Health IQ Files for IPO: Revolutionizing Life Insurance with Health-Conscious Underwriting

Health IQ

Life Insurance Technology Startups

“Just as auto insurers reward safe drivers, individuals with healthy lifestyles should not have to pay excessive life insurance premiums.”

“This statement was made by Munjal Shah, founder of Health IQ. It represents both the founding impetus behind Health IQ and the company’s core development philosophy.”

Health IQ is a life insurance agency that serves both B2B and B2C markets. Leveraging a data-driven approach, it provides insurers with more accurate risk assessments while offering consumers fair, low-rate insurance services.

Over the past six years, Health IQ has helped insurers sell policies worth more than $15 billion, becoming one of the fastest-growing life insurance agencies in the United States.

Founded two startups in a row, which were subsequently acquired by Alibaba and Google

Health IQ founder Munjal Shah, a successful serial entrepreneur, graduated from the University of California, San Diego (UCSD) with a degree in Computer Science.

In 1999, 26-year-old Munjal Shah quit his job and founded his first company—Andale, an online auction management firm. The company provided software services tailored to online sellers. Shah pioneered this niche segment before Software-as-a-Service (SaaS) became a mainstream concept.

In its founding year, Andale secured $50 million in seed funding. Unfortunately, the following year saw the burst of the dot-com bubble. Amidst a global environment where internet companies faced significant development challenges, the startup Andale was inevitably affected. Unable to secure continued financing, Munjal Shah had to lay off staff, reducing the workforce from 200 employees to around 20.

Four years later, as the internet landscape improved, Andale gradually regained its vitality, with its workforce growing back to around 200 employees. However, at this point, Munjal Shah decided to sell the company to another enterprise, Vendio. Shortly thereafter, Vendio was acquired by the Chinese e-commerce giant Alibaba, making Andale part of the Alibaba Group.

After exiting his first venture, Munjal Shah almost immediately set out to found his second company—Like.com (originally named Riya). Like.com initially started as an image recognition tool and later evolved into a shopping search engine. By scanning photos, Like.com could help users find and match items available on online shopping platforms.

In 2008, just as Like.com completed its Series C financing round, the global financial crisis struck. Having weathered the dot-com bubble burst of 2000, Munjal Shah was well aware that a global financial crisis could be virtually catastrophic for startups.

Fortunately, Munjal Shah remained focused on the development of digital technologies, leading to increasingly mature product performance. As the global economy slowly recovered, Like.com’s products caught the attention of search giant Google. Accepting Google’s overture, Munjal Shah sold Like.com to Google for $120 million in 2010, joined Google as part of the acquisition, and served as Director of Product.

In a dramatic twist, the day after Munjal Shah sold Like.com to Google, he was rushed to the emergency room with severe chest pain. Believing he had reached the pinnacle of his life, the 37-year-old feared he might be suffering from heart disease, especially given that his father had suffered a heart attack at the age of 45. Fortunately, he was later diagnosed with pneumonia, proving the scare to be unfounded.

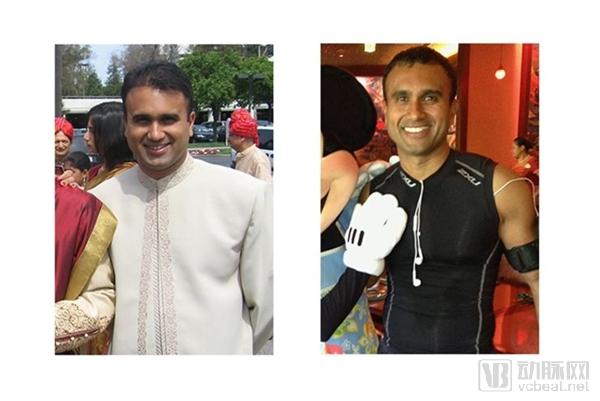

However, this experience served as a wake-up call for Munjal Shah, making him realize the importance of a healthy lifestyle. Since then, Munjal Shah has changed his dietary habits, started exercising regularly, and lost 40 pounds over the next few years.

Before-and-after fitness photos of Health IQ founder Munjal Shah (Image source: Health IQ official website)

During his time at Google, he connected with a group of individuals who had faced health challenges and successfully overcome them through healthy lifestyles. This experience also helped him identify the direction for his next venture: improving people’s overall health by rewarding those who are health-conscious.

