Deloitte Report: Orphan Drugs, Oncology Therapies, and First-in-Class Innovations Gain Prominence Amid Evolving Capital Markets

Excerpted from Deloitte’s report: “Capital Market Review and Outlook: The Pharmaceutical and Biotechnology Industry Driven by Innovative Drugs”

Building on the previous discussion, as more companies list on the Hong Kong Stock Exchange’s biotechnology sector and an investor base familiar with and preferring biotech firms becomes established, the Hong Kong biotechnology market will mature further. The Hong Kong market is expected to reach parity with the U.S. stock market. Coupled with the already mature U.S. equity market and the established STAR Market in China’s A-shares, global financing and investment activities in the pharmaceutical and biotechnology sectors will remain robust.

In the realm of mergers and acquisitions (M&A), large pharmaceutical companies have consistently needed to refresh their product pipelines to counteract the adverse effects of price reductions and patent cliffs. Furthermore, large pharmaceutical firms are generally more adept than R&D-focused biotechnology companies at navigating regulatory requirements and managing commercialization during the late stages of new drug development and post-launch, thereby securing substantial commercial returns. Consequently, M&A activity driven primarily by the acquisition of innovative drugs under patent protection will remain robust.

During this process, we can observe the following trends:

1. First-in-class new drugs continue to attract attention from the capital market; first-in-class new drugs that can effectively reduce R&D risks and maintain market exclusivity will be highly favored;

2. Special drugs, orphan drugs, biologics, and oncology therapies among new drugs will continue to be hotspots;

3. Diversified collaborations between large multinational biopharmaceutical companies and emerging biopharmaceutical firms will give rise to new high-quality enterprises that gain prominence in the capital markets;

4. Innovative drugs are entering an era of globalization, with biotech companies tending to rapidly launch multi-center clinical trials worldwide after securing global development rights, in order to capture larger markets upon drug approval.

In the field of innovative drugs, concepts such as First-in-class, Me-better, and Me-too are frequently mentioned. Strictly speaking, these terms are not precise definitions, but they vividly label innovative drugs, helping people grasp several key characteristics of a given drug; hence, they are widely used.

Unlike "me-better" and "me-too" new drugs, first-in-class drugs represent significant breakthroughs in mechanisms of action, indications, and molecular entities. Comparable categories include New Molecular Entities (NMEs) and New Chemical Entities (NCEs) as described under Section 505(b)(1) of the Federal Food, Drug, and Cosmetic Act (FDCA) for FDA new drug approvals. First-in-class drugs offer substantial potential revenue for companies, face less competition, encounter lower price-reduction pressures from government, public opinion, and supply-demand dynamics, and will continue to attract attention from the capital markets.

First-in-class new drugs are often global innovations, generating substantial returns for companies through the global market and attracting attention from global capital markets. Their primary risks stem from prolonged development timelines, significant R&D investments, and high development uncertainty. Consequently, companies that can effectively shorten development cycles, reduce R&D costs, or mitigate development risks through technological or business model innovations will garner significant attention.

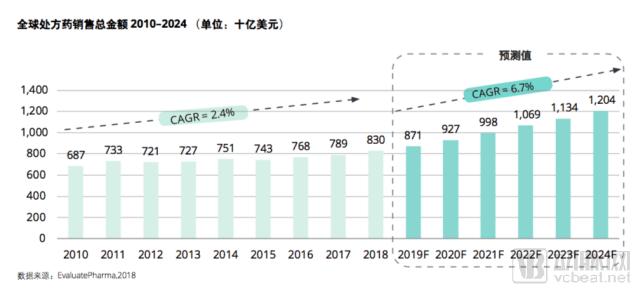

Global prescription drug sales reached $830 billion in 2018 and are projected to rise to $1.2 trillion by 2024, representing a robust compound annual growth rate (CAGR) of 6.7%. Notably, the CAGR from 2010 to 2018 was only 2.9%, indicating relatively modest growth. The projected CAGR for 2019–2024 marks a more than twofold increase compared to the previous period.1; Innovative drugs that address current critical needs and are brought to market will become a key driver of global pharmaceutical spending growth.

