From Dollar Frenzy to Rational Retreat: A Review of Digital Health M&A Activities from 2016 to Q1 2019

From being questioned as a novel concept to stepping into the public spotlight, digital health has seen its popularity soar and become a new hotspot in Silicon Valley since the inauguration of the new U.S. administration in 2016—all within just three years. During this period, capital activities in the digital health sector have been vigorous; in terms of mergers and acquisitions (M&A) alone, record-breaking deal volumes in one year are often followed by new developments the next. From the emergence of numerous unicorns to their acquisition by tech giants, from the initial patterns of the M&A wave to the capital frenzy of 2018, and then to the slowdown in 2019, digital health has indeed experienced the dramatic ups and downs of the capital market.

Specifically, in 2016, the U.S. digital health sector was experiencing its own “tumultuous times.” By the end of that year, the American healthcare landscape was poised for a major transformation following the conclusion of the presidential election, with various subsectors responding to industry reforms driven by the changing political climate. Amidst this backdrop, digital health—increasingly brought into the public eye by the rapid development of the internet and big data—saw a surge in merger and acquisition (M&A) activities. Throughout 2016, there were 40 M&A deals in the digital health space, surpassing the 36 recorded in 2015. These transactions involved many high-profile and notable companies, such as Google, Fitbit, and Philips, with the largest deal reaching $544 million.

2017 marked the inception of the wave of mergers and acquisitions in the U.S. digital health sector. On August 13, President Trump personally endorsed and launched the nation’s largest telemedicine initiative at the White House—the Department of Veterans Affairs (VA) “Telehealth Service from Anywhere to Anywhere” initiative, mandating comprehensive coverage. That year, the U.S. digital health market witnessed 778 financing transactions, with total funding reaching $7.2 billion.

In 2018, U.S. digital health M&A activity witnessed its “record-breaking year.” A wave of mergers and acquisitions, dominated by vendors, payers, and pharmacy benefit managers (PBMs), swept across the entire healthcare industry, engulfing digital health companies as well. The number of M&A transactions reached 56 in that year, setting a new historical high. Among these, 13 deals disclosed their prices, with the total transaction amount reaching $7.6 billion.

However, just as the market held high expectations for digital health M&A transactions in the new year, the Q1 2019 M&A report marked a significant turning point, with a comprehensive slowdown in M&A activity. In light of this, VCBeat (WeChat Official Account: vcbeat) has reviewed digital health M&A deals from 2016 through Q1 2019, aiming to analyze the origins, development, and prominent features of this M&A wave, while also forecasting its future trends.

Since the merger and acquisition (M&A) frenzy in the digital health sector erupted in 2016, the names of major diversified conglomerates have frequently appeared on M&A lists over the past three years. These include well-established cross-industry giants such as Roche, Google, Apple, General Electric, and Royal Philips. In contrast, the acquired companies are generally less renowned, yet they are highly sought after for their unique business models, data resources, or proprietary technologies.

The business activities of industry giants often serve as bellwethers for industrial development. The entry of multinational tech conglomerates such as Apple and Google has made the future trajectory of the healthcare sector even more pronounced. These major companies have delivered remarkable performances in the broader health sector since the inauguration of the new U.S. administration.

Below is a list of major acquisitions of digital health companies since 2016.

2016:

·Swiss electronics company Logitech acquired wireless headphone maker Jaybird for $50 million in cash;

· Early pioneer in mobile health, BioTelemetry, acquired TelCare for $7 million;

· HMS acquired Essette for $20 million;

· Fitbit acquired Coin’s wearable payment platform for tens of millions of dollars (industry estimates range from $34 million to $40 million);

· Apple acquires Gliimpse;

· Mattel acquires Sproutling;

· Huron Consulting Group acquires MyRounding;

· Philips acquires Wellcentive;

·HCA Acquires Mobile Heartbeat.

