China's Third-Party Medical Sterilization Services Market: A $10.7 Billion Opportunity Attracting Five Types of Enterprises

Preface

The growth phase of an industry represents a window of opportunity for enterprises; those who can seize the initiative will emerge as industry leaders. The policy landscape for China’s third-party sterile supply center industry has evolved through three stages: initial exploration, standard establishment, and robust support. In August 2017, the Notice on Deepening the “Delegation, Regulation, and Service” Reform to Stimulate Investment Vitality in the Medical Sector (Guo Wei Fa Zhi Fa [2017] No. 43) granted third-party sterile supply centers the status of medical institutions. In May 2018, the promulgation of the Basic Standards for Medical Sterile Supply Centers (Trial) and the Management Specifications for Medical Sterile Supply Centers (Trial) set forth detailed requirements for the construction, management, and operation of third-party sterile supply centers, promoting more standardized and scientific industry development. Driven by the combined forces of policy support, market demand, and technological advancement, the industry has entered a period of significant growth opportunities.

What opportunities do third-party sterile supply centers face? What is the market size? Which enterprises are participating? How do they differ from hospital-established facilities? What are the strategic pathways, and what are the future development trends of the industry? These are undoubtedly the questions of greatest concern to entrepreneurs, startup founders, and investors.

VCBeat Research conducts an in-depth analysis of the third-party sterile supply center industry by compiling literature, conducting market research, and interviewing enterprises. The report examines the macro-environment, market demand, market supply, and case studies of representative companies. From the perspective of an independent observer, it aims to clarify key issues and provide strategic references for entrepreneurs and investment insights for investors.

Through this report, you will gain insights into third-party sterile supply centers:

1. Policy Evolution Trajectory from 2009 to 2018

2. Construction Standards and Management and Operational Requirements

3. Market Landscape and Competitive Players

4. Comprehensive Comparison of Typical Business Models

5. How International Giants Such as STERIS Build Third-Party Sterile Supply Centers

Third-Party Central Sterile Supply Departments (CSSDs) primarily provide outsourced sterilization services to hospitals that have not established their own CSSDs, as well as to those facing needs for new construction, renovation, or expansion of their existing facilities. These services encompass the cleaning and disinfection, inspection and assembly, sterilization, logistics and distribution, and leasing of various reusable medical devices and instruments, surgical instruments, sterile surgical gowns, and single-use surgical items. Furthermore, they implement quality control throughout the processing workflow, issue monitoring reports on the sterilization and disinfection processes, and ensure full traceability of the entire handling process for sterile items, thereby guaranteeing the quality of disinfection and sterilization.

China’s third-party sterile supply services started relatively late and are still in a growth phase. The government has issued relevant policies explicitly supporting the development of the third-party sterile supply services market, thereby creating a favorable macro-policy environment for enterprises. Coupled with the rising demand for outsourced hospital sterilization services, the market is now presented with significant opportunities for growth.

Third-Party Sterile Supply Centers Enter a Period of Growth Opportunity

The construction and operation of third-party sterile supply centers are primarily governed by the "Central Sterile Supply Department (CSSD) in Hospitals—Parts 1-3" (hereinafter referred to as WS310.1/2/3-2016), issued by the National Health and Family Planning Commission in 2016. On June 11, 2018, the National Health Commission released the "Notice on Issuing the Basic Standards and Management Specifications for Three Types of Medical Institutions, Including Medical Sterile Supply Centers, for Trial Implementation." Third-party sterile supply centers are required to comply with the relevant requirements of this Notice by adjusting their infrastructure, sterilization equipment, staffing, and other aspects in accordance with the "Basic Standards for Medical Sterile Supply Centers (Trial)" and the "Management Specifications for Medical Sterile Supply Centers (Trial)," and to obtain the "Medical Institution Practice License" before June 1, 2019. The issuance of this Notice signifies that third-party sterile supply centers will completely bid farewell to the era of irregular practices and enter a track of standardized operations.

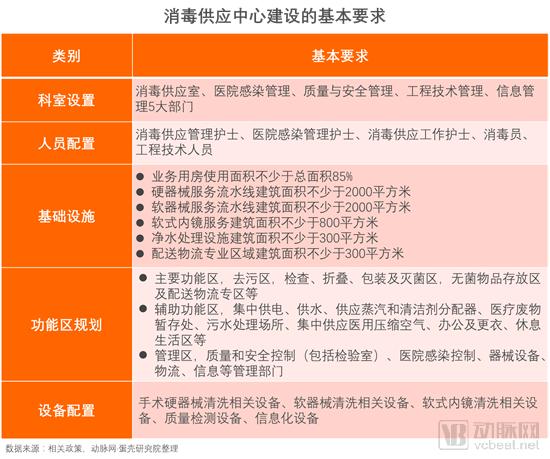

The two trial documents, namely the Basic Standards for Medical Sterile Supply Centers and the Management Specifications for Medical Sterile Supply Centers, have introduced new requirements for the construction and operation of third-party sterile supply centers, providing detailed regulations on departmental setup, staffing, infrastructure, functional zone planning, and equipment configuration.

