Business Restructuring and Overseas Expansion of Yuwell, Sinocare, iHealth, and Lepu Medical: Combined Revenue Exceeds RMB 7 Billion with Strong International Growth

In 2018, the medical device sector witnessed a continuous stream of policy initiatives. In light of this, some have predicted that the coming decade will be a “golden decade” for medical devices, which also holds true for home-use medical device companies capitalizing on the demographic dividend from China’s aging population. In April 2019, four major domestically listed home-use medical device companies successively released their annual reports for 2018. VCBeat extracted the revenue data related to home-use medical devices from each company’s business operations, as detailed below:

Overall, Sinocare Inc., through the acquisition of high-quality subsidiary businesses, became the listed company with the largest growth in its home-use medical device segment last year;

Yuwell Medical has maintained a steady upward trend, upholding its consistent stability;

Lifesense’s domestic sales business has declined due to fierce competition in the smart bracelet category in China, but growth in its overseas sales has maintained the company’s overall revenue;

Although the overall revenue of Andon Health’s iHealth product series has declined, its gross profit increased by 14% year-on-year, while its ODM/OEM product line has replaced it as the company’s largest revenue-generating business segment.

From the perspective of the revenue split between domestic and international markets in 2018, Sinocare’s overseas sales proportion rose from 7.5% in 2017 to 27.39%; Lifesense Medical’s overseas sales proportion increased from 56.94% in 2017 to 69.45%; and Yuwell Medical’s overseas sales proportion grew from 15.08% in 2017 to 15.71%. As the saying goes, rather than engaging in cutthroat competition in the domestic market, it is better for companies to expand overseas together and reap financial rewards.

Yuwell Medical saw only modest growth in its export proportion, which can be attributed to the overwhelming strength of its domestic distribution channels and brand presence. In contrast, Andon Health presents a more puzzling case: its export share not only failed to increase but actually declined from 65.03% in 2017 to 64.22%. According to VCBeat’s analysis, this trend is driven by two main factors. First, Andon Health relies heavily on Xiaomi’s extensive user base and mature channel resources within China. Second, the medical device data system solutions business of its overseas subsidiary, eDevice Inc., has experienced suboptimal growth. Moving forward, the company may consider expanding its operations into regions such as Europe and the United States through acquisitions of foreign companies.

Sinocare:NaInfusion of Strong, Fresh Blood

In 2018, Sinocare Inc. achieved total operating revenue of RMB 1,550,513,400, representing a year-on-year increase of 50.10%. The operating profit and total profit amounted to RMB 344,867,800 and RMB 354,213,200, respectively, reflecting year-on-year increases of 15.95% and 16.08%, respectively. The net profit attributable to shareholders of the listed company reached RMB 310,448,400, a year-on-year increase of 20.34%.

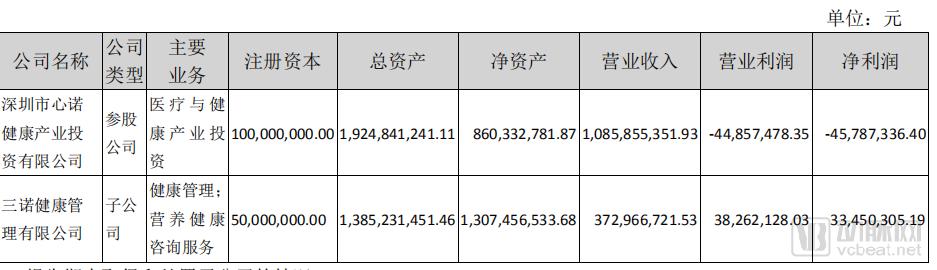

In terms of revenue from subsidiaries, Sinocare Health and Sannuo Health contributed significantly to Sinocare’s revenue, with Sannuo Health being included in Sinocare’s annual report for the first time.

In January 2018, Sinocare Inc. completed the acquisition of a 64.98% equity interest in Changsha Sinocare Health Management Co., Ltd. through the issuance of shares to purchase assets, thereby bringing its total ownership of Changsha Sinocare Health Management Co., Ltd. to 100%. January 31, 2018 was designated as the equity closing date, from which point Changsha Sinocare Health Management Co., Ltd. has been included in the consolidated financial statements of Sinocare Inc.

