Beyond the Bubble: What Drives High Valuations in Biotech Startups?

For pharmaceutical entrepreneurs, the most classic description of the 21st century is none other than the phrase, “The 21st century is the century of biotechnology.” The leapfrog progress in medical solutions driven by biotechnological innovations has also revealed the potential of biotechnology to benefit human health. Meanwhile, their market potential has attracted a surge of capital investment.

In 2018, the venture capital community experienced a so-called “capital winter,” yet even in this environment, biotechnology financing and investment set multiple records that year. According to the 2019 annual report released by Silicon Valley Bank, the total value of exits (including IPOs and M&A) in the biopharmaceutical industry exceeded $49 billion in 2018, with several transactions valued at over $1 billion each. The total value of venture capital deals also surpassed $9.6 billion in 2018. Notably, Moderna Therapeutics, valued at $7 billion, went public on the NASDAQ, marking the largest IPO in the history of the biotechnology sector to date.

Capital has been pouring into biopharmaceutical R&D like a torrent. We are witnessing growing enthusiasm among investors, driving biopharma company valuations to new heights. Notably, Bristol-Myers Squibb’s management proposed a $74 billion offer, while Roche’s bid for Spark Therapeutics approached $5 billion. Companies such as Juno Therapeutics and Aduro Biotech saw their valuations rapidly surpass the $1 billion mark within just a few years. Indeed, recent years have seen the emergence of the largest number of unicorns in the biopharmaceutical sector.

“To reach unicorn status, you first need to find venture capital firms willing to offer such a valuation,” said Mike Pellini, former CEO of Foundation Medicine, in an interview. He noted that while the reasons behind this are difficult to summarize, becoming a true unicorn necessarily requires investors willing to pay the corresponding price. So, what factors motivate venture capital firms to offer high valuations?

Biopharmaceutical investment is an investment in life sciences, so what are the quantitative indicators of whether the technology is top-notch? From an academic research perspective, the number of published papers and impact factors are inevitably the main reference factors. Is this also the case in the industry? Dr. John Ioannidis from Stanford University School of Medicine conducted a study.

Under the leadership of Dr. Ioannidis, researchers compared 18 unicorn companies with 29 former unicorns that had exited, tallying the number of papers published by these enterprises as well as the number of highly cited articles (those with more than 50 citations). Ioannidis referred to this as “secret research.”

PitchBook once compiled a list of publicly traded companies with valuations exceeding $1 billion, three of which were included in Ioannidis’s study: Aduro Biotech, FibroGen, and Juno Therapeutics. Among these three, both Aduro Biotech and FibroGen had several highly cited papers, whereas none of Juno’s 21 papers met the threshold for highly cited articles by the authors, despite the company providing key data on its lead candidate product, the CAR-T therapy JCAR017. These studies indicated that this product offered a better safety profile than the two already marketed alternatives.

Notably, rare disease treatment company Enobia Therapeutics also published few papers, yet it was acquired by Alexion Pharmaceuticals for $1.08 billion in 2012, and its product Strensiq received FDA approval for the treatment of hypophosphatasia, a rare metabolic disorder.

Notably, companies similar to Juno and Enobia were more prevalent in Ioannidis’s study. Ioannidis argued that, due to time constraints, publishing papers is not the primary priority for startups. Furthermore, a large volume of publications does not necessarily translate into a significantly high valuation for the company.

“Beyond the technology itself, corporate valuations are influenced by multiple factors, such as insider information and marketing,” said Ioannidis. “However, without scientific underpinning, these valuations may lack objectivity, exposing venture capital investments to significant risk.”

However, venture capitalists hold a slightly different perspective. Robert Nelsen, Managing Director at ARCH Venture Partners, believes that the lack of public data should not be equated with being “closed.” Known as the “adventurers” of the investment world, ARCH Venture Partners has specialized in life sciences investments for over 30 years, excelling at identifying new opportunities in early-stage technologies. Its portfolio includes numerous unicorn companies such as Kythera Biopharmaceuticals, Juno Therapeutics, CStone Pharmaceuticals, and GRAIL, earning it the reputation of a “unicorn factory.”

“Only if a fund can leverage its professional expertise to validate the data and technological pathways, and determine that the value of such data exceeds RMB 1 billion, can it gain a first-mover advantage in investment.” He believes that the ideal scenario is for portfolio companies to maintain confidentiality for as long as possible, but this secrecy should be directed toward the public, not investors. Nelsen pointed out that startups keeping information confidential from investors is a red flag, which was precisely why they declined to invest in Theranos.