In 2017, this situation did not abate but instead intensified, showing a trend of further exacerbation:

· Internet Brands acquires WebMD for $2.8 billion;

· Teladoc acquires Best Doctors for $440 million;

· athenahealth acquires health app developer Praxify for $63 million;

· General Electric acquires Monica Healthcare;

· HIMSS Acquires Health 2.0;

· Apple acquires Beddit;

· Roche acquired mySugr for nearly $100 million (the acquisition valuation of mySugr ranged between $75 million and $100 million);

· Philips acquires mobile health app developer Health&Parenting and cloud-based population health management company VitalHealth;

· Alphabet, Google's parent company, acquires Senosis;

· Livongo acquires Diabeto.

According to a report by MobiHealth News, the number and value of mergers and acquisitions in the digital health sector in 2018, as well as the high-profile nature of the companies involved, were noteworthy:

· Veritas Capital and its subsidiary Elliott acquired athenahealth for $5.5 billion;

·Platinum Equity acquired diabetes-focused technology company LifeScan for $2.1 billion;

· Vista Equity Partners acquired fitness technology company Mindbody for $1.9 billion;

· Amazon acquires PillPack;

· Best Buy acquires GreatCall;

· Roche acquires cancer research company Flatiron Health;

·ResMed acquires Propeller Health, a long-standing key player in the digital health sector.

In the first quarter of 2019, a total of 17 digital M&A transactions were announced. However, as of the end of April, aside from Teladoc Health’s acquisition of MédecinDirect, a medical consulting firm based in Paris, France, no other active major players from within or outside the industry had emerged.

Whether it is comprehensive tech giants such as Apple, Philips, and Amazon, or major companies in the healthcare sector such as Roche and Best Buy, their acquisitions of digital health companies are driven by strategic considerations, albeit with different acquisition targets.

As Best Buy stated after acquiring GreatCall for $800 million, the acquisition was part of a major corporate strategy aimed at introducing new technologies to the rapidly growing senior care market by 2020. Following its acquisition of Flatiron Health, an oncology electronic health record (EHR) software company, Daniel O’Day, CEO of pharmaceutical giant Roche, remarked, “This is a significant step in Roche’s personalized healthcare strategy, as we believe that regulatory-grade real-world evidence is a key factor in accelerating the development and access to novel cancer treatments.” Meanwhile, Amazon, the online marketplace renowned for its “one-click shopping,” acquired PillPack, a pharmacy management company, and prepared to expand its services into broader areas, including prescription drugs.

It is not without reason that giants in both the medical and non-medical sectors are keen on acquiring digital health companies. In fact, since the beginning of the 21st century, most established incumbents in the healthcare sector have gradually achieved scale in marketing. Meanwhile, the rise of internet technologies in the new millennium has introduced variables into the development of the medical industry, posing transformation challenges for large enterprises. As a key manifestation of technological reform within the industry, digital health is expected to be most effective in reducing costs for primary healthcare and hospital management systems, as well as driving product innovation and upgrades. Consequently, mergers and acquisitions of digital health companies have become a preferred strategy for many healthcare giants seeking transformation.

On the other hand, large enterprises outside the healthcare sector possess inherent advantages through their established technical authority and vast consumer bases. Furthermore, as digital technologies—particularly software—become key differentiators in healthcare and the broader medical industry, accelerating acquisitions to keep pace with this trend enables these non-traditional giants to compete effectively with established integrated healthcare providers and capture greater market share.

Therefore, for industry giants, there are several strategic considerations in acquiring digital health companies:

1. Keep pace with emerging industry technologies to ensure that existing business operations do not easily fall behind the market;

2. Directly acquire digital health technologies as a technical reserve or to eliminate potential competitors;

3. Leverage digital health to consolidate and strengthen existing businesses, or establish interwoven relationships with them, to expand market share;

4. Expand product business through digital health and enter new markets;

5. Leverage digital technologies for functional integration to achieve strategic transformation.

Furthermore, although only a handful of major corporations participated in digital health M&A activities in the first quarter of 2019, financing and investment deals in the digital health sector continued to rise. Given the ongoing incursion into the healthcare market by tech giants such as Amazon, Google, Apple, and Microsoft, the momentum of financing, investment, and mergers and acquisitions in digital health is unlikely to wane in the near term.