In terms of departmental structure, the five essential departments are the Sterile Supply Department, Hospital Infection Control, Quality and Safety Management, Engineering Technology Management, and Information Management. This imposes rectification requirements on sterile supply centers that previously suffered from chaotic departmental naming and incomplete organizational structures, thereby providing comprehensive departmental support to ensure the functional operation of the sterile supply center.

In terms of staffing, requirements are primarily imposed on nurses, sterilization technicians, and technical personnel. Individuals in these roles must possess the corresponding vocational skills and obtain the relevant practice certificates before assuming their duties. This strengthens control from a talent perspective, enhancing the quality of disinfection and sterilization by improving staff professionalism.

In terms of infrastructure, the floor area for operational sites such as sterilization and disinfection assembly lines, water purification treatment lines, and distribution logistics lines is specified to ensure that related business activities can be conducted normally.

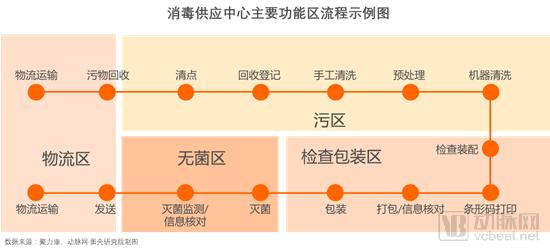

In terms of functional zone planning, the layout comprises three major sections: the main functional area, the auxiliary functional area, and the management area. Among these, the main functional area serves as the core component of the Sterile Supply Department (SSD). It encompasses operational processes such as decontamination, inspection, folding, packaging, sterilization, storage, and distribution of disinfected items. The scientific rigor and comprehensiveness of its planning directly impact the capacity and efficiency of sterile supply services, making it a critical factor for the enterprise’s survival and development.

In terms of equipment configuration, it should include equipment for cleaning surgical rigid instruments, equipment for cleaning flexible instruments, equipment for cleaning flexible endoscopes, quality testing equipment, and information technology equipment. Only a complete supporting equipment system can ensure the high-efficiency operation of the Central Sterile Supply Department (CSSD).

Currently, sterilization and disinfection technologies mainly include two categories: irradiation sterilization and ethylene oxide (EO) sterilization. Among these, irradiation sterilization primarily comprises three types: gamma rays, X-rays, and electron beams. The differences among them lie in the radiation source and penetration capability, with X-rays exhibiting the strongest penetration ability.

In terms of sterilization methods, irradiation sterilization is a destructive process. Materials that cannot withstand irradiation require the addition of more additives to the plastic to resist the effects of radiation, which can lead to the degradation and leaching of small molecules, thereby compromising material quality. Furthermore, since most medical devices are made of metal, they are not easily penetrated by radiation, which affects the sterilization efficacy within the device lumens. In contrast, ethylene oxide (EO) sterilization is a gaseous method that involves vacuuming followed by the injection of ethylene oxide, allowing it to penetrate into the internal cavities of devices for effective sterilization.

Regarding sterilization residues, irradiation sterilization disinfects and sterilizes medical devices using radiation based on the principles of nuclear radiation. Residual substances may originate from radiation-induced degradation or denaturation of the materials themselves, as well as from residual radiation; moreover, these residues may be toxic. In contrast, ethylene oxide sterilization employs gas for sterilization, and residual levels can be minimized by strictly controlling the ethylene oxide dosage.

VCBeat·VBInsight has reviewed policy documents related to Central Sterile Supply Departments (CSSD) over the past six years, and we have found that they can be broadly categorized into three phases: the exploratory trial phase, the standardization phase, and the strong support phase.

In September 2013, the State Council issued the “Several Opinions on Promoting the Development of the Health Service Industry” (Guo Fa [2013] No. 40), which explicitly encouraged the development of third-party health and medical services.

In June 2015, the “Notice on Several Policy Measures to Promote and Accelerate the Development of Socially Run Medical Institutions” (Guo Ban Fa [2015] No. 45) encouraged cooperation between public and private medical institutions, enabling the sharing of resources in sterilization supply centers within medical institutions, under the premise of ensuring medical safety and fulfilling core healthcare functions.

