurance premiums amounted to 35.95%. In January 2019, the original insurance premium income from health insurance business recorded the fastest growth, reaching RMB 79.8 billion, a year-on-year increase of 49.8%.

Behind the continuous expansion of the health insurance market lies the steady introduction of high-quality products that meet policyholders’ needs. Therefore, studying health insurance products is of significant importance: on one hand, it reveals shifts in insurers’ strategic priorities through product upgrades and iterations; on the other, it fosters a deeper understanding of the market.

This article begins with an analysis of insurance products, reviews the most popular health insurance offerings, and invites insurance product designers, insurance experts, and innovative service providers to provide multi-perspective insights into the evolving health insurance market.

The essence of insurance is risk transfer, whereby dispersed risks are transferred to an insurance company through insurance products and contracts, enabling the insured to receive compensation for losses in the event of a claim. When selecting insurance products, policyholders primarily focus on factors such as premiums, coverage scope, and sum insured.

Life insurance is increasingly becoming a standard component of personal financial planning, primarily for the following reasons: Medical expenses are rising steadily, placing growing financial pressure on individuals. In particular, as medical technology advances, cutting-edge treatment options often come with substantial costs, necessitating support from third-party payers. Meanwhile, rising income levels have made people more willing to increase their investment in health and medical care, seeking better protection and value-added services.

Middle- and high-income individuals constitute the primary target audience for health insurance. A survey conducted by EY among more than 2,000 individuals with annual incomes ranging from RMB 60,000 to RMB 300,000 has clearly delineated a precise profile of health insurance users. Their findings indicate that although public medical insurance covers a broad population, its scope of coverage is severely inadequate, failing to fully meet people’s healthcare protection needs. Customers lack confidence in managing substantial medical expenses and are particularly concerned about prescription drug coverage under health insurance plans, as well as issues related to seeking medical care across different regions. On the other hand, commercial health insurance policies are predominantly purchased through referrals from acquaintances, and consumers are generally high-income earners.

Specifically, China’s National Basic Medical Insurance scheme is designed to provide “basic coverage.” Although it covers more than 95% of the population, its scope of benefits is limited by a strictly defined drug formulary and reimbursement parameters, leaving cutting-edge therapies uncovered. Meanwhile, as the insurance fund is pooled at the regional level, cross-provincial settlement for medical services has not yet been fully integrated, creating additional barriers.

Regarding financial reserves for medical purposes, only 5% of high-income individuals have savings exceeding RMB 300,000; 22% have reserves between RMB 100,000 and RMB 300,000; 40% have no more than RMB 100,000 in savings; and approximately one-third have no dedicated savings for healthcare at all. In the face of rising disease incidence and treatment costs, such earmarked savings are woefully inadequate.

The survey also reveals that among respondents who purchased individual commercial health insurance, 61% were first-time buyers. Notably, the proportion of first-time buyers increases with rising personal income, indicating that high-income Chinese customers are more willing to try and accept individual commercial health insurance products, representing a potential incremental customer base for this sector.

Consumers often consider multiple factors, such as price and discounts, when selecting commercial health insurance products. Consequently, insurers typically adopt a strategy of initially capturing market share with low-priced offerings before gradually expanding their reach.