“I love my company; we only invest in science that has real value,” said Nelsen. “Before making an investment, we consult with Nobel laureates and numerous industry experts.” To mitigate potential biases, the company does not pay the scientists who provide advice. “They must be genuinely enthusiastic about the technology to devote their time to evaluating it and advocating for its merits,” he explained.

Unlike ARCH Venture, another star venture capital firm, OrbiMed, places greater emphasis on clinical data. Jonathan Silverstein, Co-Head of OrbiMed’s Global Private Fund, stated, “Clinical data trump everything.” He noted that if there are suspicions of data fabrication, a medical expert can be hired to verify the data. Although Ioannidis believes that companies failing to disclose their data lack credibility, investors have their own rationale for conducting due diligence on portfolio companies.

In summary, we can conclude that the number of publications and citation frequencies offer certain reference value for technology assessment. However, the industry differs from academia; beyond publication impact and volume, investors place greater emphasis on the technology itself and its clinical application status.

Nelsen also revealed that, for ARCH Venture Partners, the value of a platform outweighs that of a single asset; a company’s growth potential and its significance in driving technological change are key factors in investment decisions. This, of course, is a strategy also embraced by many domestic investment firms.

In April 2017, Aimab Therapeutics, founded just one year earlier, secured $25 million in Series A financing. Despite its products not yet having entered clinical stages, the company still achieved a favorable valuation. Aimab Therapeutics is a typical platform-based startup for novel drug development. Its founder, Wu Chenbing, was a key inventor of Abbott’s DVD-Ig bispecific antibody technology platform, which Abbott continues to utilize to this day. Leveraging its independently developed innovative research platform, Aimab Therapeutics entered into a $120 million technical collaboration with Innovent Biologics merely four months after its establishment, setting a new record for biopharmaceutical technology licensing deals in China at that time.

In most cases, the growth potential of a single-product strategy is limited; if R&D fails, the results may be completely wiped out. However, if a company possesses its own proprietary R&D platform, successful launch of the first product can be followed by a pipeline of new products, and even in the event of R&D failure, there remains an opportunity to rebound. Furthermore, leveraging a technology platform enables the company not only to conduct independent product development but also to generate early-stage revenue through technology licensing.

“A technology platform is a living source of water, whereas a single-product pipeline is a tree without roots,” remarked an investor who requested anonymity. Data from the VCBeat knowledge base reveals that R&D-focused startups such as Crystal Pharma, Hongyun Huaning, Biocytogen, and Adagene have secured relatively substantial valuations during their fundraising rounds. While not the sole determinant, companies equipped with proprietary R&D platforms undoubtedly enjoy certain advantages in securing financing.

Another point raised by Ioannidis is the convergence of disciplines. “We are in a transformative period marked by interdisciplinary integration,” he described. With the dual rise of biotechnology and information technology, there is increasing collaboration involving artificial intelligence, machine learning, and other technologies in the pharmaceutical sector, particularly in their applications for drug discovery and treatment.

“Part of the reason lies in the mutual demand for each other’s professional expertise, leading to increasingly frequent interactions between them,” said Jonathan Norris, Managing Director at Silicon Valley Bank. “They can benefit from each other’s specialized knowledge.”

Senti Biosciences, based in San Francisco, California, is a representative company in the field of interdisciplinary innovation. The company is dedicated to developing cell and gene therapy products using synthetic biology, with the integration of life sciences and computer science being one of its key features. In February 2018, the company completed a $53 million financing round led by New Enterprise Associates, a technology-focused investment firm, with participation from 8VC, which leverages IT technology to address challenges in biotechnology.

Dr. Susumu Tonegawa, Nobel Laureate in Physiology or Medicine, once proposed that “except for trauma, all human diseases are related to genes.” The essence of life lies in chemical and physical reactions governed by the genomic program; fundamentally, life is information. From the moment genes are assigned, an individual’s lifelong biological information is predetermined. Tang Yuanhua, founder of Shoudu Gene, stated, “In other words, all life on Earth can be understood as a program—a biochemical and physical process controlled by the genome.” This perspective aligns closely with the philosophy of Senti Biosciences, which posits that if genetic information constitutes humanity’s source code, then diseases resemble “bugs” arising during code execution. Senti aims to develop adaptive therapies to correct these errors.

