Centralized Pharmacy Model Emerges as Optimal Solution for the RMB 200-Billion Grassroots Pharmaceutical Market

Key Takeaways:

1. The implementation of “strengthening primary care” policies, such as tiered diagnosis and treatment, medical consortiums, multi-site practice, and family doctor contract services, has led to an increase in patient visits at primary healthcare institutions, thereby driving up medication demand.

2. Third-party tools such as laboratory testing, medical imaging, and AI have enhanced diagnostic and treatment capabilities at the primary care level, leading to greater recognition of the service capacity of primary healthcare institutions.

3. Adjustments to the National Essential Medicines List and preferential reimbursement rates under medical insurance guide patients back to primary care institutions from a payment perspective.

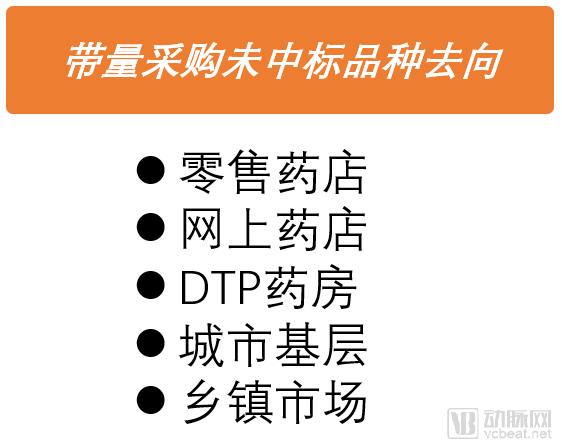

4. Varieties not selected in volume-based procurement actively expand into retail chain pharmacies and primary care terminal markets, driving market expansion.

5. Compared with urban community health service centers/stations, township health centers and village clinics have a lower degree of medication standardization, presenting greater opportunities.

Let us first examine a set of data: In 2018, the total sales across China’s three major pharmaceutical endpoints reached RMB 1.71 trillion. Among this, drug sales in public hospitals amounted to RMB 1.16 trillion, accounting for 67.4% of the total, although this proportion has been continuously declining. Drug sales through retail pharmacies and primary healthcare institutions were RMB 391.9 billion and RMB 167.1 billion, respectively, representing 22.9% and 9.7% of the total. Public hospitals remain the core channel for pharmaceutical sales.

As the data shows, the pharmaceutical market at public primary care terminals has been on a continuous rise since 2011. This period coincides with the implementation of a series of policies aimed at “strengthening primary care.” Guided by policies such as tiered diagnosis and treatment and medical consortia, primary healthcare institutions have received increasing attention, leading to enhanced service capabilities and a growth in patient visits, which has driven the sustained expansion of the primary care pharmaceutical market.

Looking ahead to the future of the grassroots pharmaceutical market, several favorable factors are at play: The tiered diagnosis and treatment system positions grassroots institutions as health “gatekeepers,” with patient visits expected to continue rising; third-party medical services, along with tools such as medical AI and big data, are enhancing diagnostic and treatment capabilities at the grassroots level, making it easier to retain patients; and pharmaceutical companies are increasingly investing in the grassroots market, strengthening the supply guarantee for essential medicines. With both demand and supply side factors converging, the sales volume of the grassroots pharmaceutical market is poised for further expansion.

Similar to other consumer goods, the pharmaceutical sales market is governed by “demand” and “supply.” When demand remains constant—meaning there are no significant changes in the disease spectrum or treatment pathways—the overall pharmaceutical sales market will not experience substantial fluctuations. The primary change lies in the structure of pharmaceutical end-points, with medication usage in tiered hospitals being gradually “diverted” to primary healthcare institutions and retail chain pharmacies.

Changes in Drug Supply and Demand at Primary Care Terminals

The rise of the primary-care terminal pharmaceutical market is primarily driven by policy. The most significant factor is the tiered diagnosis and treatment system, which aims to optimize the allocation of medical resources and foster effective division of labor and collaboration among healthcare institutions at different levels, thereby alleviating the current shortage of medical service supply. Specifically, common and chronic diseases that are easy to treat and have high incidence rates are managed at the primary care level, while difficult-to-treat specialized conditions are initially diagnosed at the primary level and then referred to higher-level hospitals with assistance. In this way, primary care institutions serve as health gatekeepers, implementing a model characterized by initial consultation at the primary level, two-way referrals, separate management of acute and chronic conditions, and coordinated care between upper- and lower-level institutions.

