Fragmentation of Physical Hospitals and the Rise of Integrated Internet Healthcare Ecosystems: New Investment Opportunities in Medical Innovation

Interesting changes are underway in the healthcare industry. On one hand, offline healthcare service providers are shifting from centralization to decentralization. Medical imaging diagnostic centers, pathology diagnostic centers, hemodialysis centers, and sterile supply centers have been spun off from the public system. Coupled with the consumerization of specialized departments such as ophthalmology, dentistry, and medical aesthetics, the decentralization of healthcare service entities has become increasingly evident.

On the other hand, shifting focus to the online sector reveals that digital health platforms have adopted a “comprehensive and all-encompassing” model. They are systematically filling in every link of the value chain—from online consultation and diagnosis, to prescription issuance and drug supply, to health management, and even commercial health insurance—through self-development, partnerships, and investments.

Why has the online and offline healthcare service system exhibited such "divergence"? Is it driven by demand or profitability requirements? Is it a result of business models or technological advancement? Amidst decentralization and centralization, what investment opportunities can be uncovered?

“The Innovator’s Prescription” describes the current predicament faced by hospitals as follows: Technological advances have enabled standardized treatment protocols for diseases that can be precisely diagnosed. Consequently, hospitals simultaneously operate under two distinct business models—the value-added services model and the expert-led model—within the same institution, making them among the most difficult organizations to manage in the history of capitalism.

The core logic of the value-added service model is to follow established procedural standards and charge consumers based on work outcomes. In contrast, the expert-led model relies more heavily on physicians’ cognition and judgment, constituting experience-based medical care. It typically adopts per-visit or per-service fee structures, with payers required to pay a significant premium for the professional services provided by “experts.”

The rationale for “unbundling” public general hospitals stems precisely from this issue. Under the previous system, hospitals operated in silos, hindering effective information sharing. Even within a single hospital, patients were shuttled back and forth among different departments and examination rooms, undergoing numerous redundant tests. Clearly defining diagnostic and treatment pathways from the outset would significantly enhance medical efficiency and reduce costs, which holds immediate significance in the context of cost containment.

The rationale for spinning off departments such as ophthalmology, dentistry, and medical aesthetics from the public healthcare system differs slightly. These departments have traditionally been peripheral within hospitals, and their separation can significantly enhance patient experience. Such improvements in experience are often predicated on higher pricing, which also reflects the improved business prospects following the spin-off.

In summary, the unbundling and restructuring of the public healthcare system are built upon a core framework of “cost containment + revenue generation.” The former enables hospitals and regions to share laboratory and diagnostic information, thereby reducing medical costs; the latter involves spinning off consumer-oriented departments to achieve higher returns on fixed investments in equipment and personnel. Whether through unbundling or restructuring, these trends represent key themes for future healthcare investment.

The development of online pharmaceutical services differs from that of offline services. Its core logic lies in the digitalization of the medical care process, i.e., migrating all medical procedures that can be conducted online to digital platforms. Apart from laboratory testing and examinations, services such as appointment scheduling and consultation, clinical diagnosis and treatment, chronic disease prescription, medication management and rehabilitation, and health management can all be completed online.

The costs of internet-based pharmaceutical services are largely “reusable,” meaning that a single investment can be leveraged multiple times and iteratively updated. Taking online consultations as an example, whether searching for specific symptoms on Chunyu Yisheng or Haodafu platforms, users can find dozens or even hundreds of physician-patient Q&A entries. New patients can refer to these resources, which offer far greater detail than a typical five-minute outpatient visit.

The reuse of information also brings a disadvantage: users leave immediately after reading, failing to achieve effective conversion. However, savvy internet professionals have devised an alternative approach—one-stop solutions. They attract traffic through disease education and search engines, retain users who require further consultation by offering advisory services, and subsequently provide prescription and medication purchasing services. Internet platforms function like a funnel, continuously filtering user needs to realize value conversion. Users enjoy a nearly seamless experience, fixed costs are diluted by the continuously growing volume of services, and profits gradually increase.

