Xiezhu Builds a Tech-Driven Platform Integrating Medical Data and Commercial Insurance with OCR-Powered Full-Line Item Automated Adjudication System

In 1992, Wu Jun and Tang Shu, then students in the United States, met while working part-time at a restaurant. In a foreign land, the two like-minded individuals quickly became close friends. After graduation, they both entered the U.S. health insurance industry, with Wu starting his career in product actuarial science and Tang in IT architecture.

“Chinese people are extremely diligent.” Wu Jun glossed over his and Tang Shu’s experiences in the United States with this single remark. It was precisely this diligence that led to Wu being dispatched by AIA (then still a subsidiary of AIG—American International Group) from the U.S. to Hong Kong in 2004, where he served as Chief Actuary for AIA’s Asia-Pacific health insurance division. In 2008, Tang, serving as Chief Architect, was sent by Wellpoint, then the largest health insurer in the U.S., from the United States to China to prepare for the establishment of a third-party claims administration company.

The two returned to China one after another and began to conduct in-depth research on commercial health insurance in China. From the perspective of their existing expertise in U.S. professional health insurance, Wu Jun found that although China’s commercial health insurance sector has been developing at a very rapid pace, there are still two core issues:

First, the operational model of China’s commercial health insurance industry is relatively extensive. Taking claims processing as an example, insurers are confronted with a large volume of medical bills during adjudication. Each bill contains detailed medical data; however, these granular details are not retained within the insurers’ systems, resulting in the loss of substantial volumes of valuable medical data.

Second, the operational model of commercial health insurance in China is relatively primitive, with most processes still relying on manual operations. These manual workflows depend heavily on the personal experience of claims adjusters, resulting in high error rates and low efficiency.

In Wu Jun’s view, addressing these issues requires leveraging the management expertise and advanced systems of U.S. commercial health insurance. At that time, Tang Shu was engaged in the “transplantation” of such systems, but practical experience revealed that American systems often faced “adaptation challenges” when implemented in China. Tang Shu explained that, structurally, China’s basic medical insurance system features broad coverage with limited benefits, where most claims are first reimbursed by public medical insurance before commercial insurers step in, resulting in a dual-payer model. In contrast, the United States operates primarily under a single-payer framework for any given claim. Consequently, the underlying architectures of the two systems are fundamentally inconsistent.

Wu Jun and Tang Shu recognized this business opportunity. “With our foundational technical expertise from the United States and a thorough understanding of China’s commercial health insurance market, we can independently develop a health insurance system tailored to local conditions.”

Driven by the vision of providing automated and efficient claims settlement services for commercial health insurance, Wu Jun and Tang Shu founded Shanghai Harmony Building Information Technology Co., Ltd. (hereinafter referred to as “Harmony Building”) in 2011. They assembled a research and development team of over ten members and began developing a fully detailed, fully automated adjudication system with 100% independent intellectual property rights.

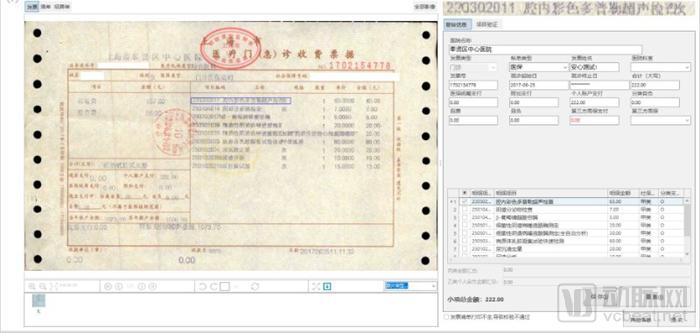

Harmony Building’s claims adjudication system is the underlying technology for insurance reimbursement based on medical invoices. Currently, medical invoices in China feature major categories on the left side, such as Western medicine fees and consultation fees, comprising a limited number of broad line items. The right side provides itemized details, listing each specific medication, examination, and other services, such as amoxicillin and CT scans.

