Deloitte Report: Innovative Drugs Gain Spotlight as Pharma and Biotech Firms Show Sustained Activity in Primary and Secondary Capital Markets

Excerpted from Deloitte’s report: “Capital Markets Review and Outlook: The Pharmaceutical and Biotechnology Industry Driven by Innovative Drugs”

Since 2018, pharmaceutical and biotechnology companies have attracted significant attention in the capital markets, primarily for three reasons:

First, in terms of the Chinese and U.S. securities markets (U.S. stocks, A-shares, and Hong Kong stocks), both the number of initial public offerings (IPOs) and the total amount of capital raised in the pharmaceutical and biotechnology sectors reached a ten-year high in 2018, with the momentum continuing unabated since the beginning of 2019.

Secondly, in early 2018, the Hong Kong Stock Exchange (HKEX) introduced new regulations permitting pre-revenue or unprofitable biotechnology companies to list in Hong Kong. This move, together with other policy initiatives, constituted the most significant reform of the HKEX in two decades. A series of biotechnology companies engaged in innovative drug R&D were able to list on the HKEX, and the Biotech Board became the first sector on the HKEX Main Board to carry an industry-specific suffix. Coincidentally, at the end of 2018, the STAR Market was established on the Shanghai Stock Exchange with a pilot registration-based IPO system. By implementing differentiated arrangements regarding profitability status and shareholding structures, the STAR Market prioritized encouraging enterprises in six key sectors, including biopharmaceuticals, to list, thereby providing unprofitable or pre-revenue biotech enterprises with a more diversified financing channel.

Finally, since 2018, the announcement of a series of mega-mergers and acquisitions, such as Takeda Pharmaceutical’s acquisition of Shire and Bristol Myers Squibb’s (BMS) acquisition of Celgene, has continuously reshaped the M&A rankings in the pharmaceutical and biotechnology sectors. Additionally, as a number of biotechnology companies have achieved major breakthroughs in oncology, rare diseases, gene therapy, and other fields, M&A activity in the pharmaceutical and biotechnology industries has entered a period of heightened vigor.

Against this backdrop, we review the capital market performance of the pharmaceutical and biotechnology sectors over the recent period and provide an outlook based on industry drivers. In the near term, investment and financing activities in the pharmaceutical and biotechnology sectors are expected to remain robust, with further growth anticipated through support from the Hong Kong Stock Exchange’s Biotech Board and the Shanghai Stock Exchange’s STAR Market. The M&A market will also continue to be active, driven by pharmaceutical companies’ demand for innovative drugs. Meanwhile, we will observe three key trends:

First, First-in-class (FIC) innovative drugs continue to attract attention from the capital market; FIC drug developers that can effectively reduce R&D risks and maintain global market exclusivity will be highly favored.

Second, specialty drugs, orphan drugs, biologics, and oncology therapies within the innovative drug sector will continue to be hotspots;

Third, diversified collaborations between emerging biotechnology companies and large pharmaceutical firms will give rise to outstanding innovative drug enterprises that make their mark in the capital markets.

