Overcoming High Costs and Industrialization Hurdles: Strategic Pathways for Gene Therapy Companies

CAR-T, CRISPR/Cas9, and AAV—these English acronyms were once largely unfamiliar to healthcare professionals a decade ago, yet they have now become central topics of discussion around conference tables. All these acronyms point to the same field: gene therapy. Gene therapy has garnered significant acclaim following the emergence of the CRISPR/Cas9 gene-editing system and experienced another surge in popularity after the successful market launch of CAR-T therapies.

However, in the aftermath of the hype, a re-examination of the industry reveals that numerous challenges have emerged alongside the rapid advancements in gene therapy technology. Although gene therapy techniques are gradually maturing, this nascent industry—launched at breakneck speed—remains plagued by issues concerning the industrialization process for translating scientific research into commercial products, as well as final product pricing.

Gene therapy refers to the introduction of exogenous normal genes into target cells to correct or compensate for diseases caused by defective and abnormal genes, ultimately achieving therapeutic goals. Depending on the pathogenesis of different diseases, various technical approaches such as gene editing and overexpression can be selected. Gene editing and overexpression technologies are at the forefront of therapeutic advancements.

Gene editing officially entered the clinical arena with the advent of CRISPR/Cas9 technology. Compared to zinc finger nucleases (ZFNs) and TALENs, CRISPR/Cas9 offers significant improvements in precision, stability, and ease of use, and has spawned numerous derivative technologies, such as single-base editing and adenine base editing. The CRISPR/Cas9 system provides a new pathway for precise manipulation of human genomic DNA. Although there remains a low probability of off-target effects, the application prospects of CRISPR/Cas9 in the field of gene editing remain highly promising.

Another major approach to gene therapy is overexpression. The therapeutic rationale behind overexpression is straightforward: since a patient’s disease arises from the deficiency or functional inactivation of a specific protein, introducing an exogenous gene that encodes this protein into cells should provide a curative solution. Currently, gene therapies based on overexpression represent the most rapidly advancing class of gene therapy drugs. Luxturna, a gene therapy approved by the FDA last year, utilizes this overexpression-based strategy.

In addition to the two aforementioned approaches, a more prominent category of gene therapy involves combining cell therapy with gene therapy. This method entails extracting autologous cells from patients, performing genetic editing on these cells ex vivo, and then reinfusing them into the patient to treat the disease. CAR-T therapy, which has gained significant attention in recent years, is a key successful example of this approach. Another notable therapy utilizing this method is Strimvelis, which was launched in Europe in 2016.

When discussing gene therapy, it is essential to highlight the key vector that enables its eventual application in clinical settings: adeno-associated virus (AAV). AAV is a type of dependovirus that requires a helper virus (typically adenovirus) for replication. Its genomic DNA is generally less than 5 kb in size, and it exhibits a broad host cell range and low immunogenicity. Consequently, after engineering, AAV has become an excellent vector for delivering gene therapy components into cells.

In addition to AAV, other types of viral vectors include retroviruses and adenoviruses. However, AAV vectors possess a key unique advantage: after entering the cell, the AAV genome does not integrate into the host cell’s genome but instead persists in the nucleus as episomal circular DNA. If a gene were to remain in the cell by integrating into the host genome, the uncertainty of insertion sites during integration could affect the expression of certain genes, thereby introducing unpredictable risks. This characteristic of AAV means that AAV vectors are completely safe for use in gene therapy and do not disrupt normal cellular physiological processes. Since the circular DNA delivered by AAV into the nucleus cannot replicate during cell division, AAV-based therapeutic strategies typically target quiescent cells, such as muscle cells, hepatocytes, and neurons.

To date, in addition to two widely renowned CAR-T products, a total of three gene therapy drugs or therapies have been approved. The first to receive approval was Glybera, a treatment for lipoprotein lipase deficiency; this was followed by Strimvelis, a therapy for severe combined immunodeficiency (SCID); and the third was Luxturna, a drug for inherited retinal dystrophy (specifically Leber congenital amaurosis), which was approved in 2017.

Figure: Glybera

Glybera is the first gene therapy drug approved for marketing in Western countries. Developed by UniQure, Glybera is indicated for the treatment of lipoprotein lipase deficiency. As the name suggests, lipoprotein lipase deficiency is caused by a lack or inactivation of lipoprotein lipase in the patient’s blood. Glybera utilizes adeno-associated virus (AAV) vectors to deliver the gene encoding lipoprotein lipase into skeletal muscle cells, enabling them to secrete lipoprotein lipase into the bloodstream, thereby achieving therapeutic effects through overexpression therapy.

Glybera was approved by the European Union in 2012 and officially launched in 2014. In addition to being the first gene therapy to gain approval, Glybera was also the most expensive drug at the time, with a treatment price of €1.11 million that far surpassed all other medications. However, UniQure cannot be solely blamed for this high price. The indication for Glybera, lipoprotein lipase deficiency, has an incidence rate of only one in a million; only at such a price could UniQure recoup its R&D costs from the limited patient population.