In September 2015, the State Council executive meeting placed special emphasis on the need to integrate regional medical resources for sterile supply services.

In December 2016, the "Standards for Hospital Sterile Supply Centers (2016)" were released, covering three parts: management specifications, technical operation specifications, and effectiveness monitoring standards. The standards added requirements for information system construction, included regional third-party sterile supply centers for the first time, and explicitly allowed public medical institutions to adopt outsourced sterile supply services.

In August 2017, the “Notice on Deepening the Reform to Streamline Administration, Delegate Power, Improve Regulation, and Upgrade Services to Stimulate Investment Vitality in the Medical Field” (Guo Wei Fa Zhi Fa [2017] No. 43) added five new categories of independently established medical institutions: rehabilitation medical centers, nursing centers, sterile supply centers, small and medium-sized ophthalmic hospitals, and health examination centers. This marked the point at which disinfection service enterprises officially acquired the status of medical institutions.

In May 2018, the Basic Standards for Medical Sterile Supply Centers (Trial) and the Management Specifications for Medical Sterile Supply Centers (Trial) were released, providing detailed regulations on departmental setup, staffing, infrastructure, functional zone planning, and equipment configuration. This marks a move toward greater standardization of third-party sterile supply centers.

In January 2019, the General Office of the State Council issued the "Opinions on Strengthening Performance Appraisal of Tertiary Public Hospitals," making medical safety a key component of the assessment indicators. As medical safety is inextricably linked to device safety, sterilization requirements for medical devices will be enforced more strictly, creating opportunities for the development of third-party sterile supply centers.

The Central Sterile Supply Department (CSSD) industry has moved beyond its nascent stage and is currently in a growth phase, marking a golden period for industrial development.

In the initial phase, sterile supply centers in China were primarily funded by government appropriations and led by regional benchmark hospitals, mainly providing sterilization services to their own institutions and affiliated hospitals. For instance, the Sterile Supply Center established in Futian District, Shenzhen, in 2002 provided services to surrounding medical institutions. The Sterile Supply Center founded by West China Hospital in 2003 served 13 small and medium-sized hospitals, and in 2008, Shenzhen Luohu People’s Hospital implemented integrated management for the sterile supply departments of more than 40 hospitals. During this initial phase, all sterile supply centers were publicly owned and managed through administrative approaches, lacking innovation.

During the development phase, encouraged and supported by policies, private capital and foreign investment began to enter the medical sterilization industry. In 2009, Sinopharm Group, an international giant in sterilization, officially launched operations of China’s first socialized medical instrument sterilization facility. One year later, Julikang, a leading enterprise in the sterilization industry, established its Shanghai Sterile Supply Center, which became the company’s first third-party sterile supply center to operate nationwide. In 2015, the sterilization center invested and built by Laoken Medical Sterilization Co., Ltd. in Chengdu officially commenced operations. In July 2016, Deyang City actively introduced private capital, with a planned investment of RMB 176 million, to construct the city’s largest and only regional sterile supply center. Meanwhile, public sterile supply centers continued to develop; in 2009, the Liyang Sterile Supply Center in Jiangsu Province was officially put into use. In 2015, Shandong Province’s first regional sterile supply center, the “Luji Sterile Supply and Assurance Center,” was established. During this period, although private and foreign entities entered the medical sterile supply industry, public institutions still dominated in terms of market share. We believe that as healthcare reform deepens, outsourcing hospital sterilization services is an inevitable trend, the private sterilization service market holds immense growth potential, and third-party sterile supply centers represent a blue ocean opportunity.

In the future, the sterile supply industry will enter a mature stage, with private sterile supply service providers capturing a larger market share than public sterile supply centers. Third-party sterile supply service enterprises, represented by Julikang and Laoken Medical, will establish nationwide service networks. At that time, the market landscape will be characterized by private-sector leadership and diversified development.

Market Demand Analysis for Third-Party Sterile Supply Centers

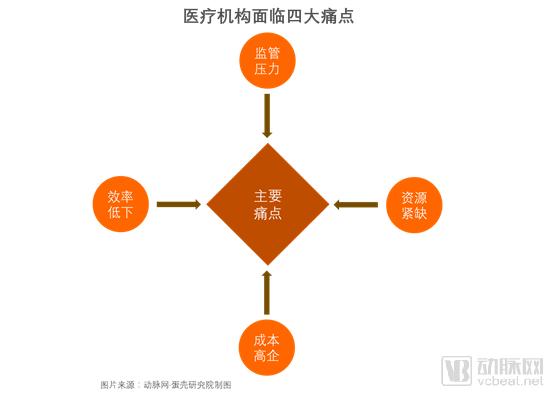

As the number of inpatients and surgical procedures in hospitals increases, the sterilization load on existing Central Sterile Supply Departments (CSSD) has been rising steadily, failing to meet sterilization demands. Many hospitals need to build new or expand existing CSSDs, further exacerbating the scarcity of land resources. Through surveys of relevant hospitals, we have identified four major pain points in hospital sterilization.

