Tongxin Medical Alliance Achieves Profitability with Unique Commercial Closed-Loop, Steering Clear of Traditional Medical AI Bidding Traps

Sophmind

Internet Medical Examination Platform

On May 7, 2019, Sophmind Technology (Beijing) Co., Ltd. (hereinafter referred to as “Sophmind”) held a strategic launch event in Beijing, unveiling its upgraded strategy for the “Technology-Driven Healthcare Platform.” In response to the current state of the industry, Sophmind advocates breaking away from the pattern of homogenized and redundant competition among medical imaging AI companies. The next phase should be oriented toward delivering tangible clinical value. Specifically, this includes:

1. Clinical Orientation: Returning to the origins and essence of imaging technology, we focus on the needs of clinicians, aiming to provide more precise diagnostic and treatment recommendations for patients as our research direction, rather than competing with radiologists and sonographers on diagnostic accuracy. Through its internet hospital services, Sophmind serves nearly 50,000 clinicians, making their needs the starting point for all technological R&D;

2. Cross-disciplinary Integration: Only by promoting cross-disciplinary collaboration among the four fields of medical imaging technology, AI technology, imaging diagnosis, and clinical application can products with genuine clinical value be developed to address the practical problems faced by physicians and patients. Sophmind operates more than 300 self-owned and partnered imaging centers across China, having accumulated over 8.5 million imaging cases, thereby possessing the capability for cross-disciplinary integration;

3. Openness and Win-Win Cooperation: Given the complexity of medicine, no single team can achieve breakthroughs in all disease areas. While each party focuses on developing its own specialty, they can collaborate to leverage complementary strengths and jointly promote the clinical application of new medical technologies. Sophmind has currently launched 38 exclusive intelligent diagnostic products, primarily serving patients with cardiovascular, cerebrovascular, and oncological conditions. Meanwhile, it has established close partnerships with nearly 100 world-class universities and research institutions, such as Tsinghua University, Peking University, and the Chinese Academy of Sciences, to leverage their respective expertise and better apply new technologies in clinical practice.

At this press conference, Sophmind also reviewed the current development status of the imaging + AI industry and presented unique industry insights.

I. Real-World Challenges of AI in Medical Imaging

While the medical imaging AI industry has attracted substantial capital investment, the reality remains starkly cold. It is common for multiple companies’ pulmonary nodule diagnosis products to be deployed in a single large hospital; yet in clinical practice, radiologists rarely use them.

The reason is that most medical imaging AI companies initially introduced algorithms from abroad, trained them using public datasets, and developed their own proprietary models. Subsequently, they collaborated with large hospitals to acquire data for further model training and clinical application. To attract attention, some companies organized human-versus-machine competitions, pitting radiology and ultrasound experts against AI algorithms to determine which party could deliver faster and more accurate diagnoses. Due to well-known reasons, AI algorithms often emerged victorious in these contests, capturing public interest and fostering the mistaken belief that technology would soon replace physicians.

Once sufficient preliminary concept promotion has been achieved, medical imaging AI companies begin applying for Class II or even Class III medical device licenses. They plan to market their products as computer-aided diagnosis software, distribute them through agents, and sell them to public hospitals via bidding processes. Thus, a modern big data–driven technology has been transformed into a healthcare IT software sales model.

Although deep learning has brought about a new wave of technological transformation, the medical field demands a high degree of professional expertise. The technical challenges faced by AI in medical imaging must be considered from three dimensions:

First, different imaging modalities operate on distinct principles, resulting in varied data outputs. For instance, X-ray and CT share similar imaging mechanisms, producing relatively simple and clear images; consequently, most medical AI companies have concentrated their efforts in this domain. In contrast, due to its different, complex, and variable imaging principles, MRI presents greater technical challenges, leading to very few medical AI companies engaging in MRI-related research. Conversely, a significant number of world-leading scientists are dedicated to AI research in MRI, given its vast potential for exploration.

Second, how to obtain standardized imaging data. Due to the low level of standardization in China's healthcare system, significant issues arise across various stages of medical care. Even with identical equipment, different hospitals employ varying imaging scanning methods, sequences, and parameters, resulting in substantial differences in data quality. In many cases, imaging data from primary-care hospitals do not even comply with the DICOM protocol. Under such conditions, the robustness of AI algorithms becomes a major concern. In particular, it poses a practical challenge whether a single algorithm package can be universally applied after obtaining medical device registration approval.

Third, disease mechanisms vary, leading to significant differences in the technical challenges AI must address. Some tasks merely involve detecting the presence of lesions and measuring their size, which is relatively straightforward; however, others require assisting in diagnosis or evaluating disease prognosis, which are far more complex. From a practical clinical perspective, given the diversity of medical subspecialties, it is impossible for a single AI expert to solve all problems. It is already a remarkable achievement to make significant contributions within a specific subspecialty—such as cardiomyopathy, Alzheimer’s disease, epilepsy, or Parkinson’s disease—after three to five years of dedicated effort.