Health Literacy Test: Creating the Largest Database in the U.S. Life Insurance Industry

In 2013, Munjal Shah resigned from his job to start a business with a group of colleagues he had met at Google. Their objective was clear: to offer lower life insurance premiums to health-conscious individuals. However, they were still uncertain about the specific operational model.

Health IQ Employee Team (Image from Health IQ Official Website)

To achieve their goal, Munjal Shah and his team needed to address two challenges: first, to demonstrate that health-conscious individuals have lower mortality rates, and second, to identify methods for determining which groups possess such health consciousness.

“First, we need to distinguish between health-conscious individuals and healthy individuals. Health-conscious people proactively choose lifestyles that benefit their health, whereas healthy people do not necessarily adopt healthy lifestyles; they are simply fortunate enough to have avoided illness,” said Munjal Shah.

In 2014, Health IQ launched a mobile application for daily health assessments, along with an online health literacy test. The Health IQ health literacy test comprises 30,000 questions covering health concepts such as nutrition, exercise, metabolism, disease, and digestion.

The company assembled a team of medical, nutrition, and fitness experts to review the scientific validity and accuracy of the questions. It then used a database of over 100,000 individuals to calibrate these 30,000 questions, identifying the 3,000 questions with the strongest predictive power for future health outcomes. After the assessment, the system calculates a score on a scale of 0–200 based on the accuracy and response time of the test-taker’s answers, and presents this score to the user.

Some Members of the Health IQ Expert Team (Screenshot from the Health IQ Official Website)

The Health IQ quiz is designed to assess individuals’ health awareness rather than evaluate their physical health status. Therefore, instead of asking whether test-takers are good at running, Health IQ asks if they can complete a one-mile run within eight minutes; nor does it ask whether they overeat, but rather tests their ability to estimate the calorie content of rice in a given photo, thereby gauging their understanding of dietary control.

Over a three-year period, more than 1 million people took Health IQ’s online test, during which approximately 2,000 test-takers passed away.

Munjal Shah’s team reached their desired conclusion through analysis: test takers with higher scores had a 41% lower mortality rate than those with lower scores. Furthermore, by comparing publicly available reports from the U.S. public and private sectors on diabetes, hypertension, and prescription drug costs, Health IQ found that individuals with higher health literacy have lower incidence rates of conditions such as diabetes, obesity, and hypertension compared to those with lower health literacy.

More importantly, the large number of participants enabled the test to collect a substantial amount of data. “Health IQ has inadvertently created the largest and entirely new population mortality database in the U.S., and indeed globally, seen in the insurance industry in nearly a century,” said Munjal Shah.

At this juncture, Munjal Shah’s team also realized that the database generated by Health IQ’s assessments could do more than simply calculate mortality rates; it could serve a broader purpose by identifying health-conscious individuals and demonstrating that they merit access to lower-priced life insurance.

From today’s perspective, big data has served as Health IQ’s moat in its competitive foray into new fields from the very beginning.

Offer 4%-33% discounts to policyholders with high health literacy

The Health IQ test not only demonstrates that “people with healthy lifestyles live longer,” but also promotes the emergence of new underwriting models, namely offering premium discounts to policyholders with high health literacy. Leveraging its proprietary database, Health IQ has successfully persuaded insurers such as SBLI, Ameritas, and Assurity, as well as reinsurer Swiss Re, to provide discounts ranging from 4% to 33% to those who take the Health IQ test.

Policyholders who wish to purchase insurance policies through Health IQ and obtain corresponding discounts need to go through three steps:

Step 1: The policyholder needs to complete a questionnaire about their personal health history on the Health IQ app or official website;

Step 2: The policyholder completes the Health IQ health literacy quiz within a specified timeframe to assess whether they are health-conscious;

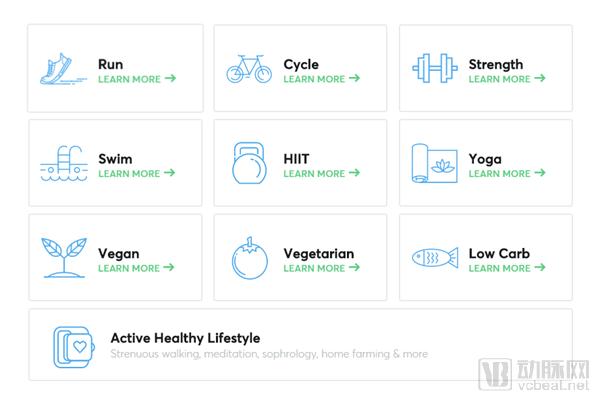

Step 3: The policyholder selects online which physical activity they have recently engaged in, such as strength training, HIIT, long-distance running, cycling, swimming, triathlon, hiking, or yoga, and submits electronic proof of exercise-related data, such as data from fitness tracking applications. If the applicant is not an avid exerciser, they may instead complete practical questions related to diet to demonstrate that they maintain an active and healthy lifestyle.

