Opportunities and Challenges in New Drug Investment: Insights from Li Yang of Puhua Capital

Editor’s Note: This article is reprinted from Qingtong Capital, with authorization granted to VCBeat for republication.

As a niche sector within the healthcare industry, innovative drugs are garnering increasing attention from investment firms. On April 10, Qingtong Capital invited Li Yang, Director at Puhua Capital, to share insights on the opportunities and challenges in investing in innovative drugs. The following are the key points from Li Yang’s presentation:

Current State of the Domestic New Drug Industry

Opportunities in New Drug Investment and Four Key Areas for Enhancement

Three Major Challenges in New Drug Investment

Four Key Comprehensive Competencies Required for Venture Creation & Investment

Observing the top ten pharmaceutical companies by market capitalization in China and the United States, we find that leading U.S. pharmaceutical firms largely leverage their core therapeutic strengths, achieving strong market performance through early-stage R&D, manufacturing, and sales; whereas leading Chinese pharmaceutical companies primarily generate profits via distribution and wholesaling models.

Overall, leading Chinese companies have primarily gained domestic market share through distributed products, while pharmaceutical R&D remains in its early to mid-stages. Under these circumstances, there is substantial room for growth for China’s biotech startups and R&D-driven enterprises. For dominant biopharmaceutical companies from Europe and the United States, China is an indispensable market. To compete with them and achieve overtaking on a bend, domestic new drug developers must possess strong comprehensive team capabilities and make thorough preparations in product selection.

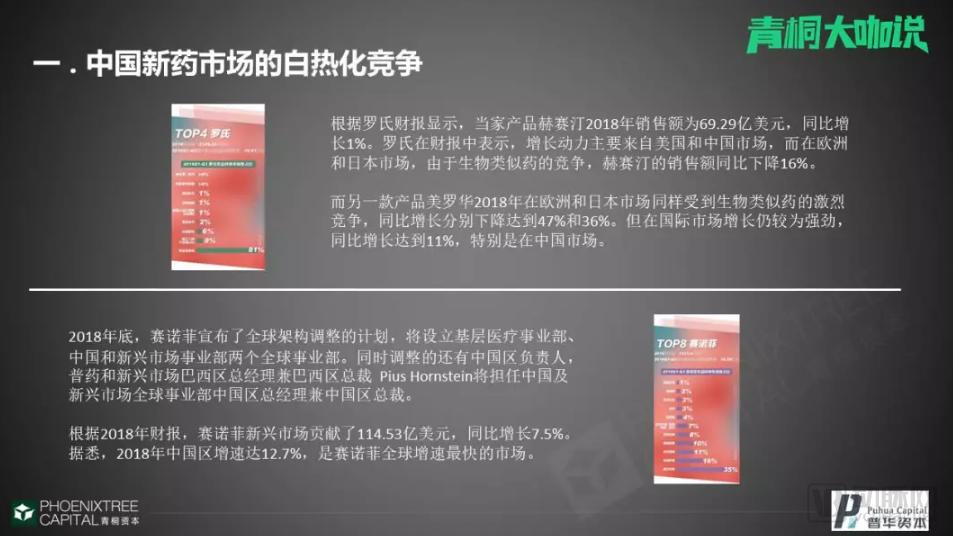

Taking Roche and Sanofi as examples, competition among foreign pharmaceutical companies in overseas markets has evolved to a stage of “mutual targeting.” Consequently, China is defined as an emerging market for certain pharmaceutical categories. Roche’s Herceptin generated $6.927 billion in sales in 2018; however, due to competition from similar drugs, its sales actually declined by 16% in the European and Japanese markets.

Why does this happen?

Biopharmaceutical R&D in Europe and the United States started earlier than in China, and biosimilars have developed more rapidly there, following a logic similar to that of generic drugs to achieve equivalent therapeutic effects. However, in other countries, particularly in China, market competition for biosimilars is not yet intense. With the international market growing at a rate of 11%, driven primarily by China, this has become a key reason why overseas pharmaceutical companies are focusing on the Chinese market.

Sanofi’s staffing strategy for its marketing team also reflects the importance it attaches to the Chinese market. China has a vast population, and many foreign pharmaceuticals have yet to penetrate this market, leaving significant gaps in coverage. New drug products are experiencing robust growth in China. Even amid extreme price pressures and volume-based procurement programs, the market still promises substantial incremental gains.

Therefore, amidst fierce competition, I believe Chinese innovative drug companies are facing a situation of extreme contrasts. Domestic brands see the blue ocean in the local market, but they also face competition from established players.