Particularly in China, drug procurement reforms aim to control overall pharmaceutical expenditure. The National Reimbursement Drug List (NRDL) underwent its most recent update in 2017, and the inclusion of innovative drugs in the list is expected to drive significant performance growth for innovative pharmaceutical companies. However, due to the “4+7” volume-based procurement reform, manufacturers of generic drugs (and even me-too new drugs) will face intensified competition, with their growth rates projected to slow down compared to previous periods.

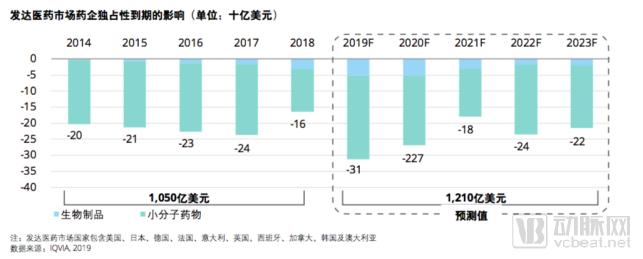

IQVIA projects that the expected impact of patent expirations for branded innovative drugs in developed markets will peak in 2019, reaching $121 billion over the next five years. This represents a significant increase from the $105 billion recorded over the previous five years, with a growth rate of 15.2%.

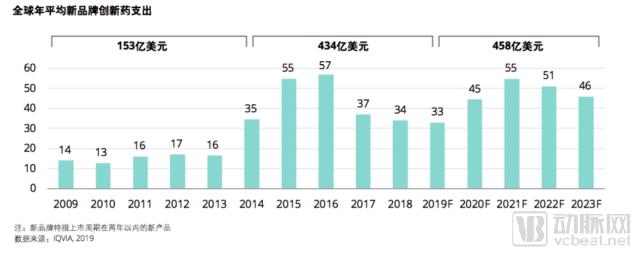

According to IQVIA’s forecasts, the number of innovative drugs and associated spending have increased significantly over the past five years. The average annual pharmaceutical expenditure on new branded innovative drugs launched between 2014 and 2018 was $43.4 billion. Total spending on new products introduced during the period from 2019 to 2023 is projected to be slightly higher, at approximately $45.8 billion.

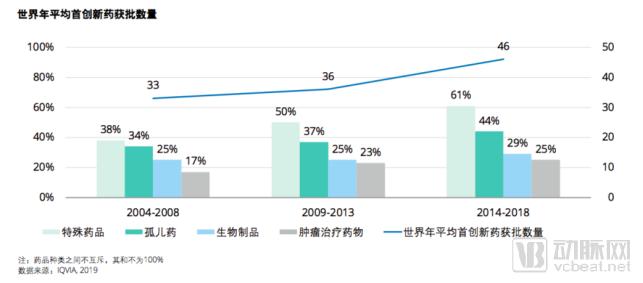

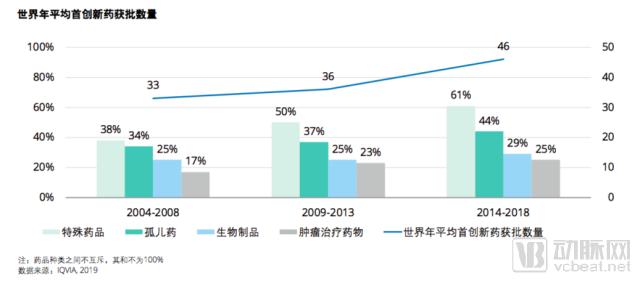

As the number of first-in-class new drug launches increases, the pharmaceutical pipeline continues to shift toward specialty drugs, orphan drugs, biologics, and oncology therapeutics. Over the next five years, specialty drugs are projected to account for nearly two-thirds of newly launched medicines, with oncology therapeutics comprising approximately 30%.