Health IQ places greater emphasis on assessing the test-taker’s health awareness (screenshot from the Health IQ official website)

The assessment system selects 30 questions from an initial pool of 3,000, tailoring the questions to each individual test-taker. To prevent cheating, respondents are required to answer within a specified time limit.

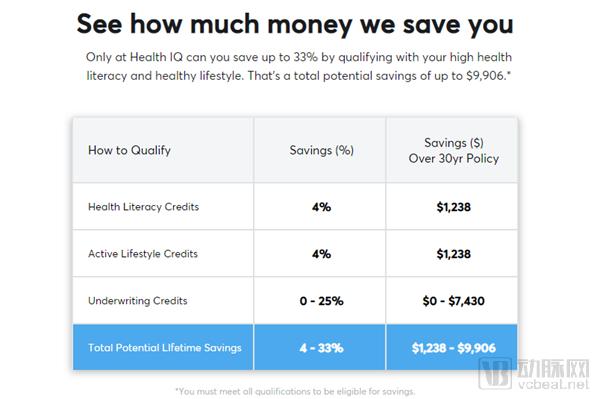

If policyholders pass Health IQ’s health literacy quiz and achieve an “Elite” score, they can receive a 4% discount on their life insurance policy; if they can verify their physical activity or healthy lifestyle with data—for example, by running a mile in under 8 minutes—they can receive an additional 4% discount on their life insurance policy. Furthermore, insurance companies partnering with Health IQ provide specialized underwriting guidance for health-conscious policyholders and offer them an additional 25% discount.

Health IQ’s life insurance can save consumers money (screenshot from the Health IQ official website)

Overall, if policyholders prioritize health and pass various assessments, their life insurance premiums can be up to 33% lower than those for the general population. By purchasing a 30-year term life insurance policy, policyholders can save nearly $10,000. According to Health IQ’s official website, 76% of applicants who apply for insurance through Health IQ are rated by insurers as being in the best underwriting classes, such as Preferred Plus and Preferred Best.

Health IQ offers three types of insurance: life insurance, disability insurance, and insurance for patients with diabetes.

Life insurance is divided into term life insurance and whole life insurance. Term life insurance generally provides coverage for 10 to 30 years, with policyholders able to pay premiums on a monthly, quarterly, or annual basis; this is the most popular and affordable type of life insurance offered by Health IQ. Whole life insurance carries slightly higher premiums than term life insurance and requires policyholders to make continuous premium payments. In return, whole life insurance provides lifelong coverage for the policyholder.

Data research from Health IQ and studies published in The New England Journal of Medicine have found that type 2 diabetes patients who control their glycated hemoglobin (HbA1c) levels through physical exercise and a healthy lifestyle experience a 40% to 72% reduction in mortality. Meanwhile, Health IQ’s database possesses the capability to predict health trends. “Individuals with higher health literacy are more inclined to maintain healthy lifestyles,” said Munjal Shah, who believes that diabetic patients with well-managed conditions should pay lower premiums for life insurance.

To this end, Health IQ partnered with Protective Life in November 2018 to launch a life insurance product specifically designed for individuals with diabetes. Diabetic patients who meet the following criteria—such as maintaining well-controlled blood glucose levels, adopting a healthy lifestyle, and achieving an “Elite” score on the Health IQ Diabetes Quiz—are eligible for a 38% discount on their life insurance premiums.

Additionally, health-conscious individuals with disabilities can also obtain coverage from Health IQ. By passing the various assessments established by Health IQ and achieving the corresponding scores, they can qualify for a 15% discount on life insurance.

Unlike traditional insurance companies, Health IQ does not assess risk solely based on an applicant’s current health status; instead, it integrates factors such as dietary habits, health literacy, physical activity levels, and overall lifestyle to predict long-term health outcomes.