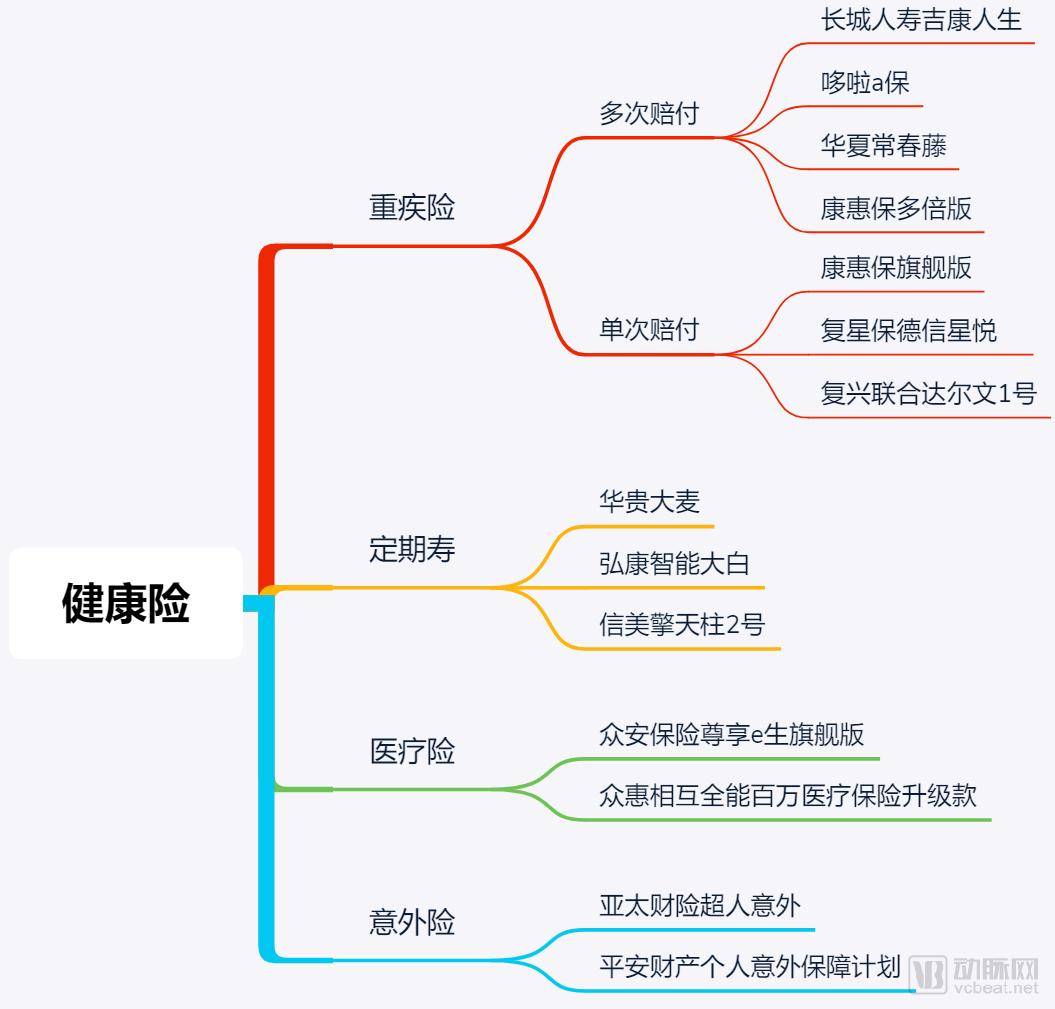

Cost-effective life insurance products are highly popular in the market. Ren Congcong, Manager of the Marketing Business Department at Beijing Financial Street Insurance Brokerage Co., Ltd., told VCBeat that when recommending products to clients and friends and family, she prioritizes cost-effectiveness above all else. According to her analysis, there are currently four major categories of widely accepted general health insurance products on the market: critical illness insurance, term life insurance, medical insurance, and accident insurance.

Critical illness insurance is further divided into two categories: multiple-payout and single-payout plans. Representative products in the former category include Hongkang Life’s “Dora A Bao,” Huaxia Life’s “Ivy,” and Bailing Life’s “Kanghuibao Multi-Pay Edition”; representative products in the latter category include Bailing Life’s “Kanghuibao” Flagship Edition and Fosun Pramerica’s “Xingyue Critical Illness Insurance.”

Representative products of term life insurance include Huagui Life’s “Damai Term Life Insurance” and Hongkang Life’s “Smart Dabai.”

The medical insurance products are ZhongAn Insurance’s “Zunxiang E-Sheng Flagship Edition” and Zhonghui Mutual’s “All-in-One Million Medical Insurance (Upgraded Version)”;

Accident insurance products include "Superman Accident" by Asia Pacific Property & Casualty Insurance and the "Personal Accident Protection Plan" by Ping An Property & Casualty Insurance. Many of these products are sold through online channels, offering high cost-effectiveness.

Figure: Overview of Popular Universal Health Insurance Products

Data Compilation: Ren Congcong

Ren Congcong told VCBeat that universal personal insurance follows certain basic “principles,” such as “protection first, investment second,” with the protective function of life insurance taking precedence; “adults before children,” since parents are their children’s greatest safeguard and should therefore be insured first; and finally, insurance coverage can be built up gradually, without the need to achieve comprehensive coverage in one step.