If the pace of ongoing research and the approval speed of orphan drugs achieving breakthrough therapies remain consistent with historical trends, orphan drugs could account for 45% of newly launched first-in-class innovative drugs over the next five years.1. It is anticipated that, in the future, more pharmaceutical companies will utilize biomarkers to identify and treat specific patients within the realms of specialty drugs, orphan drugs, biologics, and oncology therapeutics.

Against this backdrop, companies focused on the aforementioned novel drug research will continue to be hotspots in the capital markets and M&A landscape.

According to Deloitte research, the return on investment (ROI) for new drug development among large biopharmaceutical companies has hit a nine-year low of just 1.9%. For multinational pharmaceutical companies with annual R&D expenditures exceeding $10 billion, high-intensity R&D investment does not necessarily yield high returns. Investors are increasingly focusing on companies’ current product portfolios, their pipelines under development, and future growth potential.2。

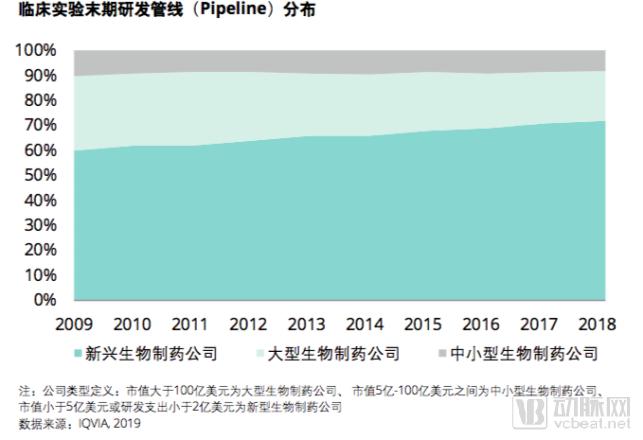

The decline in R&D return on investment has spurred a significant division of labor between large pharmaceutical companies and research-oriented biotechnology firms, with an increasing share of R&D work being conducted by biotech companies.

The late-stage clinical trial pipelines and the number of first-in-class drug approvals for emerging biopharmaceutical companies continue to strengthen. According to IQVIA research, over the past decade, the proportion of late-stage clinical trial pipelines among emerging biopharmaceutical companies—with annual revenues below $500 million or annual R&D expenditures under $200 million—increased from 60% in 2009 to 72% in 2018.

In the past five years, 68 first-in-class new drugs have been successfully launched worldwide, a significant increase from the 47 launched in the previous five-year period (2009–2013).3。

Against this backdrop, in addition to continuing the current trend of mergers and acquisitions, large pharmaceutical companies will also establish diverse forms of partnerships with emerging biopharmaceutical firms.

Mode 1: Collaborative development with large pharmaceutical companies can secure upfront payments and milestone-based payments. These cash flows are crucial for talent acquisition, R&D, and company operations before the developed products reach the market.

Innovent Biologics

According to public information, Innovent Biologics has entered into two strategic product development collaborations with Eli Lilly and Company, securing upfront payments and potential milestone payments totaling $3.3 billion. The parties signed cooperation agreements for the global development of three bispecific antibody drugs for tumor immunotherapy, among other assets, with total milestone payments exceeding $1 billion. This represents the largest biopharmaceutical international collaboration project in China to date, including the highly sought-after PD-1 monoclonal antibody for tumor immunotherapy.

Under the collaboration agreement, Innovent Biologics and Eli Lilly will jointly develop, manufacture, and commercialize the aforementioned novel drug. Innovent Biologics will lead the development, manufacturing, and commercialization in the Chinese market, while Eli Lilly will lead these activities in international markets. Should the above-mentioned antibodies be commercialized outside China, Innovent Biologics will receive additional sales royalties and other payments.

In addition to its collaboration with Eli Lilly, Innovent Biologics has also engaged in joint discovery partnerships for monoclonal antibodies and other initiatives with institutions such as Mabwell Bioscience. Innovent Biologics listed on the Hong Kong Stock Exchange’s biotech board in 2018.4。

Mode 2: By acquiring licensing rights for promising late-stage clinical drug candidates from large pharmaceutical companies in the Greater China/Asia-Pacific region, to accelerate late-phase clinical trials and commercialization in China, thereby achieving substantial returns.