(1) Stringent Regulatory Pressure

In recent years, the number of healthcare-associated infection (HAI) incidents has been on the rise. Health authorities have mandated that hospitals strengthen infection prevention and control (IPC) management to reduce infection rates. Furthermore, the quality of sterilization services and infection control has become a key component of hospital accreditation criteria, with many regions even implementing a “one-vote veto” system; thus, hospitals must excel in sterilization processes to achieve higher accreditation ratings. In particular, the release of the new Basic Standards and Management Specifications for Medical Sterile Supply Centers has imposed stricter requirements on the construction and operational management of these centers. These developments have increased managerial pressure on hospital administrators, who seek to leverage third-party sterile processing centers to enhance sterilization efficiency, ensure the safety of medical instrument use, and thereby reduce the incidence of healthcare-associated infections.

(2) Scarce Land and Talent Resources

According to relevant standards, the construction area of a medical sterile supply center must be at least 5,000 square meters. The construction of infrastructure such as outpatient departments, inpatient buildings, laboratory buildings, rehabilitation centers, and pharmacies has already occupied most of the hospital’s available land, resulting in land scarcity. Building new or expanding existing medical sterile supply centers would require substantial land use, which would undoubtedly further exacerbate the shortage of hospital land. Additionally, medical sterile supply centers need to be staffed with nurses, sterilization technicians, engineering technicians, and IT personnel. However, hospitals have limited authorized headcounts, and hiring external staff poses certain risks. Therefore, hospitals face significant challenges in staffing their medical sterile supply centers.

(3) High Operating Costs

Medical Sterile Supply Centers require cleaning equipment, decontamination equipment, sterilization equipment, quality control equipment, packaging equipment, and logistics equipment. Most of these devices are from foreign brands and are expensive. Moreover, the daily operation of the center requires investment in labor, energy, and medical materials, which also demands significant financial input. As a result, hospitals face high operational costs.

(4) Poor management efficiency

The hospital’s Central Sterile Supply Department (CSSD) is publicly owned and operates under an administrative management system. In daily operations, it faces considerable interference from various government agencies, which hinders effective management, results in low operational efficiency, and fails to adequately meet the growing demand for disinfection and sterilization services.

With the increasing volume of surgeries and examinations in hospitals, the usage of medical devices is also on the rise. Medical disinfection supplies mainly come from two major sources:

(1) Operating Room Instruments: Various endoscopic instruments and optical scopes, precision surgical instruments, orthopedic surgical tools, electrosurgical units and electrodes, as well as anesthesia-related tools and instruments used in hospital operating rooms.

(2) Endoscopes and Dental Diagnostic and Treatment Instruments: With the widespread use of precision instruments such as endoscopes and dental diagnostic and treatment instruments, along with the continuous rise in the number of patients receiving diagnosis and treatment, the utilization volume of endoscopes and dental diagnostic and treatment instruments has also increased.

In addition to the two main categories of items mentioned above, disinfection and sterilization also cover routine items such as clothing, bed sheets, blood pressure cuff sphygmomanometer cuffs, stethoscopes, tourniquets, axillary thermometers, sputum cups (or basins), bedpans, and bed rails.

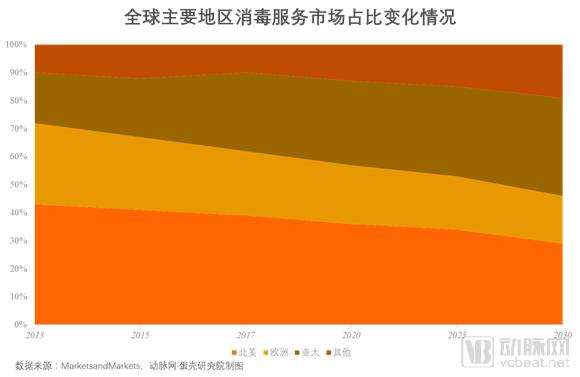

According to data released by the renowned global market research and consulting firm MarketsandMarkets, the global disinfection services market is primarily distributed across three major regions: North America, Europe, and Asia-Pacific. Currently, North America accounts for over 40% of the market share. However, with the development of healthcare systems and the increase in patient visits in major Asia-Pacific countries, the region’s market share is projected to surpass that of North America, making it the largest global market for disinfection services. Among these, China is poised to become the country with the greatest growth potential.