Therefore, within our investment framework, we categorize the overall market into two broad segments. The first is a pure blue-ocean market, where leading companies can readily achieve a monopolistic position. The second segment is one in which foreign enterprises have established a certain degree of market coverage—reflecting the current market environment. Although direct competition exists, Chinese companies benefit from policy-driven protections, such as big data regulations and preferential procurement for domestic brands. Furthermore, domestic firms hold an advantage in building trust and collaborative relationships with medical experts, and they are better positioned to develop pricing and sales strategies that are more aligned with local conditions.

Overall, the ecosystem and environment for innovative drug R&D in China are highly favorable. Even with a certain degree of market presence by multinational pharmaceutical companies, Chinese enterprises have emerged as rising stars in the market due to specific factors.

Source: 36Kr

Currently, there are numerous factors driving the strong interest of China’s domestic capital market in new drugs. This may be attributed to capital inflows from other industries into the field of new drug R&D, or to the widespread recognition of the surge in R&D talent within the biopharmaceutical sector. Between 2010 and 2018, the number of investment and financing transactions surged, with substantial amounts raised in early-stage funding rounds.

In our study of the new drug investment markets in Europe and the United States, we found that each funding round involves a relatively professional group of investors who form a fixed circle, collaborating to take over stakes from one another. This approach provides companies with a relatively stable valuation system and facilitates their public listings, while flexible channels distribute the R&D risks across various institutions and even individual investors.

China’s investment landscape is becoming increasingly specialized, albeit with some tendency toward herd behavior. As the Hong Kong stock market has absorbed a number of leading R&D-driven enterprises, China has also launched the STAR Market (Science and Technology Innovation Board). We provide support to R&D-intensive and strategically important emerging companies aligned with national priorities, even when they are operating at a loss. We ensure their market liquidity by carefully selecting investors and maintaining rigorous project quality standards. This is our vision, and I believe it is achievable as the industry continues to professionalize.

Another factor is policy. Policies related to generic drugs are squeezing the profit margins of intermediaries and generic drug manufacturers, thereby steering the market environment toward innovation and R&D. China’s unique policy landscape has provided strong impetus for domestic brands.

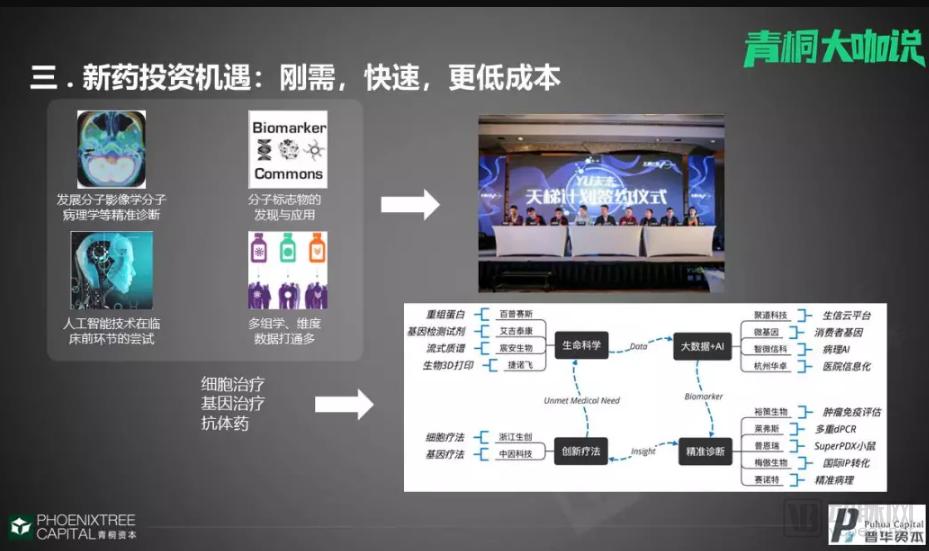

Throughout the new drug investment process, we have found that many emerging foundational technologies, novel research protocols, and innovative concepts can help increase the likelihood of rapid market entry for new drugs. There are four key areas that offer significant improvements:

1. Advancing Precision Diagnosis in Molecular Imaging and Molecular Pathology

Although we are currently witnessing numerous failures in the development of drugs for Alzheimer’s disease and other neurological disorders, significant breakthroughs have been achieved. For instance, in AstraZeneca’s project, amyloid plaque deposition can be visualized using PET/CT imaging, while drug metabolism can be monitored through various molecular diagnostic products. This represents a major advancement in the field.

2. Discovery and Application of Molecular Biomarkers

The discovery of molecular biomarkers is not new; it has long been part of basic scientific research. What matters more now is their application. In the future, a growing number of molecular biomarkers will help us refine every stage of patient care—from early disease screening and precise diagnosis to guiding treatment decisions, medication selection, and prognosis assessment.

