AccessOne Files for IPO: The U.S. 'Huabei' for Healthcare Offering 12-Month Interest-Free Plans to Over 400,000 Patients with $270 Million in Loans

AccessOne

A financial engagement platform that helps patients manage out-of-pocket medical expenses.

With the introduction of high-deductible health plans in the United States and the rise in other out-of-pocket expenses, patients have become the third-largest payer group in the U.S. healthcare industry, after Medicare and Medicaid, with a growing number of individuals bearing increasing financial burdens.

According to a report released by the U.S. consumer credit reporting agency TransUnion in June 2017, 68% of American adults with medical bills of no more than $500 failed to pay off their debts in full in 2016, up from 49% in 2014. TransUnion predicts that this proportion will rise to 95% by 2020.

When patients delay or forgo medical care due to unaffordable costs, it not only exacerbates the severity of their conditions but also increases the cost of treating these conditions when they eventually seek care. As a result, patients face greater financial strain, and the overall costs to the healthcare system rise as well.

To alleviate patients’ short-term financial burdens, specialized medical lending companies have emerged in the United States, such as CareCredit, AccessOne, and Wells Fargo Health Advantage. This article focuses on AccessOne, headquartered in Charlotte, North Carolina.

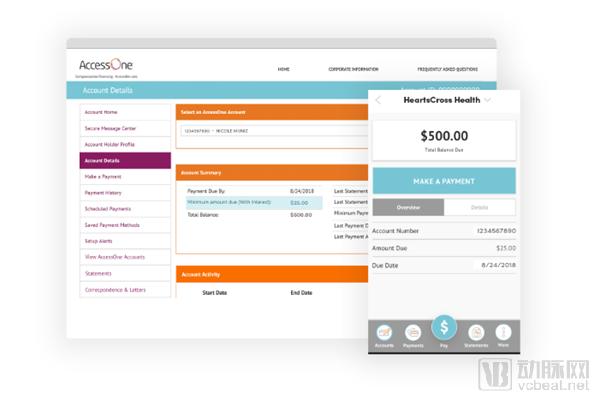

Image fromAccessOneOfficial Website

AccessOne was founded in 2002 by Russell A. Salton and Steve Bernard. Russell A. Salton serves as the company’s Chairman, President, and Chief Executive Officer. A third-generation physician in his family, he co-founded Metrolina Family Physicians, the largest independent family practice group in the southeastern United States. Subsequently, Mr. Salton co-founded Primary PhysicianCare, a managed care company, and served as Medical Director for Aetna US Healthcare in the Carolinas.

Since Mark Spinner joined AccessOne in March 2016 and assumed the roles of President and Chief Executive Officer, Russell A. Salton has stepped back from day-to-day operations to serve as Chairman of the Board.

Prior to joining AccessOne, Mark Spinner founded financial firms such as TopSpin Growth Capital Partners and ProviderWeb Capital. He also spent 15 years working in the private equity, corporate finance, and mergers and acquisitions (M&A) advisory divisions of major financial institutions, including Stephens, Deutsche Bank Alex Brown, and RBC Capital Markets. Mark Spinner possesses unique corporate management experience in both private and public capital markets, along with specialized financial expertise in credit and M&A.

AccessOne President and CEO Mark Spinner (Image from the company’s official website)

Co-founder Steve Bernard serves as the Chief Information Officer of AccessOne, overseeing the design, development, and evolution of the company’s software systems. Prior to co-founding AccessOne, Mr. Bernard was responsible for building financial systems at companies including Aetna, State Street, Fleet, Wachovia, Fidelity Investments, and United Guarantee.

Tammy Geis, Chief Operating Officer of AccessOne, joined the company in its second year and is considered a veteran at AccessOne. She previously served as Chief Financial Officer until 2018, when she assumed the role of Chief Operating Officer, overseeing call center operations, customer engagement, data management, and quality assurance.

In addition, Chief Technology Officer Connor Gray and Chief Marketing Officer Robert Meyer joined AccessOne only within the past two years, while Joe Hall, Senior Vice President of Business Development, did not join the company until last month (March 2019). It is evident that, apart from the two co-founders and the Chief Operating Officer who have longer tenures, AccessOne’s leadership team has seen a significant influx of new talent in recent years.

Nevertheless, an examination of the leadership team’s professional backgrounds reveals extensive experience in their respective fields. Furthermore, judging from AccessOne’s fundraising capabilities and market development in recent years, the new management team has injected fresh hope into the company’s growth (to be detailed later).

AccessOne is a medical credit card company that partners with healthcare institutions to provide loan programs for patients facing financial strain due to high out-of-pocket costs and high deductibles. AccessOne does not reject any patient loan applications and does not employ a credit scoring system; even applicants with poor credit histories can secure financing support from AccessOne.

When patients apply for a loan, AccessOne evaluates their credit history and formulates an appropriate repayment plan based on their individual circumstances. After registering for an AccessOne account at the doctor’s office, patients receive an AccessOne medical credit card, known as the AccessOne MedCard. With this card, patients have two borrowing options: interest-free loans and low-interest loans.