Compared with the strategic mergers and acquisitions (M&A) undertaken by industry giants, M&A activities within the digital health sector exhibit greater diversity, yet the emerging trends are already evident.

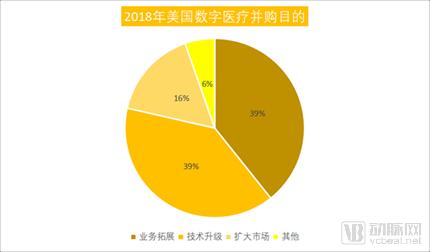

In 2018, the number of mergers and acquisitions (M&A) transactions in the digital health sector reached 56, hitting a multi-year high. The strategic rationales behind these corporate M&A activities varied; however, based on their ultimate objectives, they can be broadly categorized into three directions: technological upgrades, business enhancements, and market expansion. According to statistics, the strategic purposes of these 56 digital health M&A deals are illustrated in the figure below.

Classified, compiled, and charted by VCBeat based on 56 digital health M&A transactions in 2018

In 2018, the strategic objectives of digital health mergers and acquisitions (M&A) can be categorized into four major groups: business expansion, technological upgrading, market expansion, and other purposes (M&A strategies that are temporarily difficult to classify). VCBeat (WeChat Official Account: vcbeat) found during its compilation of M&A transactions that most small and medium-sized enterprises and startups in the digital health sector aim to achieve business expansion and technological upgrading through M&A. Only a small proportion of companies have the intention of expanding their market share, accounting for 16%. Another 6% of digital health companies have acquisition objectives distinct from the above categories; their acquisition criteria are mostly related to the specific nature of their own businesses. For instance, Prima-Temp, a technology company providing precise core body temperature measurement, acquired Kindara, a manufacturer of Wink Bluetooth-connected fertility thermometers, to consolidate its position in the digital women’s health market.

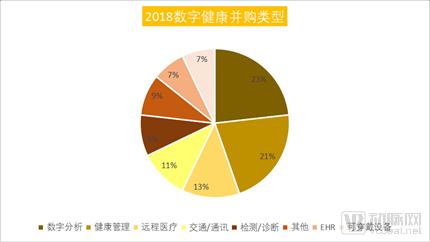

On the other hand, digital health M&A activities in 2018 showed a clear preference for specific subsectors. The breakdown of M&A types is shown in the figure below.

Classified, organized, and charted by VCBeat based on 56 digital health M&A transactions in 2018

According to statistics, digital health M&A activities in 2018 can be broadly categorized into seven major types: testing/diagnostics, EHR (Electronic Health Records), digital analytics, healthcare transportation/communications, wearable devices, online health management, and telemedicine. Additionally, a few M&A transactions were classified as “Other” due to their unique characteristics, which made them difficult to categorize.

Among these, the hottest M&A topic in 2018 was medical data analytics (digital analytics), accounting for 23% of total M&A transactions; this was closely followed by online health management platforms, which made up 21%; telemedicine and healthcare transportation/communications were nearly tied, representing 11% and 13%, respectively; while the remaining categories—wearable devices, testing/diagnostics, and EHRs—were also comparable. Other classifications included cases that are not yet easily categorized, such as those further enhancing the value of the digital health market.

Notably, this trend aligns with the digital health investment and financing trends observed in 2018. According to Mercom’s report, the majority of venture capital in the healthcare capital market in 2018 flowed into companies specializing in medical data analytics, followed by wearable devices, mobile health applications, practice management solutions, and mobile wireless companies.

Rock Health also released a similar report on digital health funding, which predicts that the digital health sector will see increased mergers and acquisitions in the coming years. The report attributes this trend to large digital health companies seeking to expand their portfolios through talent acquisitions, discounted sales, and business integration.

