Bilinx Capital Identifies Five High-Potential Medical Device Investment Sectors in 2019

Proxima Capital

Investment Institutions in the Medical Technology Field

Editor’s Note: This article is republished from Qingtong Capital, with authorization granted to VCBeat.

On April 25, Qingtong Capital invited Yan Xiaoshen, Investment Director at Proxima Capital, to share insights on investment opportunities and emerging trends in the medical device sector. Below are the key highlights from Yan Xiaoshen’s presentation (images and content provided by Proxima Capital):

Status of the 5 Hottest Sectors

Chinese Medical Device Innovators Are Catching Up

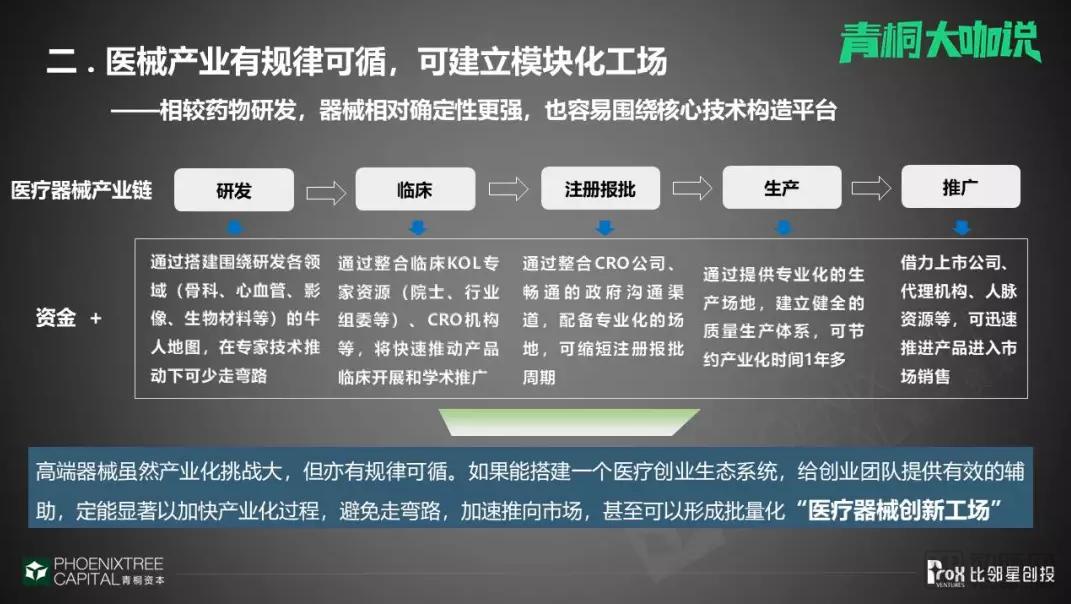

Modular Factory

Registrant System

Proxima Capital's Investment Strategy and Portfolio

Key Tracks in 2019

I previously worked in the medical device R&D industry and later joined the U.S. division of Boston Scientific. Five years later, I returned to China and joined Proxima Capital.

I chose to return to China because I recognized the immense market potential for medical devices domestically, coupled with the introduction of many favorable policies. Among these, the Marketing Authorization Holder (MAH) system is particularly crucial for aligning with international standards and driving the development of China’s medical device industry.

Currently, the medical device industry in China lags behind that of Europe and the United States. However, from a long-term perspective, the domestic market exhibits a clear growth trend. I have summarized the current status and trends of five hot sectors:

1. Surgical robots. Domestic surgical robot companies have flourished in recent years, with 4–5 companies already developing systems akin to the “da Vinci” surgical system. Other companies are focusing on specialty-specific robots, such as those for knee procedures, knee joint surgeries, and neurosurgery.

2. Artificial Organs. The demand for artificial organs in China is enormous, yet the supply remains severely inadequate. Consequently, numerous companies are engaged in the research and development of artificial heart pumps and various types of insulin pumps.