For example, for a $1,200 medical bill, patients can choose to repay in 12 interest-free monthly installments of $100 each, or opt for monthly payments of $39, including interest, until the balance is fully paid off.

This means that patients with interest-free loans have a 12-month interest-free repayment period, and their monthly repayment amount is slightly higher than that of low-interest loans. Patients with low-interest loans have relatively lower monthly repayments, and the interest rate is lower than the industry average of 11.25%. For loan amounts within $10,000, the interest rate is 9.25%; for loan amounts exceeding $10,000, the interest rate is 5%. If patients have new medical loan plans, AccessOne will adjust their minimum monthly repayment amount in a timely manner based on their repayment capacity.

When a patient is about to become delinquent, they will receive a payment reminder from AccessOne. For patients with interest-free loans, if they fail to repay on time, their accounts will be converted to interest-bearing accounts until the outstanding balance and accrued interest are fully paid off. For patients with low-interest loans, if they fail to repay on time, the interest rate will be increased to 18%. If a patient stops or refuses to make payments, AccessOne will not report the delinquency to credit bureaus, unlike other medical credit card companies; instead, it will return the patient’s account to the healthcare provider where the services were rendered.

Therefore, to ensure repayment rates, AccessOne leverages its platform’s predictive analytics tools to assess patients’ payment propensity in advance and adjust repayment amounts, keeping them within the range that patients can afford on a monthly basis. Meanwhile, to facilitate repayments, AccessOne offers three payment options: patients can make online payments through the AccessOne official website, or repay via customer service hotline or email.

Repayment Operation Page (Screenshot from the Official Website)

For patients and healthcare institutions, the loan services provided by AccessOne are a win-win choice.

From the patient perspective, AccessOne’s 24/7 Interactive Voice Response (IVR) system provides round-the-clock loan services, with its call center featuring over 210 voice systems to facilitate loan applications for patients speaking various languages. Meanwhile, AccessOne’s real-time integration capability consolidates bills from disparate healthcare information systems into a single integrated monthly statement, enabling patients to make timely repayments with ease.

Furthermore, patients applying for AccessOne loans are not subject to credit checks and benefit from a 12-month interest-free period, affordable minimum payments, and flexible payment terms that can be deferred. These services not only alleviate the financial burden of medical care but also encourage timely treatment and better health management.

Turning to healthcare institutions, AccessOne’s simplified patient financial engagement model is designed to fit into the revenue cycle workflows of healthcare providers. By integrating billing, mobile applications, email reminders, and paperless statements, AccessOne alleviates the burden on healthcare institution staff in managing medical bills.

More importantly, with loan options available, hospitals can receive medical fees from self-pay patients in advance, thereby reducing the incidence of bad debts. Meanwhile, the tendency of patients to delay or forgo care has improved, which not only helps healthcare institutions increase revenue but also contributes to lowering overall healthcare expenditures in the United States.

According to survey data from the U.S. market research firm ORC International, healthcare providers would gain a significant competitive advantage by offering interest-free or low-interest loan programs; 46% of Millennials, 36% of Generation X, and 28% of Baby Boomers indicated they would switch healthcare providers for better financing options.

AccessOne also stated that, in order to remain competitive, the number of hospitals offering medical credit cards has grown by approximately 25% annually in recent years.

Since its establishment in 2002, AccessOne has secured funding from major financial institutions such as GE Capital, Frontier Capital, and Capital One Bank, in addition to charging management fees to healthcare institutions.

According to incomplete statistics from VCBeat, in July 2009, AccessOne MedCard secured a $25 million revolving credit facility, with GE Capital, a medical financial services company, serving as the administrative agent, lead arranger, and bookrunner for the transaction.

Russell Salton, then CEO of AccessOne, stated, “GE Capital has been financing our products since 2004. In particular, continued access to funding will help us achieve our development and growth objectives amid the current challenging credit environment.”

Capital infusion has provided AccessOne with strong momentum for market expansion. Russell Salton once told the media that during its first decade of operations, AccessOne partnered with more than 50 hospitals and facilitated $270 million in medical loans for 400,000 patients.

Although there is no precise data to substantiate AccessOne’s market performance in recent years, its financing activities and client relationship development during this period indicate that between 2017 and 2018, the company secured over USD 100 million in funding and established stable partnerships with numerous major clients.

In January 2017, growth equity firm Frontier Capital made an equity investment in AccessOne, marking its third investment in the company.

One month later, Capital One Bank led a syndicate including Huntington Bank, Capital Bank, and Frontier Capital to provide AccessOne with approximately $70 million in senior credit facilities. This funding has significantly accelerated AccessOne’s market expansion and enabled continued investment in its technology platform to better serve healthcare institutions and patients.

“The completion of this financing represents a significant step forward for our company, as well as for the healthcare institutions and patients we serve,” said Mark Spinner, CEO of AccessOne. “Our partnership with the banking consortium will help us continue to provide lending programs to healthcare institutions and their patients.”