In 2017, the market shares in North America, Europe, and the Asia-Pacific region were 41.3%, 22.4%, and 28.1%, respectively. However, given the Asia-Pacific region’s large population base and advancements in healthcare systems led by countries such as China, the volume of surgical procedures and diagnostic examinations in hospitals is projected to surpass that of North America. By around 2030, the Asia-Pacific region’s market share is expected to reach 35.2%, exceeding North America’s 29.6%.

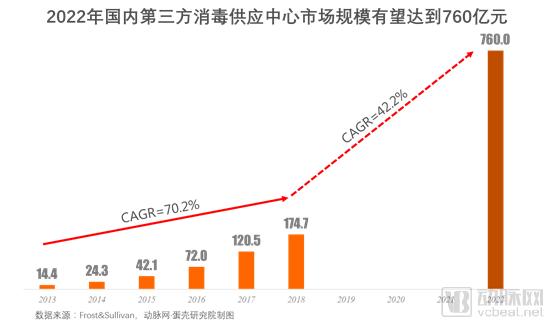

In terms of domestic demand for disinfection and sterilization services, data published by the global growth consulting firm Frost & Sullivan shows that the market size of third-party sterile supply centers in China achieved a compound annual growth rate (CAGR) of 70.2% over the past six years, increasing from RMB 1.44 billion in 2013 to RMB 17.47 billion in 2018. This is primarily because third-party sterile supply centers in China started relatively late with a low base, and the gradual liberalization of policies has promoted the development of third-party medical disinfection enterprises, thereby achieving a high CAGR. Frost & Sullivan predicts that the market size of third-party sterile supply centers will continue to grow rapidly in the coming years, expected to reach RMB 76 billion by 2020, and will undertake more than 70% of the disinfection and supply work for medical devices.

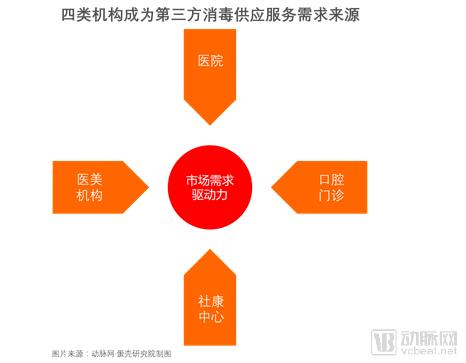

The demand for third-party sterile supply services originates from four types of healthcare institutions: hospitals, dental clinics, medical aesthetic institutions, and community health centers.

Hospitals: As of the end of 2017, there were a total of 31,056 hospitals in China. In major departments such as operating rooms, dental clinics, ophthalmology departments, gynecology departments, treatment rooms, intensive care units (ICUs), interventional radiology suites, and endoscopy centers, a large number of surgical instruments, examination instruments, and therapeutic devices are used. Most of these instruments are reusable and require strict disinfection and sterilization after each use.

Dental Outpatient Clinics: In 2017, there were 89,000 dental outpatient clinics in China. As the oral cavity is the most susceptible entry point for bacterial infiltration, sterilization of dental instruments must be prioritized. Instruments requiring sterilization in dental departments include endodontic instruments, dental handpieces, and extraction instruments, among others.

Medical Aesthetic Institutions: In 2017, the number of medical aesthetic institutions in China exceeded 9,000, with an average annual growth rate of over 20%. These institutions primarily utilize instruments for plastic surgery, including microsurgical instruments, needle holders, retractors, suction devices, emulsifiers, cannula brushes, and more.

Community Health Centers: According to data released by the National Health Commission, the number of community health centers in China reached 35,000 in 2018, basically covering major residential areas, and disinfection services at these centers have become one of the sources of demand.

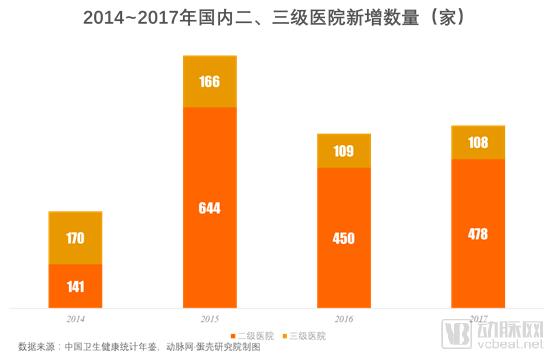

Ninety-five percent of the demand for third-party sterile supply services stems from hospitals outsourcing their sterilization processes. As previously mentioned, hospitals establishing in-house sterile supply departments face four major pain points: regulatory pressure, resource scarcity, high costs, and low efficiency. According to publicly available market data, the fixed asset investment for a sterile supply department at a tertiary hospital is approximately RMB 20 million, while that at a secondary hospital is around RMB 12 million. Based on the number of newly added hospitals in China in 2017, the fixed asset investment for newly built sterile supply departments in secondary and tertiary hospitals across the country reached RMB 7.9 billion. This figure does not include the fixed asset investments required for the renovation or expansion of existing hospitals’ sterile supply departments.