In terms of specific products, the coverage amount for term life insurance should be sufficient to cover the household’s total debts and extend until retirement age. Medical insurance and critical illness insurance form a “golden pair.” Medical insurance is a reimbursement-type policy that primarily covers medical expenses, while critical illness insurance provides financial support for the treatment of severe and costly diseases. The two complement each other in terms of coverage scope.

The demand for critical illness insurance remains strong, yet competition is fierce. After more than a decade of development and evolution, critical illness insurance has become the best-selling protection product. It is roughly estimated that there are no fewer than 1,000 types of critical illness insurance products currently available on the market. However, product homogenization is severe, and there is a trend toward disorderly competition.

Our research reveals that as public awareness of critical illnesses deepens and insurance consumption habits mature, traditional competitive factors such as price and the number of covered conditions no longer dictate purchasing decisions. Instead, consumers are increasingly prioritizing personal risk profiles, the alignment between coverage and individual needs, brand reputation, and user experience.

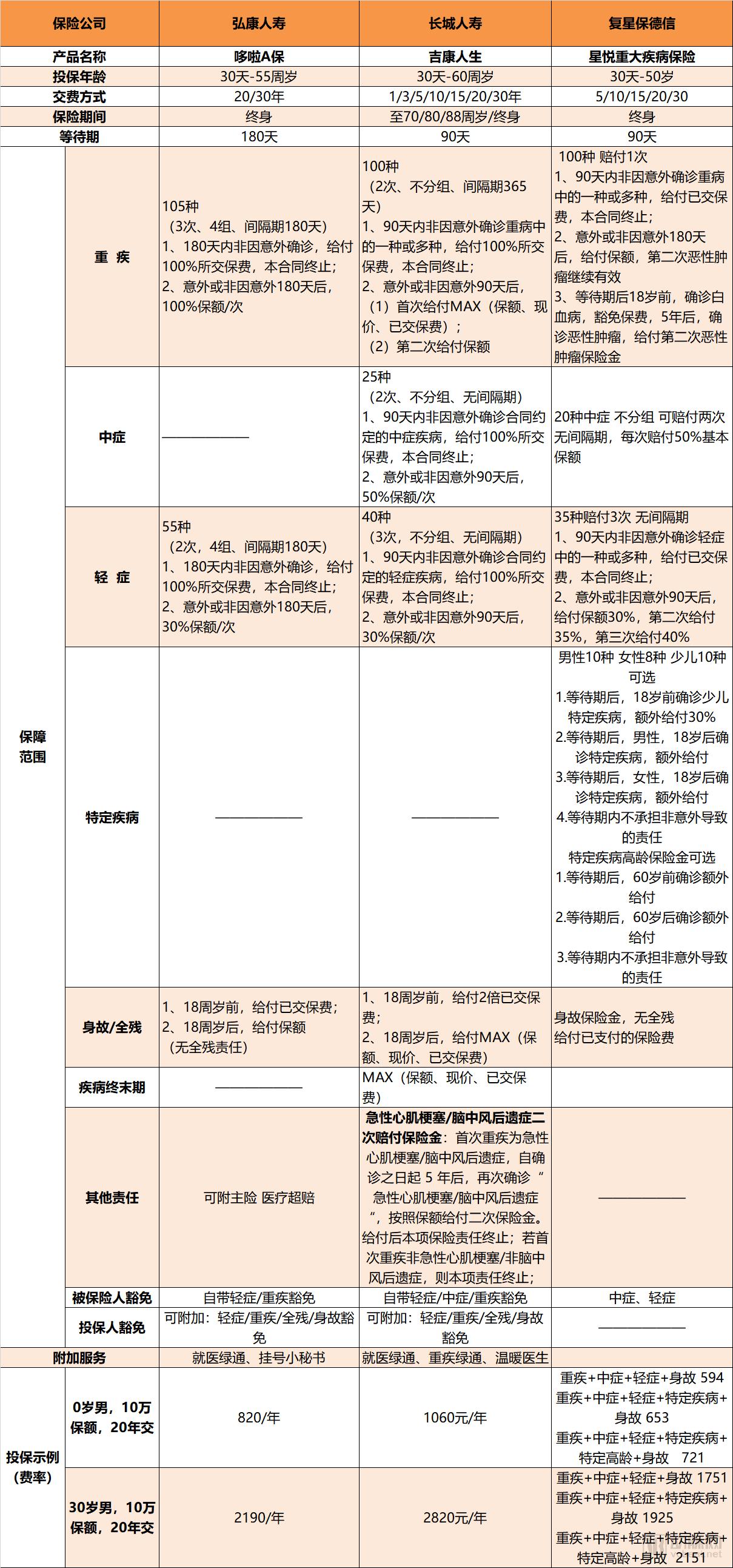

Overview of Selected Critical Illness Insurance Products

Data Compilation: Ren Congcong. Please refer to the product terms for specific details.