Currently, most medical imaging AI companies start with pulmonary nodule detection and fundus angiography, as these fields offer abundant publicly available data that is relatively easy to acquire, and pulmonary nodule images are intuitive and conducive to observational diagnosis. Subsequently, they often expand into areas such as fracture detection, bone age assessment, breast cancer pathology, and stroke analysis. These research directions are primarily driven by technological maturity rather than by the daily clinical workflows of physicians.

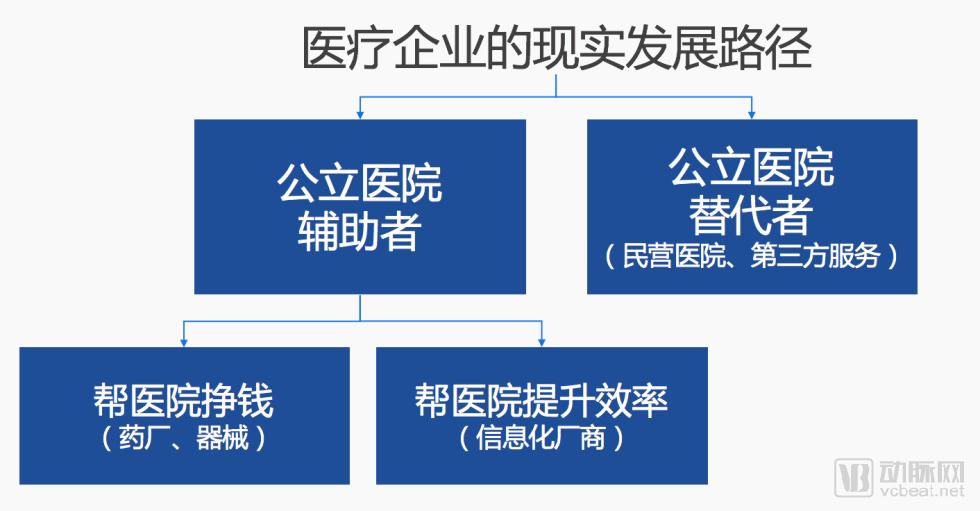

Even if technical issues are resolved, commercialization remains a major obstacle. Healthcare enterprises fall into two categories: the first, and most numerous, comprises enablers of public hospitals, providing products or services centered around these institutions; the second consists of alternatives to public hospitals, including private hospitals and third-party medical service providers.

The first category of enterprises is further divided into two types. The first type comprises companies that help hospitals generate revenue, such as pharmaceutical firms, medical device manufacturers, and consumables suppliers. By introducing their products, hospitals can create more medical service items and thereby increase economic income, making it relatively easier for these companies to promote their business. The second type includes vendors that help hospitals improve efficiency, such as healthcare IT providers. These companies leverage information technology to optimize current clinical and service workflows, enhancing operational and management capabilities. However, since their services do not directly generate new revenue streams for hospitals, market expansion faces significant challenges, and the collection of accounts receivable is particularly difficult.

By the same token, if AI imaging companies merely assist radiologists in making diagnoses faster and better without creating new revenue streams, they are even less likely to genuinely reduce radiologist staffing levels, resulting in uncertain market prospects. Even if AI were to truly replace radiologists one day, based on China’s 150,000 radiologists with an average annual salary of RMB 100,000, the total addressable market would amount to only RMB 15 billion. Compared to the current level of resource investment, this market size is simply too small.

Sophmind integrates imaging technology with AI, implementing these solutions within its own imaging centers. Operating under a medical chain management model, Sophmind has established a mature standardized imaging system to ensure standardized data acquisition. By deploying these systems in its proprietary imaging centers, the company also circumvents issues related to the general adaptability and robustness of its algorithms. Furthermore, implementation within these centers facilitates the effective transformation of technology into commercial products, achieving a closed-loop business model by addressing practical patient needs. Sophmind achieved overall profitability in 2018.

II. The Misunderstood Value of Imaging AI

So, where exactly does the value of AI in medical imaging lie?

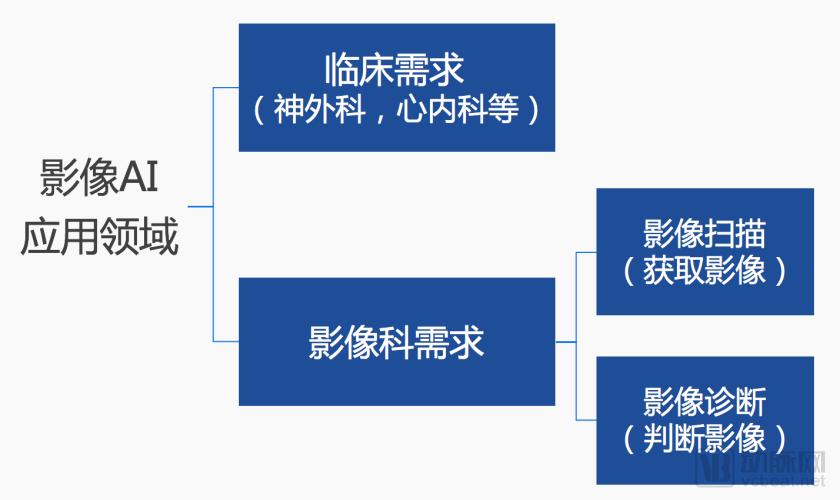

Medical imaging AI should not merely address issues within radiology departments; instead, it should focus on leveraging imaging technology combined with AI to solve clinical problems, thereby unlocking unlimited future growth potential. The application areas of medical imaging AI can be divided into two major directions:

