StartUp Health Q1 2019 Healthcare Startup Funding Report: Sharp Drop in Deal Count, Increasing Investment Diversity

Recently, StartUp Health, one of the most influential digital health startup accelerators globally, released its Q1 2019 Healthcare Startup Funding Report. As is well known, a key distinguishing feature of this report is that its data on transactions and investors has been tracked since 2010.

“Digital Health” is being redefined today, encompassing medical innovation, healthcare IT, biotechnology, medical technology, pharmaceuticals, healthcare services, and consumers. Among these, the importance of medical innovation is self-evident; beyond digital solutions, connectivity, and data, it includes new business models, design thinking, and other critical factors that help transform the current healthcare landscape.

We can address the current challenges facing the healthcare sector through such innovations as the “Health Moonshot”—which aims to effectively deliver high-quality care to billions of people, end cancer, and fundamentally reduce healthcare costs. Launched by StartUp Health in 2017, the initiative specifically focuses on improving care accessibility, lowering healthcare costs, curing diseases, ending cancer, and advancing women’s health, children’s health, brain health, mental health, nutrition and fitness, and longevity programs.

Awkwardly, although the pace of medical innovation has surpassed our expectations, many healthcare needs remain unmet. Currently, the healthcare sector is a vibrant market globally, suggesting that “true innovation” may yet be on the horizon.

Based on the financing and investment data from the first quarter of 2019, StartUp Health has drawn several key insights. VCBeat has compiled this report for our readers. The main contents are as follows:

New Characteristics Emerging in the Healthcare Sector

Reclassifying the Medical Innovation Market

Total Financing Volume Declines Slightly, with Investment Showing Diversified Characteristics

Investors Are Active in the Field of Medical Innovation

Emergence of New Medical Innovation Centers

I. New Characteristics in the Medical Field

1. Sharp Decline in Transaction Volume, Market Maturing

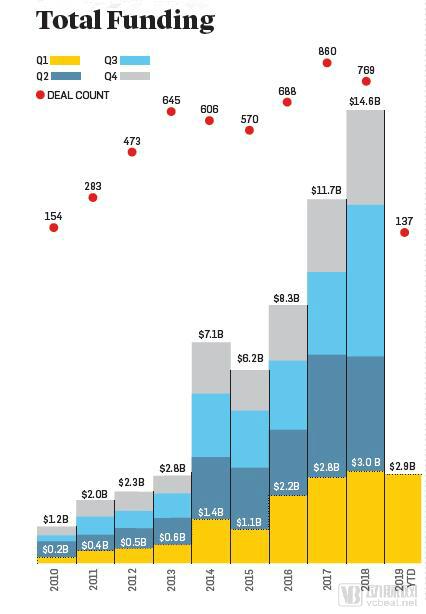

Total funding in the first quarter of 2019 reached $2.8 billion, a mere 3.7% decline year-on-year, while the number of deals dropped by 37%. This disparity was largely driven by several mega-deals, such as Clover Health’s $500 million financing round completed in January 2019. (For a case study on Clover Health, please refer to the report by VCBeat.)

Although the financing momentum at the start of 2019 slowed compared to previous years, signs indicate that the market continues to mature, with the median overall deal size climbing to $9.2 million, and deal volumes are likely to surpass those of the previous quarter. In fact, among the 11 “Health Moonshots” tracked by StartUp Health, more than 40% involved transactions exceeding $10 million.

2. New Opportunities for the Insurance Industry

U.S. health insurance company Devoted Health completed a $300 million Series B financing round in the fourth quarter of 2018, closely followed by Clover Health’s $500 million funding round, indicating strong investor interest in the health insurance sector. Healthcare innovation companies are also striving to identify optimal models for collaboration with the insurance industry, as this represents new opportunities.

3. Reducing healthcare costs and improving care accessibility are of paramount importance

Within the “Health Moonshot” initiative, the initiatives to reduce healthcare costs and improve care accessibility secured the most funding, at $1.1 billion and $983 million, respectively. This also indicates that investment institutions are currently more focused on these two areas.