Beyond therapeutic research, greater cross-industry integration among companies is evident in drug discovery and medical big data projects. After acquiring Iceland’s NextCODE for $65 million, WuXi AppTec merged it with its WuXi NextCODE Center to establish the current entity, NextCode Genetics (Mingma Biology). In addition to sequencing services, NextCode Genetics’ standout feature is its AI-driven data mining. As precision medicine data enters a phase of exponential growth, mining genomic and clinical phenotypic data may yield novel insights. Empowered by artificial intelligence, NextCode Genetics can identify driver genes within molecular pathways to facilitate drug design or disease diagnosis, leverage pathogenic variants to recognize undiagnosed disease subtypes, and uncover core disease mechanisms as well as progression and survival indicators across diseases.

Of course, the broader application of artificial intelligence in biomedicine lies in drug development. In 2017, VCBeat·VBInsight released the “2017 Report on the Medical Big Data and Artificial Intelligence Industry,” which highlighted seven innovative directions for AI in drug R&D, primarily focusing on the new drug discovery phase and the clinical trial phase, totaling seven areas.

Source: VCBeat · VBInsight

In terms of financing amounts, most of these companies are highly valued.

The underlying reason for this phenomenon is the cultural convergence between life sciences investment and venture capital. Technology investors have historically possessed a keen eye, whereas investment in the life sciences sector is more methodical.

However, Nelsen disagrees with this view. He believes that the influence of tech investment culture is more evident in health technology and hybrid sectors, but has not yet penetrated the core technological domains of life sciences.

“The pure biotech professionals I know have not joined this large-scale movement. I believe this phenomenon is actually driven by various factors,” he stated. In particular, as the pace of innovation accelerates and potential impact grows, biopharmaceutical startups have attracted a group of investors willing to provide long-term support.

“From the perspectives of valuation and investment pace, it seems that tech investors have accelerated their activities in this process,” he continued. In an era where most institutions are placing heavy bets, investment firms face considerable competition among themselves; however, he emphasized that this does not imply inadequate due diligence on their part.

According to the "2014-2018 Investment and Financing Data Report in the New Pharmaceutical Sector" released by VCBeat·VBInsight in 2019, 2014 marked a significant turning point for global investment and financing in the biopharmaceutical sector. The total global financing amount in this field remained below $500 million in both 2011 and 2012, before surpassing $1 billion for the first time in 2013. However, despite the increase in total financing volume in 2013, the number of investment and financing transactions remained at previous levels. Prior to 2013, innovation in biopharmaceuticals had not received sufficient attention.

Since 2014, financing in the biopharmaceutical sector has experienced rapid growth, with increases in both the number of financing deals and the total amount raised. By 2018, global financing in this field had exceeded $17.4 billion, nearly ten times the 2014 level.

Furthermore, the share of biopharmaceutical financing within the overall healthcare industry has been steadily rising. In 2014, this figure stood at merely 20%, whereas by 2018 it had essentially reached 35%. The proportion of investment deals also hit 30% and continues to show an upward trend. Internal competition exists in every industry. As most institutions have turned their attention to the biotechnology sector, investment competition has inevitably intensified. In the race to secure high-quality projects, phenomena such as “price inflation” are unavoidable.

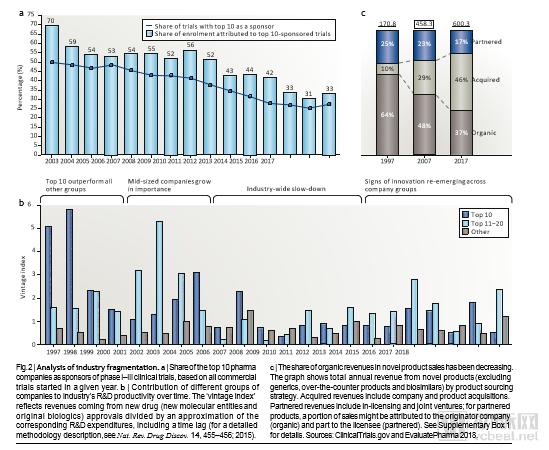

Of course, the influence of large companies in an industry is also significant, and their actions will impact the development of the industry. Data from Nature Reviews Drug Discovery shows that in recent years, the total revenue of the top ten pharmaceutical giants accounts for about 40% of the overall industry revenue. However, compared to earlier years, this figure has declined to some extent. In the early 2000s, this proportion could reach 50%.