However, patients seemed unconvinced. During the four years Glybera was on the market, only one patient received treatment with Glybera, and this occurred only after substantial reimbursement from an insurance company. In April 2017, as its marketing authorization was about to expire, UniQure announced that it would not seek renewal. Thus, the first gene therapy drug quietly exited the stage. Today, what people still frequently discuss is not the achievements of Glybera, but rather its million-dollar price tag and the awkward reality of treating only one patient over four years.

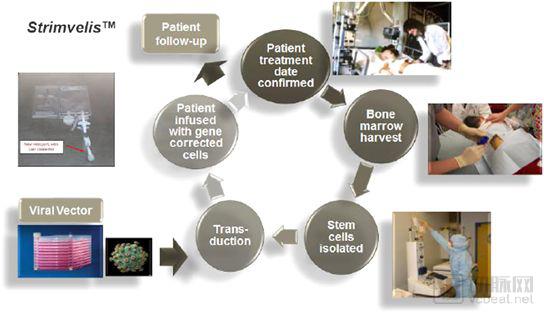

Figure: Strimvelis

Following Glybera, the European Union approved the second gene therapy drug, Strimvelis, in May 2016. Developed by pharmaceutical giant GlaxoSmithKline (GSK), Strimvelis is indicated for the treatment of severe combined immunodeficiency (SCID), with a therapeutic mechanism similar to that of CAR-T therapy. SCID results from abnormal T lymphocyte development caused by adenosine deaminase (ADA) mutations. During Strimvelis treatment, patients’ hematopoietic stem cells are harvested, genetically modified ex vivo to introduce a functional ADA gene, and then reinfused into the patient. These modified stem cells generate normal T cells, thereby rebuilding the patient’s immune system.

Strimvelis is priced at €594,000. Although this is only half the price of Glybera, it can still be considered an astronomical figure. However, there are fewer than 20 patients in Europe each year; even if all of them received Strimvelis treatment, annual sales would amount to only €10 million. Moreover, Strimvelis has not performed well commercially, with its first patient treated nearly a year after approval.

The first CAR-T product, Kymriah, was approved in August 2017, with Novartis taking the lead. Shortly thereafter, in October 2017, Yescarta, acquired by Gilead Sciences, also received approval for marketing. Not long after the approval of these two CAR-T products, the U.S. FDA approved another gene therapy product. In December 2017, the U.S. FDA approved Spark Therapeutics’ Luxturna for the treatment of Leber congenital amaurosis. Luxturna’s therapeutic approach is similar to that of Glybera, utilizing adeno-associated virus (AAV) vectors to deliver a functional RPE65 gene into retinal cells to treat the disease.

Figure: Luxturna

Luxturna’s pricing represents a reduction compared to Glybera, yet it remains as high as $850,000. Ophthalmic gene therapies possess unique industrial advantages. The target cell population in the eye is small and localized, eliminating the need for large-scale viral vector production; pilot-scale manufacturing may suffice to meet clinical demand. Furthermore, Luxturna does not treat all forms of Leber congenital amaurosis (LCA); it is effective only for LCA caused by mutations in the RPE65 gene.

“High cost” is likely an indelible label attached to gene therapy. To date, among the five drugs or treatment regimens approved for market in Western countries, the least expensive, Yescarta, costs $373,000, equivalent to RMB 2.5 million. According to estimates by the International Monetary Fund (IMF), the per capita GDP in the United States was $62,500 in 2018. Even for the American middle class, $373,000 represents a prohibitive expense. Although health insurance covers most of the treatment costs, such exorbitant prices place significant pressure on insurers and may lead to difficulties in reimbursement.

What gene therapy faces is an imbalance between price and patient demand. The indications for gene therapy are predominantly rare diseases, which affect a small patient population; however, the research and development (R&D) process for gene therapies still requires substantial capital investment. Spark Therapeutics spent approximately $200 million developing Glybera. Product pricing must cover costs and generate a certain level of revenue for the company before patent expiration. Given the small target population, the R&D cost allocated per patient necessarily increases. However, excessively high pricing can dampen patients’ willingness to undergo treatment. Therefore, it is difficult to achieve an appropriate balance between gene therapy pricing and patient demand.