The state is promoting tiered diagnosis and treatment through policy measures, such as adjusting health insurance reimbursement rates and coverage, and reserving appointment slots at higher-level hospitals, to encourage initial consultations at primary care facilities. As basic medical security and critical illness insurance systems are strengthened, the healthcare needs of the grassroots population will be fully stimulated, leading to faster growth in demand for primary care services. Meanwhile, rural residents currently have extremely low levels of healthcare consumption; as the health insurance system continues to improve, their healthcare demands will be fully unleashed, resulting in increased patient visits to rural primary care institutions.

“The Situation Where the National Essential Medicines List Left Primary Care Facilities With No Drugs Available” Is Now a Thing of the Past; Adjustments to the List Have Empowered Primary Healthcare Institutions to Meet Patients’ Medication Needs. In October 2018, the new version of the National Essential Medicines List was released, increasing the number of listed varieties from the original 520 to 685, a rise of over 30%. The adjustments no longer merely safeguard “basic” needs; cost-effectiveness is no longer the primary consideration, with clinical value becoming a key criterion for inclusion. Particularly in the categories of chemical drugs and biological products, certain varieties—including monoclonal antibodies, advanced formulations, insulin analogs, and newly approved drugs—have been incorporated, thereby strengthening the drug supply guarantee capacity of primary healthcare institutions.

It is also worth noting the impact of volume-based procurement (VBP) on pharmaceuticals. First, regarding pricing: VBP establishes reimbursement prices under the medical insurance scheme. This means that regardless of whether a company participates in centralized procurement or wins the bid, it will ultimately be affected by the VBP-determined prices, leading to significant adjustments in drug prices. Second, concerning market share: VBP stipulates guaranteed purchase volumes, with winning bidders directly securing 60%–70% of the market share. Consequently, the addressable market for non-winning companies becomes very limited, making out-of-hospital channels and primary care markets key areas of focus for their non-winning products.

Compared with retail pharmacies, primary healthcare institutions hold greater advantages in public credibility, professional service capabilities, and medical insurance support. Urban community health service centers/stations are predominantly public-owned, backed by institutional credibility; physicians can directly diagnose conditions and prescribe medications, offering a superior service experience; primary healthcare institutions can utilize pooled fund payments, whereas pharmacies are limited to individual account card transactions. Although both parties benefit from the tiered diagnosis and treatment system and the separation of prescribing and dispensing, primary healthcare institutions demonstrate more pronounced advantages over retail chain pharmacies.

Furthermore, we observe that the policy includes a series of measures to “strengthen primary care,” such as increasing investment in equipment for primary healthcare institutions, encouraging private capital participation, and promoting the development of third-party medical services like laboratory testing. These initiatives will enhance the service capacity of primary healthcare institutions and help retain patients. Meanwhile, primary healthcare institutions are permitted to “retain surpluses” under their performance evaluation frameworks; such effective incentive mechanisms will stimulate the enthusiasm of primary healthcare professionals.

China has more than 2,850 county-level administrative divisions, 417,000 towns and townships, 662,200 villages, and 670,000 village clinics, with a township population of 674 million. Compared to the urban primary healthcare system, primary healthcare in towns and townships suffers from a more severe shortage of medical personnel and medicines. Many village doctors still rely on the “old three” diagnostic tools—stethoscopes, thermometers, and sphygmomanometers—which no longer meet patients’ actual needs. The backward level of diagnosis and treatment at the township and village primary care level forces patients to “migrate” to large hospitals. This patient outflow leads to declining incomes for village doctors and limited professional development, further dampening their motivation to improve clinical capabilities, thereby creating a vicious cycle.