In the 2018 annual report, the operating revenue of Sinocare Health included in the consolidated financial statements of Sinocare Biosensor Co., Ltd. due to the acquisition was RMB 372.97 million, accounting for 24.05% of Sinocare Biosensor’s consolidated operating revenue for 2018. The total assets included in the consolidated financial statements of Sinocare Biosensor as a result of this acquisition amounted to RMB 1,385.30 million, representing 46.08% of Sinocare Biosensor’s consolidated total assets at the end of 2018.

In addition, Trividia is a wholly-owned subsidiary of Sinocare Health, and PTS is a wholly-owned subsidiary of Sinocare Management. PTS owns the “A1C Now+” glycated hemoglobin testing system, the “Cardio Chek” blood lipid testing system, as well as products such as Cotinine and PTS Services. Trividia owns the “TRUE” series of blood glucose monitoring products and diabetes auxiliary products (including diabetes skin care products, diabetes management software, urine ketone testing systems, fiber tablets, and multivitamins).

From an operational perspective, in 2018, Sinocare Biotech continued to strengthen its channel and terminal advantages, enhanced its capabilities in serving key accounts and operating self-run e-commerce platforms, improved terminal penetration and market expansion efforts, and increased brand promotion and marketing initiatives, thereby further driving product sales. The company accelerated its layout of patient-centered whole-course disease management. It also expedited the synergy and collaboration among R&D, procurement, production, and sales for Sinocare and PTS.

Furthermore, Sinocare has intensified its efforts to expand into the hospital market, primary healthcare market, international markets, and non-blood glucose monitoring product segments, while strengthening market cultivation and investment.

In the retail market, Sinocare has been directly engaging end-users and enhancing terminal penetration by continuously advancing its diabetes patient identification program. The company has also strengthened its capabilities in serving key accounts and operating self-run e-commerce platforms. By deepening engagement with its existing user base and promoting the implementation of patient screening initiatives, educational specialist promotion programs, and distributor multiplication plans, Sinocare ensures sustained and stable growth in its retail business.

In the clinical market, Sinocare has enhanced its management and business development capabilities by building an industry-leading marketing team. By introducing in-hospital blood glucose management systems, the company continuously promotes the application of its products in clinical settings. Furthermore, Sinocare has established a specialized clinical promotion team and a dedicated clinical sales service team, improving operational efficiency through refined marketing strategies and management. While consolidating product usage in hospitals already served, the company is constantly expanding its reach to new hospitals.

In the international market, Sinocare’s products are sold in synergy with those of PTS and Trividia, integrating overseas marketing networks to expand global business operations. While consolidating sales of lipid profile and HbA1c testing products, PTS has intensified efforts to upgrade its product portfolio and adjust its structure for Cotinine and Services offerings, thereby strengthening its expansion and strategic layout in the global market.

Yuwell Medical:StableSheng Zhongsheng

Yuwell Medical has established three core business pillars—home healthcare, clinical medical care, and better living—as its strategic development directions. In the home health sector, the company focuses on expanding its product market presence in three major therapeutic areas: respiratory, cardiovascular, and endocrine diseases. Since its initial public offering, Yuwell has extended its business scope from home-use medical devices into clinical medical devices and the better-living segment through mergers and acquisitions, thereby achieving sustained and rapid growth in profitability and market competitiveness.

During the reporting period, Yuwell Medical maintained stable overall operations, with a steady improvement in operational quality and sound performance in assets, operations, and financial position. The Company achieved total operating revenue of RMB 4.183 billion, representing a year-on-year increase of 18.12%; net profit attributable to shareholders of the listed company amounted to RMB 727 million, up by 22.82% compared to the same period last year; net profit attributable to shareholders of the listed company after deducting non-recurring gains and losses reached RMB 642 million, an increase of 25.26% year on year; and net cash flow from operating activities totaled RMB 798 million, surging by 229.68% compared to the same period last year.

Looking back on the past year, in terms of product R&D, Yuwell Medical established Shenzhen Lianpu Medical Technology Co., Ltd. in March 2018 to undertake AED research and development tasks, accelerate the resolution of production capacity challenges, enhance product performance, and localize the manufacturing of AEDs and other devices. Subsequently, Yuwell established Primedic (Suzhou) Medical Technology Co., Ltd. as a subsidiary to leverage advanced German technologies for the R&D and manufacturing of emergency medical equipment such as AEDs.

In the home healthcare segment, online platforms demonstrated outstanding performance growth, with a year-on-year increase of over 40%. Yuwell expanded its sales channels by adopting a multi-point distribution strategy, achieving single-day sales exceeding RMB 100 million for the first time in November. The company ranked first in sales across nine major product categories, maintained its position as the industry leader in home healthcare for four consecutive years, and earned widespread consumer preference. Meanwhile, offline platforms also achieved growth of more than 10%, driven by personnel and organizational adjustments as well as refined terminal management strategies.

