Leng Yan of Legend Star: Assessing NGS Company Valuation and Innovation Opportunities in the IVD Sector

VCBeat New Medicine (WeChat ID: biobeat1) has learned thatRecently, Leng Yan, a partner at Legendstar Capital, was invited to attend the “Precision Medicine: Seizing Opportunities in Ningbo” – 2019 Ningbo Precision Medicine Industry Investment Forum hosted by Zero2IPO Group, and delivered a keynote speech titled “Assessing the Value of Next-Generation Sequencing Companies to Identify Innovation and Investment Opportunities in the IVD Sector.”

Leng Yan believes that,The IVD Sector Is a "Jianghu", as the founderLearn to Calculate Three Accounts: Calculating the books for hospitals, for distributors, and for one’s own enterprise. If even one of these three sets of accounts is not clearly understood, the company’s development may fall short of expectations. And in this “jianghu” (competitive landscape), as an investor,When selecting investment targets, personnel fit is the most critical factor.。

Leng Yan also analyzed why the NGS oncology sector has emerged as a winner, how to assess the investment value of an NGS company, and the factors influencing the break-even point for tumor NGS enterprises, while providing an in-depth discussion on future investment opportunities.

Here are the highlights from the speech:

Good morning/afternoon, everyone. Thank you very much to Zero2IPO for the invitation. It is a pleasure to have this opportunity to discuss with you today how assessing the value of next-generation sequencing (NGS) companies can shed light on innovation and investment opportunities in the IVD sector.

Legendstar Capital is a comprehensive fund focused on early-stage investments, primarily targeting three sectors: artificial intelligence, TMT (Technology, Media, and Telecom), and healthcare, with an emphasis on Angel and Series A rounds. Since 2010, we have invested in nearly 300 projects, including more than 50 in the healthcare sector. Our investment strategy in the healthcare field has evolved from prioritizing domestic market size and technological leadership before 2013 to, over the past five years, placing greater emphasis onInnovations verifiable through international collaboration; founders and teams with a global perspective and experience; and whether the product addresses unmet clinical needs (uniqueness).etc.

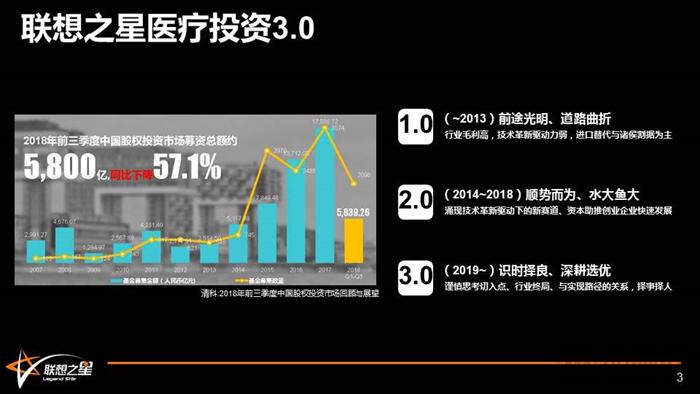

Let’s first look back at the past decade. InPrior to 2013Early-stage investing in the healthcare sector is a challenging endeavor. From 2007 to 2013, I worked on mergers and acquisitions at a publicly listed pharmaceutical company. During that period, the launch of the ChiNext Board made companies with strong revenue and profit growth potential, as well as those with a technology-driven narrative, particularly attractive in the primary market. As for industrial M&A, there was also a clear preference for targets capable of contributing consolidated profits or whose products were on the verge of obtaining regulatory approval.

During that phase, the key characteristics of the IVD industry were primarily:The industry boasts high gross margins, with companies operating in a fragmented landscape. Growth is primarily driven by import substitution through incremental innovations or minor improvements, while the impact of new technologies remains relatively limited. Investors show little interest in companies stuck in the J-curve plateau, making it difficult for early-stage enterprises to secure funding. Consequently, entrepreneurs often opt to enter industries with lower barriers to entry.

After 2014, the situation underwent significant changes. In fact, cyclical fluctuations have always existed in the primary market, but as we can see from the chart,2014 to 2018During this cycle, the equivalent amount of available capital in the primary market was several times greater than in previous cycles. Consequently, there was strong demand from investors for investable targets, with limited sensitivity to valuations. Coupled with national policies encouraging innovation and entrepreneurship, this dual drive of technology and capital gave rise to rapidly emerging new sectors, such as NGS-based companion diagnostics for oncology in the IVD field and biopharmaceuticals in the innovative drug sector. Startups during this phase rode the wave of favorable conditions, benefiting from a vast market that enabled significant growth.

