Tasly Biopharmaceuticals Files for Hong Kong IPO with Blockbuster Drug Puyouke Generating Over RMB 220 Million in 2018 Sales

On April 23, Tasly Group issued an announcement stating that its subsidiary, Tasly Biological Products, will apply for a separate listing on the Hong Kong Stock Exchange. This move aims to establish independent financing capabilities for Tasly Biological Products, support its future business development, and unlock the value of the company’s biologics segment.

The announcement disclosed Tasly’s profitability data for the past three years. The net profit attributable to shareholders of the parent company amounted to approximately RMB 1,176.42 million, RMB 1,376.54 million, and RMB 1,545.16 million in 2016, 2017, and 2018, respectively. Tasly has achieved consecutive profits over the past three years. Furthermore, there is no horizontal competition with its subsidiary, Tasly Biological; its assets and finances are independent; and there is no overlap in managerial positions. These factors confirm that the Hong Kong listing of its subsidiary, Tasly Biological, complies with the regulations of the China Securities Regulatory Commission (CSRC).

Tasly Biopharma Valued at $1.895 Billion

Shanghai Tasly Pharmaceutical Co., Ltd. (formerly known as Shanghai Tasly Pharmaceutical Co., Ltd.) was established in 2001 and is primarily engaged in the research and development of biopharmaceuticals, serving as a commercialization platform for biological drugs across multiple therapeutic areas. Tasly Biologics’ flagship product is Pro-urokinase for Injection (brand name: Puyouke), China’s first Class 1.1 innovative biological drug with independent intellectual property rights, which underwent ten years of development. Among biopharmaceutical companies listed in Hong Kong, Tasly Biologics is one of the few that already has mature products on the market. The company is also advancing its R&D layout in three major fields—cardiovascular and cerebrovascular diseases, digestion and metabolism, and oncology and immunology—rapidly progressing its pipeline of candidates with international competitive advantages.

Prior to its initial public offering, Tasly Biopharmaceuticals carried out a capital increase and share expansion in July 2018. By introducing internationally renowned pharmaceutical companies and healthcare industry funds as strategic investors, the company achieved a separate valuation for Tasly’s innovative biological drugs. This capital increase involved five institutional investors, including four overseas investment institutions and one international pharmaceutical company, with a total investment of USD 132.5 million. These investors subscribed to 75.71 million newly issued shares of Tasly Biopharmaceuticals, representing approximately 6.99% of the company’s total share capital after the completion of the capital increase and share expansion.

Among them, four overseas investment institutions, including Huiqiao Capital, Puke Cayman, BOCOM International, and Jiaheng Investment, contributed USD 84.5 million in cash, accounting for 4.46%; Transgene SA contributed USD 48 million in non-monetary assets (50% equity interest in Tasly GenesisJie and the “T101 patent”), accounting for 2.53%. Transgene SA is a joint venture partner of GenesisJie (Tianjin) Pharmaceutical Co., Ltd., a subsidiary of Tasly Bio-pharmaceutical. According to the agreement, the pre-money valuation of Tasly Bio-pharmaceutical was USD 1.762 billion, and the post-money valuation after the capital increase and share expansion was USD 1.895 billion. This valuation is significantly higher than the typical USD 1–1.5 billion valuations seen among other companies listing in Hong Kong.

The Tasly Bio platform is a typical example of Tasly leveraging minority equity investments to capitalize and innovate its industrial layout in novel drugs. Tasly Bio was established through multiple initiatives, including the joint venture forming Tasly Genescience (Tianjin) Biopharmaceutical Co., Ltd., the acquisition of Shanghai Saiyuan Technology Co., Ltd., and investments in R&D-focused platforms such as Tianjing Biotech (Shanghai) Co., Ltd., PegBio, and Jianya Bio, as well as collaborations with South Korea’s Genexine and Ascletis Pharma. Its pipeline primarily covers three major therapeutic areas: cardiovascular and cerebrovascular diseases, digestive and metabolic disorders, and oncology and immunology.