As of now, with the first quarter of 2019 having passed, mergers and acquisitions in the digital health sector have not shown a surge.

In February, there were five M&A deals in the digital health sector:

·Crossover Health acquires asynchronous telehealth company Sherpaa;

· Health insurer Guidewell Connect acquires health tech platform Onlife Health;

· WellSky (Mediware) Acquires Health Care Software;

· Interoperable healthcare IT company Medsphere Systems Corporation acquires Wellsoft, a specialist in ED information systems;

· Livongo acquires MyStrength; PerfectServe acquires two AI-related projects.

Mergers and acquisitions continued in March and April:

·On March 6, PointClickCare, a health technology company focused on the elderly population, acquired QuickMar, a manufacturer of post-emergency care management systems;

· On March 8, medical device/software company Zoll Medical acquired medical record management company Golden Hour;

·On March 19, Teladoc Health acquired MédecinDirect to solidify its foothold in the French market;

· On April 4, Femtech company Advantia Health acquired Pacify, a video chat platform for mothers and infants.

In summary, M&A activity in digital health continues to revolve around technological upgrades, business expansion, and market strategy, with data analytics technology standing out among various digital health solutions and rapidly becoming a new favorite of investors.

The number of digital health M&A transactions grew from a total of 40 in 2016 to 56 in 2018, with 19 deals completed in the first quarter of 2019 alone, demonstrating surprising activity in the capital markets. However, viewed against a broader strategic backdrop, such M&A activity is not unexpected. Within the broader healthcare industry, digital health M&A shares similarities with merger and acquisition activities in the pharmaceutical and medical device sectors. Outside the healthcare industry, such M&A behavior is no different from that seen in other acquisition-driven sectors such as telecommunications, media, and energy.

The following factors are driving M&A in digital health.

One is the prerequisite for the wave of digital health M&A, namely, a favorable economic and capital environment.

A review of U.S. merger and acquisition (M&A) history since the 20th century reveals that all M&A peaks have occurred during periods of economic expansion, such as post-war recoveries or the advent of the “New Economy,” without exception. It is reported that the U.S. economy remained sluggish in the aftermath of the 2008 financial crisis but entered the longest economic expansion cycle in its history under the policy maneuvers of the new administration inaugurated in 2016. According to JPMorgan Chase statistics, this round of U.S. economic expansion has lasted for 108 months, ranking second in historical terms and demonstrating strong growth momentum.

Moreover, OECD leading indicators show that since 2016, the U.S. economy has stabilized and improved, exhibiting a recovery trend. The unemployment rate has gradually declined from its peak of 10% during the financial crisis to below the natural rate of unemployment, the PMI has remained above the boom-bust threshold for consecutive months, and the CPI has operated within a reasonable range. Buoyed by the stabilization and improvement of the economy, the U.S. stock market has experienced a magnificent bull run lasting more than 3,452 days, making it the longest bull market in history and delivering an exuberant capital feast for investors.

Consumer-centric digital health companies attracted the most venture capital investment in 2018, with a total of 447 deals accounting for 55% of the total funding; companies focused on practice management accounted for the remaining 45%, with 251 deals raising $4.3 billion. In addition, two companies had IPOs totaling $1.23 billion in 2018.

All of this has further fueled the wave of mergers and acquisitions in the digital health industry, one of the many specialized sectors.

Second, the intrinsic driver of the M&A wave is industrial transformation.

The demand for industrial transformation and upgrading in the healthcare sector is the primary internal driver behind mergers, acquisitions, and restructuring in digital health.

On the one hand, for many large-scale digital health companies, mergers and acquisitions (M&A) and integration constitute a key strategic approach to reshaping their business operations. For the healthcare industry as a whole, M&A is also an important pathway to enhancing industrial efficiency and achieving industrial upgrading. The current wave of digital health M&A has emerged largely to address the long-standing inefficiencies in the traditional healthcare sector. Previously, many U.S. digital health companies were founded on technological innovations such as cloud computing and artificial intelligence (AI), with their product commercialization and business models still in the exploratory phase. M&A enables these companies to expand their scale, thereby improving corporate performance.

