Digital Health IPO Surge: Why These Companies Broke the Listing Drought

SmileDirectClub

Orthodontic Service Provider

Health Catalyst

Medical Data Development Service Company

Livongo

Chronic Disease Management Service Provider

Ancestry

Ancestry.com LLC

In【Three-Year Review of Digital Health: Part I】VCBeat (WeChat Official Account: vcbeat) has examined the context and key industry milestones of digital health M&A transactions over the past three years from the perspective of corporate mergers and acquisitions.This article continues to focus on the digital health sector, using four soon-to-be-listed digital health companies as case studies to explore the reasons behind their successful breakthroughs and to interpret future development trends in the industry.

Readers following this sector will have noticed that while valuations of digital health companies have soared in recent years, their performance in the primary market has been lackluster. For three consecutive years, not a single digital health company went public. The last IPO in the digital health space dates back to 2016, when cardiac monitoring firm iRhythm rang the opening bell.

Recently, as numerous high-tech companies such as Uber, Lyft, and Zoom have raced to go public, startups in the digital health sector have also begun appearing frequently in the IPO news section of The Wall Street Journal. According to reports, at least four digital health technology companies, with a combined valuation of approximately $7.6 billion, are preparing for initial public offerings this year.

Among companies planning to go public:

Livongo, a Diabetes Monitoring and Management Company, headquartered in California, has hired Morgan Stanley, Goldman Sachs, and JPMorgan Chase to underwrite its initial public offering, with an expected valuation of over $1 billion. Livongo was founded in 2014 and raised $240 million in six previous funding rounds, with investors including Kinnevik AB and General Catalyst.

Health Catalyst, a medical data management and analytics company, headquartered in Utah, has hired Goldman Sachs and JPMorgan Chase to underwrite its initial public offering. The company is currently valued at approximately $1 billion and plans to raise $150 million to $200 million in the IPO. Founded in 2008, Health Catalyst raised a total of $392 million across nine previous funding rounds, with investors including OrbiMed Advisors, Sequoia Capital, and Norwest Venture Partners.

Personal DNA Sequencing Company Ancestry, headquartered in Utah, was valued at $2.6 billion in 2016. The company was founded in 1989 and went public in 2009, raising approximately $100 million. In 2012, Ancestry was taken private by the private equity firm Permira Advisers for $1.6 billion.

SmileDirectClub (SDC), a Teledentistry Company, headquartered in Tennessee, has hired JPMorgan Chase to underwrite its initial public offering and is currently valued at approximately $3.2 billion. SDC was founded in 2014 and raised nearly $400 million in two previous funding rounds, with investors including Clayton, Dubilier & Rice, Spark Capital, and Kleiner Perkins.

For the securities trading market, the four companies’ preparations for initial public offerings epitomize the digital health sector’s resurgence after a period of dormancy.

VCBeat (WeChat Official Account: vcbeat) will first summarizeRecent Development Trends in the Digital Health Capital Market; then focus on analyzing the four companies'Competitive Advantage, to clarify the reasons behind their ability to break the deadlock and achieve a successful breakout; finally, we present selected comments from Wall Street’s star investors on this wave of IPO frenzy for our readers’ enjoyment.

The news that digital health unicorns are successively preparing for initial public offerings (IPOs) reflects, at a macro level, certain changes in the market and industry landscape. As mentioned in the previous article, the frequency of mergers and acquisitions (M&A) in the digital health sector has gradually slowed down since 2019. Considering the trends in financing and investment transactions since last year,VCBeat believes:In 2019, the “capital frenzy” in the digital health sector gradually subsided, as the market shifted toward a new era characterized by industry segmentation and the increasing prominence of leading players.

At the beginning of the year, VCBeat noted in its article “Review of 2018 Global Digital Health Investment Deals: Total Funding Reached $9.5 Billion as Investment Became More Rational” that global venture capital firms invested a record-breaking $9.5 billion in digital health in 2018. However, the slight annual decline in the number of transactions indicated that investors had begun to place greater emphasis on leading companies in the digital health sector and emerging enterprises with significant growth potential.