Internet healthcare platforms have also begun to “empower” offline institutions, aiming to further expand traffic entry and exit points, create more service opportunities, and generate additional revenue streams. Taking pharmaceutical e-commerce as an example, services initially consisted solely of online pharmacy operations, but later gradually expanded to include online consultations and prescription services. If users seek offline services, these platforms provide support to offline institutions through services such as medical consultations and drug procurement. The business expansion of leading platforms such as 1YaoWang (1 Drug Network), Ali Health, and Jianke follows this trajectory.

Physical Entities Move Left, the Internet Moves Right. This does not imply that the two follow entirely divergent development paths; rather, it reflects a natural choice driven by distinct business models and technological contexts—namely, always opting for directions that facilitate platform growth, enhance operational efficiency, and improve user experience.

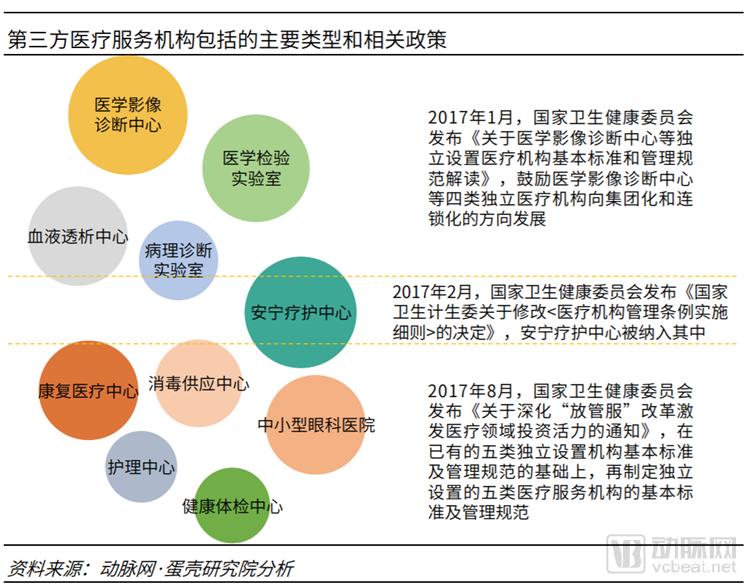

For the booming third-party medical service providers, they can be broadly categorized into two types. One type includes medical imaging diagnostic centers, medical laboratories, pathology diagnostic laboratories, and sterile supply centers, which provide auxiliary services to medical institutions through specialized equipment and personnel. The other type comprises hemodialysis centers, hospice care centers, rehabilitation medical centers, nursing centers, and small- and medium-sized ophthalmic hospitals, which represent the specialization of departments within general hospitals. However, whether providing auxiliary services or representing departmental specialization, all will face challenges from the existing system.

Public hospitals have grown accustomed to the “large and comprehensive” model; even county-level hospitals, though small in scale, are fully equipped with all necessary departments and a complete array of laboratory and diagnostic equipment. If auxiliary third-party medical service providers fail to gain recognition from public hospitals, market expansion will be exceedingly difficult.

Public tertiary Grade A hospitals exhibit a significant “siphon” effect on patients, resulting in high patient volumes. This determines that the primary source of business for ancillary third-party medical services will be these large tertiary Grade A hospitals. The more concentrated the customer base, the greater the customers’ bargaining power, which will compress the pricing of third-party medical services. Furthermore, public tertiary Grade A hospitals already have very low costs for inspection and testing, supported by medical insurance. If third-party medical institutions fail to deliver service quality that meets or exceeds that of general hospitals, patients will engage in adverse selection.

Tiered diagnosis and treatment may also hinder the development of third-party medical services, as a key policy under this framework is the Medical Consortium. The Medical Consortium aims to “separate acute and chronic care management and facilitate referrals between primary and tertiary levels.” In practice, however, these consortia are led by Grade 3A hospitals, with lower-tier hospitals referring patients upward, thereby further strengthening the patient-siphoning effect of comprehensive Grade 3A hospitals.