3. Neuromodulation. The neuromodulation market has developed rapidly overseas, while the Chinese market is gradually awakening, with applications predominantly in the treatment of epilepsy and Parkinson’s disease. In fact, neuromodulation can be applied to a broader range of fields, such as headache management and inflammation management.

4. Medical AI. This is a topic of significant public interest. Currently, there is considerable homogenization in AI-driven healthcare applications, with the majority focused on pulmonary nodules, pathology, ophthalmology, and cardiovascular diseases. Furthermore, critical issues such as clinical implementation, profitability, and the ability to genuinely address pain points and enhance efficiency warrant close attention.

5. Rapid minimally invasive transformation of cardiac surgery. The shift toward minimally invasive procedures has created numerous investment hotspots. Boston Scientific’s investment philosophy is to invest in technologies where minimally invasive approaches can serve as alternatives. Examples include minimally invasive interventions for valvular diseases, heart failure, mitral valve disorders, and most structural heart diseases, as well as surgical instruments designed for microscopic or endoscopic procedures.

A significant gap remains between the Chinese and U.S. medical device industries. In the U.S. market, the ratio of medical devices to pharmaceuticals stands at 1:1, with total industry output reaching $208.4 billion. The sector is highly concentrated among leading companies, which collectively invest over $10.4 billion in R&D. In contrast, China’s market size is RMB 370 billion, dominated by small and medium-sized enterprises. The ratio of medical devices to pharmaceuticals is only 0.33:1, and product updates are relatively slow.

Compared with new drugs, R&D investment in medical devices in China is relatively lagging. This is due to the dispersed distribution of device talent within the healthcare sector, conservative treatment approaches among physicians, insufficient innovation by clinicians, and relatively inadequate government funding.

However, in the long run, the Chinese market presents significant opportunities, with innovative enterprises rapidly catching up and the industrial foundation maturing.

In terms of talent, a large number of overseas returnees have come back to China to start businesses, and many forward-thinking professionals, such as physicians and academicians, have recognized promising technologies and initiated collaborations with enterprises.

From a technical perspective, as China’s precision machining technology has become increasingly mature and materials science has continued to advance, multinational corporations have cultivated a cohort of professionals in machining and material quality control by appointing local agents in China.

Capital has also identified opportunities herein, with growing attention directed toward the healthcare industry, particularly the medical device sector.