Phase 3.0 Starting from 2019, both capital and enterprises will face a new landscape. In terms of challenges, liquidity in the primary market has tightened compared to previous years. However, the opportunities lie in the clear policy tilt toward medical technology companies with an innovation label, as seen with the Hong Kong Stock Exchange in 2018 and the STAR Market in 2019, which have provided clearer exit channels for both early-stage investors and startups.

Recently, I have also been involved in the fundraising efforts for Legendstar Capital’s new fund, and I have found that many LPs are highly concerned about investment strategies amid industry shifts.For Legendstar Capital, our enduring investment discipline has been to conduct continuous industry research, deepen our understanding, and hone our ability to identify opportunities; we avoid blindly following phenomenally hyped trends and ensure that our investments always remain anchored in the fundamentals of business.Early-stage investing and mid-to-late-stage investing have distinct characteristics. Mid-to-late-stage investments involve substantial capital; as long as there is a return, they are profitable. In contrast, early-stage investments hold little significance if the return multiple is insufficient. This makesWhen selecting targets, we place significant emphasis on the factor of “growth potential.”. Therefore, within the IVD sector, early-stage investors and mid-to-late-stage investors adopt different logics in selecting their benchmarking targets.

The IVD Industry Is a Cutthroat Arena: As we know, in the early days of China’s IVD market, there were hardly any domestic manufacturers. Hospitals mostly relied on manual or semi-automated methods, resulting in outdated testing technologies and significant operational errors. Later, higher-cost imported products were adopted, and foreign manufacturers once dominated the in vitro diagnostics market.

After the 1980s, import substitution began to emerge.. We observe that in 2017, the top five global manufacturers held a 55% market share, indicating a stable competitive landscape. In the Chinese market, the five major imported brands accounted for 36.8%, demonstrating that over the past three decades, under the theme of import substitution in the IVD sector,Domestic production has become the mainstream.However, it is also evident that the industry is highly fragmented, with more than 1,000 companies competing in a market valued at RMB 60 billion.

Therefore,The IVD market is a world of its own. In this world, anyone with a sword can roam the land.In the past, barriers to entry in this industry were relatively low; possessing a proprietary niche secret was sufficient to sustain a business for over a decade. This can be attributed to the following industry characteristics: low market concentration, high gross margins, heavy reliance on distributors, an entrenched existing landscape that is not easily disrupted, technology not being the primary driver of innovation, regional fragmentation, and significant differences in the operational attributes across hospitals of varying tiers.In summary, the IVD market can be characterized by two words: traditional. In four words: very traditional.

From the perspective of leading companies in sub-sectors, Mindray Medical, the industry leader, has a market capitalization of RMB 150 billion (noting that Mindray’s portfolio includes patient monitoring and other categories). The market capitalizations or valuations of leading enterprises in other sub-sectors are not yet on the same order of magnitude, indicating substantial room for organic growth. With the average price-to-earnings (P/E) ratio in the secondary market at 40x and low industry concentration, there is strong momentum for mergers and acquisitions. Furthermore, apart from the next-generation sequencing (NGS) segment, the valuation inversion between the primary and secondary markets is not significant across the overall in vitro diagnostics (IVD) industry. IVD companies with primary-market valuations around RMB 1 billion and revenues near RMB 100 million will be ideal candidates for listing on the STAR Market if they incorporate biological, intelligent, or automation attributes.

Let's discuss again.NGS: Why Has It Emerged as a Leader in the Oncology Sector?Within the NGS sector, unicorns have already emerged in the fields of NIPT-based prenatal screening and tumor companion diagnostics (including ctDNA early screening), such as Burning Rock Biotech, which was invested in by Legendstar Capital in 2014. In other tracks, such as consumer-grade genetic testing, CTCs, microbiomics, and genetic diseases, no particularly large enterprises have yet emerged.

Taking Tumors as an Example: A ReviewKey Boundary Conditions for the Rapid Development of This Sector: The maturation of NGS technology (with established benchmarks from overseas implementations), the characteristics of oncological diseases, the inflection point in sequencing costs, the concept of precision medicine, and the boost from loose capital conditions (significant capital influx between 2014 and 2018).

Among these factors, I believe the inherent characteristics of oncological diseases are the most critical. Due to the complexity of tumors, there is a strong demand among physicians for obtaining more information at the molecular level. Furthermore, given the high overall cost of cancer treatment, patients exhibit a strong willingness to pay for methods that can guide medication decisions. A further favorable catalyst has been the market launch of various targeted therapies in recent years, as conventional approaches have failed to meet the clinical need for personalized drug selection. It is precisely due to these combined characteristics that this previously non-existent sector has rapidly developed.