Few organizations have focused on the rural pharmaceutical market. VCBeat’s observations reveal several key reasons: first, the overall scale of the rural market is small, resulting in a mismatch between investment and returns; second, rural healthcare institutions are geographically dispersed, with limited medication demand per individual health room or clinic; and third, inadequate infrastructure, such as pharmaceutical logistics, makes it difficult for large enterprises to reach these areas.

A county-level pharmaceutical distributor told VCBeat that markups on drugs are significant as they move from manufacturers to village clinics and other primary care facilities. Typically, more than three tiers of distributors are involved, ranging from provincial and municipal agents to county-level operators. County-level distribution enterprises generally engage in both wholesale and retail operations; they operate chain pharmacies and deliver medications to village clinics, leveraging their extensive networks that cover these grassroots facilities. Medication practices in village clinics exhibit low standardization, with limited attention paid to the latest clinical guidelines and diagnostic and treatment norms, resulting in slow updates. Furthermore, prescriptions are sometimes driven by economic incentives rather than clinical needs, and the practice of selling drugs in broken bulk (partial packages) is relatively common.

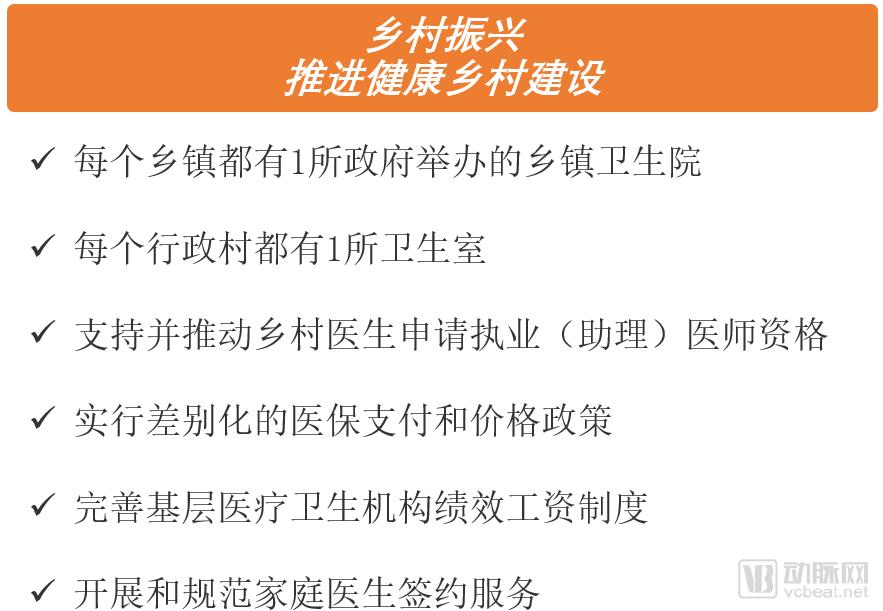

The “Rural Revitalization” strategy calls for strengthening the primary healthcare service system, with the basic goal of ensuring that each township has one government-run township health center, each administrative village has one clinic, and each township health center is staffed with general practitioners. It also supports the standardized construction and equipment upgrading of primary healthcare institutions in central and western regions.

Strengthen the workforce of village doctors by supporting and facilitating their applications for Licensed (Assistant) Physician qualifications. Fully establish a tiered diagnosis and treatment system, implementing differentiated medical insurance payment and pricing policies. Deepen comprehensive reforms in primary healthcare and improve the performance-based salary system for primary medical and health institutions. Develop and standardize family doctor contract services. These measures will further enhance primary healthcare service capabilities at the township level while promoting growth in the pharmaceutical market size.

The development of the grassroots pharmaceutical market in rural areas primarily proceeds from two aspects. First, it involves establishing pharmaceutical distribution infrastructure, such as commercial networks and logistics warehousing. Second, it focuses on empowering physicians by providing tools via SaaS systems, websites, and mobile apps to access cutting-edge information, academic education, and clinical medication guidance. Additionally, these tools assist physicians in creating health records for villagers and conducting rehabilitation follow-ups, thereby stimulating and fulfilling medication demand.