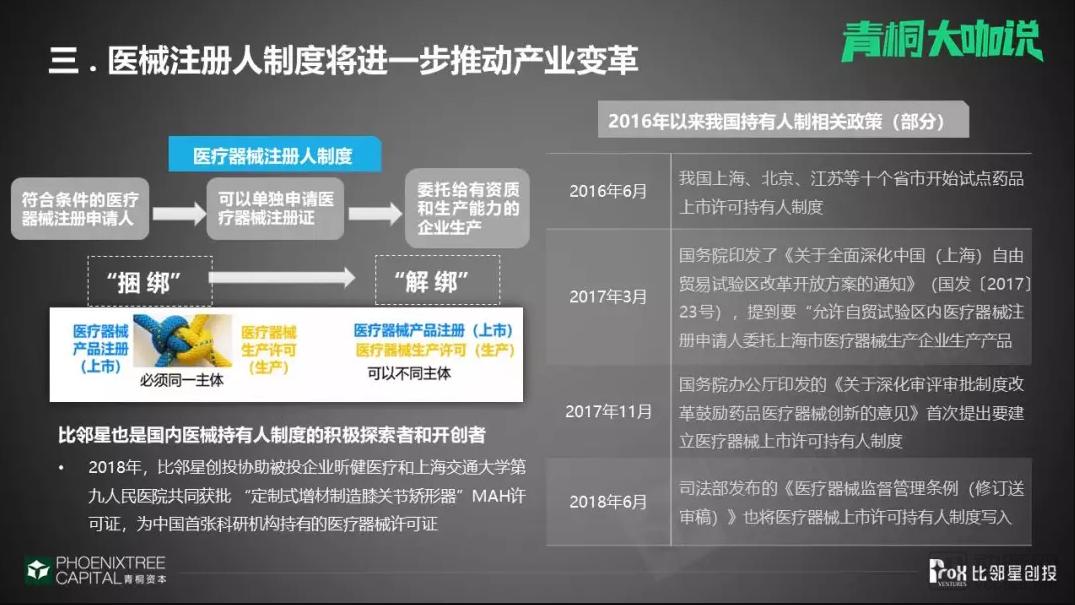

Furthermore, policy serves as a critical driving force. Initiatives such as major national science and technology projects and green channels facilitate accelerated reviews; for instance, the approval pathway for innovative medical devices can save healthcare companies more than six months. Additionally, the Medical Device Registrant System allows Class II medical device manufacturers to outsource production rather than building their own facilities. This represents a significant innovation, enabling companies to focus more effectively on research and development without the burden of heavy asset investment.

During this period, industrial clusters have emerged across various regions, with particularly notable developments in Suzhou, Shanghai, Beijing, Hangzhou, and Shenzhen. As of December 31, 2018, following the implementation of the Green Channel policy, 197 products had received special approval through innovative pathways, and 54 innovative medical enterprises had been approved for market listing. This progress has gradually broken foreign monopolies, and leading companies have emerged in fields such as cardiovascular care, in vitro diagnostics (IVD), medical imaging, neuromodulation, neurostimulation, and surgical robotics.

Compared with drug development, medical devices offer greater certainty and make it easier to build platforms around core technologies.

As the number of innovative enterprises continues to grow, the medical device industry chain has become relatively comprehensive, with companies engaged in research, development, and manufacturing at every stage.

One R&D model is the “Expert + Enterprise” approach, where physicians bring their ideas to relevant companies. A case in point is the tricuspid valve project developed through the collaboration between Proxima Capital’s portfolio company Ningbo Jian Shi and Changhai Hospital. Conversely, enterprises also proactively engage leading physicians, with top-tier KOLs, academicians, and committee members spearheading animal or clinical trials, while CRO firms provide supporting services to accelerate development.

Professional service agencies are available for the remaining stages of registration and approval, manufacturing, and promotion. This significantly reduces detours and encourages talented individuals with innovative ideas and technical expertise to engage in medical device innovation.

From a policy perspective, the benefit brought by the Medical Device Registrant System is that it has activated a large number of CDMO platforms. Producing Class II medical devices through CDMOs can better help enterprises reduce their burdens, allowing the “Foxconns” of the medical device industry to provide superior manufacturing services. However, the resulting drawback is that the investment threshold for Class II and lower-category medical devices will be significantly lowered.

From my perspective, the Two-Invoice System has not had a significant impact on innovative medical enterprises, as it primarily targets distributors and agents. The “4+7” volume-based procurement policy has already been implemented in the pharmaceutical sector, and I believe similar measures for medical consumables are imminent. Furthermore, I am more concerned about the Marketing Authorization Holder (MAH) system and certain Green Channel policies, which will have an impact on innovative enterprises.

Overall, I believe the Chinese medical device market is very promising, especially for small enterprises. In Europe and the United States, it is extremely difficult for small companies to compete with large corporations, as the latter devote substantial resources to specific clinical departments and have deeply entrenched stakeholder interests. Consequently, exits for small enterprises in those markets occur primarily through mergers and acquisitions.

In China, even highly active medical device companies still lack sufficient innovation; many products approved through innovative pathways are not produced by these Chinese giants. Innovative Chinese medical device manufacturers, such as Anhan and Qiming, can go public, which would be impossible in the United States.

The Chinese medical device market is in a prime window of opportunity; once Chinese innovative enterprises truly mature, they will generate a “big tree effect.”

Proxima Capital, established in 2016, is an industry-focused fund dedicated to the healthcare and wellness sector. We manage both RMB and USD funds, investing in projects ranging from the angel stage to the growth stage, with a primary focus on medical devices, in vitro diagnostics (IVD), and biopharmaceuticals.