I. Performance of Pharmaceutical and Biotechnology Companies in the Securities Market

1. Continued Growth in IPOs of Pharmaceutical and Biotechnology Companies

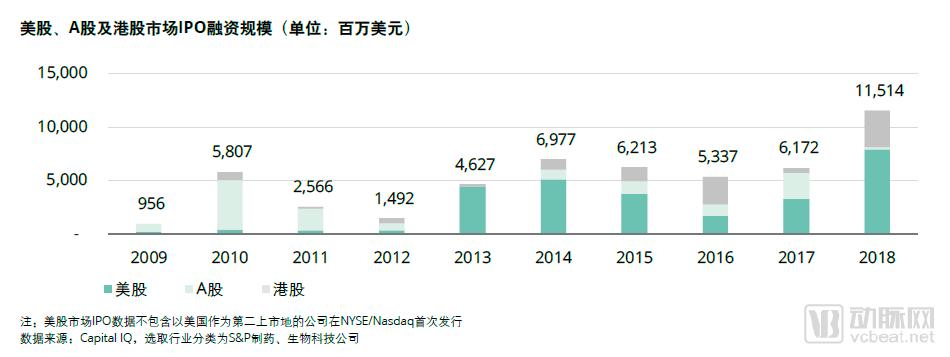

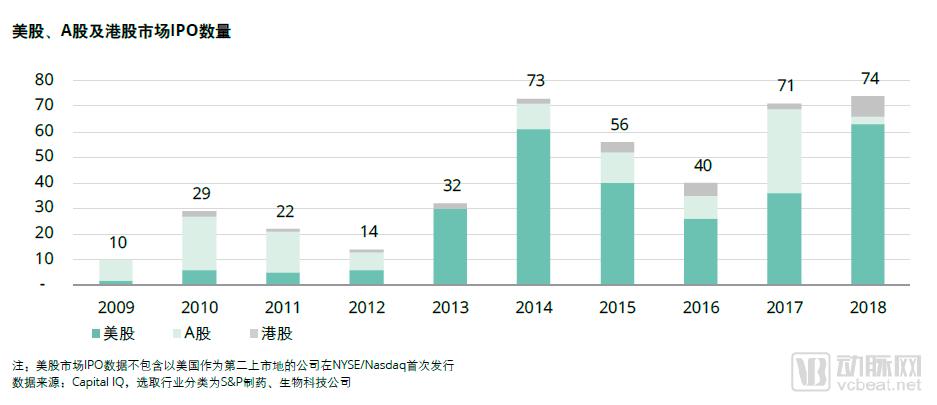

Whether measured by the number of deals or total proceeds, 2018 was a landmark year for initial public offerings (IPOs) in the global pharmaceutical and biotechnology sectors. Based on data from the U.S., A-share, and Hong Kong stock markets, the total capital raised through IPOs in these industries reached $11.5 billion in 2018, with 74 companies going public, both figures hitting ten-year highs.

Over the past decade, IPOs in the U.S. pharmaceutical and biotechnology sectors have shown an overall upward trend amidst fluctuations. As the center of the global financial market, the United States holds a prominent position in this field in terms of both the scale and number of financings.

