Rock Health Q1 2019 Digital Health Funding Report: $986M Raised as Top Unicorns See Valuations Surge

In 2018, funding in the digital health sector reached a record high, but the investment momentum slowed in the first quarter of 2019. Meanwhile, after a two-and-a-half-year “drought,” the IPO market for digital health companies saw a turning point. Rock Health recently released its Q1 2019 Digital Health Funding Report, which was compiled and summarized by VCBeat (WeChat ID: vcbeat), with key highlights focusing on the following aspects:

I. Slowdown in Financing for Digital Health Companies in Q1 2019

II. Companies Are Eager to Invest in the Digital Health Sector

III. The “Drought” Period for Digital Health IPOs Is Coming to an End

IV. Call for Digital Health Companies to Adopt Outcome-Based Business Models

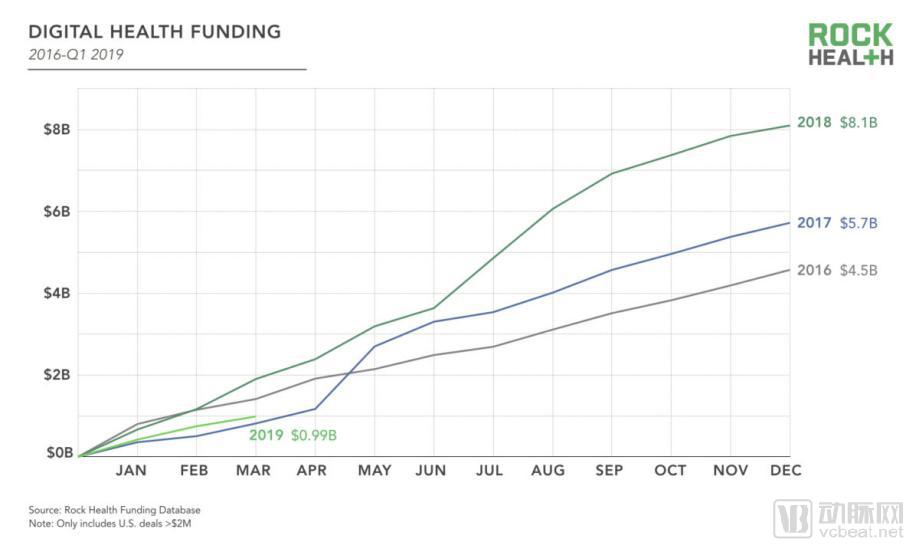

In the record-breaking year of 2018, U.S. digital health companies raised a total of $8.1 billion. In the first quarter of 2019, U.S. digital health companies raised $986 million across 61 deals. This amount was approximately half of the funding raised in the first quarter of 2018, but roughly on par with the same period in 2017, and 31% lower than the same period in 2016.

Comparison of U.S. Digital Health Financing, 2016–2018 (Screenshot from the Original Report)

Comparison of U.S. Digital Health Financing, 2016–2018 (Screenshot from the Original Report)

Over the past six months, fundraising for U.S. digital health companies has remained stable, although the period around mid-2018 was somewhat exceptional. In the third quarter of 2018 alone, investors injected $3.3 billion into the sector at a remarkable pace, followed by $1.2 billion in the fourth quarter of 2018. Excluding the surge in capital during the peak popularity of digital health in mid-2018, the average quarterly investment over the two-year period from Q1 2017 to Q1 2019 stood at $1.4 billion. This also implies that the $986 million invested in Q1 2019 was slightly below the recent trend.

Two new digital health unicorns showed strong growth in the first quarter of 2019, indicating a continued rise in their valuations.

Among them, Calm, a meditation app developer, reached a valuation of $1 billion after raising $88 million in its Series B funding round. Calm plans to use the proceeds from this round to develop new products and expand into international markets.

Health Analytics platform provider Health Catalyst raised $100 million in its Series F funding round, reaching a valuation of $1 billion. The company plans to continue building its platform to help hospitals link and analyze siloed databases. It is reported that Health Catalyst is planning an initial public offering (IPO).