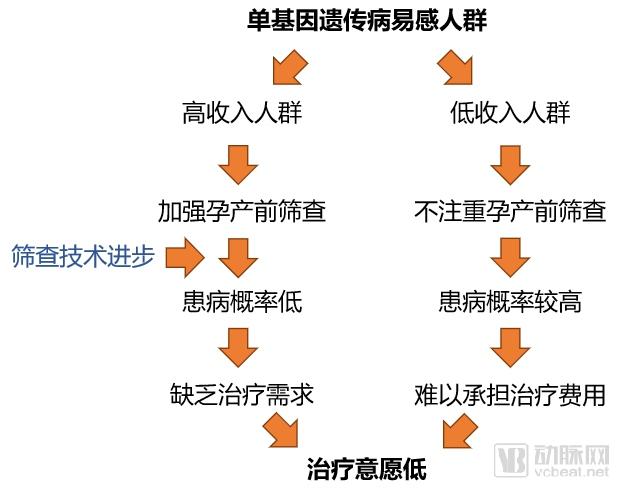

Figure: The Pricing Dilemma of Monogenic Disease Therapies

For monogenic genetic disorders, advancements in screening methods have further complicated the pricing of gene therapies. Due to improvements in prenatal and pre-conception screening technologies, most individuals with access to comprehensive screening undergo thorough testing before birth to mitigate the risk of hereditary diseases. Consequently, newborns who ultimately present with these conditions often come from lower-income households. As a result, gene therapies for monogenic genetic disorders face a dilemma: those who can afford the treatment have little need for it, while those who need it cannot afford it.

Insurance appears to be an excellent solution to this problem. For the sole patient treated with Glybera and the first patient treated with Strimvelis, insurance covered the majority of the costs. However, issues have arisen regarding insurance reimbursement for CAR-T therapy. Although CAR-T has been on the market in the United States for a year and a half, specific details regarding insurance reimbursement have yet to be finalized. In the clinical application of CAR-T therapy, in addition to the cost of the treatment itself, there are many other expenses, including staff training, related equipment and instruments, and hospital profit margins, among others.

Insurance providers have committed to covering patient costs, yet hospitals are experiencing significant delays in receiving payments. Consequently, the resulting financial losses must be borne by the hospitals themselves. According to statistics from two pharmaceutical companies with FDA-approved CAR-T therapies on the market—Gilead Sciences and Novartis—approximately 130 medical institutions in the United States are currently capable of providing CAR-T therapy to patients, but fewer than 2,000 patients have cumulatively received this treatment. While the annual loss incurred by each hospital for treating ten patients may remain within a manageable range for now, such a situation is unsustainable in the long run and hinders the healthy development of the industry.

Although insurance coverage for CAR-T therapy is currently suboptimal, medical insurance remains one of the most effective solutions to address payment challenges. Only insurance has the capacity to cover the high treatment costs for the majority of patients. Benefiting from advancements in the gene therapy industry, insurance policies will become more comprehensive, and the efficiency of processing claims for relevant patients will increase significantly.

Amid inadequate insurance reimbursement, companies are beginning to compromise on alternative payment models. Learning from the lessons of Glybera, Luxturna allows for multiple payment mechanisms to coexist. First, Luxturna commits to a pay-for-performance model, under which it will refund a portion of the treatment costs if the drug fails to achieve short-term (30–90 days) and long-term (30 months) therapeutic outcomes. Meanwhile, Luxturna permits patients to pay for treatment in installments, significantly lowering the financial barrier to access. In the first three quarters of 2018, Luxturna generated $15.6 million in revenue for Spark Therapeutics, with continued growth over several quarters. Although such payment arrangements may affect the company’s cash flow recovery, it is more critical to secure product sales than to face stagnant market uptake.

Another critical issue in the gene therapy industry is industrialization. Technological maturity has been achieved only at the research level, and bridging the gap from research to clinical application remains an urgent challenge for the gene therapy sector. Patrick Rivers, head of Aquilo Capital Management, stated at a forum organized by the Alliance for Regenerative Medicine that the most crucial factor when evaluating portfolio companies is their manufacturing processes, particularly for gene therapy developers reliant on viral vector supplies.

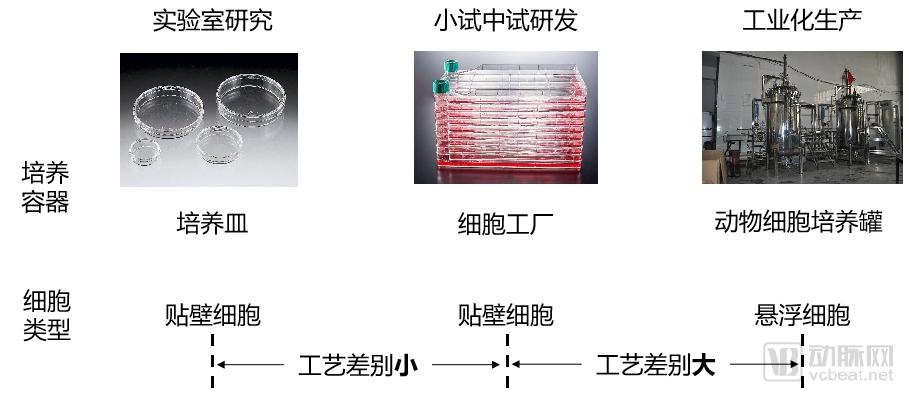

Figure: The Process Gap from R&D to Industrial-Scale Production

Taking AAV packaging as an example, the quantity of AAV vectors used in mouse experiments can be met by culturing adherent cells in petri dishes. For further applications, such as primate studies or clinical trials involving one or two patients, larger culture flasks or cell factories may barely suffice. This mode of product supply can address small-scale experimental needs; however, it incurs high costs and fails to ensure consistency between experiments.