Behind this phenomenon lies the fragmentation of R&D capabilities among pharmaceutical companies. Among Phase I–III clinical trial applications accepted by the FDA, the share accounted for by the top ten companies has declined from 50% in 2000 to 27% in 2017.

Image source: Nature Reviews Drug Discovery

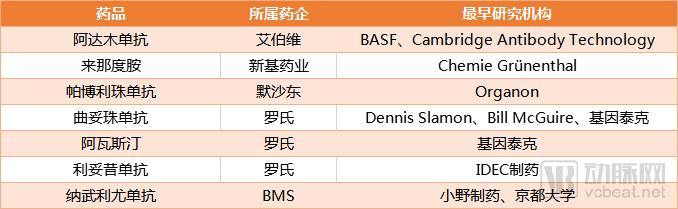

Two decades ago, large pharmaceutical companies remained the primary drivers of R&D in the pharmaceutical industry. It was not until the early 21st century, with the advent of monoclonal antibody therapies, that innovation in drug development began to shift outward. From the 1990s to the early 2000s, major pharmaceutical firms also achieved considerable success through a series of acquisitions. For instance, Opdivo, the flagship product of Bristol Myers Squibb (BMS), was initially co-developed by Japan’s Ono Pharmaceutical and Kyoto University. Later, U.S.-based Medarex entered into an R&D collaboration with Ono Pharmaceutical. BMS subsequently acquired Medarex, thereby securing the rights to Opdivo—a move that proved pivotal in BMS’s patent dispute victory over Merck & Co.

Moreover, it is evident that the majority of the top-selling drugs in global rankings were acquired by pharmaceutical giants through mergers and acquisitions.

In recent years, the pharmaceutical industry has also witnessed a continuous wave of mergers and acquisitions, where larger companies absorb smaller ones.

Gilead acquired Kite Pharma for $11.9 billion, propelling itself into the top tier of gene therapy; Sanofi acquired Bioverativ for €11.6 billion to obtain the latter’s portfolio of treatments for rare blood disorders; Takeda Pharmaceutical ultimately secured Shire for $62 billion, consolidating its influence in core rare disease areas including hematology, immunology, genetic disorders, neuroscience, and internal medicine; Eli Lilly acquired Loxo Oncology for $8 billion to strengthen its oncology pipeline; and Roche acquired Spark Therapeutics for $4.8 billion to address its gaps in gene therapy. The most sensational development, however, was the series of acquisitions involving Bristol-Myers Squibb (BMS), Celgene, and Juno Therapeutics. First, Celgene acquired Juno at $90 per share to obtain its CAR-T product, and a year later, BMS announced it would acquire Celgene for $74 billion. However, the latter transaction faced fierce opposition from BMS shareholders, and whether it will proceed as scheduled remains subject to subsequent voting.

Behind a series of large-scale transactions lies the lack of innovation in buyers’ R&D pipelines; they seek to fill this gap more rapidly through capital-driven strategies. Taking the current top ten best-selling drugs as an example, blockbusters such as Humira, Revlimid, and Rituxan are facing patent expirations. To maintain their industry standing, major pharmaceutical companies must identify successor products before these patents expire. If such candidates are absent from their internal pipelines, acquisition naturally becomes the preferred approach.

On the other hand, large pharmaceutical companies face intense competition, which is reflected to some extent in product R&D, but more specifically in the scope of product indications and product sales. Therefore, starting from scratch would increase the time, cost, and risk associated with product development, which is not what these companies desire. As a result, acquiring product pipelines from startups and collaborating with laboratories on R&D have naturally become their preferred strategies.

As early-stage R&D has become concentrated in laboratories and startups, innovative research and development have begun to be marginalized. An article in Nature Reviews Drug Discovery noted that the R&D expenditure of the top ten pharmaceutical companies decreased by approximately 5 percentage points between 2000 and 2017. As both venture capital firms and large pharmaceutical companies rely on startups to generate returns, their valuations have naturally risen accordingly.

Summary:

Does a high valuation necessarily imply a bubble? Certainly not. Beyond bubbles, sky-high transaction prices may reflect a combination of factors such as innovation capability, market competition, and industry trends. In any case, high valuations invariably serve to encourage entrepreneurs and signal the opportunities awaiting them. For venture capital firms, a vibrant entrepreneurial ecosystem offers more investment options, while also demanding greater professional acumen in selection and decision-making.