Operating room instruments from hospitals constitute the primary source of items for sterilization at third-party sterile supply centers. According to public data, the top 20 hospitals in 2017 performed an average of 104,000 surgeries annually, with hospital surgical volumes showing a continuous upward trend.

Therefore, whether viewed from the perspective of global market share distribution or the growth rate of domestic demand, third-party sterile supply centers (CSSDs) demonstrate significant market potential, with hospitals emerging as the most critical customer base. Moreover, third-party CSSDs currently account for less than 1% of the total medical sterile supply services market. Given this substantial blue-ocean opportunity, which types of enterprises are vying for a share? What are their business models, and what are the respective advantages and disadvantages of each? We will conduct a further analysis on these questions.

An Analysis of Business Opportunities in Third-Party Central Sterile Supply Departments

From the perspective of the policy evolution of third-party sterile supply centers, the sector has now entered a phase of strong government support. Hospital administrators, facing stringent regulatory constraints, can leverage third-party resources to enhance the quality and safety of hospital sterilization processes. Moreover, establishing independent sterile supply centers does not require hospitals to allocate their own land resources; instead, enterprises acquire land, construct facilities, and manage operations, thereby alleviating hospitals’ challenges related to land scarcity and staff shortages. Additionally, all infrastructure, sterilization equipment, and consumables are invested in by the enterprise, allowing hospitals to significantly reduce substantial cost expenditures through outsourcing sterilization services. Enterprises adopt specialized and standardized management mechanisms that are more efficient than those typically employed by hospitals.

(1) Analysis of the Medical Sterile Supply Service Industry Chain

From the perspective of industrial chain distribution, the upstream sector primarily consists of manufacturers of sterilization equipment and consumables. These include foreign companies such as STERIS and NOXILIZER; state-owned enterprises represented by Sinopharm Medical Devices and Xinhua Medical; and private enterprises represented by Laoken Medical, Jianghan Medical, and Maier Technology. These companies mainly manufacture various types of sterilization equipment and consumables required for the sterilization process. As a key player within the Sinopharm Group specializing in the development of medical device businesses, Sinopharm Medical Devices generates annual revenue exceeding RMB 30 billion. Its sterilization equipment products, developed and manufactured in-house, are sold both domestically and internationally. Notably, its independently developed MATACHANA low-temperature steam formaldehyde sterilizer is specifically designed for sterilizing medical instruments and equipment made from heat-sensitive materials. It effectively addresses the sterilization needs of flexible endoscopes and minimally invasive surgical instruments, and can also be used for optical instruments, cables, probes, connectors, and various other accessories.

The midstream of the industry chain comprises third-party sterile supply companies, including global sterilization giant STERIS (which acquired Synergy Health, the world’s second-largest outsourced sterilization company, for $1.9 billion in October 2014), Sinopharm Jienuo, Julikang, Laoken Medical, Juyoulian, and Ruikang Pharmaceutical.

Downstream of the industry chain are disinfection service clients, including hospitals, pharmaceutical companies, and other institutions.

(2) Analysis of Sterile Supply Service Enterprise Entities

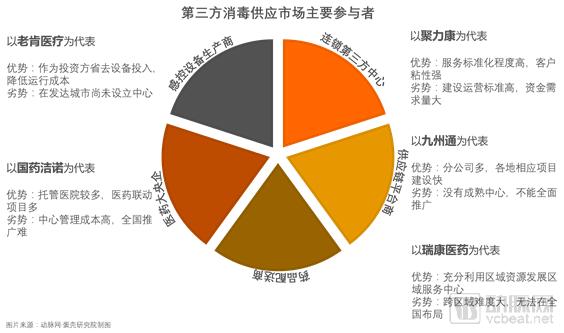

An analysis of enterprises in the midstream of the sterile supply chain reveals that the main participants currently competing in the market fall into five categories: infection control equipment manufacturers, chained third-party sterilization service centers, supply chain platform providers, pharmaceutical distributors, and large state-owned pharmaceutical enterprises.