3. Applications of Artificial Intelligence in Preclinical Stages

The integration of artificial intelligence and new drug development has long been a hot topic of discussion. Many projects in the industry are largely based on the various steps involved in the new drug development process; some focus on small-molecule drugs, while others may target the application of molecular biomarkers, conducting correlation analyses between phenotypic characteristics and molecular biomarkers.

In the early stages, these companies refined their algorithms using public databases or literature. In later stages, they engaged in more extensive trials and collaborations with enterprises. Such companies are currently at a relatively early stage of development, and few have achieved substantial sales volumes or reached profitability.

However, we are quite confident in this area. We hope to see more innovative methods emerge in the future that can enhance the entire new drug development process. I consider it a relatively intelligent attempt.

4. Integration of Multi-Omics and Multi-Dimensional Data

In March 2017, Yuce Bio, a portfolio company specializing in tumor neoantigen-based diagnostics and therapeutics, joined forces with Academician Zhan Qimin to launch the “Ladder Project.” The Ladder Project provides auxiliary treatment decision support for scientists and clinicians in oncology, offers reliable target selection for pharmaceutical drug development, and builds a collaborative, mutually beneficial, and win-winning “ladder” against cancer. It aims to accelerate the clinical translation of the latest tumor immunotherapies and help achieve China’s ambitious goals in cancer combat. The Ladder Project has gathered numerous industry professionals focused on tumor immunology, including entrepreneurs, physicians, and research scholars. We also hope that more partners within the industry will join the Ladder Project.

We have also observed this trend, which is why Puhua integrates diverse foundational technologies and teams in its new drug R&D efforts. Some focus on upstream recombinant protein production, others on front-end sales, biological validation, genomic big data, or end-user data collection. Ultimately, we have invested in several companies related to new drug development to foster collaboration with them. We believe this constitutes a cyclical ecosystem.

In addition to recognizing the industry-wide opportunities in new drug development, we also see numerous challenges within this sector.

1. Directional Clustering: Beware of Bubbles

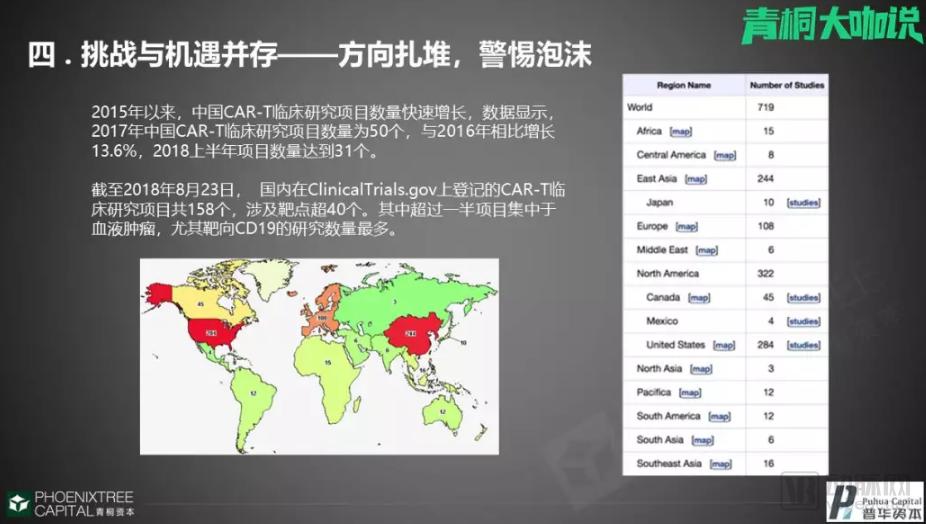

The first challenge is the formation of a bubble, which essentially refers to clustered R&D efforts. From an investment perspective, institutions are highly eager to invest in leading companies within major therapeutic categories (such as oncology and cardiovascular diseases), particularly in sectors with a robust pipeline and high mortality rates where there is an urgent need for new drugs.

We have observed that when a particular industry shows significant promise, companies tend to cluster within it. Taking the CAR-T sector as an example, the number of clinical trials in China’s CAR-T field has actually surged. On the global landscape, the red areas indicate the number of companies conducting CAR-T clinical trials. Apart from the United States, China is the other major player, with efforts primarily concentrated on the CD19 target.

In addition to the concentration of CAR-T therapies for hematologic malignancies, a large number of companies are simultaneously filing applications for related antibody drugs or CAR-NK cell therapies.

2. Complex Business Model Covering the Entire Process

New drug development is a highly complex, end-to-end business model. We have observed numerous overseas cases in which the new drug development process is broken down with great clarity and exhibits a high degree of standardization.

