Global Pharma M&A Report 2019: $270 Billion in Deals, Industry Giants Refocus on Core Businesses

2018 was a landmark year for mergers and acquisitions in the pharmaceutical industry. This significance stems not from the transaction volume being comparable to that of 2016 and 2017, but rather from the fact that these deals fundamentally reshaped the competitive landscape for several major pharmaceutical companies.

VCBeat (WeChat ID: vcbeat) has translated the “2019 Pharmaceutical Industry M&A Report” released by the globally renowned consulting firm Kurmann Partners. The report shows that in 2018, there were approximately 360 mergers and acquisitions in the pharmaceutical industry, with a total transaction value of $270 billion. Among these, the largest deal was Takeda Pharmaceutical’s acquisition of Shire for approximately $80 billion.

So, what will the M&A landscape look like in 2019? Experts predict that some large pharmaceutical companies may undertake significant divestitures to streamline their operations. Additionally, mergers between major pharmaceutical firms will occur within the industry; for instance, in January 2019, Bristol-Myers Squibb announced its acquisition of Celgene. Strategically, acquisitions among patented drug manufacturers may make sense. However, industry-wide uncertainty stemming from Brexit and U.S. politics could complicate the execution of large-scale deals.

As a long-established Japanese company, Takeda Pharmaceutical aims to accelerate its internationalization and build a value-based, R&D-driven global leading biopharmaceutical company through the acquisition of Shire, achieving a scale sufficient to secure financing for competitive drug development. This merger will also trigger a wave of divestitures to streamline the business platform and repay Takeda’s debt by increasing revenue.

Takeda Pharmaceutical’s acquisition of Shire helped it expand into new business areas, thereby achieving commercial diversification, while Novartis pursued a different strategic direction by continuing to focus on innovative drugs.

In November 2018, Novartis announced the spin-off of its eye care division, Alcon. On April 9, 2019, Alcon was listed as an independent company on both the Swiss Exchange and the New York Stock Exchange, with its market capitalization expected to reach $21 billion. Alcon’s departure marked a milestone in Novartis’s development. In 2014, after a decade-long acquisition spree that transformed it into a complex healthcare enterprise, Novartis embarked on a systematic strategic shift to focus on innovative pharmaceuticals. Rumors also suggest that Novartis plans to spin off its generics division, Sandoz.

In 2018, GlaxoSmithKline’s (GSK) merger and acquisition activities drew the most attention, as they transformed the company’s business model. In March 2018, GSK announced it would acquire Novartis’s 36.5% stake in their consumer healthcare joint venture for $13 billion. Later, at the end of 2018, Pfizer and GSK announced the formation of a joint venture to merge their consumer healthcare businesses, with GSK becoming the majority shareholder. The paid-in capital of the GSK-Pfizer joint venture reached $12.7 billion, positioning it to become a market leader in the United States and China. Based on the valuation of the Novartis-GSK transaction, experts estimated that Pfizer’s 32% stake in the joint venture was worth approximately $17 billion.

However, GlaxoSmithKline did not stop there. Concurrent with its transaction with Pfizer, GlaxoSmithKline planned to split into two companies within two to three years: one focused on consumer health and the other on the development and commercialization of innovative medicines.

By analyzing the mergers, acquisitions, and spin-offs of large pharmaceutical companies, it becomes evident that mid-stage large pharmaceutical enterprises must choose one of the following four development strategies: patented drug manufacturing, generic drug manufacturing, over-the-counter (OTC)/consumer health, and point-of-care. Each strategy corresponds to distinct corporate cultures and objectives, and entails different capital structures. Moreover, hybrid business models increase complexity and reduce competitiveness.

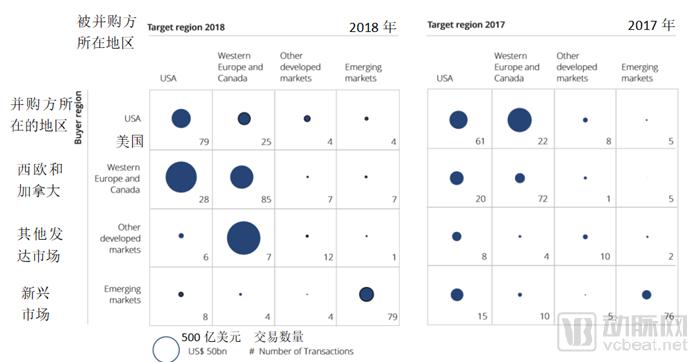

Figure 1: M&A Activity in the Pharmaceutical Industry in 2018. The numbers indicate the number of transactions, and the circle sizes represent the total disclosed or estimated transaction value.