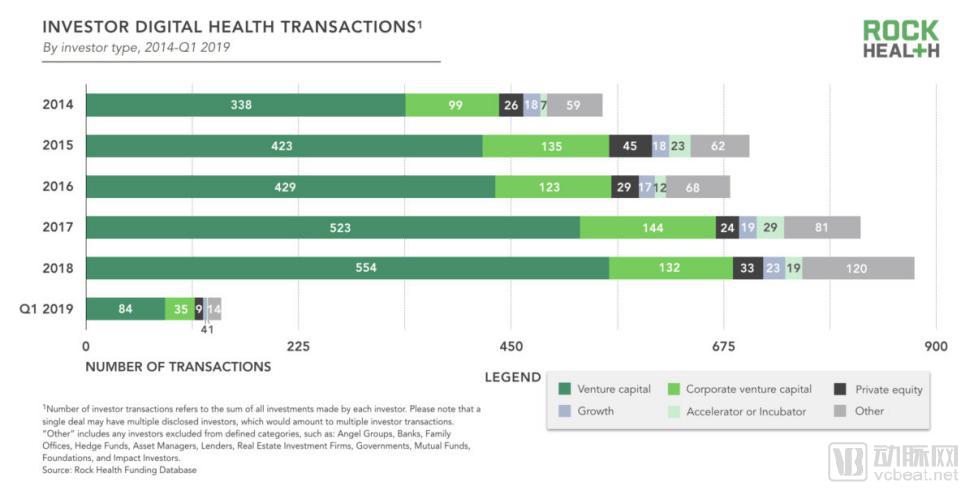

Investors in the digital health sector primarily include prominent venture capital firms, technology companies, and healthcare enterprises. Andreessen Horowitz, Khosla Ventures, New Enterprise Associates, Y Combinator, Novartis, Merck, and GV, among others, all made digital health investments in the first quarter of 2019, having maintained continuous investment in this field over the past several years.

Digital Healthcare Investment Transaction Analysis (Screenshot from the Original Report)

Digital Healthcare Investment Transaction Analysis (Screenshot from the Original Report)

Over the past five years, corporate venture capital (CVC) firms have participated in approximately one-third of all digital health transactions. This stands in stark contrast to overall CVC activity by U.S. corporations in non-healthcare sectors. Between 2014 and 2018, corporates accounted for only 13%–16% of venture capital investments in non-healthcare industries—merely half the volume seen in digital health. Given that roughly 85% of digital health companies tend to be acquired by corporate entities, it is hardly surprising that corporations are keen on investing in digital health, as this serves as an effective strategy to leverage external innovation for driving corporate growth and profitability.

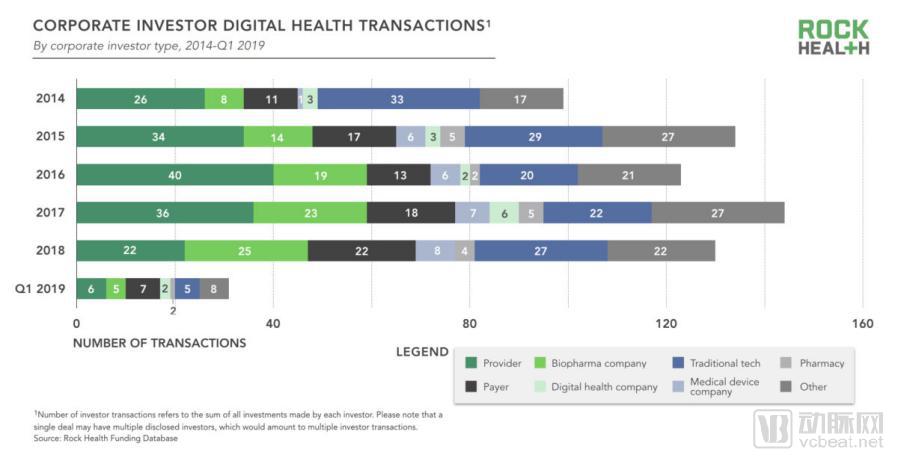

Corporate Investment in Digital Health: Transaction Analysis (Screenshot from the Original Report)

Corporate Investment in Digital Health: Transaction Analysis (Screenshot from the Original Report)

Health systems have long been proactive corporate investors, leveraging their unique capabilities and specialized clinical expertise to identify innovative initiatives targeting healthcare providers and patients.

Kaiser Permanente, Mayo Clinic, and Ascension have been among the more active healthcare organizations over the past five years, each making more than 10 investments since 2014. Moreover, they are three of the 11 corporate venture capital firms whose number of digital health investments has reached double digits.

The last IPO by a U.S. digital health company occurred in 2016, a situation that is set to change rapidly this year. Reportedly, Livongo, Peloton, Change Healthcare, and Health Catalyst are all planning to go public in 2019, with Goldman Sachs and JPMorgan Chase playing leading roles in these four companies’ IPO processes. Among them, Livongo, Health Catalyst, and Peloton have an average history of 10 years and have raised an average of $505 million in funding, which aligns with the historical average observed in prior tracking.

Notably, the prospective IPO candidate Change Healthcare (CHC) was acquired by McKesson for $3.3 billion in 2016, a deal that was hailed by the media as the largest digital health M&A transaction of that year.

While an initial public offering (IPO) represents a significant milestone for early-stage venture capitalists, investors should also closely monitor how these IPOs influence the way companies serve patients, customers, and future public market investors.

Moreover, this potential surge in digital health IPOs was anticipated by several well-known technology companies, including Uber, Lyft, Slack, and Pinterest, which are planning to go public. Interestingly, in its initial public offering (IPO) filing, Lyft specifically highlighted its intention to expand into the healthcare sector to enable more patients to schedule vehicle rides in a timely manner.