For instance, preclinical CROs and regulatory affairs consulting firms each fulfill their specialized roles. Consequently, it is quite common abroad for asset-light novel drug development companies to emerge, or for institutions to directly commercialize research outputs and rapidly bring them to market.

However, in China, the requirements for entrepreneurial qualities are more comprehensive. Entrepreneurs must navigate a more complex model when introducing a company or product to the market.

Let’s take CAR-T therapy as an example. Overseas, several companies, such as Oxford BioMedica, possess core technologies for viral vector manufacturing. However, in China, we have yet to see many startups capable of achieving high-quality viral vector production or highly scalable manufacturing processes. These companies must simultaneously achieve production scale while ensuring product stability and usability. Therefore, even with a concentration of downstream enterprises, upstream service providers may still face supply shortages.

3. Stringent Regulation and Strong Policy Orientation

Policies in China are continuously being refined and standardized. However, this environment is not necessarily favorable for early adopters of many medical products. In addition to technical expertise, manufacturing processes, and quality control capabilities, these teams must also possess strong operational and public relations skills, such as maintaining government relations and building connections with hospital experts. Since China’s healthcare system remains predominantly public, our fundamental goal is to help ensure that everyone receives timely and improved treatment.

Therefore, on this basis, pharmaceutical companies must be able to meet the increasing demands of the pharmaceutical and healthcare sectors and ensure mutual compatibility. As much of the underlying infrastructure in China is still under development, enterprises face numerous challenges: some must build their own production lines, others need to seek global partners, and still others must source raw materials from overseas markets.

As an investment institution, we tend to favor companies with more comprehensive or well-rounded teams. At the same time, we recognize that there are still numerous avenues available for exploration, both from a policy and regulatory perspective. We can adopt a more segmented approach to identify specific drug candidates suitable for regulatory approval as orphan drugs.

Investment institutions can only generate profits in relatively emerging markets, which actually places very high demands on their professional capabilities as well as their ability to identify, screen, and evaluate early-stage projects.

In this environment, investment will become increasingly differentiated, with capital no longer so heavily concentrated in top-tier players. Driven by policy and shaped by capital dynamics, leading enterprises may gradually emerge into prominence, while investors will identify suitable targets among other companies by approaching them from diverse angles.

Whether in investment or entrepreneurship, we believe that a team must have a strong understanding of four fundamental elements to secure better investment opportunities in new drug development.

1. Strategic Landscape. This refers to what we commonly describe as “who are our friends and who are our rivals,” or, in terms of current practical realities, the China-U.S. trade war, the Belt and Road Initiative (BRI), and other such developments, along with the dividends or challenges they bring.

2. Cycle Alignment. The development cycle of an enterprise must be aligned with the lifecycle of financial instruments. It is essential to balance the company’s overall R&D progress and regulatory review pace with financing valuations in both the primary and secondary markets, thereby securing more robust support in subsequent stages. Furthermore, enterprises should strategically leverage currently available professional and standardized financing channels.

3. Policies. Policies are region-specific rules of the game formulated based on existing industry characteristics. Leverage favorable policies to enhance practical operational capabilities.

4. The Foundation Layer. We interpret this as technology, encompassing medical robots resulting from the integration of medicine and engineering, navigation technologies, as well as gene editing and cell therapy in the field of new drug development. Many entrepreneurs, even those within large conglomerates, continuously monitor technological advancements and assess whether their businesses might be disrupted by emerging technologies.

Based on these four elements, investment allocation will exhibit distinct preferences and a unique style. From a practical standpoint, the first step is to implement a strategic, global layout. The dividend periods for these four elements may not be confined within a single national system; rather, they may manifest across various countries, both domestic and international, at different stages of time.

We are also exploring the window of opportunity in China’s manufacturing and process engineering sectors. Therefore, we leverage top-tier Chinese contract manufacturers to produce our lab-stage R&D products (such as smart glasses), achieving cost efficiencies on both sides. This approach not only helps companies identify global partners from a corporate perspective but also allows us, as investors, to engage at an earlier stage.

Many institutions ask themselves during investment, “Can we invest across an entire industry chain, or fully cover a specific category within a particular medical department?” Only through comprehensive ecosystem layout can enterprises achieve upstream and downstream synergy, share channels, and grow collectively.

Currently, 80% of Puhua’s portfolio companies share channels, user bases, or upstream and downstream manufacturers of raw materials and equipment. Additionally, at least six enterprises have established joint ventures to foster collaborative growth.

In summary, despite the intense external competition driven by globalization, China’s innovative drug R&D sector continues to benefit from support from domestic investment institutions and favorable policies, creating a highly advantageous overall environment. By avoiding overcrowded competition and market bubbles, we look forward to seeing more talent join this industry.