In January 2018, AccessOne acquired HealthFirst Financial, a healthcare services company that provides customized financial solutions to medical institutions. HealthFirst Financial offers a mobile application that allows users to view and edit account information, make payments, and review payment records. Since its establishment in 2001, HealthFirst Financial has partnered with 77,000 households and 220 medical institutions. Following the acquisition, the HealthFirst Financial mobile application became the property of AccessOne.

Since its inception, AccessOne’s market has gradually expanded from the southern United States to a national scale. Healthcare institutions such as Hampton Regional Medical Center, St. Luke’s Hospital, the hospital chain Carolinas HealthCare System, and the health information technology company Acryness, along with third-party medical service providers, have successively become stable clients of AccessOne. Among them, the Charlotte-headquartered hospital chain Carolinas HealthCare System, which owns the CMC (Clinical Medicine Cloud) smart healthcare platform, is AccessOne’s largest client.

These achievements may be attributed to the significant overhaul of AccessOne’s leadership. The new management team has introduced fresh development strategies, which have yielded notably positive results. In particular, Mark Spinner, who brings extensive experience in capital operations and financial credit, has repeatedly stated since assuming the role of CEO that he intends to transform AccessOne into a nationwide healthcare IT company. This indicates that AccessOne is not content with remaining merely a medical credit card company offering healthcare loan services.

Due to the high level of out-of-pocket medical expenses, patients in China also face significant financial pressure. In response, the Chinese government has repeatedly introduced policies to encourage the development of supplementary medical payment mechanisms. The Outline of the “Healthy China 2030” Plan proposes: fully mobilizing the enthusiasm of social organizations and enterprises to form a diversified funding structure; encouraging financial institutions and others to innovate products and services, and improving supportive measures. The 13th Five-Year Plan for Deepening the Reform of the Medical and Health Care System also mentions: exploring intangible asset pledge loan businesses and encouraging the development of health-related consumer credit.

In the corporate sector, to alleviate the short-term payment burden for domestic patients, some companies in China have turned their attention to installment payment solutions. In January 2018, Zhongnuo Puhui leveraged inclusive finance as a tool to launch a variety of medical finance and insurance products, enabling more patients to afford and receive quality medical care.

Zhongnuo Puhui offers six service offerings, including: a phased surgical payment solution—Zhongnuo Wuyou; a financial solution for self-pay high-cost medications—Zhongnuo Kangjian; a comprehensive hospital payment solution—Zhongnuo Smart Hospital; an advanced payment solution for medical insurance reimbursements—Zhongnuo Anfu; customized insurance solutions—Zhongnuo Jianbao; and a payment solution for medical retail chains—Zhongnuo Smart Medical Retail.

Zhongnuo Puhui positions itself as a medical technology finance company, aiming to build a medical installment payment platform that establishes robust trust with patients in China’s market, where doctor-patient tensions are acute, thereby becoming a platform truly relied upon by patients.

In terms of user verification, Zhongnuo Puhui has established a financial risk control department to assess the creditworthiness and repayment capacity of every patient applying for installment payments. The review process encompasses both medical risk control and financial risk control. This technology-driven risk management framework accelerates the verification process, enabling applicants to receive a response within 24 hours and disbursement within 48 hours upon submission of complete documentation. The overall application procedure is streamlined and efficient, thereby removing initial barriers for patients.

In its go-to-market strategy, Zhongnuo Puhui has adopted a dual-pronged approach targeting both business-to-business (B2B) and consumer-to-consumer (C2C) segments. On the B2B front, Zhongnuo collaborates with pharmaceutical companies and medical device manufacturers; once a specific drug is linked to its corporate platform, patients purchasing that medication become eligible to apply for charitable assistance programs. On the C2C side, Zhongnuo employs an integrated online-and-offline promotional strategy, enabling patients to submit applications when needed, thereby alleviating their financial burden. Furthermore, Zhongnuo Puhui is partnering with hospitals and physicians to jointly promote these initiatives.

As of August 2018, Zhongnuo Puhui’s services covered more than ten disease categories, serving over one thousand patients and earning widespread acclaim from patients.

In fact, beyond Zhongnuo Puhui, installment payment platforms catering to various sectors have been gradually emerging in China. The medical aesthetics industry, characterized by its strong liquidity, appears particularly enthusiastic about adopting installment payment options. To boost customer acquisition rates, medical aesthetics companies such as New Oxygen, Gengmei, Yuemei, and Meili Shenqi have either built their own online installment platforms or partnered with third-party financial institutions, rolling out installment payment services over the past two years.

In addition, some companies have entered the market by focusing on niche segments and offering installment payment services. For example, Kuai Kangda has launched a medical installment financing platform with zero down payment and zero interest, using insulin pumps as its entry point. Even Ant Credit Pay (Huabei) entered the healthcare sector in 2016, providing financial services to patients through partnerships with hospitals. In the future, installment payment platforms may become another major growth opportunity in the healthcare industry.