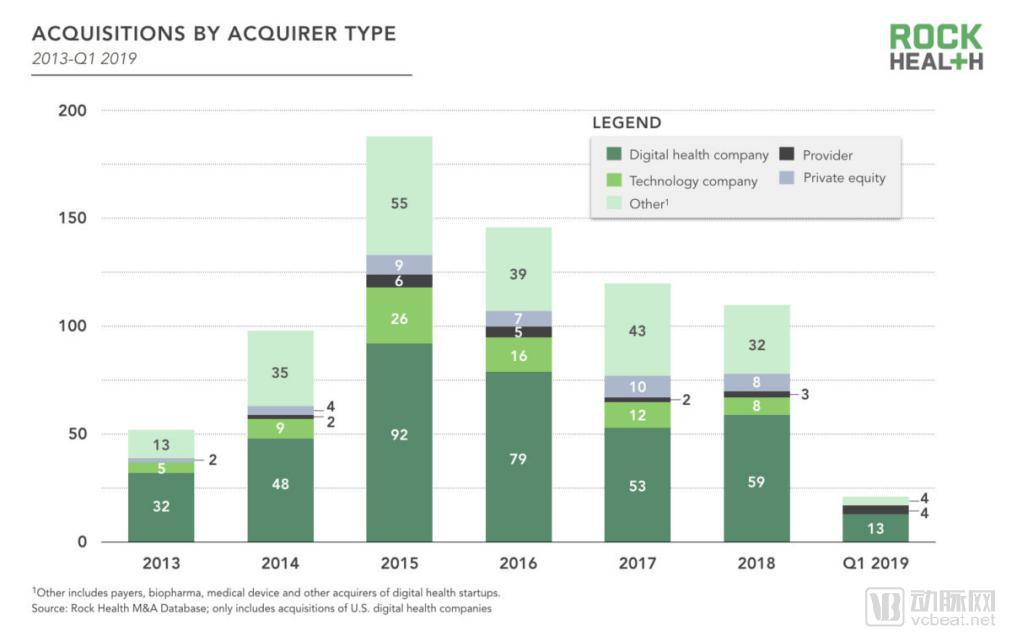

Analysis of Acquisition Types (Screenshot from the Original Report)

Analysis of Acquisition Types (Screenshot from the Original Report)

The pace of digital health M&A slowed in Q1 2019, with 21 startups acquired—a 32% decline from the quarterly average of 31 deals between 2016 and 2018. Consolidation within the digital health sector continued, as digital health companies accounted for 13 of these acquisitions (more than half of the quarter’s total M&A activity).

Behavioral health is gradually becoming a hot sector. Virtual behavioral healthcare provider Ableto acquired Joyable, which offers coach-supported wellness programs to help users overcome anxiety and depression. Meanwhile, Livongo acquired Mystrength, a company that provides evidence-based and clinically assessed therapies such as cognitive behavioral therapy (CBT), marking Livongo’s third acquisition in 18 months.

The acquisition activities of the aforementioned companies represent an industry trend: a growing number of enterprises are bundling multiple products into broader solutions to capitalize on commercial channels driven by shared platforms.

In the first quarter of 2019, 25% of transactions were concentrated in nursing and disease monitoring. This was, to some extent, a response to improved reimbursement mechanisms for digital solutions, particularly Remote Patient Monitoring (RPM) and Chronic Care Management (CCM).

On January 1, 2019, the Centers for Medicare & Medicaid Services (CMS) implemented three new CPT codes for remote patient monitoring. These billing codes establish specific rules and conditions under which healthcare providers can seek reimbursement for delivering services that remotely monitor physiological parameters and provide remote therapeutic management. There is synergy between RPM and CCM services, and these new billing codes signify recognition of the value delivered by digital health companies providing telehealth, chronic care management, and other forms of virtual care.

This represents a significant step forward for the industry, enabling healthcare providers to receive greater reimbursement for services without requiring patients to visit physician offices. If implemented effectively, this approach benefits all stakeholders; consequently, an increasing number of companies are beginning to provide technological support for remote care to healthcare providers.

However, some companies may overly emphasize the short-term benefits under these new CPT codes without placing corresponding importance on the innovation and transformation of their RPM/CCM services, a situation that is more common among startups. Startups may chase short-term revenue because they believe investors will value this over long-term potential and vision. However, in the long run, the healthcare market will severely penalize short-term profit-seeking behavior.

This is why we urge digital health companies to adopt outcome-based business models. Marigold Health serves as a prime example, offering specific reimbursement codes for care coordination services built upon an evidence-based program that rigorously measures and manages patient relapse and readmission rates.

Original article link:

https://rockhealth.com/reports/q1-2019-the-end-of-the-digital-health-ipo-drought/

(Compiled by Xu Shengnan)