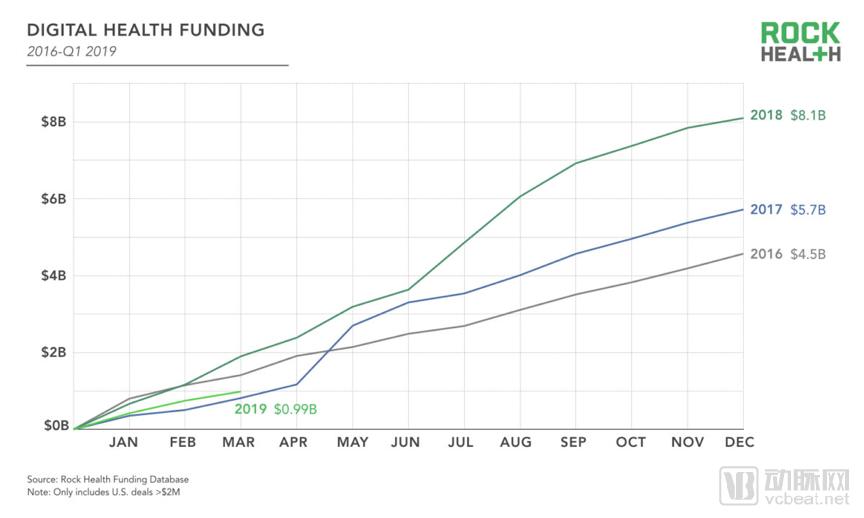

Source: Rock Health Official Website

According to Rock Health’s Q1 2019 financing and investment report, there were a total of 61 deals in the digital health sector in the first quarter of 2019, with total funding amounting to only $986 million—just half of the figure recorded in Q1 2018. The average quarterly funding over the previous two years stood at $1.4 billion. Despite the sub-$1 billion total, several large-scale financing rounds occurred, including Calm’s $88 million Series B round and Health Catalyst’s $100 million Series F round. Both companies have achieved unicorn status with valuations exceeding $1 billion.

Based on the above data, we have distilled two key insights:

Total financing in 2018 reached a historic high, yet the number of financing deals declined significantly.

Total financing in Q1 2019 declined significantly, yet digital health companies experienced a peak in IPOs.

In fact, underlying these two seemingly contradictory sets of investment and financing data is a fundamental investment logic. As the digital health market matures further, the Matthew effect in capital flows has begun to emerge. The decline in the frequency of digital health investment deals, coupled with the clustered IPOs of industry unicorns, indicates that capital is gradually shifting from scattered allocations toward a select few companies with core competencies. After being tempered by market and industry forces, companies that rely solely on business model innovation and possess high replicability may struggle to survive, whereas enterprises that can articulate a compelling narrative and possess core technologies will attract greater favor from investors.

What enabled these four companies, each operating in a different niche, to stand out amidst the financing and investment transactions in the digital health sector over the past three years?

These four companies share commonalities in two major areas. On one hand, among themAll three companies possess telemedicine attributes.They have developed products that improve healthcare accessibility, which corroborates the trend toward home-based healthcare. On the other hand,Three companies have also launched direct-to-consumer products., and reduced individual healthcare costs, reflecting the consumer-centric direction of healthcare reform.

VCBeat will also fromBusiness Features, Customer Base, Financial Performance, and Competitor ComparisonAnalyze the unique competitive advantages of these four companies from dimensions such as...

Livongo, a Diabetes Monitoring and Management Company

Livongo is a leader in the field of mobile chronic disease management, dedicated to empowering patients with chronic conditions to achieve a better quality of life.

To reduce the healthcare costs associated with diabetes management, Livongo currently offers consumers a comprehensive, one-stop diabetes management service that integrates FDA-cleared two-way interactive blood glucose meters, a mobile app, cloud-based analytics, and a real-time coaching team. This innovative diabetes management system combines mobile technology with behavioral coaching to provide users with blood glucose data collection and tracking, as well as on-demand expert guidance. This empowers patients with diabetes and their families to gain a better understanding of the condition and identify treatment plans tailored to their individual needs.

Livongo partners with more than 650 organizations, including Fortune 500 insurers, innovative health systems, five of the seven largest health insurance plans, and the two largest pharmacy benefit management (PBM) companies.