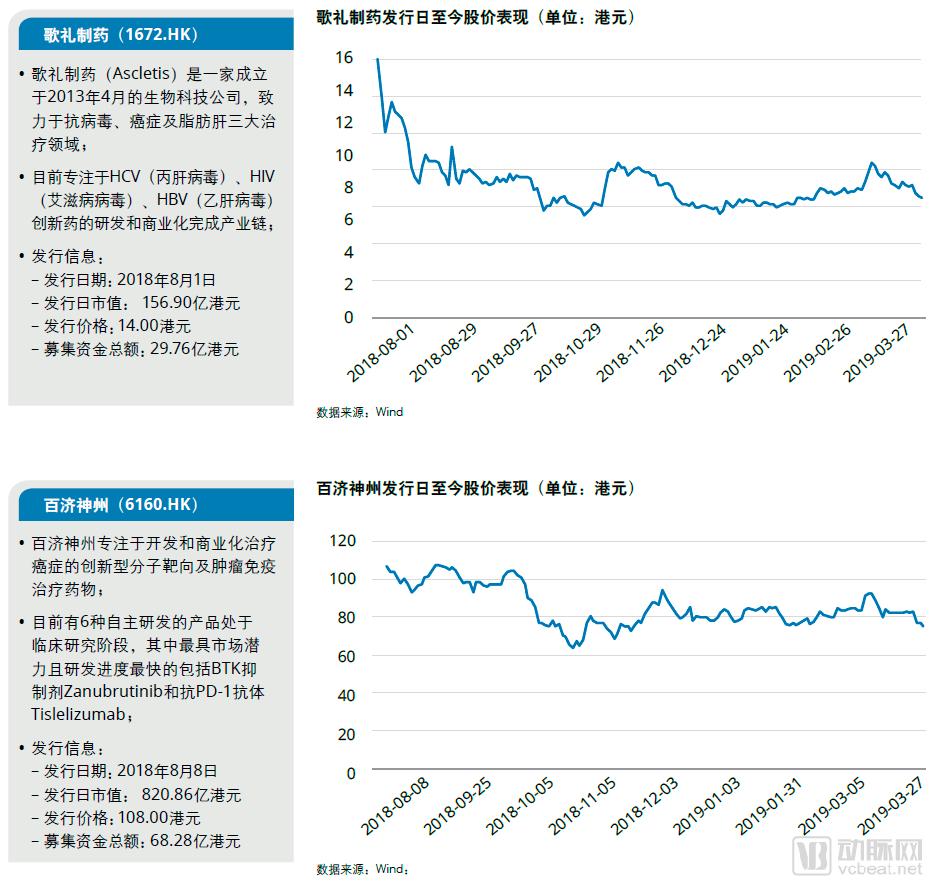

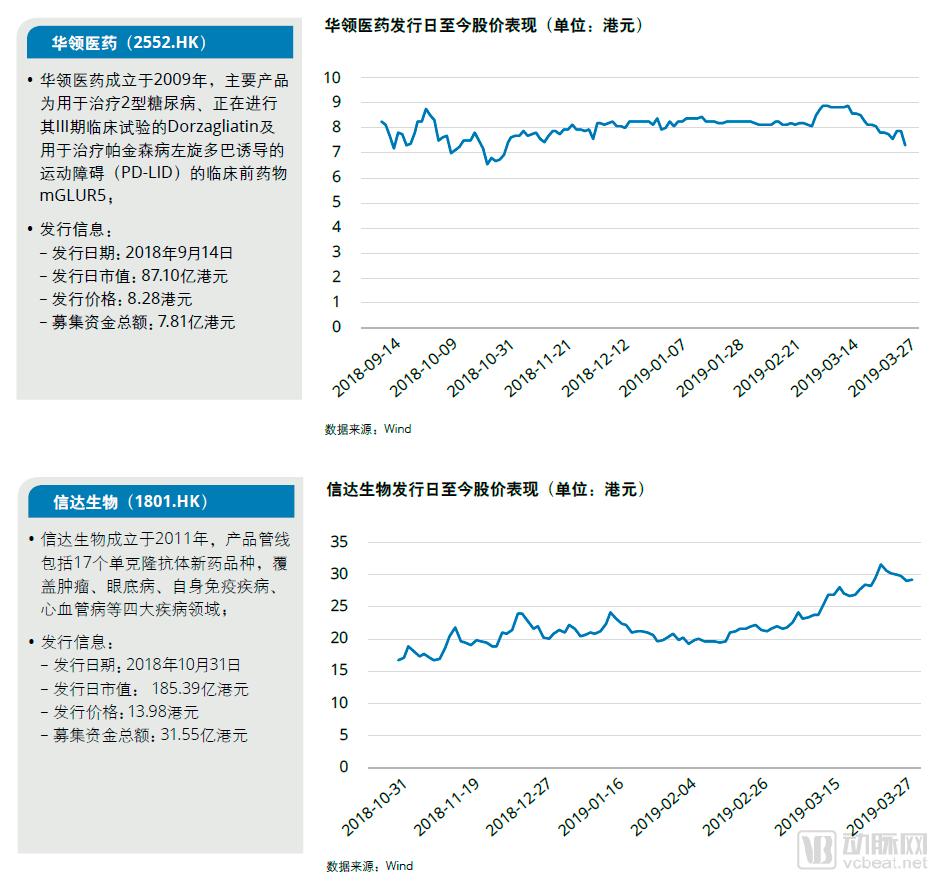

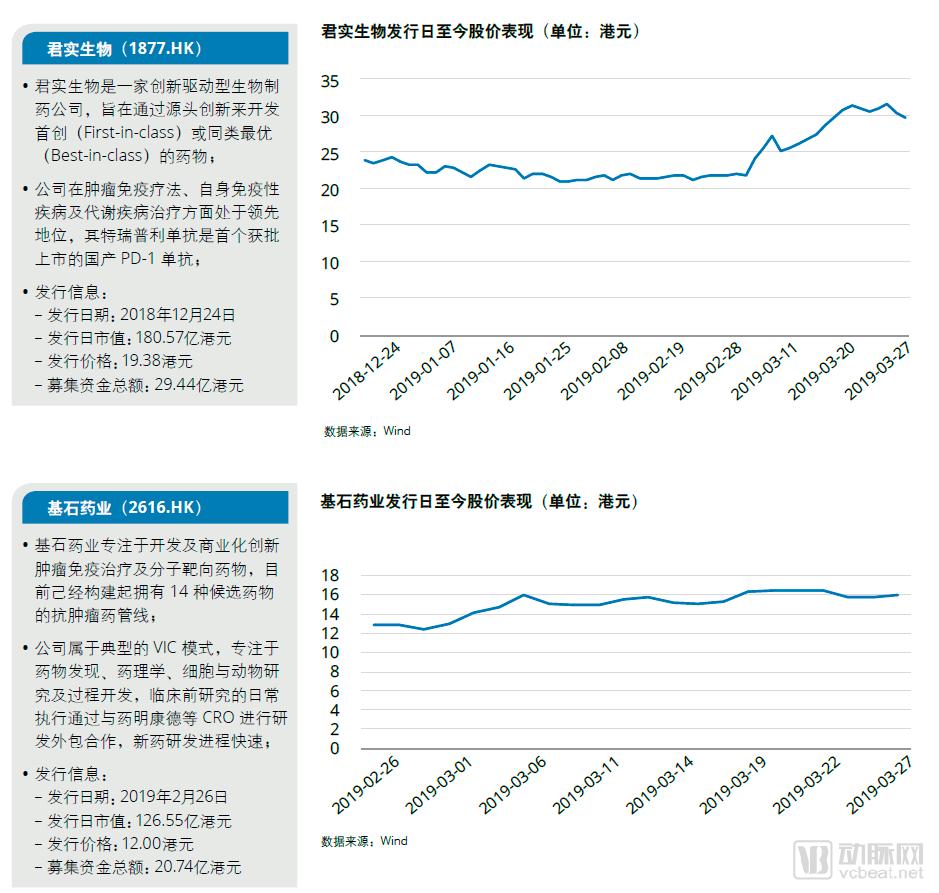

The Hong Kong market is one of the most attractive markets in Asia for global investors and serves as a vital link connecting mainland China’s capital markets with global capital markets. Over the past decade, Hong Kong-listed stocks have played a significant role in initial public offerings (IPOs) within the global pharmaceutical and biotechnology sectors. In 2018, the IPO performance of pharmaceutical and biotechnology companies on the Hong Kong stock market was particularly impressive, with eight companies completing their IPOs, surpassing 2017 figures both in number and total proceeds. In early 2018, the Hong Kong Stock Exchange introduced new regulations allowing pre-revenue or unprofitable biotechnology companies to list in Hong Kong. Throughout 2018, five companies successfully listed on the Hong Kong stock market under these new rules.