The first category of directions is to address clinical needs, such as those required by departments like neurosurgery and cardiology. Since its inception, medical imaging has been a specialty that addresses clinical needs through imaging technology, evolving alongside advancements in fundamental physics and biomedical engineering. Nearly all clinical departments require support from medical imaging. If AI in medical imaging can solve practical problems across various clinical specialties, then there will be demand among all physicians—namely, providing precise diagnoses and effective treatment recommendations through digital analysis.

Why is implementation so challenging? The reason lies in the knowledge gaps spanning four distinct disciplines: biomedical engineering, computer AI, diagnostic imaging, and clinical needs. Without the resources and capabilities for cross-disciplinary integration, the difficulty is substantial.

The second category addresses the intrinsic needs of radiology departments, which can be further divided into two scenarios:

The first issue pertains to image scanning, specifically how to enhance efficiency and accuracy during image data acquisition. This aspect is often overlooked by the general public. For instance, if the raw photographs captured by a camera are of poor quality, subsequent editing with any software will rarely yield satisfactory results.

Abroad, significant progress has been made in leveraging imaging combined with AI technology to achieve rapid image acquisition, shorten examination times, and reduce radiation exposure. In China, however, this area has received insufficient attention. This is primarily because public hospitals dominate the healthcare system and lack strong incentives to improve efficiency; regardless of patient volume, their daily workload remains stable, with excess patients simply placed on waiting lists. Meanwhile, private hospitals do not have sufficient patient volumes to generate demand for such solutions. Additionally, there is less emphasis in China compared to abroad on the health risks associated with medical imaging radiation. These technologies can substantially enhance the operational efficiency of radiology departments and are therefore highly valuable.

The second category is imaging diagnosis, such as AI-assisted diagnosis of pulmonary nodules. However, the real-world scenario faced by radiologists is as follows: when a patient undergoes a chest CT scan, the radiologist typically has no prior knowledge of the patient’s specific condition. Therefore, the resulting chest CT images must be evaluated for all potential pathologies. There are at least ten common lung diseases; consequently, an tool capable of detecting only pulmonary nodules does not serve as the optimal assistant for radiologists.

For instance, if an article potentially contains ten grammatical errors, but AI can only flag one, leaving the remaining nine to be identified through manual re-reading and screening, then such an AI application holds limited practical value.

Particularly in scenarios where physicians are burdened with the cumbersome process of importing medical images from the Picture Archiving and Communication System (PACS) into AI systems and then exporting the diagnostic results back to PACS. The actual need of radiologists is for AI to flag all suspected lesions in the region of interest (regardless of lesion type, as long as they are abnormal), allowing radiologists to perform a secondary review and verification. This eliminates the need to manually re-examine over 100 images one by one, thereby significantly improving efficiency. However, meeting this demand imposes extremely high requirements on algorithms and data, which remain difficult to achieve at present.

Tongxin Medical Alliance has its own complete team of radiologists, technicians, nurses, and marketing professionals, effectively meeting the practical needs of clinicians and patients. Meanwhile, Tongxin Medical Alliance collaborates with clinicians through its internet hospital to provide follow-up consultations, imaging examinations, follow-up management, and pharmaceutical services for returning patients, ensuring that all technologies are implementable and forming a closed-loop service system.

III. The Future Development of Imaging AI

Integrating the technical characteristics of imaging AI with its clinical applications, future development should focus on the following four aspects:

1. Guided by clinical needs, integrate imaging technology with AI, collaborate closely with radiologists and clinicians, and develop practical, high-value products for physicians.

II. Given the specialized nature of healthcare, each company should identify its own niche and area of expertise, rather than rushing to develop homogeneous products. Such homogenization will lead to cutthroat competition and hinder the industry’s long-term development. Considering the lengthy R&D cycles in healthcare, focusing on a specific professional domain allows companies to build increasingly high competitive barriers through continuous data accumulation and sustained research investment.

3. Since no single company can achieve comprehensive coverage across all disease types and imaging equipment, open collaboration and leveraging respective strengths will become an inevitable trend. This approach will not only contribute to the overall advancement of medicine but also facilitate the practical implementation of AI technologies.

IV. Relying on investment for survival means the company is always on a “countdown to life or death.” Grounded in reality, achieving profitability is the only viable path.

Compared with internet healthcare, AI technology has the opportunity to fundamentally address the insufficiency in medical supply, representing a technological transformation with more profound implications. However, this technological revolution must return to its original intent and proceed with pragmatism to turn ideals into reality.