It is reported that the company is expected to generate at least $100 million in revenue this year from over 120,000 patients, with next year’s revenue projected to double from this year’s level.

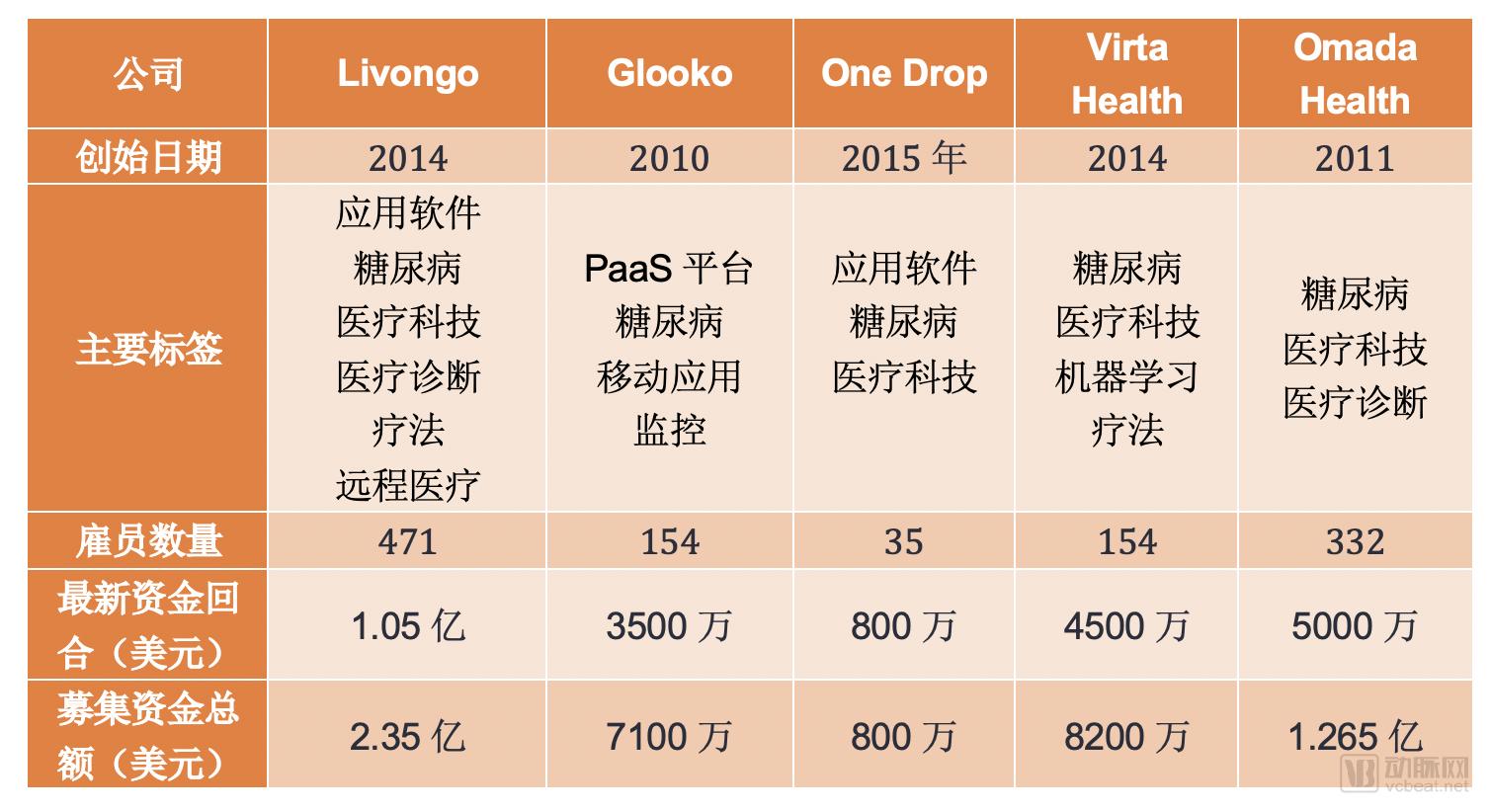

According to CB Insights, Livongo has approximately 16 competitors in this vertical sector. VCBeat has selected the four most outstanding companies among them for a general comparison.