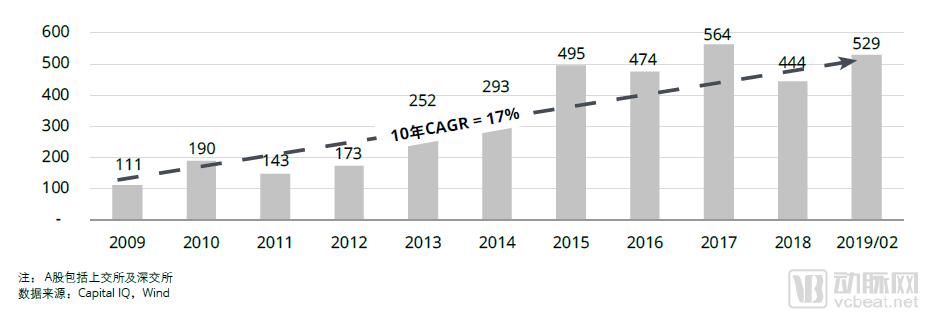

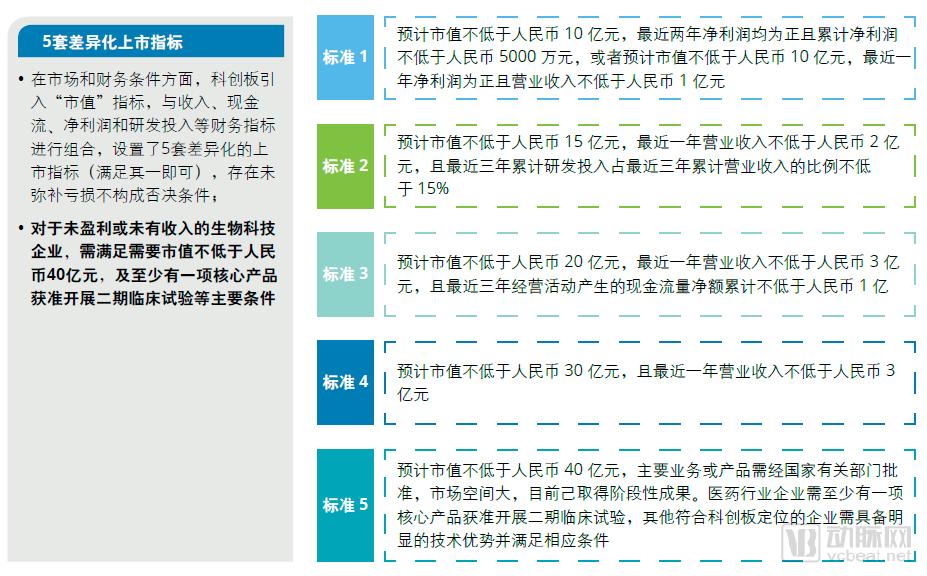

IPO performance in the pharmaceutical and biotechnology sectors of China’s A-share market has remained volatile over the past decade. The year 2017 witnessed a surge in biomedical IPOs, with 33 companies completing their listings. In contrast, tightened IPO regulations in 2018 resulted in only three pharmaceutical and biotech firms going public. Significant progress has been made in “hard-tech” innovations within China’s pharmaceutical and biotechnology industries. Historically, the technological attributes of this sector were not fully reflected in the A-share market; however, this trend is expected to be fundamentally reversed with the emergence of the STAR Market. The launch of the STAR Market will drive a revaluation of the industry and usher in a prosperous cycle for new listings.

The growth in IPOs among pharmaceutical and biotechnology companies indicates strong capital interest in this sector; a smooth IPO channel has become an important financing option for these enterprises.

2. The Total Market Capitalization of the Pharmaceutical and Biotechnology Sector Continues to Rise

As of the end of February 2019, the market capitalization of the biopharmaceutical sector in the U.S. stock market accounted for 9.9% of the total U.S. equity market capitalization, while the corresponding figures for A-shares and Hong Kong stocks were 6.7% and 7.9%, respectively. The scale of the U.S. biopharmaceutical sector far exceeds that of the A-share and Hong Kong stock markets.

Over the past decade, the market capitalizations of biopharmaceutical companies in the U.S., A-share, and Hong Kong stock markets have all shown a trend of rapid growth, with the growth rates in the A-share and Hong Kong markets surpassing that of the U.S. market.

3. The Launch of Hong Kong’s Biotech Board Encourages Biotechnology Companies to Go Public

On April 30, 2018, the Hong Kong Stock Exchange’s new listing rules came into effect, adding two new chapters to the Main Board Listing Rules to allow pre-revenue or unprofitable biotechnology companies to list in Hong Kong. This new policy not only provides a more attractive financing platform for biotech companies but also offers their investors an earlier exit channel through public listings in the Hong Kong capital market.