Puyouke’s 2018 sales exceeded RMB 220 million

Puyouke is the only marketed pro-urokinase product expressed in Chinese Hamster Ovary (CHO) cells worldwide. It is produced through genetic engineering using CHO cell expression and is indicated for thrombolytic therapy in acute ST-segment elevation myocardial infarction (STEMI), belonging to the third generation of thrombolytic agents. It exerts selective thrombolytic effects primarily by activating plasminogen on the surface of fibrin and has been included in multiple clinical practice guidelines for cardiovascular diseases.

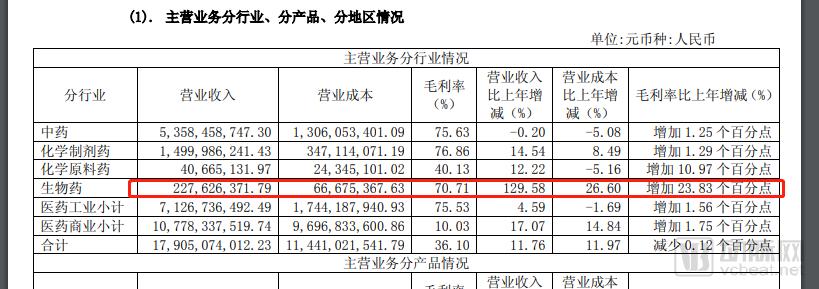

In 2017, Puyouke entered the National Reimbursement Drug List (NRDL) through price negotiations conducted by the Ministry of Human Resources and Social Security, with a price reduction of 11.5% and a reimbursement price of RMB 1,020 per vial. Sales revenue for Puyouke was RMB 38 million in 2016 and rose to RMB 99 million in 2017, marking rapid growth. After its inclusion in the NRDL, Puyouke became the leading thrombolytic product, driving continued substantial sales growth in 2018. In 2018, Puyouke’s sales revenue exceeded RMB 220 million, representing a year-on-year increase of 129.58% compared to 2017.

Tasly's 2018 annual report disclosed the 2018 sales revenue of Puyouke.

Myocardial infarction is typically treated with percutaneous coronary intervention (PCI) or thrombolytic therapy, with PCI being the preferred first-line treatment. However, emergency PCI is technically challenging, and county- and district-level hospitals accounted for only 7.68% of PCI cases in China (based on 2016 data on coronary intervention in mainland China). In hospitals without PCI capabilities, intravenous thrombolysis can be employed. First-generation thrombolytic agents, such as urokinase, are rarely used in current international clinical practice due to their low recanalization rates and high bleeding risks. Second-generation thrombolytics, such as alteplase, have limited potential for adoption in primary care settings due to their short half-life and inconvenient administration. Puyouke is a third-generation thrombolytic agent.

Currently, the mainstream drugs in the market are alteplase and urokinase, with alteplase accounting for 54.56% of sales. As a representative third-generation thrombolytic agent, Puyouke (rhTNK-tPA) features fibrin specificity and lacks antigenicity and allergic reactions. Data from 2,088 cases in its Phase IV clinical trials demonstrated that the drug achieved a vessel recanalization rate of 85.2% in patients with acute myocardial infarction, with a drug-related intracranial hemorrhage incidence of only 0.19%. Furthermore, its half-life reaches 114 minutes, offering high overall cost-effectiveness.

In 2018, Tasly Biological’s Puyouke project for secondary capacity expansion and process optimization at the 20L reactor scale completed production process validation and related data testing. The process was successfully put into production in the first half of 2018, with Puyouke’s maximum annual production capacity reaching approximately 640,000 units. The Puyouke 300L reactor project completed the Factory Acceptance Testing (FAT) of major equipment and initiated the renovation of the production workshop. Upon completion, the annual production capacity is expected to reach 2 million units, providing a capacity guarantee to meet the rapidly growing market demand for Puyouke.