Source: Compiled based on Craft and public data

We can observe that, although the five digital health companies depicted in the figure above all focus on diabetes management, regardless of whether it is fromin terms of business and technological coverage, number of employees, or amount of financing raised,Livongo Outperforms. Additionally, according to The Wall Street Journal, although venture capital firms are racing to invest in major diabetes management companies, none of the companies’Revenue and User BaseCapable of rivaling Livongo. Given the diabetes market’s nearly RMB 100 billion size, it is hardly surprising that Livongo, as a leading player in this sector, was able to go public first.

Medical Data Management and Analytics Company Health Catalyst

Health Catalyst is a U.S. healthcare data management and analytics services company., the company initially focused on creating databases for clinics and hospitals, and later launched mature predictive analytics software with predictive analysis capabilities, further improving the operational efficiency of healthcare systems, reducing waste of health resources, and promoting the standardization of medical processes.

Currently, technologies that leverage machine learning and predictive analytics to improve the healthcare industry are typically in the hands of artificial intelligence experts.Meanwhile, the company’s open-source predictive analytics software, Healthcare.ai, has lowered the barrier to applying machine learning techniques in medical practice.The software can convert patients’ medical and genetic information, billing systems, customer surveys, and laboratory data into user-friendly formats, enabling healthcare professionals with only basic computer skills—but who are interested in leveraging new technologies to improve healthcare—to use the software with ease.

Health Catalyst continues to excel in customer acquisition, with its software used by over 500 hospitals and 5,000 clinics to manage data for approximately 100 million individuals. OSF HealthCare has leveraged the company’s algorithms to identify patients at risk of readmission.

This technology saves OSF at least $2 million annually in labor costs, significantly reducing the time healthcare professionals spend on patient assessments.

In 2018, Health Catalyst’s annual recurring revenue increased by more than 65% year-over-year, total revenue grew by over 50%, and gross profit rose by 80%. Driven by this strong performance, the company was included in Deloitte’s 2018 Global Technology Fast 500 list of the fastest-growing technology companies.