In terms of refined management, Yuwell Medical continues to implement refined management practices to steadily enhance the company’s overall competitiveness. In 2019, the SAP project will be officially implemented and put into use. The SAP system serves as the company’s technological platform for integrating value chain information, providing critical data support for management in making strategic decisions and advancing refined management.

Lifesense Medical: Weak Domestic Sales Relied on Exports

2018 was a year of exploration and innovation for Lifesense Medical. During the reporting period, the Company actively expanded into high-end markets both domestically and internationally, strengthened collaborations with premium industry clients, and extended its business reach across a wide range of sectors, including healthcare, insurance, transportation, retail, gifts, internet, wellness, and education. The Company maintained strong partnerships with renowned domestic and international brands such as Braun, Philips, Welch Allyn, Withings, Dretec, and Beurer, fully leveraging its advantages in R&D, medical-grade manufacturing systems, the most comprehensive health IoT product portfolio, medical service capabilities, and big data analytics.

According to the latest data from market research firm IDC, Lifesense Medical’s smart band shipments ranked among the top three in the industry in 2018.

During the reporting period, LifeSense Medical maintained stable overall operations. The company achieved annual operating revenue of RMB 775.1032 million, representing a year-on-year decrease of 10.56%. Among this, overseas sales generated operating revenue of RMB 538.3358 million, a year-on-year increase of 9.10%, demonstrating steady growth primarily driven by increased sales of medical devices such as electronic blood pressure monitors and body fat analyzers. Domestic sales generated operating revenue of RMB 232.9937 million, a year-on-year decrease of 37.35%. The decline in domestic operating revenue was mainly attributable to intense competition in the smart wristband category within the Chinese market.

During the reporting period, Lexin Medical achieved a net profit of RMB 22.0349 million, representing a year-on-year increase of 26.17%. The net profit attributable to shareholders of the parent company amounted to RMB 24.0159 million, up by 34.61% from the same period last year. In 2018, the company’s total R&D investment reached RMB 56.4042 million, accounting for 7.28% of its total operating revenue.

In addition, during the reporting period, Lifesense Medical continued to launch new products such as the “Lifesense S9 Body Fat Monitor” and other models of health scales and blood pressure monitors, all of which have obtained Class II medical device certification. In October 2018, Lifesense’s first professional medical-grade smartwatch, the Lifesense Health Watch, made its debut at the First China Hospital Internet of Things Conference. Currently, this medical-grade health smartwatch is undergoing registration with the CFDA.

Andon Health:OEM/ODM Business Replaces iHealth's Core Position

In 2018, Andon Health aligned with industry development trends and continued to advance its strategy of “entering the mobile healthcare and health big data sectors through wearable devices and smart hardware, thereby building a user-centric health ecosystem.” iHealth upgraded traditional consumer health products, such as electronic blood pressure monitors and glucometers, into smart hardware integrated with mobile apps and cloud platforms to harness massive amounts of data and deliver personalized services to users.