If a drug candidate ultimately advances to mass production, relying solely on laboratory-scale cell culture techniques is insufficient. The culture systems may need to be upgraded to larger bioreactors, and the cell types may need to be switched from adherent to suspension cells. During this scale-up process, the entire cell culture system undergoes significant changes, rendering established small-scale and pilot-scale processes developed in the laboratory unsuitable for direct application in industrial manufacturing. Consequently, industrial production requires re-optimization of all parameters, ranging from cell culture and transfection methods to virus concentration. In addition to changes in culture methods, the establishment of clinical standards must also be considered. Ensuring that products transitioning from research to clinical use meet clinical standards, and maintaining consistent stability across different batches, are critical challenges to be addressed in the industrial production of gene therapies.

Although gene therapy products have been successively launched on the market, the industry as a whole lacks clear consensus. The industrial manufacturing models for these products are treated as proprietary trade secrets within individual companies and even serve as key competitive assets in the industry. Details of the production processes for already marketed products remain confidential. Those unfamiliar with the field are left to grope in the dark, while those with knowledge remain tight-lipped, making the industrialization of the gene therapy sector even more challenging. Dennis Purcell, founder of Aisling Capital, once noted that clinical trials in the gene therapy industry are quite transparent; however, they encountered significant difficulties when conducting due diligence on manufacturing operations.

The first option is to build in-house facilities. Recently, many leading gene therapy companies have begun constructing industrial-scale manufacturing plants. Bluebird bio’s new gene therapy facility in North Carolina was inaugurated last month; AveXis, a subsidiary of Novartis, announced in February 2019 that it would expand its North Carolina plant, and in April further announced the acquisition of a manufacturing facility in Colorado to produce its upcoming gene therapy for spinal muscular atrophy, Zolgensma. Amid an industry-wide shortage of third-party contract manufacturing organizations (CMOs), many companies have opted to build their own GMP-compliant production facilities, a path that also represents the future direction for most startups.

The second option is to anticipate acquisition by large pharmaceutical companies. In fact, major pharma giants such as Pfizer, Novartis, and Roche are actively expanding their presence in the gene therapy sector. Notably, Juno Therapeutics and Kite Pharma, two leading CAR-T companies, were acquired by Celgene and Gilead Sciences, respectively. Large pharmaceutical companies possess greater expertise in product commercialization and have ample cash flow to sustain project progress and industrial-scale R&D.

In addition to the two aforementioned approaches, third-party contract manufacturing organizations (CMOs) represent an excellent solution to this challenge. If gene therapy becomes a focal point of the healthcare industry in the coming years, the CMO sector serving gene therapy will inevitably experience corresponding growth. Although the lack of standardized processes has made the initial development of the CMO industry challenging, these greater challenges also bring greater opportunities. At this current juncture, where the industrialization of gene therapy has become a prominent issue, significant opportunities lie before the relevant CMO industry. Companies that can successfully address the industrialization challenges of gene therapy products are poised to rapidly grow into unicorns within this cutting-edge sector.

At a forum hosted by the Regenerative Medicine Alliance, Matthew Gline, Chief Financial Officer of Roivant Sciences, expressed a positive outlook. He believes that addressing manufacturing needs presents an excellent opportunity for startups. Such companies could spare more gene therapy firms from the challenges of industrialization and ultimately grow to occupy a position in the industry analogous to Illumina’s role in genetic testing.

Everyone hopes for medicines that are accessible, affordable, and effective. However, current gene therapies fall far short of meeting these standards. In fact, this situation is not unique to the gene therapy industry; rather, this rapidly emerging sector has amplified the impact of these challenges. Similar issues exist in other fields, such as targeted drug development, genetic testing, and liquid biopsy. While technological advancements will ultimately overcome these hurdles and make these cutting-edge technologies widely accessible, the key question remains: how long will it take for these nascent technologies to mature?

Today, it is the gene therapy industry that remains trapped by challenges in pricing and industrialization. When gene therapy successfully breaks through these barriers, will other industries find themselves facing the same dilemmas? Can the healthcare sector draw lessons from gene therapy’s experience to ensure that emerging industries are no longer constrained by these long-standing issues? These problems will ultimately be resolved; we only hope that day arrives sooner rather than later.