4. Strong Growth in the “Women’s Health” Initiative

Women’s health initiatives saw robust growth starting in the first quarter of 2018, with eight deals raising a total of $91.6 million, compared to just $7.8 million during the same period in 2017. There were 20 deals in women’s health initiatives throughout 2018, and this upward trend is expected to continue in 2019.

5. The Emergence of New Global Innovation Hubs

Although global medical innovation participants from Lausanne, Switzerland, and Athens, Greece, appear diminutive in comparison to the San Francisco Bay Area, their involvement has introduced greater possibilities for medical innovation. Among the ten largest healthcare deals in the United States, five originated in the San Francisco Bay Area, with capital involvement exceeding the combined total of all other U.S. transactions.

II. Reclassifying the Medical Innovation Market

Since 2010, StartUp Health has analyzed more than 5,000 financing deals, revealing that the market’s total funding surged to $58.3 billion during this period, with new companies emerging worldwide each year.

As the scale of financing expands rapidly, market complexity increases accordingly. To adapt to the current complex market environment, StartUp Health has proposed a framework for classifying and tracking companies.

Generally, many enterprises and industry research institutions are simply categorized as “healthcare companies,” “artificial intelligence companies,” or “oncology platforms.” While this approach provides a reference framework for the audience, such frameworks are often limited and fail to deliver substantial value. To address this, StartUp Health has developed a new classification system based on market segmentation.

Startup Health Classification Criteria:

1. Create a more nuanced approach to analyzing market trends;

2. Provide new opportunities for entrepreneurs, investors, and key stakeholders;

3. Encourage investors, customers, and other stakeholders to articulate their industry perspectives in greater detail, with the aim of improving existing collaboration frameworks and establishing new partnerships with startups.

Six Key Attributes:

First, each company is broken down into six attributes to analyze capital flows from different dimensions. A company may have more than one “Health Moonshot” initiative, specialty, end user, technology, or application, but it has only one function. Therefore, as shown in the report, the same company can be evaluated across multiple dimensions:

1. “Health Moonshot”: Long-Term Global Impact, e.g., Improving Care Accessibility and Reducing Healthcare Costs.

2. Function: The company's primary activities or value drivers. For example: healthcare, research.

3. Specialty: The specific medical or disease subfields in which the company is involved, such as oncology and cardiology.

4. End users: Organizations or individuals that benefit from the company's value. For example: patients, suppliers.

5. Technology: The company’s value delivery mechanism. For example: machine learning, robotics.

6. Applications: Case studies of the company’s technology applications. For example: diagnosis, billing.

“Patient authorization” is typically the most valued by investors, but “insurance” took the lead this quarter. (Screenshot from the original report)

Compared with the first quarter of 2018, financing volume in the first quarter of 2019 increased by 93%, driven by Clover Health’s funding round. There were only two deals in the “Education + Content” sector, accounting for less than 1% of the total financing amount for the quarter. “Health” was the second-largest source of financing; HIMS, a men’s health e-commerce startup, announced in January that it had completed a $100 million funding round, representing 15% of the total financing in the first quarter of 2019.

III. Total Financing Amount Declines Slightly, with Investment Showing Diversified Characteristics

Transaction volume in the first quarter of 2019 decreased by 35% compared with the first quarter of 2018 and remained flat relative to the fourth quarter of 2018. However, total financing amount lagged behind that of the first quarter of 2018 by only 3.7%, leading to a 79% increase in the median transaction value. Many may consider transaction quality more important than quantity, as fewer but larger deals may indicate a more mature market.

It is worth noting, however, that this marks the first time on record that first-quarter financing has failed to exceed fourth-quarter levels of the previous year.

Clover Health accounted for 17% of the total financing in Q1 2019, marking the first time such a proportion has been seen since Outcome Health raised $600 million in Q2 2017. In Clover Health’s deal, investments in the insurance sector were particularly prominent, representing 23% of the total financing amount but only 4% of the number of transactions.

Despite a slight decline in total financing this quarter, transaction records indicate that capital investments have expanded into more sectors, exhibiting greater diversity.