On the other hand, the emergence of new technologies has also fueled merger and acquisition (M&A) activities. Traditional industries have sought transformation and upgrading by acquiring new technologies and entering new sectors through M&A, a trend particularly evident among established medical device and pharmaceutical giants such as Medtronic and Johnson & Johnson. The wave of digital health M&A, which has been active since 2016, coincides with the advent of a new industrial revolution centered on internet technology, information technology (IT), and biotechnology. The emergence and maturation of big data in the healthcare sector have necessitated significant structural adjustments and upgrades across the industry, thereby driving a series of M&A transactions focused on digital technologies.

Third, policies and laws related to the broader health sector directly influence the rise and fall of the wave of digital health M&A, as well as the types of mergers and acquisitions.

Despite the stark contrast with China’s robust policy-driven business environment, the United States’ highly competitive market limits the impact of government policies. However, due to the prolonged slump in the healthcare industry since the implementation of the Affordable Care Act in 2010, the healthcare market’s backlash against new policies has been more intense than ever before.

Following the U.S. government’s launch of telemedicine initiatives, the tax reform passed in late 2017 struck while the iron was hot, slashing the corporate tax rate from 35% to 15% and quickly invigorating merger and acquisition activity across industries.

According to the aforementioned statistics, the hot acquisition targets in the record-breaking year for mergers and acquisitions were medical data analytics, online health management, and telemedicine. These sectors all aligned with the core directive of the new healthcare reform—affordable care aimed at “reducing healthcare costs.” In this light, it is highly likely that the Republican Party will leverage digital health as a key instrument to control healthcare costs and improve care quality during its efforts to reform and advance the U.S. healthcare industry over the next 4–8 years. Therefore, in the forthcoming development of healthcare, emerging telemedicine technology companies such as MORE Health, which possess top-tier medical resources and advanced medical technologies, will become a critically important component in enhancing the quality of healthcare for the entire population.

Despite the continuous growth in the value of digital health and the surge in financing, investment, and M&A transactions, the market implementation of various products has been less than satisfactory. Recently, a health affairs study focusing on 20 top U.S. digital health companies detailed that there is little evidence to suggest that digital health tools have had a positive impact on patients with high-burden health conditions such as heart disease, diabetes, and depression. Furthermore, although capital has largely flowed toward data analytics companies, only a few have produced tangible research outcomes.

This may explain the slowdown in digital health M&A activity in the first quarter of 2019. According to Rock Health, only 21 startups in the digital health sector were acquired in Q1 2019, representing a 32% decline from the quarterly average of 31 acquisitions observed between 2016 and 2018.

Not only that, 2019 will also be a year when digital health innovators are held accountable for delivering tangible results. Pressure from consumer demand and the policy and regulatory environment will become the main drivers for strengthening accountability. At the same time, policymakers will more actively explore policy changes to accelerate product time-to-market, thereby increasing patient access, improving healthcare efficiency, reducing provider burden, and creating new pathways for non-hospital-based medical services.

In this context, in the coming year, digital health innovators will need to demonstrate how technology can enhance access to healthcare services and narrow gaps in care and coverage, rather than simply bringing a digital tool to market through mergers and acquisitions.

Nevertheless, valuations of digital health companies continued to climb in 2019. Among the digital health firms that completed mergers and acquisitions in the first quarter, Livongo and Health Catalyst each achieved valuations exceeding $1 billion and were preparing for initial public offerings (IPOs) to break the three-year stalemate in the IPO market. The digital health sector is poised for significant developments this year; where will the new wave of IPOs lead? Stay tuned for VCBeat’s article, “[A Three-Year Review of Digital Health, Part II] A New Wave of IPOs Is Coming: Why These Companies Broke the Listing Stalemate,” to be released on May 28 (WeChat official account: vcbeat).