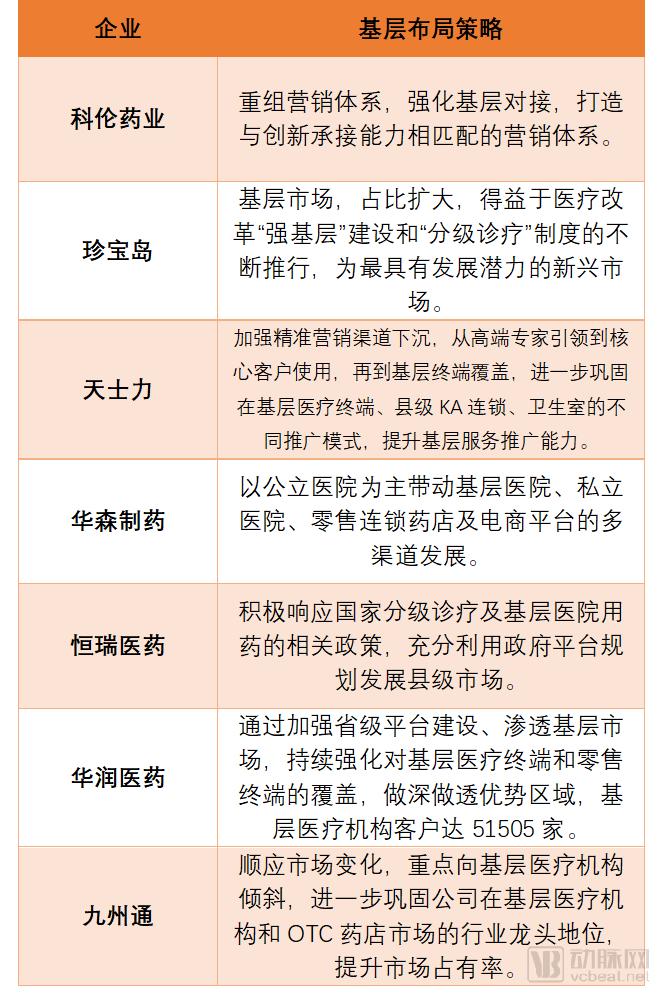

In the urban primary healthcare pharmaceutical market, foreign pharmaceutical companies such as Bayer, Pfizer, Sanofi, Novo Nordisk, and AstraZeneca hold a significant share. In contrast, in the township-level primary healthcare pharmaceutical market, domestic pharmaceutical companies such as Kelun Pharmaceutical, Wuzhou Pharmaceutical, Zhenbaodao Pharmaceutical, and Cisen Pharmaceutical dominate. Additionally, many other pharmaceutical companies are turning their attention to the primary healthcare sector. Below are selected statements from major listed pharmaceutical companies regarding their strategies for expanding into the primary healthcare market.

Strategies of Listed Pharmaceutical Companies for Grassroots Market Deployment

Data source: Pharmaceutical company annual reports

As can be seen, both industrial enterprises and distribution companies regard the primary care sector as a key focus for future volume growth. In comparison, distribution companies are more proactive in establishing their presence in the primary care market. This is because the tiered hospital market has been significantly impacted by volume-based procurement (VBP), where distribution and delivery arrangements are largely contract-based and remain relatively stable. Therefore, actively expanding into the primary care market is essential for achieving additional growth.

From the perspective of specific drug categories, PwC’s report on new retail for prescription drugs points out that there is motivation to enter the retail market for medications treating cardiovascular and cerebrovascular diseases, diabetes, and chronic respiratory diseases. Specifically, originator products whose patents have expired face competition from generics and pressure from policies restricting or capping usage, creating a need to expand into out-of-hospital channels.

Taking diabetes medications as an example, according to the National Guidelines for the Prevention and Management of Diabetes in Primary Care, primary healthcare institutions should be equipped with the following five major classes of essential glucose-lowering drugs: metformin, insulin secretagogues, alpha-glucosidase inhibitors, thiazolidinediones (TZDs), and insulin. This represents a significant positive development for relevant manufacturers, enabling them to align with policy directions and strategically position themselves in the primary care market.