Total Financing from Q1 2010 to Q1 2019 (Screenshot from the Original Report)

Top 10 Transactions in the United States (Screenshot from the Original Report)

Top 10 Non-U.S. Transactions (Screenshot from the Original Report)

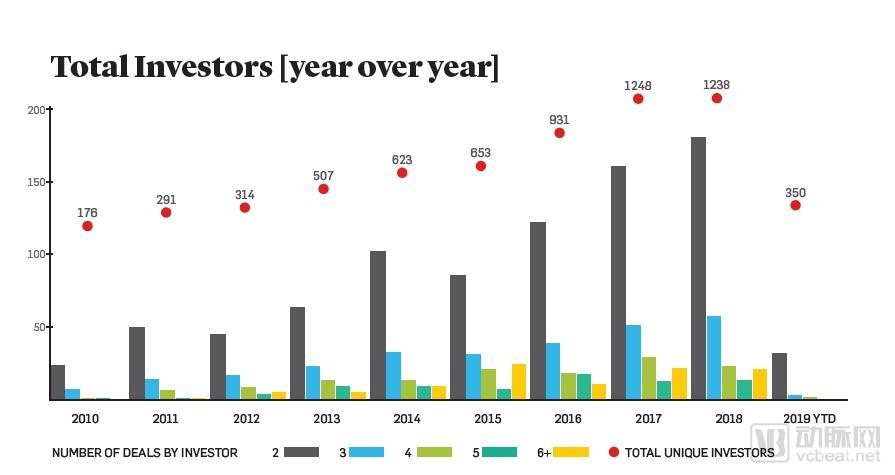

IV. Investors Are Active in the Field of Medical Innovation

Comparison of Total Number of Investors from Q1 2010 to Q1 2019 (Screenshot from the Original Report)

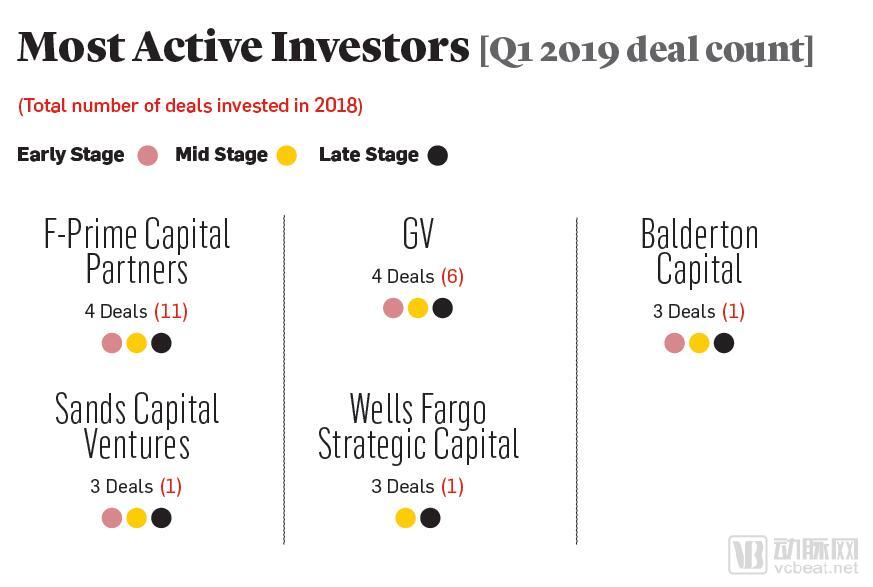

The Most Active Investors in Q1 2019 (Screenshot from the Original Report)

In the first quarter of 2019, a total of 350 independent investment firms conducted transactions, on par with the same period in 2018. During Q1 2019, GV and F-Prime Capital Partners topped the list of most active investors, each with four investments.

Investment firms such as Balderton Capital, Sands Capital Ventures, and Wells Fargo Strategic Capital, which had previously been minimally involved in the medical innovation market—with only one transaction in 2018—have already completed three deals in the first quarter of this year alone.

This year, 11% of investors invested in two or more companies. Among the 38 most active investment firms from 2018 to the present, 11 only entered the healthcare innovation sector in the first quarter of 2019.