For medical device investments, Proxima Capital primarily focuses on three major investment strategies and key areas:

1. Focus on significant, urgent, and unmet clinical needs, while avoiding ordinary products

We will invest in critical clinical areas with high patient volumes and urgent unmet needs, such as valvular heart disease and life support systems, as well as neurology, pulmonology, and urology and gastroenterology, where effective solutions are still lacking.

We focus on leading enterprises, such as those that have gained access to the innovation fast track, achieved significant innovations, or received support from major national special projects.

2. Principles that have been or are being validated in the European and American markets

This theory or the corresponding device principle has already been validated in the European and American markets, or is currently undergoing validation. For instance, it has obtained FDA clearance or is supported by large-scale clinical data; however, such validation is not yet available in China.

We have become increasingly hesitant to invest in traditional domestic substitution initiatives, as I believe the concept of domestic substitution is sometimes a pseudo-proposition. In reality, major Grade-A tertiary hospitals, particularly those with high-value services, still rely predominantly on imported medical devices, with domestic brands rarely making it into their procurement catalogs. Gaining entry into high-traffic Grade-A tertiary hospitals remains challenging and carries significant risks.

3. High-Value Consumables

High-value consumables, such as a heart valve priced at RMB 200,000 or a deep brain stimulation (DBS) system for neuromodulation priced at RMB 300,000, represent significant market segments. In China’s pharmaceutical sector, the “4+7” volume-based procurement program has already been implemented; however, I believe that similar centralized procurement for medical consumables is imminent. Consequently, high-value consumables still carry certain hedging risks. While low-price competition is likely to be curbed in the future, high-value consumables continue to offer substantial investment potential.

Guided by its three core investment strategies, Proxima Capital has established a relatively comprehensive industrial portfolio since its inception, covering the lungs, vascular system, digestive tract, orthopedics, biomaterials, next-generation sequencing (NGS), biotechnology and pharmaceuticals, psychological services, and athletic apparel. In its first fund, the firm invested in 17 healthcare companies, 14 of which were in the medical device sector.

In terms of medical devices, we have invested in multiple projects in the gastrointestinal field. For instance, Tangji Medical; comparable companies in the United States have already reached a valuation of $300 million. We have high expectations for Tangji Medical.

Furthermore, we also focus on the broader health and wellness industry, such as mental health and fitness. Therefore, we have invested in Yi Dian Ling, an online psychological services platform, and Particle Fever, a sports brand company.

In addition to investment, Proxima Capital has established six innovation hubs in Wuhan, Hangzhou, Zhengzhou, Chengdu, Wuxi, and Boston, nurturing numerous healthcare enterprises with the aim of collaboratively tackling 27 major disease areas.

There are numerous sub-sectors within the medical device industry. In my view, cardiology, neurointerventional procedures, and pulmonology warranted particular attention in 2019.

In the cardiac sector, cardiovascular companies have consistently commanded high valuations, but there are limited remaining opportunities in this space. Key attention should be directed toward heart valves, particularly mitral valves, where a significant number of new enterprises are expected to emerge due to the substantial market size. For stents, especially metallic stents and drug-coated balloons, I believe there is no favorable investment window. Bioresorbable stents remain under observation; having worked with bioresorbable stents in the United States, I found that clinical trials there yielded unsatisfactory results, leading to poor acceptance among physicians. It remains uncertain whether Chinese physicians will accept this technology.

In the field of neurointervention, I believe the scope extends beyond coils and thrombectomy stents. There are superior neurointerventional products available abroad, and domestic manufacturers have also begun to develop them.

In the pulmonary sector, I believe several high-quality medical device companies will also emerge. China has a massive population of patients with lung diseases, which distinguishes it from other countries. By integrating healthcare with clinical practice, I think domestic innovation in China has the potential to surpass that of the United States.