Other transactions in 2018 also reflected the pharmaceutical industry’s trend toward streamlining business platforms and focusing on one of four strategic development pillars. In the consumer health sector, Merck sold its consumer health business to Procter & Gamble for $4.2 billion, while Bristol-Myers Squibb divested its French over-the-counter (OTC) drug business to Taisho Pharmaceutical for $1.6 billion. To strengthen point-of-care services in dermatology, LEO Pharma acquired Bayer’s prescription dermatology business for approximately $800 million. Servier, France’s second-largest pharmaceutical company, acquired the commercial rights to Shire’s oncology portfolio for $2.4 billion, thereby securing its commercial operations in the U.S. market.

In January 2018, Sanofi announced two major acquisitions aimed at establishing a sustainable platform in specific niche segments to provide “end-to-end” services. The French pharmaceutical giant initially agreed to acquire Bioverativ for $11.6 billion, and just days later, it acquired Ablynx for $4.5 billion. Bioverativ already had two hemophilia treatments on the market, generating approximately $1.1 billion in revenue in 2018, a 30% year-on-year increase. Through the acquisition of Ablynx, Sanofi gained an innovative technology platform that included drug development programs for coagulation disorders, one of which had already received approval in Europe. With these two transactions, Sanofi aims to become a leader in the market for rare blood disorder therapies.

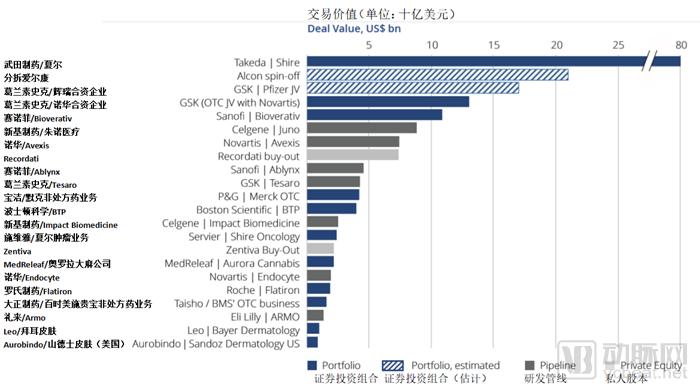

Figure 2: Transactions in 2018 by Strategic Type. Securities Investment Portfolio – Acquisition or Divestiture of Business Platforms. R&D Pipeline – Acquisition of Drug Development Projects. Private Equity – Acquisitions by Financial Investors.

As in previous years, pharmaceutical companies sought to acquire innovative drugs in late-stage development or early commercialization through several major transactions in 2018. For example, Celgene acquired Juno Therapeutics, a biopharmaceutical company specializing in CAR-T and TCR therapies, for $8.8 billion; Novartis acquired gene therapy company AveXis for $7.5 billion; and GlaxoSmithKline acquired Tesaro for $5 billion, whose marketed PARP inhibitor is used for cancer treatment.

In addition to the traditional pharmaceutical industry, the legalization of cannabis in Canada and certain U.S. states has also spurred several transactions. In 2018, there were approximately 30 deals involving the manufacturing or commercialization of medical cannabis. The largest of these was Aurora Cannabis’s all-stock acquisition of MedReleaf, valued at $2 billion, equivalent to 66 times MedReleaf’s 2018 revenue. This represents an exceptionally high price for a cannabis producer. Although market participants anticipated that legalization would significantly boost demand, the company’s valuation was indeed high relative to the industry.

Takeda Pharmaceutical’s acquisition of Shire was one of the largest mergers and acquisitions in the history of the pharmaceutical industry, yet it carried high risks and uncertain outcomes.

Currently, Takeda Pharmaceutical Company, following its merger with Shire, ranks among the top ten pharmaceutical groups worldwide. On one hand, by integrating Shire, Japan’s largest pharmaceutical company, Takeda has truly become a global enterprise. On the other hand, Shire’s shareholders also stand to benefit from the deal. However, beyond expanding its business footprint, Takeda also aims to achieve a strategic transformation through this acquisition.

Five years ago, Takeda Pharmaceutical was significantly impacted by the contraction of Japan’s domestic market—which accounted for nearly 50% of its revenue—as well as the impending patent expiration and safety concerns surrounding its previously best-selling diabetes drug, Actose. Furthermore, despite large-scale overseas acquisitions, including the $8.8 billion purchase of U.S.-based Millennium Pharmaceuticals in 2008 and the $13.7 billion acquisition of Swiss pharmaceutical company Nycomed in 2011, which expanded its operations in Europe and Latin America respectively, Takeda’s corporate culture and business focus remained distinctly Japanese.