The traditional claims adjustment method in China involves staff manually reviewing claim documents and then compensating customers. During this process, the insurance company’s system retains only a limited number of major line items, without entering detailed data into the system or performing structured processing. Since detailed data do not directly participate in the claims adjustment within the system, risk control relies solely on manual expertise, which can sometimes lead to errors. For instance, discrepancies between diagnosis and treatment (such as prescribing antihypertensive medication for a cold) are judged entirely by humans, making it highly prone to oversight.

To address errors arising from manual operations in claims adjustment services, Harmony Building has leveraged its underlying systems to establish a systematic and detailed knowledge base. Wu Jun stated, “This is indeed a highly complex task. Taking pharmaceuticals as an example, there are 250,000 drug products and dosage forms in China. We must first assign unified codes to them. For instance, amoxicillin is manufactured by two to thirty companies in China, each potentially using different product names.” Over a period of four to five years, Harmony Building has compiled diagnostic and treatment information—including drugs, medical devices, examinations, and surgical procedures—into standardized knowledge graphs and coding systems, which have been aligned with local medical insurance regulations across various regions.

To enable automated claims processing, the system first parses insurance policies, transforming textual rules into system configurations akin to assembling LEGO blocks. Subsequently, based on these predefined configurations, the system automatically decomposes the medical expenses submitted by patients, determining which portions are covered by the insurer and which are to be paid out-of-pocket by the individual.

To ensure accuracy, Harmony Building has introduced human-machine collaboration features. The system automatically flags risks (such as discrepancies between diagnosis and treatment) and displays them on a pop-up page for reviewers to examine. Claims are reimbursed only after further review by the personnel. Wu Jun told reporters that this approach improves efficiency by five to ten times and reduces the skill requirements for staff.

Notably, Harmony Building’s fully detailed, fully automated claims adjudication system is a universal platform capable of automatically processing claims for all insurance policies available on the market.

As claims adjustment systems have been implemented across various insurance companies, business volumes have gradually increased. Wu Jun identified an issue with the entire system: detailed data still requires manual entry.

“Currently, domestic OCR (Optical Character Recognition) technology is relatively mature, but its accuracy in the field of medical invoice recognition is only 30%, rendering it practically unusable,” explained Wu Jun. He noted that medical invoices in China are machine-printed and present numerous challenges, such as watermarks on the paper, various stamps affixed to the invoices, and misaligned printing. Furthermore, the format of medical invoices varies across different hospitals in China.

These factors have all contributed to the low accuracy of OCR recognition in medical data. Consequently, five years after the development of its first automated adjudication system, Harmony Building began developing its second AI-powered OCR system based on deep learning.

Harmony Building Recognition Performance (Image source: Provided by the company)

After two years of development, this OCR system has been trained on millions of invoice images and millions of line-item records, achieving recognition accuracy rates exceeding 90% for both scanned and photographed images. Single-threaded processing enables second-level recognition per invoice, and a single server equipped with four GPUs can process tens of millions of invoices annually.

In actual production, to ensure 100% accuracy of entered information, Harmony Building adopts a model combining automatic recognition with manual review. Notably, erroneous data corrected manually during the production process are accumulated and used to retrain the recognition engine, continuously enhancing the system’s recognition capabilities while reducing the need for manual intervention. Currently, this has established a virtuous cycle characterized by “machine-led entry, supplemented by manual verification, with continuous learning from erroneous data.”

Currently, Harmony Building’s two systems work in tandem. Claimants upload images of medical documents via a WeChat mini-program or mobile app. The OCR system recognizes the content, and the human-in-the-loop collaboration system then completes the review process. Subsequently, the itemized data from the invoices is fed into the automated claims adjustment system in a structured format, ultimately enabling claim settlement.

In terms of future planning, Harmony Building will continue to deepen its application of machine learning and establish partnerships with major insurance companies.

It is understood that Harmony Building is currently undergoing its Series B financing round.