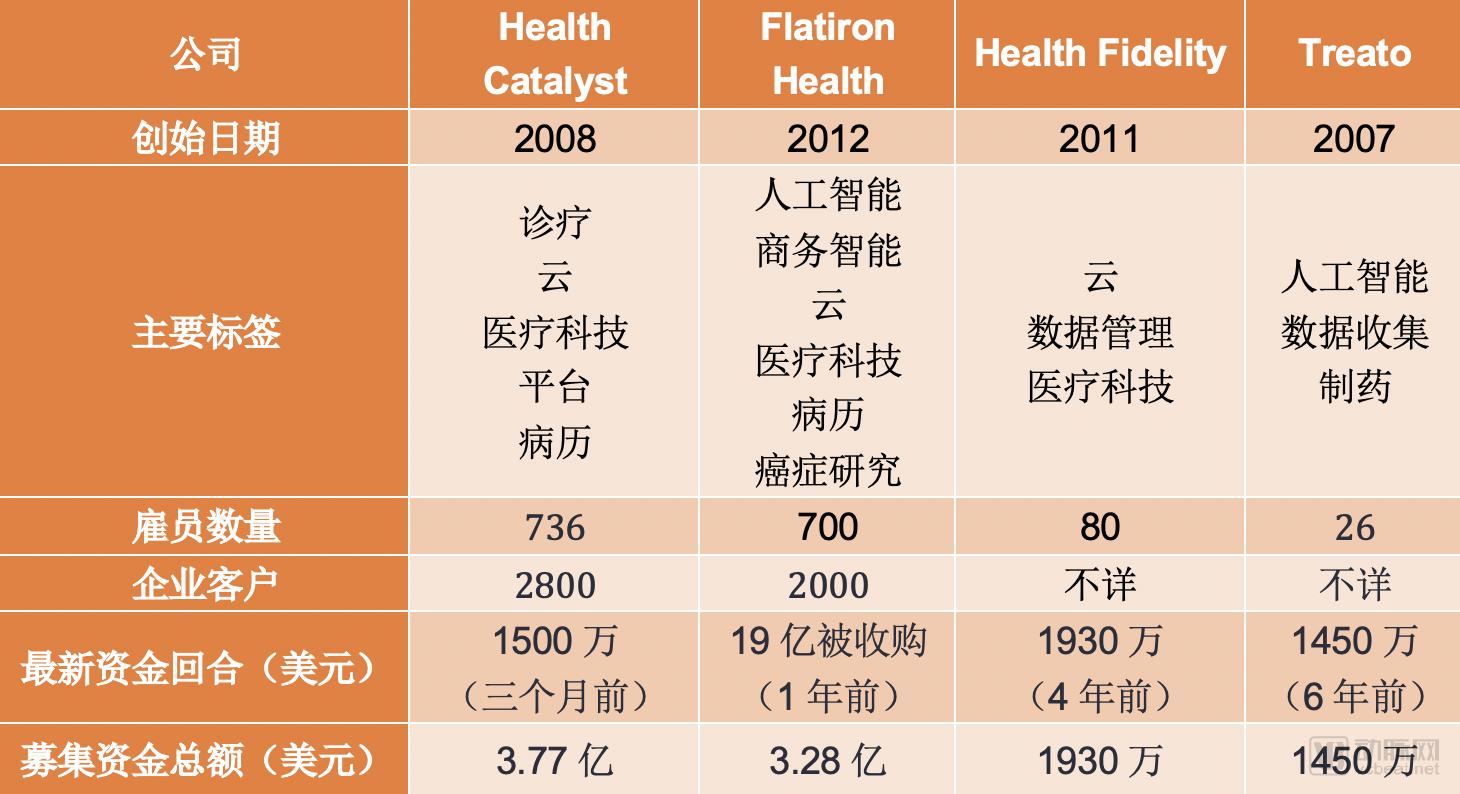

Health Catalyst competes with several healthcare technology giants, such as IBM Watson and Optum. Furthermore, according to CB Insights data, Health Catalyst has five peer competitors in this vertical sector, two of which are smaller in scale and not included in the listing.

Source: Compiled based on Craft and public data

Data shows that although Health Fidelity and Treato were established earlier, their competitiveness is significantly lacking. The primary competitor of Health Catalyst is likely Flatiron Health.Although based on the same technology, the two companies have slightly different strategic positioning.Flatiron Health, an electronic health record company focused on oncology, has built a platform for analyzing real-world data from cancer patients to accelerate cancer research; the company has been acquired by Roche. In contrast, Health Catalyst currently focuses on leveraging artificial intelligence and machine learning to help healthcare providers improve medical systems. As such, Health Catalyst has established a unique competitive advantage in this field, backed by its substantial customer base and strong performance. We believe that the company’s initial public offering will create further opportunities.

Personal DNA Sequencing Company—Ancestry.com

Ancestry.com has a history of nearly 30 years, having gone through stages from fundraising and going public to being acquired, and is already a leading player in the DNA sequencing company sector.

Ancestry.com currently allows users to maintain online family trees to track their family history.Users can now use AncestryHealth for free, adding health information to their family trees to track chronic diseases and lifestyle choices affecting each family member. The website then uses algorithms to reveal the hidden health insights within this data. Users can print out their family health history to discuss with their doctors. The company is also exploring the integration of electronic health records to help users share data more directly with their physicians.

2017 was the last year the company publicly reported its financial performance, with sales reaching $1 billion. In 2018, industry estimates indicated that the number of consumers using direct-to-consumer (DTC) DNA tests nearly tripled, exceeding 12 million. Of these consumers, 7 million used Ancestry, compared to just 3 million in 2017.

The company’s primary competitor is the publicly listed 23andMe Inc., and Ancestry has surpassed this rival in sales volume.As of November 2018, Ancestry had sold 14 million DNA kits globally, while 23andMe’s sales reached only 10 million by April 2019.

Teledentistry Company—SmileDirectClub

SmileDirectClub is a direct-to-consumer orthodontics company.