Great Wall Life’s “Ji Kang Ren Sheng” is one of the most popular critical illness insurance products in recent years, hailed by the industry as ushering critical illness insurance into the 5.0 era.

Qiu Hualong, General Manager of the Marketing Department at Great Wall Life Insurance, told VCBeat that critical illness insurance is a key product focus for the company. Great Wall Life has accumulated extensive experience in product development and marketing within this sector, and has established independent capabilities in disease progression modeling, insurable risk research, and product innovation. In response to intense market competition, the company places greater emphasis on standardized and professional principles in critical illness product development, striving to build a distinctive portfolio of critical illness products based on deep insights into customers’ genuine needs.

“Based on these market conditions, and combining our research on the development trends of critical illness insurance, disease-specific studies, product experience analysis, customer selection, and real needs assessment, we formulated the development direction and design philosophy for Great Wall Life’s critical illness health insurance products, and launched the ‘Jikang Rensheng’ critical illness product in July 2018,” said Qiu Hualong.

Specifically, Great Wall Jikang Rensheng is a critical illness protection plan that scientifically optimizes covered conditions, offering customers true ungrouped, multiple-payout coverage for mild, moderate, and severe illnesses, thereby pioneering the “Disease Protection System.”

Disease chains such as “Minor Stroke Sequelae – Moderate Stroke – Stroke Sequelae – Stroke Sequelae (Recurrence)” and “Atypical Myocardial Infarction – Moderate Acute Myocardial Infarction – Acute Myocardial Infarction – Acute Myocardial Infarction (Recurrence)” are market firsts.

Enable critical illness insurance products to offer a comprehensive ten-in-one coverage package, including protection for 40 common mild conditions, 25 moderate conditions, 100 critical illnesses, death/total permanent disability, secondary benefits for stroke sequelae, secondary benefits for acute myocardial infarction, terminal illness, and premium waivers for mild, moderate, and critical conditions.

Coverage for multiple secondary conditions alleviates customers’ concerns about being unable to secure further critical illness insurance after a diagnosis. Furthermore, the provision of second or multiple claims without disease grouping maximizes the scope of coverage and customer benefits. Policyholders can also choose to receive refunds of paid premiums at different ages, ensuring comprehensive, all-around protection. To enhance customer experience and added value, additional services are provided, including arranged medical consultations for critical illnesses and remote expert second opinions, according to specified standards.

In-depth channel cultivation has also been a key factor in Ji Kang Ren Sheng’s gradual market expansion. “Given that Ji Kang Ren Sheng offers relatively comprehensive and holistic coverage, with rich disease protection scenarios and additional benefits such as end-stage disease coverage, triple premium waivers, and death and total disability benefits, as well as an optional premium return feature, its promotion requires a certain level of explanatory and interpretive expertise. Therefore, this product is primarily marketed through professional brokerage and agency channels, while we are also exploring promotional strategies via specialized internet platforms to adapt to the new market landscape,” said Qiu Hualong.

Qiu Hualong stated that Jikang Rensheng’s products, officially launched in mid-2018 and on the market for less than a year, have been well received amid strong market demand and intense competition, remaining in the golden phase of their product life cycle.

In response to the industry trend of adjusting critical illness research, Great Wall Life Insurance has proactively conducted assessments and studies on critical illness risks and standardized disease definitions. Moving forward, the company will intensify efforts to upgrade and iterate critical illness insurance products for segmented customer groups, enhance the flexibility of flagship products such as “Jikang Rensheng,” and continue researching disease diagnosis, classification, correlations, and evolution. It will strategically launch new critical illness insurance products tailored to market conditions and demands at appropriate times.