Infection control equipment manufacturers, represented by Laoken Medical, initially focused on the research and development, production, and sales of hospital infection control equipment. Their main products include air disinfection products, instrument sterilization products, instrument cleaning products, accessories, and consumables. In May 2013, Laoken Technology jointly established Sichuan Sinopharm Laoken Xinheli Medical Sterilization Co., Ltd. with the UK’s Shinva Group and Sinopharm Group. Its Chengdu Sterilization Center officially commenced operations on August 1, 2015. Its advantage lies in being a manufacturer of sterilization equipment itself, allowing the sterilization center to avoid capital expenditure on equipment; however, it has not yet established regional centers in developed cities.

Chain third-party centers, represented by Julikang, were founded in 2010 and have established third-party sterile supply centers in seven major cities across China. Their primary clients are medical institutions at all levels, with over 200 clients served nationwide and a 100% annual contract renewal rate. Julikang adopts the latest international and domestic standards for management and operations, achieving high service standardization and strong customer retention. However, these high standards require significant investment and substantial funding to support business expansion.

Supply chain platform providers, represented by Jointown Pharmaceutical Group, are joint-stock enterprises whose core businesses include the wholesale, logistics and distribution, retail chain operations, and e-commerce of Western medicines, traditional Chinese medicines, and medical devices. Leveraging Jointown’s nationwide business network, sterile supply centers can be rapidly deployed across China; however, due to a lack of professional expertise in managing sterilization projects, mature centers have not yet been established.

Pharmaceutical distributors, represented by Realcan Pharmaceutical, have established nationwide procurement channels for drugs, vaccines, and medical devices. The company provides direct distribution services to over 4,000 manufacturers across healthcare institutions throughout China, while also engaging in pharmaceutical product placement. Currently, it is leveraging its advantageous resources within Shandong Province to offer sterilization and disinfection services; however, achieving a cross-regional footprint will require additional time.

Major state-owned pharmaceutical enterprises, represented by Sinopharm Jienuo, are affiliated with Sinopharm Group and possess inherent advantages in technology and capital. As Sinopharm Group manages a large number of hospitals, it can leverage medical-pharmaceutical synergy to carry out disinfection and sterilization services. However, the management structure of state-owned enterprises has also become a constraint on the company’s development, necessitating further improvements in management and operational efficiency.

Based on differences in business models, domestic sterile supply centers (SSCs) can be categorized into three types: hospital-owned SSCs, hospital-enterprise joint venture SSCs, and third-party SSCs. These models vary in terms of investment structure, leading party, hospital reputation, equipment sourcing, staffing strategies, service pricing, and other aspects. The following section provides an analysis of these three models.

(1) Hospital-built Central Sterile Supply Department

Hospital-built Sterile Supply Centers refer to sterile supply centers established by regional benchmark hospitals under the guidance of health and medical administrative authorities, providing sterilization services for themselves and their affiliated medical institutions. Benchmark hospitals can play a leading role throughout the entire process, from construction to management and operation. By signing contracts with surrounding hospitals, they can provide services to these contracted hospitals while meeting their own needs for the disinfection and sterilization of medical supplies. Examples include the Sterile Supply Center of West China Hospital, the Sterile Supply Center of Shenzhen Luohu District People’s Hospital, the Sterile Supply Center of Wujiang Shengze Hospital, and the Sterile Supply Center of Liyang People’s Hospital. Benchmark hospitals are typically regional Grade A tertiary general hospitals, which have sufficient technical, personnel, and financial resources to support the management and operation of sterile supply centers.

The Liyang Model in Jiangsu: In response to the call from local government authorities and under the guidance of relevant policy documents, Liyang People's Hospital in Jiangsu Province expanded its Sterile Supply Department (SSD) into a Regional Sterile Supply Center for Liyang City, providing sterilization services to surrounding medical institutions. The funding for this expansion primarily came from the hospital’s own funds and matching fiscal subsidies.

Hospital-built Sterile Supply Centers (SSCs) rely primarily on fiscal investment, with hospitals responsible for construction, operation, and equipment procurement. Service pricing is determined in accordance with local price control policies, and the hospital’s brand serves as the brand of the SSC. By leveraging owned land for construction, these centers require relatively less capital and have shorter project cycles. They serve the host hospital and nearby facilities, benefiting from short logistics distances; however, this also limits their service radius. Furthermore, administrative management approaches constrain operational efficiency, increase operating costs, and hinder scalable expansion.

(2) Sterile Supply Center Jointly Established by Hospital and Enterprise

A Sterile Supply Center Co-established by a Hospital and an Enterprise refers to a collaborative model in which the hospital provides the premises, while the enterprise is responsible for investment and daily operations. This model is typically adopted by large, benchmark-setting Grade III Class A hospitals in the region. Enterprises are willing to partner with such hospitals because, leveraging the hospital’s local influence, they can attract other hospitals as clients for the sterile supply center, strengthen their cooperative relationship with the hospital, and lay the foundation for expanding other business areas. Additionally, the enterprise does not incur land acquisition costs; it is only responsible for facility construction, equipment investment, and participation in management. For instance, Sinopharm Jienuo has attempted to co-establish sterile supply centers with partner hospitals to compete for market share.