So, how to judge the investment value of an NGS company?

For example, in the oncology sector, at its peak, there were over a thousand NGS companies providing services around this field. I am looking into this area.When evaluating whether a company is worth investing in, the following are the key points I pay particular attention to:

First isCompliance.Frankly speaking, this is an emerging industry that has developed rapidly in recent years. Any nascent industry will undergo a period of regulatory ambiguity. However, with the issuance of the first batch of NGS oncology registration certificates, compliance has become a prerequisite for the survival of NGS companies. This includes obtaining registration certificates for test kits and accreditation for high-throughput sequencing laboratories issued by the National Clinical Laboratory Center (NCLC) under the National Health Commission.

Secondly,Revenue and corresponding sales expenses. The current situation is that the entire industry is burning cash; leading companies need to generate over RMB 500 million in revenue just to break even, while most non-leading companies may never achieve breakeven under their existing financial models.Whether an NGS company will have the opportunity to emerge victorious in the future depends on one formula:Pocket Depth (Financing Amount) + Hematopoietic Capacity (Revenue) - Degree of Blood Loss (Sales and Administrative Expenses Corresponding to Revenue),Revenue generated at the cost of high expense ratios is unsustainable.

Third,Proportion of In-Hospital Sales. When small and medium-sized hospitals have insufficient sample volumes, or during the early stages of a product’s lifecycle, tests that these hospitals are not yet capable of performing are typically outsourced to third-party providers. However, for high-gross-margin tests, mainstream large hospitals tend to build in-house capabilities and perform them internally. Furthermore, for companies, revenue generated from in-hospital testing contributes to corporate value rather than individual sales representatives’ personal value. Additionally, in-hospital revenue requires lower commercial investment and yields higher output per employee, making it a higher-quality revenue stream for enterprises.

Additionally,Product lines for regulatory approval and R&D investment,These figures represent the growth potential of the companies. To put it bluntly, due to the “abundant capital and rapid expansion” seen in previous years, valuations in this industry are generally inflated with a certain degree of bubble. The key question is: what will fill this bubble? Based on a reverse calculation using the current A-share market’s valuation rules for NGS (Next-Generation Sequencing) companies, those with annual revenues below RMB 300 million should not be valued at more than RMB 2 billion; otherwise, investors entering at the mid-to-late stages would stand no chance of making a profit.

What Factors Affect the Break-Even Point of Tumor NGS Companies? (Why Is the Entire Oncology NGS Industry Burning Cash?)

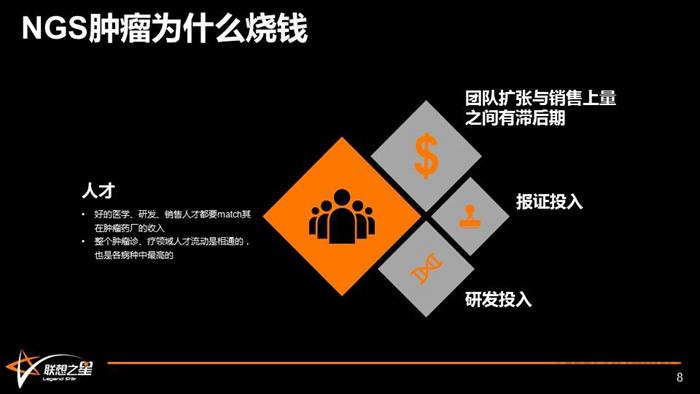

In fact, it is not surprising that this industry is highly capital-intensive, as the various costs associated with oncology products are inherently higher than those in other therapeutic areas.

First,Talent Costs:Top talent in medical affairs, R&D, and sales must be compensated in line with income levels at oncology pharmaceutical companies. Talent mobility within the oncology field is highly interconnected, representing the highest turnover rate among all therapeutic areas. In oncology drug sales, regional managers typically earn an annual salary starting at RMB 1 million, while directors earn between RMB 1.5 million and RMB 2 million. By contrast, regional managers for other therapeutic areas generally earn around RMB 700,000 to RMB 900,000. In medical affairs, director-level positions start at approximately RMB 1 million annually, and Chief Medical Officers (CMOs) earn between RMB 1.5 million and RMB 2 million. These figures represent standard compensation levels within the oncology pharmaceutical industry. Based on my financial modeling of a listed large-molecule oncology drug developer, a company may still incur losses even after achieving RMB 1 billion in sales revenue.

Next isThere is a lag between team expansion and sales growth.