Furthermore, in light of the entrenched issue of product imitation in the market, Great Wall Life Insurance is increasing the application of new technologies and health management services in its disease insurance products to enhance customer recognition and user experience, thereby building the brand and market influence of its critical illness insurance products.

Kong Qingkun, Product Director of the Health Insurance Division at ZhongAn Insurance, told VCBeat that when configuring health insurance coverage, individuals can follow the principle of prioritizing accident insurance, medical insurance, short-term critical illness insurance, long-term critical illness insurance, and term life insurance.

However, at present, many first-time policyholders also choose to purchase “Million Medical Insurance” through online channels. In particular, individuals born in the 1980s and 1990s, as digital natives, exhibit a high level of acceptance toward online platforms and often subsequently help their parents and family members secure such insurance coverage.

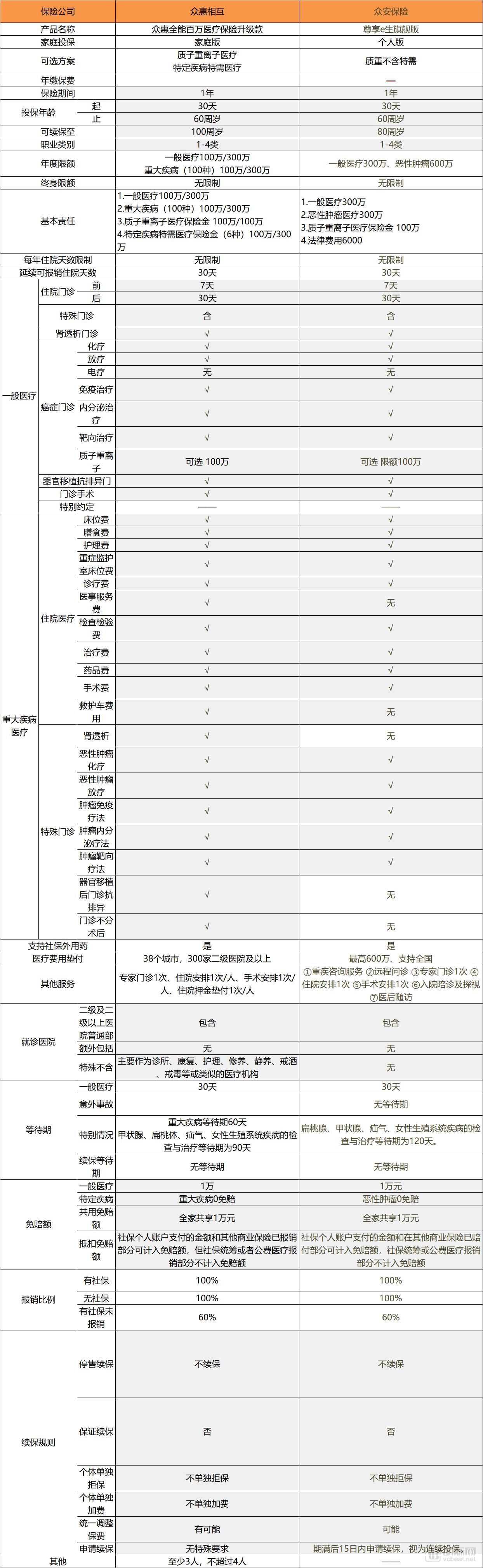

Comparison of Two Medical Insurance Product Information

Information compiled by Ren Congcong; please refer to the product terms and conditions for specific details.

ZhongAn’s “Zunxiang E-Sheng” product series has become virtually synonymous with “million-yuan medical insurance,” setting the benchmark for this category through its underwriting rules, coverage scope, and value-added services. The predecessor of Zunxiang E-Sheng was “Zunxiang Wuyou,” launched in 2015; it was renamed in 2016 and had undergone 13 iterations by March 2019.

Kong Qingkun told VCBeat that the iterative updates of "Zunxiang Yisheng" have primarily focused on three areas: coverage details, value-added services, and personalization. In terms of coverage, in February 2017, Zunxiang Yisheng raised the sum insured to RMB 3 million, with a maximum of RMB 6 million for malignant cancer cases. It pioneered zero deductible for malignant cancers and extended coverage to include outpatient and emergency visits before and after hospitalization, as well as outpatient surgeries. Later, it became the first in the industry to include rehabilitation services within the scope of mid-end medical insurance coverage.