Therefore, in 2014, Takeda Pharmaceutical chose to shift its strategy to further advance its internationalization, a move that inevitably brought corresponding pressures. Christophe Weber, the first foreigner to lead Takeda, has been committed to transforming the Japanese company, founded in 1781, into a global pharmaceutical enterprise since he assumed the role of Chief Executive Officer in 2015.

However, changing a company’s internal culture is theoretically quite challenging. In 2017, Takeda Pharmaceutical acquired the oncology company Ariad and the cell therapy company Tigenix for $5.2 billion, which indeed helped accelerate Takeda’s drug development process. Yet, as Weber stated in May 2018 when announcing the acquisition of Shire, amid pricing pressures and rising drug development costs, only large-scale acquisitions capable of expanding Takeda’s size represented a “path to survival.” In fact, many believe that his personal ambition and sense of urgency were key factors driving the deal.

Following the acquisition of Shire, Takeda Pharmaceutical doubled in size, but perhaps more importantly, the deal fundamentally transformed Takeda, helping it evolve into a truly global pharmaceutical group. Specifically, the proportion of non-Japanese employees rose from less than 70% to over 82%, while its revenue base continued to diversify, with Japan’s share of total revenue declining from one-third to less than one-sixth. Furthermore, the acquisition internationalized Takeda’s ownership structure, as half of the purchase price was paid in Takeda stock, resulting in a significantly higher proportion of shares now held by foreign shareholders (former Shire shareholders).

The question, however, is whether these benefits truly justify such a high price. The acquisition process spanned several months, with Takeda Pharmaceutical’s final offer being its fifth bid and representing a 60% premium over Shire’s actual share price prior to Takeda’s initial public takeover approach. For a mature company with a market capitalization in the tens of billions of dollars, this valuation is indeed exceptionally high.

On the other hand, some observers believe that Shire is undervalued. They argue that Shire’s stock price does not fully reflect its transformation. Initially, Shire focused on specialty pharmaceuticals, but it later acquired a series of orphan drug and biotechnology companies, most notably Baxalta for up to $32 billion. Today, approximately three-quarters of Shire’s revenue comes from biopharmaceuticals. As one analyst noted, Takeda Pharmaceutical values the specialty pharmaceutical sector. Even so, Takeda’s acquisition price amounted to 5.3 times revenue and 32 times EBITDA.

However, some of Takeda Pharmaceutical’s shareholders were initially skeptical about the acquisition. Since news of the Shire takeover first emerged, Takeda’s share price had fallen by 25%. Ultimately, following strong advocacy by CEO Christophe Weber, a majority of Takeda’s shareholders voted in favor of the deal at an extraordinary general meeting held in early December 2018. The acquisition of Shire was completed on January 7, 2019.

This acquisition represents the largest overseas deal ever undertaken by a Japanese company, but it also carries significant risks. The integration process will be long and arduous. Prior to the acquisition, Takeda Pharmaceutical was already burdened with substantial debt (four times its EBITDA), so it will have to divest certain assets post-acquisition to repay these obligations. Furthermore, Takeda needs to address its purely domestic brands and non-core products, which may yield relatively low returns compared to the price paid for Shire. Indeed, whether the acquisition of Shire will ultimately deliver commensurate returns to Takeda’s shareholders remains an open question.

For decades, Swiss pharmaceutical giant Novartis has leveraged mergers and acquisitions to build a diversified healthcare group. In 2014, Novartis shifted its development strategy. Since then, the company has divested one business after another, choosing to focus on its core business: innovative medicines.

On November 15, 2018, local newspapers in Basel reported that Swiss pharmaceutical giant Novartis planned to divest its generic drug division, Sandoz. Novartis’s official response stated: “The transaction is not imminent; however, Sandoz will be restructured into an independent business unit, while Novartis will retain full ownership.”

Since its founding in 1996, Novartis has envisioned becoming a diversified health products provider, akin to Johnson & Johnson. By the end of 2004, Novartis had expanded beyond its core business of innovative prescription drugs, offering not only generic medicines (Sandoz), over-the-counter medications, and vaccines, but also consumer eye care products (Ciba Vision), medical nutrition, diagnostics, and animal health products. However, some business units were too small and lacked competitiveness, prompting Novartis to pursue large-scale acquisitions to expand its platform.