Tasly Bio's Pipeline in Development

Tasly Biological Drug R&D Pipeline

In addition to Puyouke, Tasly’s key products under development include 14 Class I novel biologics targeting cardiovascular and cerebrovascular diseases, oncology, and diabetes (two of which are new indications for Puyouke). These candidates cover common oncology targets, third-generation insulin, and diabetes-related targets. In 2016, Puyouke received clinical trial approvals for two new indications: ischemic stroke and acute pulmonary embolism (pulmonary infarction). The ischemic stroke indication has entered Phase III clinical trials for both the 0–4.5-hour and 4.5–6-hour treatment windows, with patient enrollment proceeding smoothly. The acute pulmonary embolism indication has entered Phase II clinical trials. As the stroke indication is included in the priority review pathway, approval is expected in 2019. Currently, the incidence of cerebral infarction in China far exceeds that of myocardial infarction, indicating substantial market potential. Once the two new indications are approved, the three indications for Puyouke could generate annual revenues exceeding RMB 3 billion.

Anmeimu MAb, fully named “Recombinant Fully Human Anti-EGFR Monoclonal Antibody,” is a Class 1 biologic drug developed by Shanghai Sailun Bio, a subsidiary of Tasly, for the treatment of colorectal cancer. Tasly Biopharmaceuticals ranks among the top tier in China’s R&D landscape. The drug is currently undergoing Phase I clinical trials, with preliminary results demonstrating definitive efficacy and a safety profile superior to that of internationally marketed comparable products.

T101 is the world’s first therapeutic hepatitis B vaccine using an adenovirus vector, jointly developed by Tasly Chuangshijie, a subsidiary of Tasly Biopharmaceuticals, and Transgene, a company under the French Merieux Group. It was included in the Center for Drug Evaluation (CDE)’s Priority Review List in 2016 and is currently undergoing Phase I clinical trials. Unlike antiviral therapies that suppress HBV replication through medication, T101 works by inducing patients’ own HBV antigen-specific cytotoxic T lymphocytes (CTLs), thereby inhibiting or even clearing HBV, or inducing apoptosis of HBV-infected hepatocytes, leading to sustained disease control. T601 (recombinant oncolytic vaccinia virus injection) has obtained clinical trial approval. Additionally, two other products—Lizhingsu (an FGF21 analog injection) and a fully human anti-PCSK9 monoclonal antibody injection for targeted treatment of hyperlipidemia—are poised to submit applications for clinical studies.

Tasly Biopharmaceuticals invested in PegBio, securing market priority rights for PegBio’s long-acting GLP-1 analog and its dual GLP-1/glucagon receptor agonist. The long-acting GLP-1 analog is a Class 1.1 innovative drug for the treatment of type 2 diabetes. It has simultaneously completed four Phase I clinical trials in both China and the United States, demonstrating superior glucose-lowering efficacy compared to currently marketed GLP-1 drugs in China. Tasly Biopharmaceuticals made a strategic investment of USD 50 million in Jianya Bio, obtaining sales priority rights for Jianya Bio’s insulin glargine and insulin lispro in mainland China. Jianya Bio is currently a leader in the research and development of third-generation insulins in China.

If Tasly Biopharmaceuticals successfully lists in Hong Kong, its biologic drug platform will achieve independent development. The strong sales performance of its already marketed drugs will ensure the company’s self-sustaining revenue generation capability, while new financing will significantly alleviate the parent company’s cash flow pressure. Tasly Biopharmaceuticals will use the raised funds for R&D, introducing new drug pipelines, and daily operations, which can effectively improve its asset structure, promote healthy operations and sustainable development, and provide financial assurance for subsequent R&D of innovative biologics.

References:

Tasly 2018 Annual Report

Caitong Securities: Tasly Biopharma’s Imminent HKEX Listing and Innovation-Driven Transformation to Comprehensively Boost Company Valuation

GF Securities: Tasly Bio’s Pre-IPO Round Concluded, Valuation Ranks Among the Top