In terms of departmental specialization, mature models have already emerged in fields such as ophthalmology, dentistry, and medical aesthetics, giving rise to specialized chain healthcare groups, publicly listed companies, and healthcare management firms. The long-standing challenges in specialty expansion—namely talent acquisition, operations, and cost control—have hindered the scalable replication of departmental specialization. In contrast, public hospitals hold a competitive advantage: they attract talent through opportunities for professional title advancement and research, enjoy stronger brand recognition and reputation, face no shortage of patients, and benefit from government subsidies.

The key to competitive differentiation in specialized departments lies in offering services and experiences distinct from those of general hospitals, with a greater reliance on professional talent—particularly physicians with strong brand recognition and reputations. Expansion efforts must balance speed and quality, avoiding blind investment. It is also advisable to moderately explore supply chain integration, such as strategic positioning in medical equipment, consumables, and raw materials. This approach not only helps reduce operational costs but also unlocks the advantages of supply chain synergy.

“Digitalization + Pharmaceuticals” has formed a complete ecosystem. Digital tools or technologies undoubtedly possess the qualities most urgently needed by the pharmaceutical industry. This refers to the application of internet and information technologies across various stages of pharmaceutical operations to transform existing business processes and models, with the primary aim of reducing costs, improving efficiency, or both.

From the R&D perspective, new technologies such as artificial intelligence have improved the efficiency of target screening, molecular discovery, and crystal form construction. From the clinical perspective, electronic data capture systems, big data technology, and digitalization have enhanced data mining capabilities. From the market perspective, “Internet Plus” has increased drug accessibility, with new retail gaining significant momentum. Digital technology serves as the foundational infrastructure and is one of the most critical drivers in the pharmaceutical industry.

The research and development of innovative drugs is time-consuming, capital-intensive, and high-risk. Although technologies such as artificial intelligence and big data have been extensively applied in the pharmaceutical industry, it will take time for these investments to yield returns. In contrast, the changes brought by the internet in the distribution and trading sectors are, to some extent, more “immediate.”

Taking “Internet + Pharmaceutical Wholesale” as an example, there are more than 500 players in the B2B pharmaceutical e-commerce sector. Since 2016, companies such as Rongguan E-commerce, Yaopin Zhongduan Wang (Pharmaceutical Terminal Network), Weiming Penguin, Yao Pianyi (Medicine Cheap), and Yaoshibang (Pharmacist Helper) have secured multiple rounds of financing, with cumulative funding exceeding RMB 1 billion. Investors include Matrix Partners China, Chengwei Capital, GGV Capital, Ivy Capital, Fosun Pharma, and SoftBank China.

Online pharmaceutical trading platforms target the out-of-hospital market, namely small pharmacy chains, independent pharmacies, and clinics. Prior to the emergence of online trading platforms, the pharmaceutical distribution chain involved numerous tiers, lacked transparency, and featured a fragmented operational structure with over 13,000 drug distributors across China, resulting in process costs far exceeding the actual cost of the drugs themselves. The advent of the online model has broken down these barriers and fostered a cohort of internet-enabled pharmaceutical distributors. Subsequently, drug trading platforms have expanded into supply chain finance, smart logistics, and other services, further enhancing the efficiency of pharmaceutical distribution.

E-commerce in the pharmaceutical sector has evolved from a single-minded focus on online transactions of drugs and health supplements to an integrated service model that combines patient education, medical consultations, prescription refills for chronic diseases, and health management. Furthermore, it is actively expanding into offline channels by opening physical stores, integrating into healthcare service processes, and even entering the pharmaceutical distribution sector.

Alibaba Health’s development is the most representative. In its early stages, it primarily relied on self-operated product sales, supplemented by e-commerce platform revenue, to sustain its growth. As its e-commerce platform business matured, the company began expanding into smart healthcare, internet hospitals, and health management services. It also partnered with offline chain pharmacies to develop online-to-offline (O2O) medication delivery services, and subsequently further invested in and acquired controlling stakes in regional pharmacy chains such as Guizhou Yishu and Gansu Deshengtang. Currently, its key strategic priority is to integrate into the hospital system, laying out services including appointment registration and consultations, payment solutions, and medical artificial intelligence (AI).