In Munjal Shah’s view, if policyholders have a high level of health literacy and maintain an active lifestyle, they can improve their health in the future, even if their current health status is poor. This is one of the key reasons why Health IQ dares to provide insurance coverage for patients with diabetes.

Facebook and Airbnb Investors Remain Bullish on Its Underwriting Model

Currently, Health IQ has completed its Series C financing, raising a total of $81 million in funding. Investors include prominent venture capital firms such as Andreessen Horowitz, Charles River Ventures, First Round Capital, and Foundation Capital.

Andreessen Horowitz, renowned in the United States for its investments in Facebook, Slack, and Airbnb, recognized Health IQ’s growth potential and its significant impact on the life insurance industry. After leading Health IQ’s Series B financing round, Andreessen Horowitz continued to lead the company’s Series C financing round.

Health IQ’s revenue model involves earning commissions from both insurance companies and policyholders. Despite this dual-source compensation, it has not hindered Health IQ’s popularity.

Since its inception, Health IQ has continuously broken its own performance records. Within 12 months of launching its first life insurance product, Health IQ sold $500 million worth of policies; within 22 months, total policy sales reached $5.3 billion. To date, Health IQ has sold policies with a total value exceeding $15 billion.

More than 30 insurance companies, including Prudential, Pacific Life, Securian, Transamerica, Mutual of Omaha, and Principal, have partnered with Health IQ. Health IQ has also earned an A+ rating from the Better Business Bureau (BBB).

Nowadays, Health IQ has established its brand presence in the industry and carved out a new niche market for itself. Moldow, a member of Health IQ’s board of directors, believes this market is worth tens of billions of dollars. In Health IQ’s strategic plans, the company intends to expand its business from life insurance into areas such as long-term care and cancer coverage.

In fact, the concept of rewarding healthy policyholders has long been prevalent in the U.S. insurance industry; for example, Oscar Health’s additional services include cash rewards for users who engage in daily exercise.

John Hancock, one of the top ten life insurance companies in the United States, launched the “Vitality Program” in 2015, a health-based insurance initiative that rewards customers for maintaining healthy lifestyles. According to statistics from a database containing over three million exercise records, John Hancock policyholders take nearly twice as many steps as the average American. Ultimately, John Hancock decided to offer only those insurance products that encourage healthier lifestyles and help extend customers’ lifespans.

In China, encouraging policyholders to improve their health through healthy behaviors is gradually becoming a prevailing philosophy among domestic insurance companies.

Manulife-Sinochem Life Insurance launched the MOVE program in 2016, encouraging consumers to invest in their future healthy lifestyles by starting with small daily steps. Upon becoming a MOVE member, consumers can claim a complimentary smart fitness tracker and, upon achieving specified activity goals, become eligible for life insurance coverage of up to RMB 200,000.

Furthermore, third-party insurance brokerage firms that connect insurers with policyholders are also exploring similar models. Miao Jiankang, a health technology company, has spent three years building a comprehensive empowerment service system centered on health data tracking, AI-driven health interventions, and gamified operations, leveraging big data on health behaviors and artificial intelligence. While helping insurers enhance customer acquisition and conversion capabilities, develop differentiated insurance products, improve user affinity and stickiness, and reduce claim ratios, Miao Jiankang also assists users in continuously improving their health behaviors, with the ultimate goal of extending lifespan.

In the domestic market, many insurance products have emerged that dynamically adjust coverage amounts through health services or interactive mechanisms. Examples include Ping An Insurance’s “Ping An Fu Run” program and Tencent’s WeSure “WeFit” program. These products are characterized by their “interactive” concept, with premiums primarily determined by users’ daily step counts.

Globally, whether it is insurance companies like John Hancock and Manulife-Sinochem adopting the underwriting model of “health management + insurance,” or third-party enterprises like More Health, or even the operational model of Health IQ, which offers discounts to policyholders with high health literacy through testing and screening, all are striving in the same direction: encouraging users to improve their health status through healthy behaviors, thereby leading healthier lives. This represents one of the most fundamental and effective ways for the insurance industry to control risk, and it is also one of the core reasons for the existence of the insurance sector.

Reference link:

https://www.healthiq.com/

https://markets.businessinsider.com/news/stocks/health-iq-secures-34-6-million-in-series-c-funding-led-by-andreessen-horowitz-1008128607

https://foundr.com/life-mission-munjal-shah-health-iq/

https://www.noexam.com/life-insurance/companies/health-iq/