V. Emergence of New Medical Innovation Centers

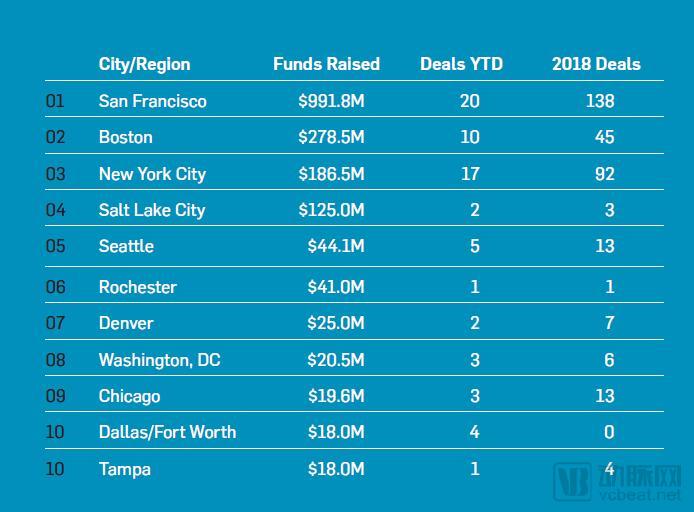

Financing Landscape of the Most Active U.S. Metropolitan Areas in Medical Innovation (Screenshot from the Original Report)

In the United States, San Francisco, New York, and Boston have consistently topped the list of cities with the highest funding volumes, and the first quarter of 2019 was no exception. Five of the largest financing deals in the U.S. during this quarter took place in the San Francisco Bay Area, exceeding the combined total of deal amounts in all other cities. Although New York saw a relatively low number of transactions in the first quarter of 2019, it trailed only four deals from coastal regions.

Seattle completed five deals in the first quarter of 2019, compared with only one deal in the same period last year, while the total transaction value increased from $1 million to $44 million. Dallas/Fort Worth made its debut on the list, completing four deals and raising a total of $18 million in the first quarter of 2019.

Although large deals are typically concentrated in coastal regions, transactions across the United States are beginning to diversify, with 29 metropolitan areas completing a significant volume of deals this quarter.

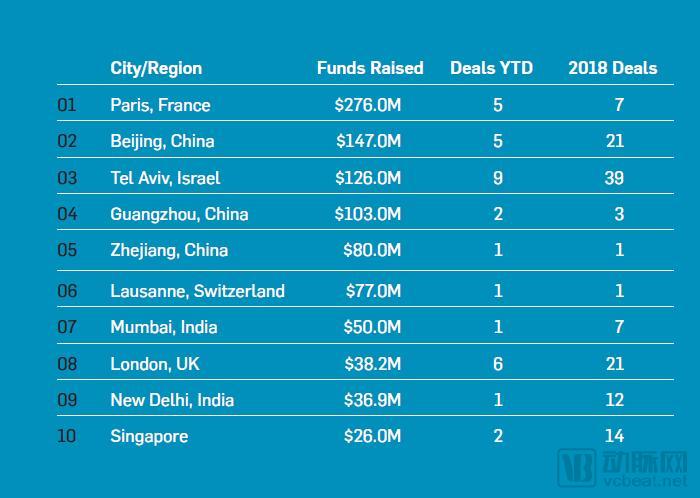

Funding Landscape in Medical Innovation for the Most Active International Metropolitan Areas (Excluding the U.S.) (Screenshot from the Original Report)

Medical innovation is a global movement, with 36% of funding originating from outside the United States. Turning our attention to non-U.S. metropolitan areas, we observe that the Paris region demonstrated particularly strong fundraising performance in the first quarter of 2019.

Although London and Beijing frequently top the global rankings for healthcare innovation in major metropolitan areas, Paris, known as the “City of Lights,” closed five deals led by Doctolib and Dental Monitoring in the first quarter of 2019, with total financing nearly double that of the Beijing region. Ranking second on the list, Beijing remains a powerful hub for healthcare innovation.

Notably, Sophia Genetics, based in Lausanne, Switzerland, raised $77 million. As a result, Lausanne has made its debut on the list of active international metropolitan areas for investment in medical innovation. The company is a major data analytics firm that leverages artificial intelligence (AI) to help healthcare professionals diagnose and treat patients through genomic analysis.

(Compiled by: Xu Shengnan)