111 Group is another typical case. 1YaoWang initially started as a sub-channel of Yihaodian, later operated independently, and eventually evolved into the 111 Group with its “three pillars”: the B2C pharmaceutical platform “1YaoWang,” the internet hospital “1Zhen,” and the B2B pharmaceutical platform “1YaoCheng.” Through an innovative T2B2C model, it has comprehensively achieved integrated development across B-end and C-end, online and offline, self-operated and platform-based, as well as medical services and pharmaceuticals. Recently, 111 Group has also been exploring collaborations with commercial insurance companies to develop new insurance products and pilot PBM (Pharmacy Benefit Management) services.

Other platforms, such as Jianke, Qilekang, and Kangaidu, have also followed a “from simple to complex” development logic: starting as e-commerce players, then expanding into a synergistic “healthcare + pharmaceuticals” model, with all of them covering online hospital services or pharmaceutical distribution businesses.

The logic behind the transformation of “Internet + Healthcare” is shifting from serving customers to serving the industry. In the initial model, B2B e-commerce platforms served small-scale end-users, while B2C pharmacies catered to individuals. However, the healthcare industry itself constitutes a complete “ecosystem,” where a closed business loop can only be achieved through collaboration among pharmaceutical manufacturers, medical institutions, and drug distribution channels. As an intermediary, “Internet + Healthcare” enterprises can leverage technology and traffic to support and rejuvenate the industry.

Online Integration, Offline Diversification: How Do Professional Investors View This Trend? Li Zhe, founder of Baichuanghui, a medical investment and incubation firm, told VCBeat that the primary driver behind these two major shifts is “healthcare reform.”

As emphasized in the guiding principles for promoting “Internet + Healthcare,” developing “Internet + Healthcare” services can enhance the modernization of healthcare management, optimize resource allocation, innovate service models, improve service efficiency, reduce costs, and meet the growing public demand for medical and health services. Meanwhile, vigorously developing third-party medical services can provide “multi-level and diversified” healthcare offerings, thereby addressing the scarcity and accessibility issues of high-quality medical resources from the supply side.

How to Seize Innovation and Investment Opportunities Driven by Policy and Technology? Huang Shengxuan, Managing Director of Sunshine Ronghui Capital, Proposed the "Three New" Concept for Healthcare Investment: New Technologies, New Models, and New Payment Mechanisms. Specifically, new technologies refer to biotechnology, immunotherapy, artificial intelligence, big data, and other advancements; new models involve the reorganization and redistribution of healthcare resources, including the aforementioned shift from centralized to distributed third-party medical services, tiered diagnosis and treatment systems, and the upgrading of healthcare consumption experiences.

Payment Reform Is a More Critical IssuePayment reform has become an increasingly critical issue, particularly within China’s payment system dominated by basic medical insurance. Driven by factors such as population aging, the operational pressure on basic medical insurance funds is intensifying, leading to stricter cost-containment measures. The National Healthcare Security Administration (NHSA) has emerged as the primary implementer of cost containment, executing its strategy through adjustments to the medical insurance reimbursement list, centralized volume-based procurement of pharmaceuticals, and reforms in payment methods. Meanwhile, innovation in pharmaceuticals and medical devices is being encouraged to replace low-value products with high-value ones, thereby achieving a strategic reallocation of medical insurance fund resources, often described as “vacating the cage to change the bird.”

In contrast, the commercial medical insurance market continues to expand, with commercial health insurance increasingly becoming a significant payment force in the healthcare sector. The industry itself is undergoing transformation: from accelerating innovation and optimization of traditional health insurance products, to closely integrating with healthcare services, exploring managed care models, and applying technologies such as artificial intelligence and big data to actuarial science, risk control, and other areas. Furthermore, the specialized capabilities of commercial insurers are also serving basic medical insurance, including participation in critical illness insurance programs and cost-containment initiatives within the public insurance system. These changes in commercial insurance stem from shifts in the policy environment and social demands, particularly its synergy and coordination with healthcare reform.

No industry remains static; whether it is the spin-off of general hospitals or the business expansion of online platforms, these developments align with the current medical policy environment, market trends, and end-user demands. The only constant is a patient-centric approach that builds a “value-based healthcare” system by addressing unmet needs.