4. The establishment of the STAR Market will benefit biotechnology companies

In late 2018, the STAR Market was established on the Shanghai Stock Exchange as a pilot for the registration-based IPO system. By implementing differentiated arrangements in areas such as profitability requirements and shareholding structures, the STAR Market has significantly enhanced its inclusiveness and adaptability toward technology-driven innovative enterprises. Adjustments to the issuance mechanism and listing thresholds of the STAR Market not only provide more high-quality tech-innovation companies with opportunities to raise capital through public listings—thereby supporting their growth—but also position it as another key listing venue for biotechnology firms, following NASDAQ and the Hong Kong Stock Exchange’s Chapter 18A (Biotech Board). Meanwhile, it offers private equity (PE) and venture capital (VC) investors richer exit channels.

5. Biotech companies engaged in innovative drug R&D, such as Loxo, have attracted significant attention

In recent times, biotechnology companies engaged in innovative drug research and development (R&D) that have achieved significant progress in both R&D and commercialization, such as Loxo Oncology, have attracted considerable attention from the capital markets. Loxo Oncology is a biotechnology company founded in 2013, primarily focused on developing genome-defined precision oncology therapies. In late December 2017, Loxo submitted a marketing application for LOXO-101 to the U.S. Food and Drug Administration (FDA). In May 2018, the FDA accepted the New Drug Application (NDA) for LOXO-101 and granted it Priority Review designation. The drug was officially approved for marketing in November 2018. Following the completion of Phase II clinical trials, Loxo’s stock price rose with fluctuations, driven by market expectations. On January 7, 2019, Eli Lilly announced it would acquire Loxo in an all-cash transaction at $235 per share, with a total deal value of $8 billion.

For R&D-focused biotech companies that do not yet have any commercialized products, investors are still willing to assign high valuations despite the likelihood of prolonged unprofitability, driven by strong sales expectations for their pipeline candidates post-launch. Their leading R&D capabilities in certain niche segments also make them attractive acquisition targets for large pharmaceutical companies.

Judging from the stock price performance of emerging biotechnology companies in the United States, Phase II and Phase III clinical trials are key time points that drive valuation disparities. As certain clinical data (safety/efficacy) for innovative drugs have already been disclosed, investors hold optimistic expectations regarding the future market potential and approval likelihood of these new drugs, thereby driving valuations upward.

6. Core Innovative Drug Products Drive Major Performance Growth

Historically, there have been numerous cases similar to that of Loxo. Amgen, which went public on the U.S. stock market in 1984, serves as a prime example. Prior to the launch of Neulasta in 2002, the company’s financial performance remained relatively stagnant. However, driven by positive expectations stemming from Neulasta’s successful completion of Phase III clinical trials, Amgen’s market capitalization trended upward with fluctuations between 1998 and 2002. Following its commercial launch, Neulasta’s performance met investor expectations, leading to long-term stock price stability. As sales of the new drug rapidly scaled up, the company’s earnings per share (EPS) improved, resulting in a downward trend in its P/E multiple.

Amgen’s core products, pegfilgrastim (Neulasta) and denosumab (Prolia/Xgeva), were approved by the U.S. FDA in January 2002 and June 2010, respectively. Based on their development timelines and actual sales performance, both drugs experienced rapid volume growth after launch and maintained consistently high annual sales levels. In 2017, they generated substantial revenues of $4.53 billion and $3.55 billion for the company, respectively.

7. Capital Markets Give Full Attention to Innovative Drug Companies

In early 2013, AbbVie Inc., spun off from the innovative pharmaceutical division of Abbott Laboratories, successfully went public. Following the spin-off, the new Abbott retained its nutrition and medical diagnostics businesses.

Abbott retained its generics and off-patent drug business, while AbbVie took nearly all patented medicines, including blockbuster products such as Humira, Niaspan, Creon, and Tricor. Following the spin-off from Abbott, AbbVie focused on innovative drug R&D, rapidly elevating its R&D investment to levels comparable with industry leaders within a short period. The company also addressed gaps in R&D efficiency through collaborative research and development. The separation of Abbott’s innovative pharmaceutical business into two distinct entities better aligned with the diverse investment preferences of investors.