In terms of value-added services, Zunxiang e-Sheng expanded to cover proton and heavy ion therapy in 2018, offering exclusive 100% reimbursement. It subsequently extended coverage to cancer treatment in Japan, pioneering overseas medical access channels that enable insured individuals to benefit from the world’s most advanced cancer treatments. Additional services include oncology pharmaceutical care, postoperative home nursing, green-channel access for malignant tumor treatment, and medical expense advances.

In terms of personalization, the "Zunxiang Yisheng Sports Edition," launched in July 2017, serves as a typical example. It integrates with wearable devices to provide “customized” mid-end medical insurance for fitness enthusiasts. Subsequently introduced versions, such as the "Zunxiang Yisheng Chronic Disease Edition" and the "Zunxiang Yisheng Parents Edition," have offered personalized options to a broader population.

Through rigorous product design and multiple iterations, ZhongAn’s “Zunxiang E-Sheng” series has gained widespread popularity and is affectionately known as the “National Health Insurance.” Currently, ZhongAn is also working to build a comprehensive health insurance ecosystem. By leveraging synergies among ZhongAn Life, ZhongAn Technology, and ZhongAn Insurance, as well as collaborating with external partners, the company aims to further enhance the insurance experience and coverage capabilities.

For instance, ZhongAn Life offers genetic testing services for pre-underwriting risk assessment and for determining the suitability of targeted therapies during treatment; meanwhile, ZhongAn Technology provides solutions in insurance marketing, financial credit, and healthcare, empowering the insurance industry through technology.

Health insurance is closely linked to individuals’ health status; factors such as disease incidence and treatment pathway selection can affect claim payout levels. Both mature markets in Europe and the United States and emerging markets in China are exploring managed care models or “insurance + healthcare” collaborative approaches to enhance customer experience and effectively control medical costs.

For instance, UnitedHealth in the United States offers PBM (pharmacy benefit management), medical informatization, and population health management services through its subsidiary Optum, providing insurance customers with more diversified services. Recently, U.S. pharmaceutical retail giant CVS Health announced the completion of its acquisition of Aetna, while Cigna acquired Express Scripts, the largest independent PBM and pharmaceutical retail company in the United States. These moves reflect an important trend toward synergy between insurance and healthcare services.

In China, there are also positive examples such as China Life Insurance engaging in investments in the big health sector, Taikang entering the hospital industry, and Ping An incubating Ping An Good Doctor.

Liu Lu from Zefang Consulting stated that in discussions with heads of health insurance companies, it was learned that they are either integrating with medical services or collaborating with companies specializing in health management and disease prediction. These insurers are actively exploring a synergistic “insurance + healthcare” model, aiming to effectively control costs and enhance customer experience. However, the process is complex, and there is currently no robust practical experience to draw upon.

Regarding the challenges of exploring the synergy between “insurance + healthcare” services in China, Kong Qingkun, Product Director of the Health Insurance Division at ZhongAn Insurance, stated that the main issue lies in the fact that China stillDominance of the Public Healthcare System, Limited Scale of Commercial Health Insurance, and Lack of Bargaining Power over Healthcare Institutions。

Users also tend to prefer public hospitals for medical care, opting for private hospitals only for minor ailments or premium medical services, while still choosing public hospitals for serious conditions or hospitalization. However, with the future development of private healthcare and the liberalization of multi-site physician practice, the synergistic “insurance + healthcare” model will become a significant trend.

Regarding the specific implementation pathway, Tang Shaoming, a consultant at Mercer, stated that international practices could serve as a reference for the “Insurance + Healthcare” model: first, utilizing health big data during underwriting to identify high-risk populations or design insurance products for specific diseases; second, controlling or reducing claims through preventive medicine, chronic disease management, and second medical opinions; and third, managing consultation costs by designating specific hospitals and physicians.

He also pointed out that there are still no particularly mature implementation cases in China, and both insurance companies and healthcare service providers are hoping to achieve breakthroughs.

Whether through technology empowerment or the synergy of “insurance + healthcare,” the ultimate deliverable to users will take the form of health insurance products or services. Users primarily purchase health insurance for protection purposes, with experience optimization and value-added services serving as complementary enhancements. Multi-party innovation is essential to foster greater user acceptance of health insurance and to share in the industry’s upward growth momentum.