Additionally, tens of millions ofCertificate Investment, and each case varies but amounts to at least tens of millions or even hundreds of millionsR&D Investment, which serves as a sustainable foundation for the company's future value.

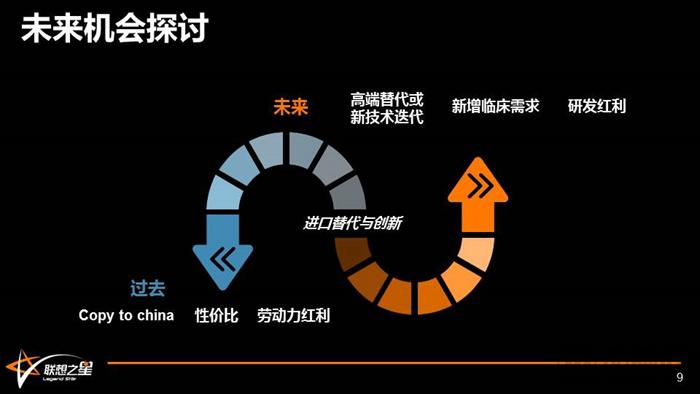

Let's Discuss FurtherFuture Investment Opportunities。

First,Import Substitution and InnovationIn terms of growth, the import substitution theme over the past three decades was primarily driven by micro-innovation, leveraging the demographic dividend to produce cost-effective products or those involving relatively simple replication. In the future, opportunities for straightforward import substitution will diminish (the top five multinational corporations account for 36.8% of the domestic market share). While there remains some room for import substitution in high-end segments, the driving force will shift to the benefits derived from the mobility of R&D personnel in foreign enterprises. Additionally, aroundNew Markets Addressing Unmet Clinical Needs Will Become the Primary Battleground for Startups, such as personalized oncology and China-specific implementation scenarios (primary care settings combined with Internet-based services).

Secondly,Investment Opportunities Centered on New Biomarkers or Emerging Technologies: In terms of new biomarkers, there are substantial unmet clinical needs in tumor-specific diagnostics, microbial detection, and the management of various chronic diseases. Regarding emerging technologies, microfluidic platforms still have significant room for growth, given their current level of commercialization and potential technological reserves. Additionally, domestic digital PCR products are on the verge of regulatory approval, and novel applications such as single-cell sequencing are highly anticipated.

In conclusion.

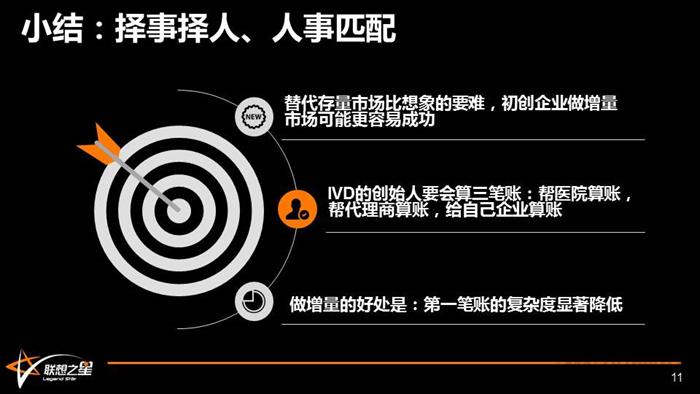

In the “competitive landscape” of IVD, replacing the existing stock market is much more difficult than imagined; startups may find it easier to succeed by targeting incremental markets.Founders of IVD companies must learn to calculate three sets of accounts: for hospitals, for distributors, and for their own enterprises.. If one of the three accounts is not calculated clearly, the company's development may fall short of expectations.

The most challenging aspect is calculating the hospital’s economics: Are the pain points perceived by entrepreneurs truly critical pain points, or merely minor irritants? This distinction directly influences the strength of their willingness to pay. For instance, we often hear founders claim how cumbersome a certain testing procedure used to be for hospitals and how their technology simplifies it. But was the original process really that burdensome? Might many tasks have become less troublesome simply through familiarity? Furthermore, if one specific inconvenience is resolved, could it trigger other complications? Hospitals are complex economic entities, even though many operate as non-profit organizations. Therefore, calculating the hospital’s economics is significantly more difficult than assessing the subsequent two categories of accounts. The advantage of targeting incremental markets is that the complexity of this first calculation is substantially reduced.

Therefore,IVD is a competitive arena; when selecting investment targets in this industry, we believe that the alignment between personnel and roles is paramount.

That concludes my sharing for today. I hope to have more opportunities to exchange ideas with you all. Thank you!