After overtaking Plavix in 2012, Humira topped global sales for six consecutive years, generating substantial revenue for the company. Viekira, the hepatitis C combination therapy co-developed by AbbVie and Enanta, was successfully launched in 2014, significantly boosting investor confidence in the company. By the end of 2014, AbbVie’s capital market performance continued to strengthen, with its price-to-earnings ratio reaching 53x. In the third year following its spin-off, AbbVie’s market capitalization had already surpassed the total market value of Abbott Laboratories prior to the split. Over the past seven years, AbbVie’s compound annual growth rate (CAGR) in market capitalization reached 16%, delivering significant returns to shareholders.

In the securities market, investors are willing to assign high valuations to innovative drug companies, which in turn have delivered substantial returns. Behind this trend lies the fact that innovative drugs—particularly first-in-class therapies—generate robust profits for companies by leveraging advantages such as limited competition and minimal pricing pressure during their post-launch exclusivity periods, a level of profitability that generic drugs or Me-too/Me-better agents struggle to match.

II. Three Major M&A Transactions Occurred in Q1 2019

1. Active M&A Transactions in the Pharmaceutical and Biotechnology Industries

Overall, global M&A transactions in the pharmaceutical and biotechnology industries have maintained an upward trend amid fluctuations over the past decade.

M&A activity in the pharmaceutical and biotechnology sectors is expected to further increase in 2019, exemplified by Eli Lilly’s $8 billion acquisition of Loxo Oncology. The primary drivers behind this trend include pharmaceutical companies’ needs for structural and strategic adjustments, as well as the influence of media coverage. Expanding product portfolios, completing value chain integration, and further consolidating market position remain the key motivations for mergers and acquisitions.

In January 2019, BMS announced its acquisition of the biotechnology company Celgene for $74 billion, marking the second-largest merger and acquisition (M&A) deal in the history of the biopharmaceutical industry, surpassed only by the Pfizer/Warner-Lambert merger in 1999. In February of the same year, Roche announced that it had signed an agreement to acquire Spark Therapeutics, a leader in gene therapy, for $4.3 billion. The frequent M&A activities since the beginning of the year drove the total transaction value in the first two months of 2019 to 57% of the full-year total for 2018.

2. Mergers and Acquisitions of Biotech Companies by Large Pharmaceutical Firms Become the Primary Driver of the M&A Market

Among the top ten mergers and acquisitions (M&A) deals in the global pharmaceutical and biotechnology industry over the past five years, apart from Teva, the Israeli generic drug giant, acquiring Allergan’s generic drug business, and Pfizer acquiring Hospira, which specializes in biosimilars, large-scale M&A transactions have largely concentrated on new drug research and development. Drivers behind these M&A activities include acquiring new products to achieve product diversification and expanding

Business coverage expansion, deepening business globalization, and entering new business areas, etc.

3. Large pharmaceutical companies enhance innovation capabilities through frequent mergers and acquisitions

In recent years, with the continued acceleration of biosimilar growth, pharmaceutical companies will inevitably face a decline in annual drug revenue after their exclusivity periods expire.

Amid the broader context of slowing growth in pharmaceutical expenditures, large pharmaceutical companies have been compelled to transform their “price-hike-driven” performance growth models. Drug development is characterized by long cycles, high risks, and substantial, long-term capital investment requirements, whereas smaller biotechnology firms or emerging biopharmaceutical companies are distinguished by their ability to deliver innovative products or technologies. In this ecosystem, frequent mergers and acquisitions by pharmaceutical companies have become a prevailing trend.

On January 3, 2019, BMS and Celgene jointly announced that they had reached an acquisition agreement, under which BMS would acquire Celgene for a total consideration of $74 billion (corresponding to an enterprise value of $89.5 billion), marking the largest M&A transaction in recent years.

On January 7, 2019, Eli Lilly announced that it would acquire Loxo Oncology, a biopharmaceutical company primarily engaged in the research and development of genomically defined precision cancer medicines, for a total transaction value of $8 billion.

On February 25, 2019, Roche Holding announced the acquisition of Spark Therapeutics, a leader in gene therapy, for $4.3 billion.