Zai Lab

Zai Lab’s collaboration model with pharmaceutical companies involves paying licensing fees to secure R&D and commercialization rights for late-stage products in the Greater China or Asia-Pacific regions. According to public information, since 2014, Zai Lab has successively obtained R&D and sales licenses for the Greater China region from pharmaceutical companies such as Sanofi, BMS, and Tesaro, thereby building its product pipeline.5。

Mode 3: By the time a pharmaceutical company completes Phase II clinical trials and initiates Phase III trials, it has typically invested substantial capital and time while acquiring valuable trial sample data. Innovative biotechnology companies can acquire the rights to new drugs that have failed to demonstrate efficacy in Phase III clinical trials. Leveraging their proprietary technologies, these companies can redevelop such drugs at a lower cost and with a shortened R&D cycle, thereby ensuring substantial long-term returns for the company.

Suoyuan Bio

Suoyuan Bio’s collaboration model with large pharmaceutical companies involves acquiring late-stage R&D pipelines with global rights from these companies. Leveraging its AI- and big data-driven biomarker platform, Suoyuan Bio precisely identifies biomarkers associated with drug efficacy and develops new therapies tailored to responsive patient populations.

According to public information, Sorrento Therapeutics has acquired the global rights to three first-in-class novel drugs from Eli Lilly and Bristol Myers Squibb (BMS), among others. One of these is Enzastaurin, a small-molecule anti-tumor agent currently in Phase III clinical trials. Sorrento Therapeutics has obtained all global rights for the development, manufacturing, and commercialization of this drug, along with all intellectual property rights and other related rights and information, and has initiated a series of Phase III clinical trials for indications including diffuse large B-cell lymphoma (DLBCL) and glioblastoma multiforme (GBM). Another drug is Pomaglumetad, a first-in-class antipsychotic for schizophrenia that completed Phase II clinical trials at Eli Lilly. Sorrento Therapeutics has secured all global regulatory submission materials, clinical data, patents, and trademark rights for this asset, with Phase III clinical trials expected to commence in the near future. Additionally, Sorrento has acquired the global rights to Liafensine, a first-in-class novel drug for the treatment of resistant depression, from BMS and AMRI, holding the global rights for its research and development, manufacturing, and sales.6。

Mode 4: A professional team conducts independent R&D of first-in-class novel drugs from scratch, building upon early research achievements from renowned large-scale research institutions.

Xinyue Biomedicine

Xinyue Biomed’s professional team comprises seasoned experts with extensive industry experience. Leveraging drug R&D achievements accumulated during their early tenure at prominent large-scale research institutions or academic centers, the team independently develops novel classes of therapeutics for central nervous system-related disorders.

As indicated in Xinyue Biomed’s public prospectus, the intellectual property rights for its R&D pipeline were invented by the founder during his early tenure at renowned research institutions—Massachusetts General Hospital and the University of California, Los Angeles. Multiple investigational drugs have received FDA Orphan Drug Designation and Breakthrough Therapy Designation. Notably, orphan drug exclusivity will last for 7 to 7.5 years.

Upon completion of R&D or upon achieving milestone breakthroughs, Xinyue Biomed will secure high-value upfront payments, milestone payments, and post-launch sales royalties through collaborations and licensing agreements with major international pharmaceutical companies.7。

Endnotes

1. IQVIA Market Prognosis, Sep 2018.

2. Deloitte uk measuring return on pharma innovation report 2018.

3. IQVIA Market Prognosis, Sep 2018.

4. Innovent Biologics Prospectus

5. Zai Lab website: http://www.zailaboratory.com/

6. De Novo Biopharma Website: http://www.denovobiopharma.com/Chinese/

7. Syneurx Website: http://www.syneurx.com/