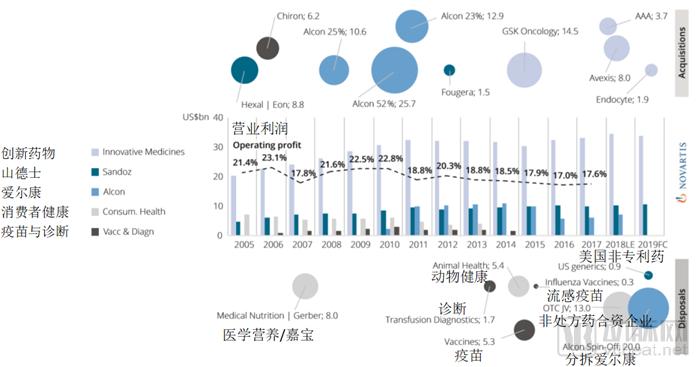

Figure 3: Selected acquisitions by Novartis since 2005 (upper part) and divestitures of its businesses (lower part). The size of the circles corresponds to the publicly disclosed transaction amounts. The central chart reflects Novartis’s revenue (bar chart) and operating profit (dashed line) (in billions of U.S. dollars).

In 2005, Novartis acquired Germany’s Hexal AG and EON Labs for more than $8 billion, making its generics division, Sandoz, one of the largest generic drug suppliers and a leader in the development of biosimilars. In 2006, Novartis acquired the U.S.-based Chiron Corporation (vaccines, diagnostics, and biologics). However, the company’s largest transaction to date occurred between 2008 and 2011, when it acquired Alcon in three steps, with a total transaction value exceeding $50 billion.

By 2012, Novartis primarily comprised five divisions: Innovative Medicines, Eye Care (Alcon), Generics (Sandoz), Consumer Health (including Animal Health), and Vaccines & Diagnostics. Alcon, Sandoz, and the Innovative Medicines division (including the Oncology unit) were all global market leaders; however, the group had become overly large and complex to manage, prompting Novartis to change its strategic direction.

In April 2014, Novartis announced the divestiture of all its consumer health, diagnostics, and vaccine-related divisions. In a series of concurrent transactions, the over-the-counter (OTC) pharmaceuticals division was transferred to a joint venture with GlaxoSmithKline (GSK), the vaccines business was sold to GSK, and the animal health unit was sold to Eli Lilly and Company. Concurrently, Novartis acquired GSK’s oncology portfolio, including late-stage development projects and marketed innovative drugs. This strategic move significantly strengthened Novartis’ oncology business, becoming one of the key drivers of its growth and profit expansion.

In the subsequent quarters, there were many signs that Novartis was also seeking solutions for Alcon. In 2016, after transferring Alcon’s eye care products (valued at approximately $4 billion) to the Innovative Medicines division, investors found that Alcon’s surgical and eye care products were causing significant losses for the company. Rumors circulated that Novartis had attempted to sell the division but was unsuccessful. Finally, in mid-2018, Novartis announced the spin-off of Alcon through a distribution of Alcon shares, a move scheduled to be completed in the second quarter of 2019.

In addition to acquiring large commercial platforms, Novartis has been continuously refining its drug development pipeline, aiming to secure innovative technology platforms through larger (and higher-risk) deals that could serve as the foundation for a series of novel therapies. For instance, in early 2018, Novartis acquired Advanced Accelerator Applications, establishing a strong position in radiopharmaceuticals and safeguarding its existing proprietary rights in neuroendocrine tumors. Reportedly, Novartis will also acquire Endocyte in the second quarter of 2019 for $2 billion.

Furthermore, in September 2018, Novartis acquired AveXis. AveXis is a gene therapy company with a gene therapy development program. However, this alone was unlikely to drive Novartis’ $8 billion acquisition offer, as only 700 patients per year in the United States would benefit from AveXis’s spinal muscular atrophy (SMA) therapy. Nevertheless, AveXis’s expertise in gene delivery could be applied to many other areas. Through this high-stakes, high-value transaction, Novartis further solidified its leadership position as a developer of gene therapies, a status previously established by its successful development of the first CAR-T cell therapy.

By acquiring companies such as Advanced Accelerator Applications and AveXis, Novartis has expanded its platform and enabled the continued growth of its Innovative Medicines division, raising another question: How does Sandoz fit into Novartis’s future?

It is difficult to be a cost leader in one area while simultaneously being an innovation leader in another. Facing significant price pressure in the global market, particularly in the United States, for generic drug sales, Novartis chose to sell most of its U.S. generic drug business to India’s Aurobindo Pharma.

Furthermore, Sandoz’s core business—biosimilars—may be better suited for the oncology division, where they can be marketed as part of combination therapies. Therefore, transferring high-margin biosimilars from Sandoz to the Innovative Medicines division and subsequently spinning off Sandoz is, in theory, a logical decision.