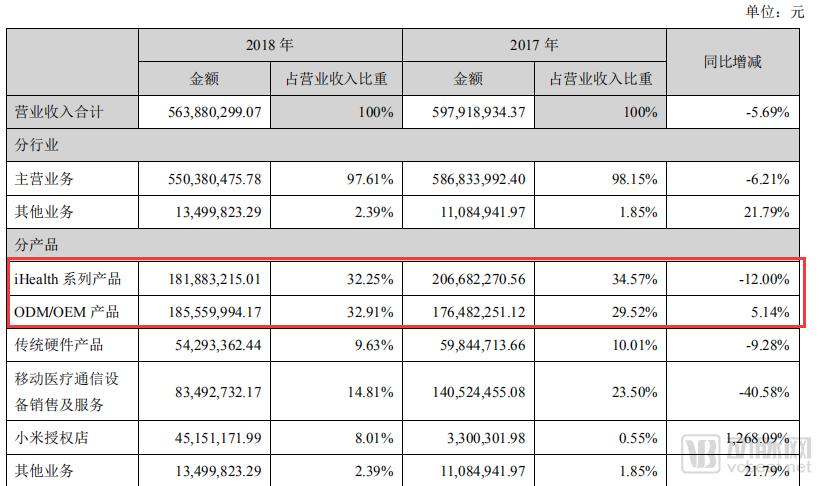

During the reporting period, Andon Health Co., Ltd. achieved an operating revenue of RMB 563.8803 million, representing a slight year-on-year decrease, primarily due to the company's adjustment of its sales structure and a decline in revenue from eDevice. The net profit attributable to owners of the parent company amounted to RMB 12.6868 million, a year-on-year increase of 107.65%, mainly driven by the transfer of equity interests in associate companies and the implementation of quality improvement and efficiency enhancement measures during the reporting period. In response, Andon Health will continue to implement cost reduction and efficiency enhancement measures. Administrative expenses totaled RMB 151.8785 million, a significant year-on-year decrease of 20.34%, while R&D investment reached RMB 137.4678 million, a year-on-year increase of 2.49%.

In terms of revenue, although the iHealth product series saw a 12% year-on-year decline, its operating costs decreased by 27.67%. However, in 2018, the share of revenue from the iHealth product series dropped from 34.57% in 2017 to 32.25%. Meanwhile, the revenue share of its ODM/OEM product line increased from 29.52% in 2017 to 32.91%, becoming the company’s largest business segment.

However, this scenario was clearly not part of Andon Health’s strategic plan. In its 2019 roadmap, Andon Health outlined a comprehensive improvement plan for the iHealth product series.

In 2019, Andon Health will accelerate the implementation of its “Online-to-Offline” (O+O) new model for internet-plus medical diabetes diagnosis and treatment in Tianjin, Beijing, Shanghai, Guangzhou, Shenzhen, and Shenyang, while also speeding up its expansion in the United States and Singapore. Meanwhile, the company will continuously optimize its organizational structure by breaking down functional silos, downsizing individual accounting units, and forming project teams and product-focused subsidiaries centered on business operations to launch products with ultimate cost-performance ratios.

To achieve the Company’s strategic transformation objectives and balance investment with performance, Andon Health will focus its operational plans for core businesses on the following key areas:

The iHealth series adopts smart hardware as an entry point to capture massive amounts of data and deliver personalized services, marking the company’s transition from hardware to service-oriented solutions. Adhering to a global development strategy, iHealth integrates comprehensive smart hardware for chronic disease management with its cloud platform, pioneering a new “O+O” model for diabetes diagnosis and treatment.

The company’s diabetes diagnosis and treatment initiative—the Big Data- and AI-based Clinical Diabetes Management System—was approved for establishment in 2018 under Tianjin’s Major Special Projects. The company plans to sign agreements with more physicians in 2019, aiming to serve 10,000 patients each in Tianjin and Beijing. The U.S. team will continue to expand the B2B sales channels for iHealth’s line of hardware products; some contracted professional client projects will enter the procurement phase ahead of schedule, and the number of signed physicians and initial beta users has exceeded expectations.

The iHealth Europe team is responsible for developing the patient-facing mobile application and the web-based management platform for the POWER2DM project, an EU government health management initiative for diabetes patients. The team also provides algorithmic support for data collection, analysis, and decision-making. In 2019, clinical studies will continue to be conducted simultaneously in Spain and the Netherlands.

In response, Andon Health will continue to collaborate with professional medical institutions both domestically and internationally to refine the new “O+O” model for diabetes diagnosis and treatment, thereby better serving patients with diabetes. As this new model is further expanded and deepened, higher demands will be placed on iHealth products and their supporting platform systems. The company will continue to accelerate technological upgrades for its smart hardware products, mobile applications, and cloud platforms.

In 2019, Andon Health will continue to launch ultra-high-cost-performance products on the Xiaomi platform—similar to its iHealth blood pressure monitors and thermometers—to help users better manage their health. The company will begin laying out new technological breakthroughs in areas such as blood pressure, continuous glucose monitoring (CGM), body composition, and temperature measurement, further consolidating its technical advantages in the “Internet + Healthcare” sector. By meticulously refining product definition and design, Andon Health aims to deliver a brand-new user experience.

In addition, Andon Health will continue to monitor market demand, collect user feedback, iteratively optimize existing products, and launch more new products that achieve both market success and positive reputation. Based on market research, the company previously launched nebulizers, neck massagers, ear thermometers, Doppler fetal heart rate monitors, and other products through Xiaomi’s channels, offering both practicality and high cost-performance ratio. In 2019, Andon Health will continue to consider launching one or two ultra-high-cost-performance products in the consumer electronics sector.