In terms of business model innovation, SmileDirectClub has truly put the concept of telemedicine into practice in the field of dental care, allowing consumers to complete the entire orthodontic treatment process through a digital online platform.Users can create dental impressions (i.e., take molds) at home and mail them to SmileDirectClub, or undergo dental scanning at offline SmileShops. The company then ships the clear aligners directly to users, while authorized dental professionals remotely monitor their orthodontic progress. These experts are available 23 hours a day via phone, email, chat, or social media to address any customer inquiries.

This company, founded just four years ago, has already provided teeth cleaning and orthodontic services to over 500,000 customers. To date, official data from SmileDirectClub shows that it has captured 95% of the at-home clear aligner market share, employed more than 3,200 staff, and opened over 150 retail stores across China. The company projects its 2019 revenue will reach $1 billion.

SmileDirectClub’s primary competitor was Invisalign, a brand under Align Technology, a traditional orthodontics company that has served more than 5.8 million patients to date. Its clear aligners account for over 80% of the market share. The emergence of SmileDirectClub’s direct-to-consumer oral care model dealt a significant blow to Invisalign. Invisalign previously sued SmileDirectClub over patent disputes, but less than a year later, the two companies reached a partnership agreement: Invisalign invested $46.7 million to acquire a 17% stake in SmileDirectClub and became the exclusive supplier for certain clear aligner products.

It is evident that SmileDirectClub’s innovative business model is disrupting traditional oral care practices. This highly appealing consumer product not only offers a price advantage but also eliminates the hassle of frequent hospital visits for patients. Essentially, enhanced accessibility to healthcare and reduced costs are the primary factors enabling the company to capture market share and achieve success in a short period.

Overall, these four companies have earned the trust of the capital markets by leveraging strong market growth momentum, along with their distinctive commercial advantages, extensive customer base, and outstanding performance.Their public listings signal the emergence of a new wave of digital health leaders, who are gradually distinguishing themselves in this sector.

However, other digital health companies will face greater challenges in breaking through.Coupled with an increasingly stable competitive landscape and more stringent investment criteria, digital health companies must focus more on refining their products and services, enhancing their core competitiveness, and accurately positioning themselves to establish a competitive edge. Only then can they emerge as dark horses in the digital health sector.

Star investors on Wall Street have shared their insights on the recent IPOs of these companies. VCBeat has selected and compiled some of their most notable comments for readers’ reference.

“Digital health companies will usher in a second wave of IPOs.”

—Jorge Conde, Partner at Andreessen Horowitz’s Biotechnology Investment Division

“These soon-to-be-public digital health companies are poised to lead the second wave of digital health IPOs. Companies in the earlier first wave often focused on building core infrastructure for digital healthcare systems, such as electronic health records, with their resulting products sometimes being merely applications. Consequently, with few exceptions (such as Epic and Cerner), most of these companies failed to identify suitable opportunities for business expansion.”

Currently, this situation has begun to change. We are starting to see some companies break away from single-business models and move toward diversification. For companies like Livongo or SmileDirectClub, they are no longer offering standalone software but rather providing technology solutions that can be utilized across the entire healthcare system, laying the foundation for them to become truly large-scale enterprises.

“Long-term success requires a robust business model.”

—Graham Brown, Partner at Lerer Hippeau

“While an initial public offering may have a transformative impact on digital health companies, long-term success requires them to have well-established business models. SmileDirectClub’s business model caters to consumer needs and features a unique profit model.”

“Different IPO Projects: Digital Health Prioritizes Transformation, While Biotechnology Focuses on Fundraising.”

—Krishna Yeshwant, Partner at Google Ventures

“Many of the biotechnology companies we have invested in, including Gritstone Oncology, Alector, and Magenta Therapeutics, have gone public in recent years. Unlike the digital health market, the IPO window for biotechnology companies has been open for some time.”

The public listings in the digital health sector reflect, to some extent, significant corporate transformations; whereas IPOs by biotechnology companies are more akin to a means of raising additional capital and do not necessarily indicate a qualitative shift in their development. Although investing in health IT companies is a sound strategy, the ultimate survival of digital health firms post-IPO will depend on each company’s performance and prospects.