Overall, household common medicines, chronic disease medications, adjuvant therapies, and drugs that failed to win bids in volume-based procurement (VBP) will focus on expanding into the primary care market. Chronic disease management, aligned with the “rehabilitation at the primary care level” initiative, can leverage expert consultations, free clinics, and internet healthcare to deliver high-quality medical and pharmaceutical services to grassroots levels, thereby driving drug sales. In contrast, VBP non-winning products will primarily target the out-of-hospital market, with a strategic emphasis on retail chain pharmacies.

As previously mentioned, the small and fragmented medication demand in the primary care market poses challenges for pharmaceutical companies seeking to expand into this sector. The solution lies in the central pharmacy model, whereby a central pharmacy is established within a region to supply medications to primary healthcare institutions and retail chain pharmacies, while also meeting patient needs for services such as self-pickup and home delivery.

Shanghai Pharmaceuticals is a key case study in the development of central pharmacies. Its subsidiary, Shanghai Pharma Cloud Health, operates the “Yiyao Cloud Pharmacy” business. By establishing central pharmacies and integrating with electronic prescriptions, it provides home delivery of medications to users. Currently, central pharmacies have been set up in Shanghai, Guangzhou, and Zhenjiang, enabling 24/7 service responsiveness and delivery within 150 kilometers in under six hours.

According to the annual report, by the end of 2018, Shanghai Pharmaceuticals Cloud Health (SPH Cloud Health) had facilitated the electronic circulation of 8.4887 million prescriptions nationwide, marking explosive growth. The company had integrated with 340 medical institutions and served over 3.6 million patients. Notably, the prescription volume for Shanghai’s community-based extended prescription program doubled, achieving a market share of nearly 70% and covering 160 of the 242 community hospitals in Shanghai.

Some enterprises are also actively leveraging “Internet + Healthcare” solutions to empower grassroots healthcare providers. For instance, Akang Health offers supply chain upgrade services ranging from “product supply” to “disease-specific solutions,” along with online-to-offline integrated cloud pharmacies. By integrating orders and logistics, restructuring the pharmaceutical supply chain, and significantly reducing intermediate links, these initiatives can effectively address the challenges of medication shortages and high medical costs at the grassroots level.

We have identified the following enterprises that provide “cloud pharmacy” or central pharmacy services to urban and township grassroots levels:

Source: VCBeat Database, Corporate Official Websites

As can be seen from the above, “Cloud Pharmacies” generally fall into two categories: one type is backed by pharmaceutical distribution companies, such as Shanghai Pharma Cloud Health, A-Kang Health, and Sinopharm Online; the other type consists of information platforms, including Medlinker and Zhuojian Technology. Regardless of whether they are backed by distributors or operate as information platforms, these entities address the shortage of medical resources and medications at the primary care level by sharing drug variety information through digital platforms to meet the medication needs of grassroots healthcare facilities.

Regarding “cloud pharmacy” information platforms, a research report by Guosheng Securities points out that robust IT infrastructure is a prerequisite for the “outflow of prescriptions”: 1) Prescription circulation platforms enable interconnectivity among hospital information systems, medical prescription circulation information platforms, cloud pharmacy platforms, community pharmacies, and distribution systems, thereby ensuring proper collection, review, dispensing, verification, and storage of electronic prescriptions; 2) Medical insurance review and settlement platforms facilitate information sharing between healthcare institutions’ prescriptions and drug retail data, promoting intelligent medical insurance audits and “one-stop” settlement. These developments have improved the efficiency of medical resource utilization and created incremental market opportunities for enterprises.

Amid the backdrop of tiered diagnosis and treatment, volume-based procurement (VBP), and the outflow of prescriptions from hospitals, the service capabilities of primary healthcare institutions have continued to improve. Patients are “returning” to these grassroots facilities, driving up demand for medications. Coupled with the flow of VBP-listed drugs into the primary care market, this sector has become a highly coveted target for pharmaceutical companies. Meanwhile, the “Internet + Healthcare” model has introduced new applications such as internet hospitals, prescription-sharing platforms, and cloud pharmacies, further boosting the primary care market. With growth on both the supply and demand sides, the scale of the primary care pharmaceutical market is poised for further expansion in the future.