Under this model, the hospital provides the site while the enterprise is responsible for investment. This arrangement allows the hospital to save on construction and equipment procurement costs, while the enterprise reduces land acquisition expenses. Daily management and operations of the center are determined through negotiation between the hospital and the enterprise. Service pricing is based on the hospital’s relevant standards, with the enterprise retaining a certain degree of autonomy in setting prices. As this is a collaborative project jointly developed by the hospital and the enterprise, capital requirements and project construction timelines are moderate. The facility serves the host hospital and nearby hospitals, resulting in short logistics distances but a limited service scope. The hospital also participates in daily operations, which subjects it to administrative pressures that may somewhat affect management efficiency.

(3) Third-Party Sterile Supply Center

Third-party sterile supply centers refer to facilities that are not reliant on hospital premises; instead, enterprises independently select and acquire land, assuming full responsibility for construction and operations, and provide services to healthcare institutions. This represents a fully market-driven approach, whereby companies choose locations rationally and plan scientifically in alignment with market demand and their own development strategies to establish regional sterile supply centers. Such enterprises bear all investment costs, procure their own equipment, and have the autonomy to set pricing for sterilization services, with their brand influence determining their market competitiveness. Typical representatives of this model include Julikang, Laoken Medical, and New Heli.

Although this model involves numerous administrative approvals, cumbersome procedures, and high investment costs from project planning to implementation, it avoids administrative interference, improves management efficiency, reduces daily operational costs, facilitates scalable expansion, and extends the service radius. Interviews reveal that the current sterilization cost per instrument is RMB 4.5–5.5 for tertiary hospitals and approximately RMB 6.5–7.5 for secondary hospitals. Higher-tier hospitals benefit from relatively saturated capacity and better utilization of equipment and facility resources, resulting in lower fixed asset depreciation and amortization allocated per instrument. In contrast, third-party sterile supply centers can reduce the sterilization cost per instrument to RMB 3–4, saving tertiary hospitals approximately RMB 7 million and secondary hospitals approximately RMB 3 million in annual operational costs. Therefore, an increasing number of hospitals are expected to outsource sterilization services in the future, making third-party sterile supply centers potentially the dominant model.

The above covers the first three chapters of this report. The full structure of the report is as follows:

I. Third-Party Sterile Supply Centers Enter a Period of Growth Opportunity

1.1 Standardization of Center Construction

1.2 Technological Innovation as a Catalyst

1.3 Policy Support for Industry Development

1.4 The Industry Is in Its Growth Phase

II. Market Demand Analysis for Third-Party Sterile Supply Centers

2.1 Four Major Pain Points Facing Hospitals

2.2 North America Dominates the Market, While Asia-Pacific Holds the Greatest Growth Potential

2.3 Market Demand for Third-Party Sterile Supply Services in China Becomes Prominent

2.4 Four Types of Institutions Drive Growth in Demand for Third-Party Sterile Supply Services

III. An Analysis of Business Opportunities for Third-Party Central Sterile Supply Departments

3.1 Third-Party Sterile Supply Centers Address Pain Points Faced by Hospitals

3.2 Various Entities Vie to Enter the Third-Party Sterilization Services Market

3.3 Analysis of the Business Model of the Sterile Supply Center

IV. Analysis of Typical Enterprises in Third-Party Central Sterile Supply Departments (CSSD)

4.1 STERIS – The World’s Largest Integrated Provider of Third-Party Medical Sterilization Solutions

4.2 Julikang – A Leading Third-Party Sterile Supply Service Provider in China

V. Analysis of Future Trends in Third-Party Sterile Supply Services

5.1 Outsourced Hospital Sterilization Services Will Gradually Replace In-House Sterilization Centers

5.2 Standardization, Chain Operation, and Branding Will Become Prominent Features of Third-Party Sterile Supply Centers

5.3 Supply Chain Integration May Become the Preferred Strategic Breakthrough for Enterprises

Scan the QR code below with a long press to receive the full version of the "Special Report on Third-Party Sterile Supply Centers" free of charge. Additionally, you can join the VCBeat membership platform, where, over the next year, you will enjoy unlimited access to comprehensive industry trend reports, timely updates on the latest global investment and financing activities, a comprehensive database of healthcare companies, and extensive resource-matching opportunities.

*Cover source: https://pixabay.com/